Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Core & Main Inc (NYSE:CNM) reported its fiscal second quarter 2025 results on September 9, showing solid sales growth but lowering its full-year outlook. The water infrastructure distributor’s stock dropped 8.45% in premarket trading to $60.96, reflecting investor concerns about the reduced guidance despite quarterly performance that exceeded expectations in several key metrics.

The company’s presentation revealed a 7% increase in net sales year-over-year, driven by strength in municipal demand and stability in non-residential markets, which helped offset softer residential lot development demand. However, Core & Main reduced its full-year adjusted EBITDA guidance, citing current market conditions and higher operating expenses.

Quarterly Performance Highlights

Core & Main delivered strong financial results for Q2 2025, with notable improvements across most key metrics compared to the same period last year.

"We saw solid sales growth supported by balanced end markets and the execution of our product, customer, and geographic expansion initiatives," said Mark Witkowski, Chief Executive Officer, according to the presentation materials.

The company reported significant year-over-year improvements in revenue and profitability metrics:

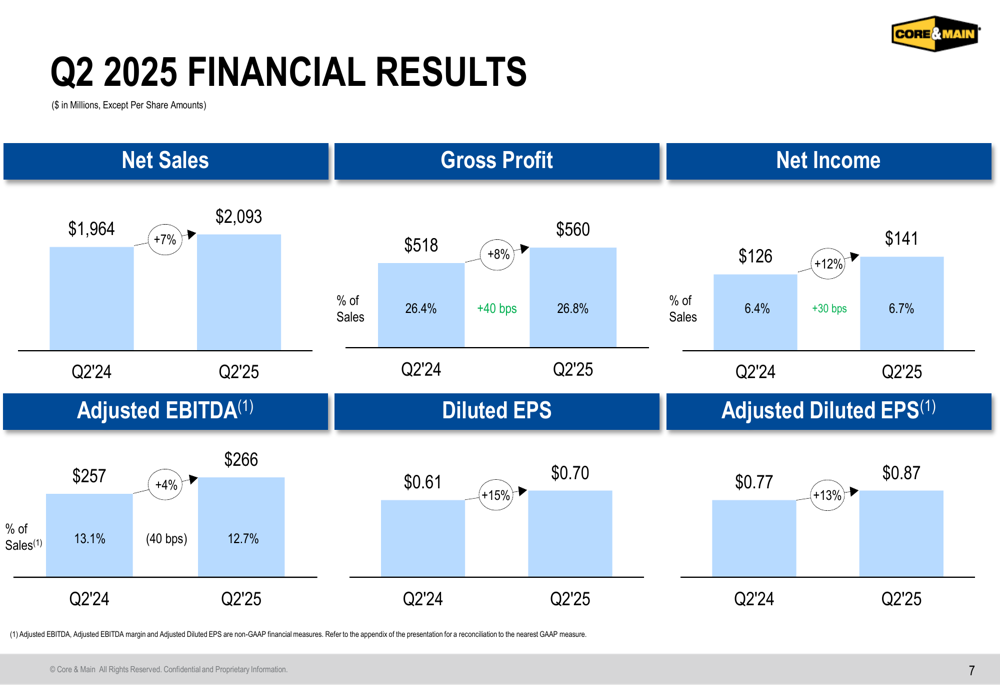

As shown in the following chart of quarterly financial results:

Net sales increased 7% to $2,093 million, up from $1,964 million in Q2 2024. Gross profit rose 8% to $560 million with gross margin expanding 40 basis points to 26.8%. Net income grew 12% to $141 million, with net income margin improving 30 basis points to 6.7%.

Diluted earnings per share increased 15% to $0.70, while adjusted diluted EPS rose 13% to $0.87. Adjusted EBITDA grew 4% to $266 million, though adjusted EBITDA margin contracted 40 basis points to 12.7%.

During the quarter, Core & Main continued its expansion by opening new locations in Kansas City, Kansas and Columbus, Wisconsin. The company also announced the acquisition of Canada Waterworks on September 2, 2025, furthering its inorganic growth strategy.

Detailed Financial Analysis

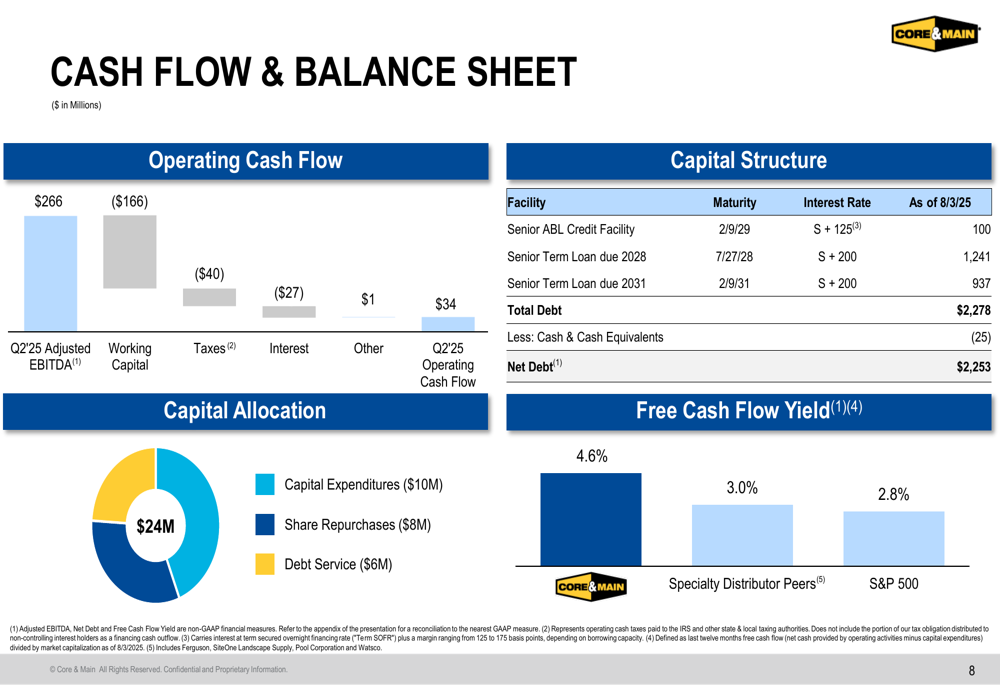

Core & Main’s cash flow and balance sheet position remained solid, though operating cash flow for Q2 2025 was $34 million, reflecting typical seasonal patterns in the business.

The company’s capital structure and cash flow allocation are illustrated in the following chart:

As of August 3, 2025, Core & Main reported total debt of $2,278 million, consisting of a $100 million Senior ABL Credit Facility due February 2029, a $1,241 million Senior Term Loan due July 2028, and a $937 million Senior Term Loan due February 2031. With cash and cash equivalents of $25 million, net debt stood at $2,253 million.

The company’s free cash flow yield of 4.6% outperforms both specialty distributor peers (3.0%) and the S&P 500 (2.8%), highlighting Core & Main’s strong cash generation capabilities relative to its industry and the broader market.

Capital allocation during the quarter included $10 million for capital expenditures, $8 million for share repurchases, and $6 million for debt service, demonstrating the company’s balanced approach to deploying capital across growth initiatives and shareholder returns.

Forward-Looking Statements

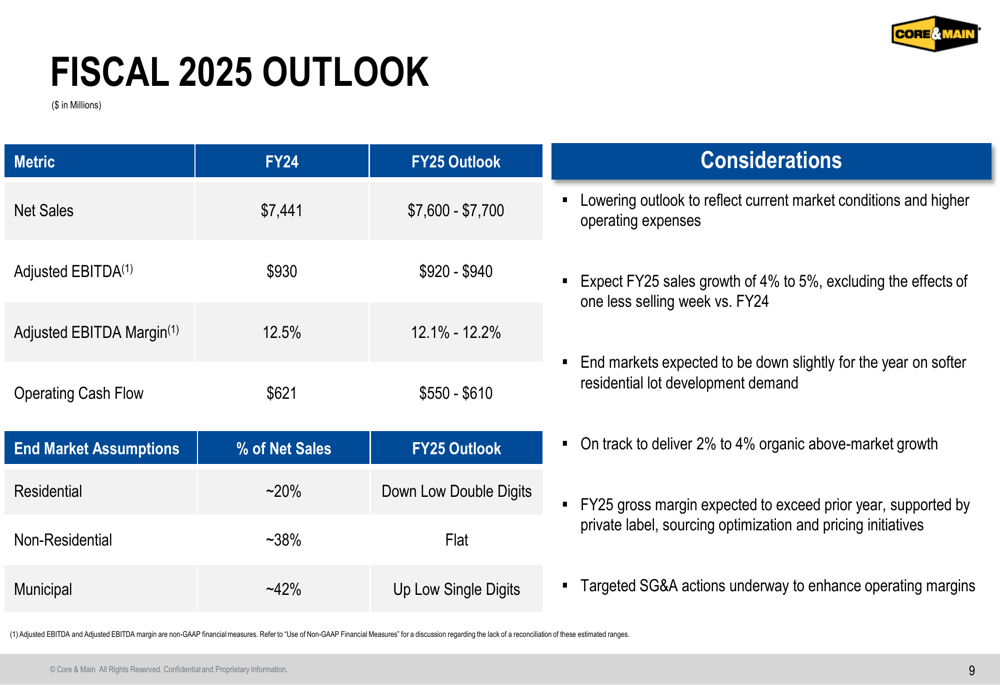

Core & Main revised its fiscal 2025 outlook downward, which likely contributed to the negative premarket stock reaction:

As shown in the following guidance table:

The company now projects net sales of $7,600-$7,700 million for fiscal 2025, compared to $7,441 million in FY24. This represents a reduction from the previous guidance of $7,600-$7,800 million provided during Q1 results.

More significantly, adjusted EBITDA is now expected to be $920-$940 million, down from the previous guidance of $950-$1,000 million. Adjusted EBITDA margin is projected at 12.1%-12.2%, compared to 12.5% in FY24.

Operating cash flow is forecast at $550-$610 million, versus $621 million in the previous fiscal year.

The outlook revision reflects current market conditions and higher operating expenses, though the company still expects 4%-5% sales growth for FY25 (excluding the effects of one less selling week). End markets are expected to be down slightly due to softer residential lot development demand, with residential markets (approximately 20% of net sales) projected to decline by low double digits. Non-residential markets (38% of net sales) are expected to remain flat, while municipal markets (42% of net sales) are forecast to grow by low single digits.

Strategic Initiatives

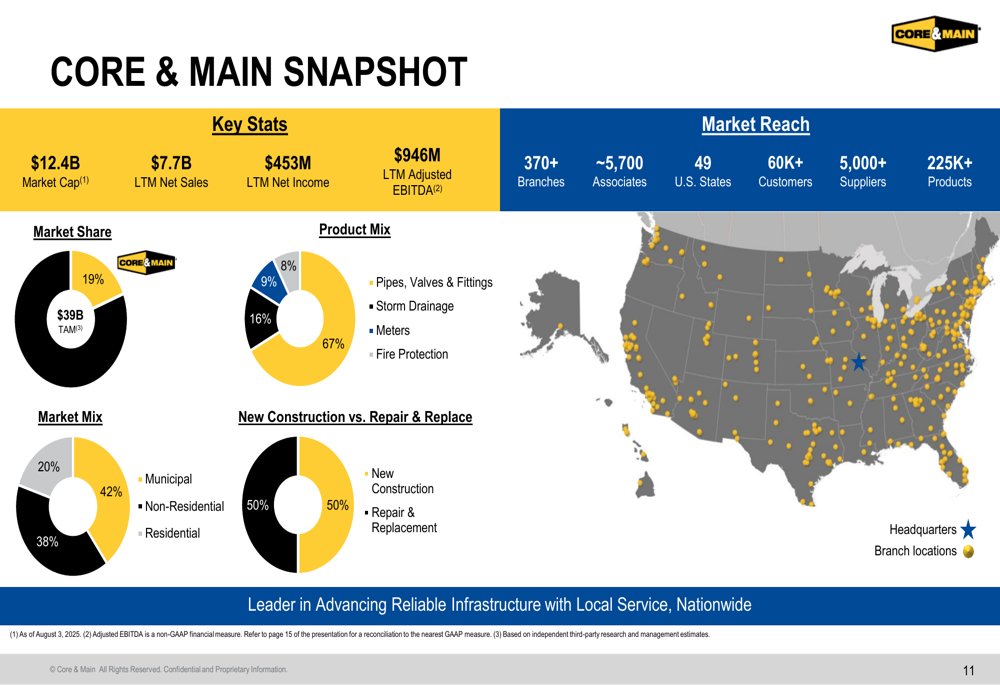

Despite the near-term challenges, Core & Main continues to execute on its long-term strategic initiatives and value creation targets. The company maintains a strong market position with 19% share of a $39 billion total addressable market.

The following snapshot provides an overview of Core & Main’s market presence:

With 370+ branches across 49 U.S. states, approximately 5,700 associates, and relationships with over 60,000 customers and 5,000 suppliers, Core & Main has established itself as a leading distributor in the water infrastructure space. The company’s product mix is dominated by pipes, valves, and fittings (67%), followed by storm drainage (16%), meters (9%), and fire protection (8%).

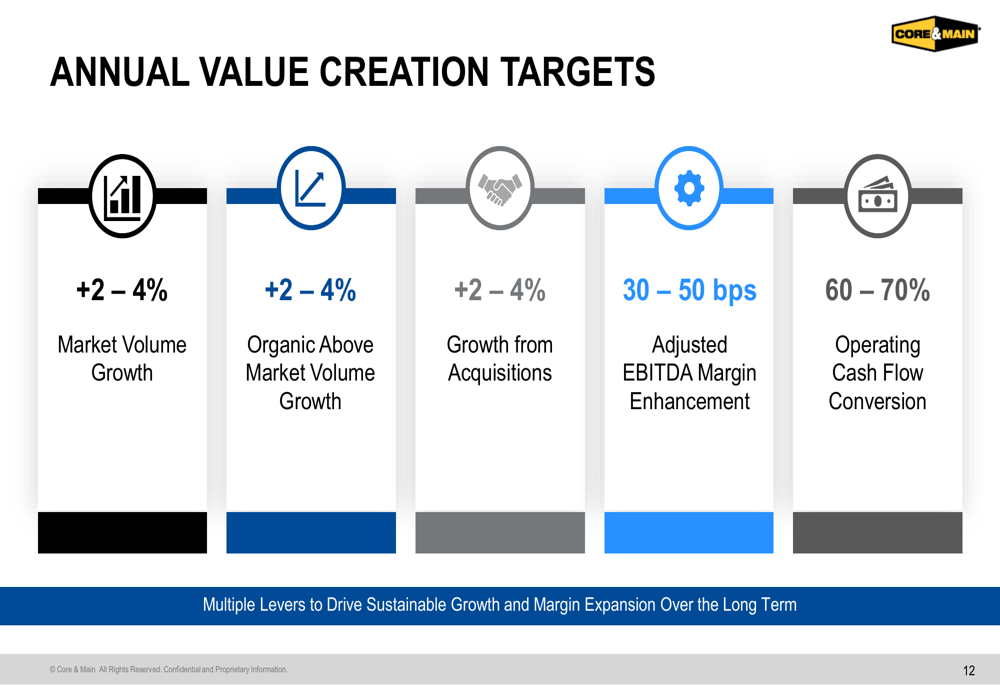

Core & Main’s annual value creation targets highlight its long-term growth strategy:

The company aims to achieve 2%-4% market volume growth, complemented by 2%-4% organic above-market volume growth and an additional 2%-4% growth from acquisitions. Core & Main also targets annual adjusted EBITDA margin enhancement of 30-50 basis points and operating cash flow conversion of 60%-70%.

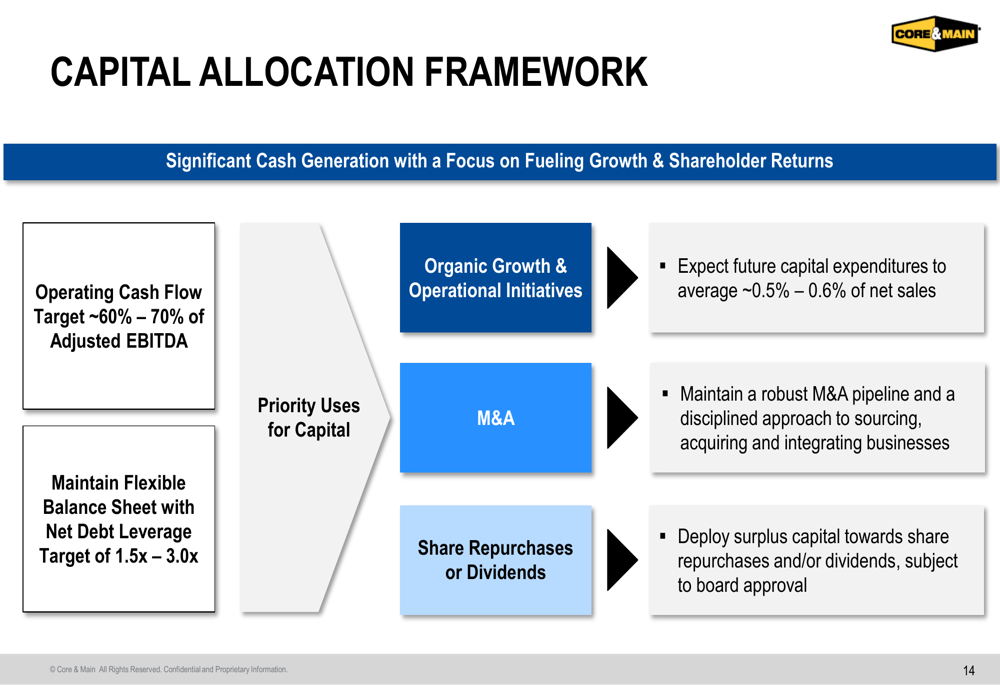

The company’s capital allocation framework emphasizes its focus on growth and shareholder returns:

Core & Main maintains a flexible balance sheet with a net debt leverage target of 1.5x-3.0x. Priority uses for capital include organic growth and operational initiatives, with future capital expenditures expected to average 0.5%-0.6% of net sales; mergers and acquisitions, with a disciplined approach to sourcing, acquiring, and integrating businesses; and share repurchases or dividends to deploy surplus capital, subject to board approval.

While the revised guidance suggests some near-term headwinds, Core & Main’s diversified end-market exposure and balanced approach to growth position it to navigate current market conditions while continuing to execute on its long-term strategic objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.