Figma Shares Indicated To Open $105/$110

Corning Incorporated (NYSE:GLW) reported strong second-quarter 2025 results on July 29, exceeding analyst expectations with significant growth in its Optical Communications segment and progress on its Springboard strategic plan. The company’s stock jumped 6.48% in premarket trading following the announcement.

Quarterly Performance Highlights

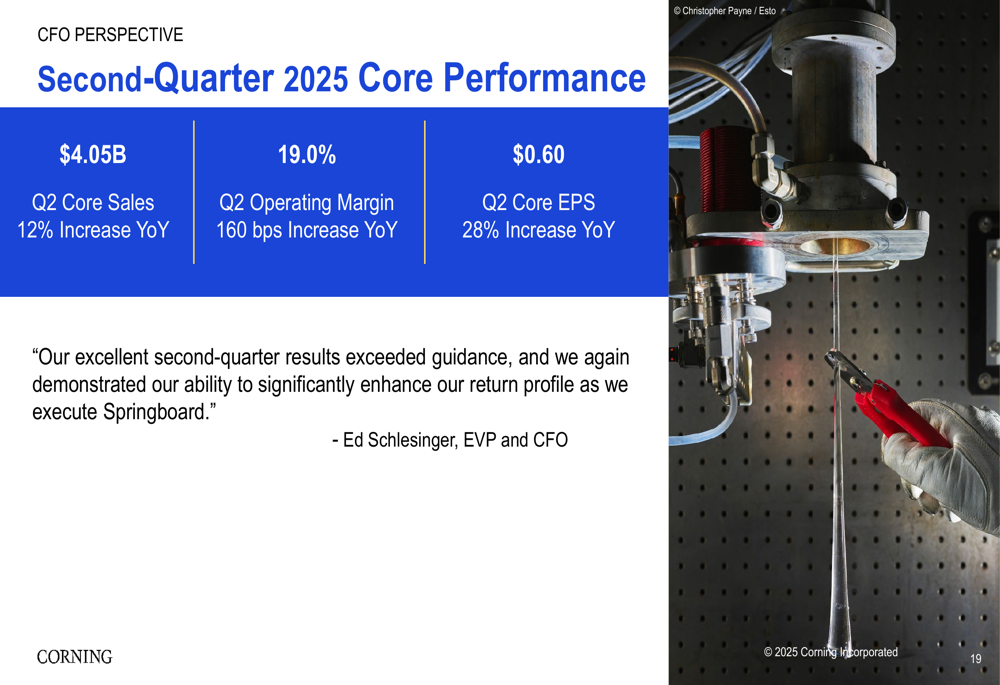

Corning delivered core sales of $4.05 billion in Q2 2025, representing a 12% year-over-year increase, while core earnings per share reached $0.60, up 28% from the same period last year. The company’s operating margin expanded to 19.0%, a 160 basis point improvement year-over-year.

As shown in the following quarterly performance summary:

"Our excellent second-quarter results exceeded our guidance," said Ed Schlesinger, Executive Vice President and CFO. "We have demonstrated our ability to significantly enhance the return profile as we execute Springboard."

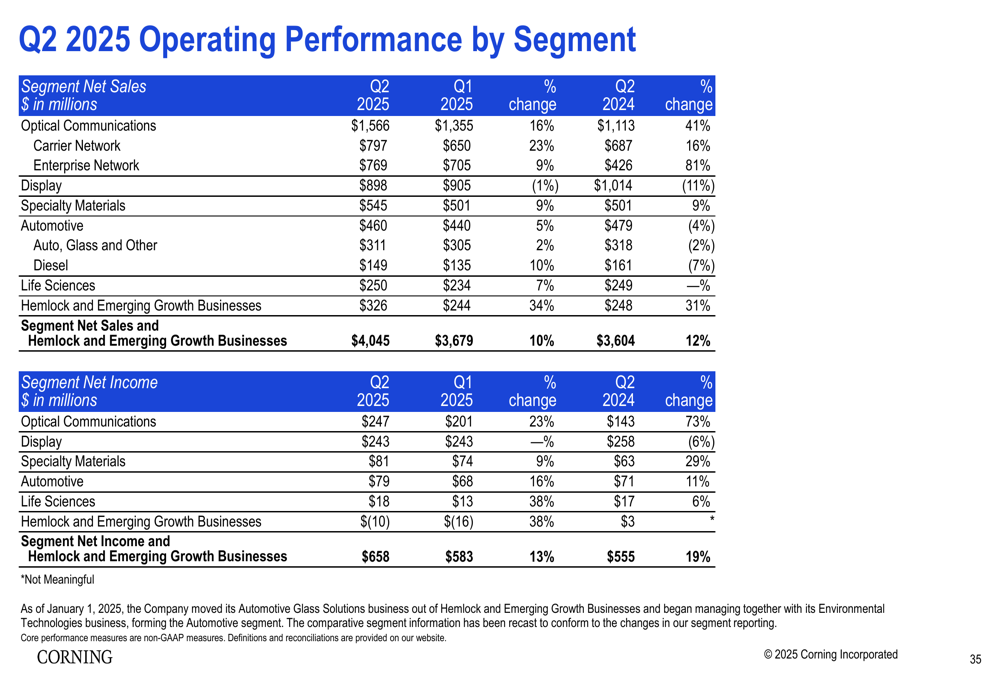

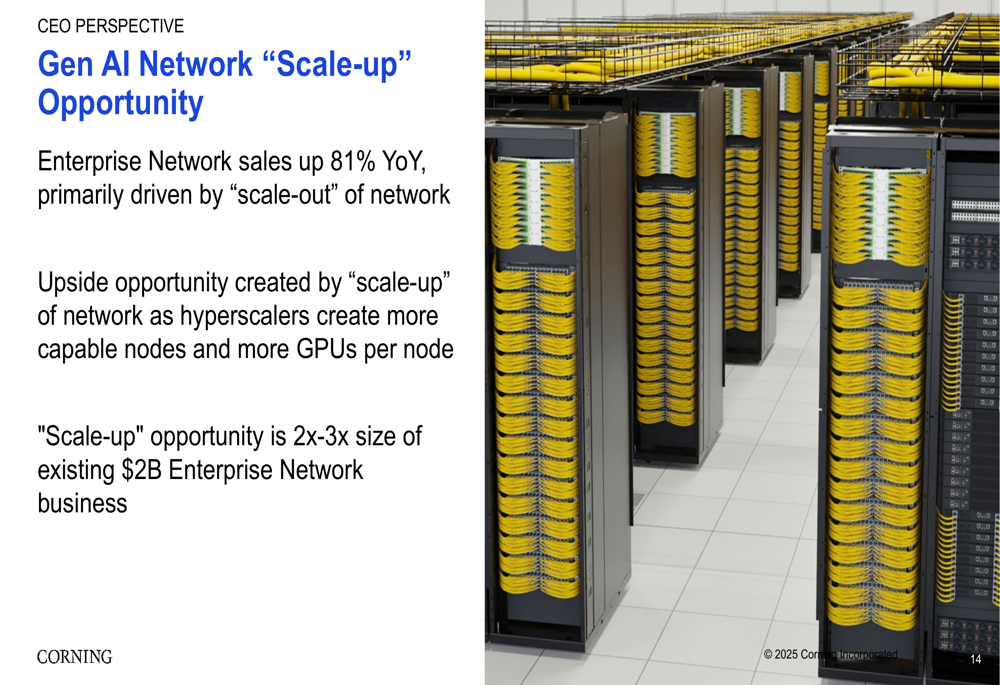

The company’s Optical Communications segment led growth with Q2 net sales of $1.57 billion, up 41% year-over-year, and net income of $247 million, up 73%. This exceptional performance was primarily driven by the Enterprise Network business, which grew 81% year-over-year due to increasing demand for GenAI infrastructure.

The following segment breakdown illustrates the varied performance across Corning’s business units:

Springboard Plan Progress

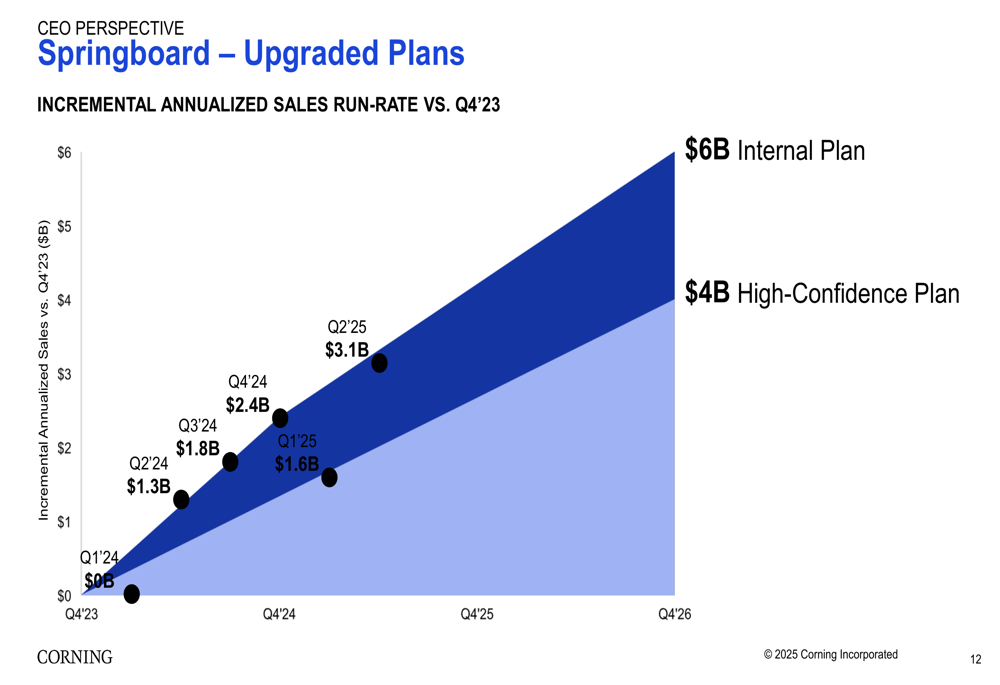

Corning launched its Springboard plan in Q4 2023 with the goal of growing sales, enhancing its return profile, and increasing operating margin to 20% by the end of 2026. The company has made substantial progress, adding over $3 billion to its annualized sales run rate since the plan’s inception.

Based on this strong performance, Corning has upgraded its Springboard targets, raising its high-confidence plan from $3 billion to $4 billion in incremental annualized sales by 2026, with an internal plan target of $6 billion, up from the original $5 billion.

The following chart shows Corning’s progress against these upgraded targets:

"We are halfway through the Springboard plan and the return profile is significantly enhanced," noted Wendell Weeks, Chairman and CEO. "The strong growth drivers increase our confidence in maintaining momentum through 2026 and beyond."

Growth Drivers: GenAI and Solar Opportunities

Corning identified two major growth opportunities driving its upgraded outlook: GenAI network infrastructure and solar manufacturing.

The company’s Enterprise Network business is benefiting from both the "scale-out" of networks (up 81% year-over-year) and an emerging "scale-up" opportunity as hyperscalers create more capable nodes with more GPUs per node. Corning estimates this scale-up opportunity to be 2-3 times the size of its existing $2 billion Enterprise Network business.

As illustrated in the following slide on the GenAI network opportunity:

In the solar segment, Corning has built a strong foundation for rapidly accelerating growth by activating idle assets to serve the need for domestic solar polysilicon and adding capability to produce higher-value, domestically made solar wafers. The company has secured committed customers for 100% of its available 2025 polysilicon and wafer capacity, and 80% for the next 5 years.

Corning expects its solar business to triple by 2027, adding $1.6 billion of new annualized revenue, and ultimately building into a $2.5 billion revenue stream by 2028.

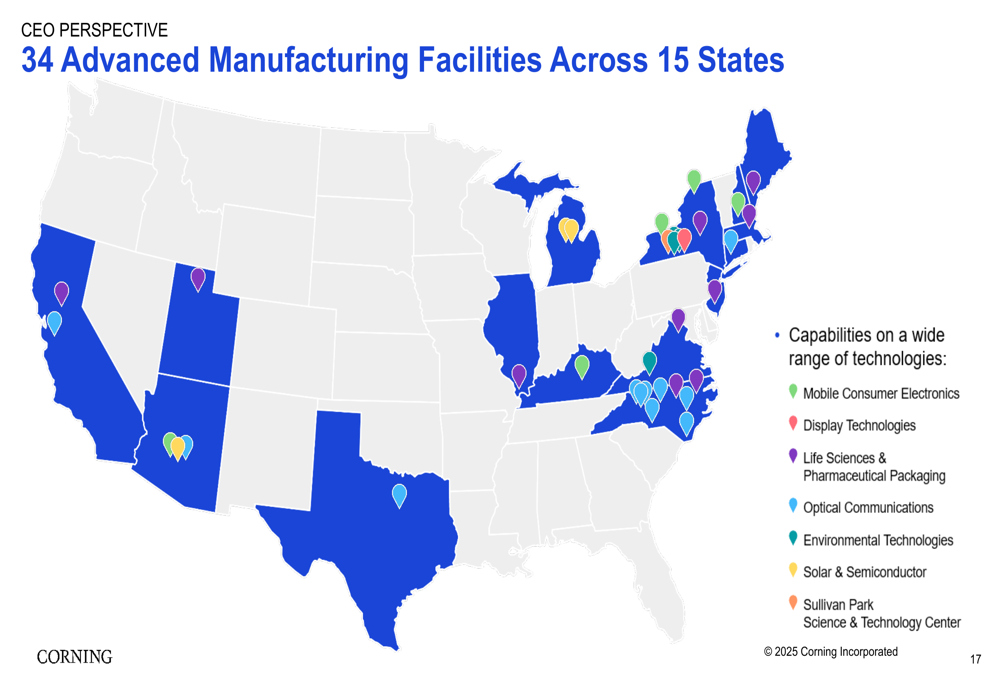

Manufacturing Footprint and Domestic Production

A key competitive advantage for Corning is its extensive U.S. manufacturing footprint, with 34 advanced manufacturing facilities across 15 states. This positions the company well to benefit from domestic production incentives and meet growing demand for U.S.-made components.

The following map highlights Corning’s manufacturing presence:

This domestic manufacturing capability is particularly valuable as customers seek to secure supply chains and benefit from government initiatives promoting U.S. production.

Financial Outlook

For the third quarter of 2025, Corning projects core sales of approximately $4.2 billion and core EPS between $0.63 and $0.67. This guidance includes a $0.01-$0.02 impact from currently enacted tariffs and a $0.02-$0.03 impact from temporarily higher ramp costs.

The company anticipates significant adjusted free cash flow generation in 2025, with approximately $1.3 billion in planned capital investments. Q2 adjusted free cash flow grew 28% year-over-year, reflecting the company’s improved profitability and operational efficiency.

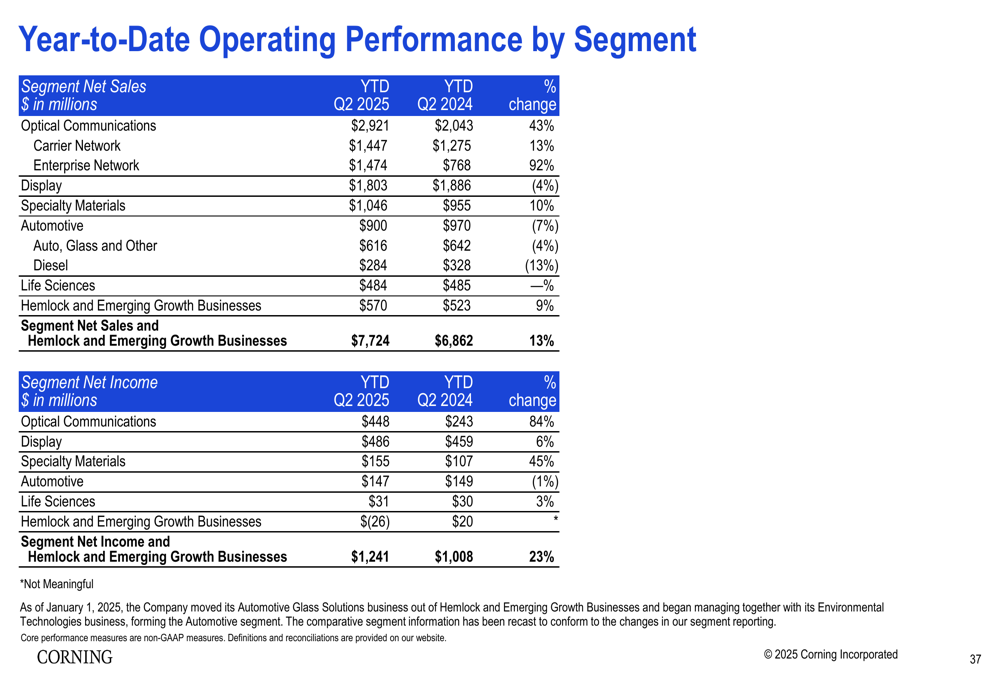

Looking at year-to-date performance through Q2 2025, Corning has demonstrated consistent growth across most segments:

Strategic Positioning

Corning’s strategic focus on innovation and "More Corning" content is driving growth across multiple segments. In the Display segment, the company successfully implemented double-digit price increases in the second half of 2024 and has hedged yen exposure for 2025 and 2026, expecting to be at the high end of its 2025 segment net income range of $900-950 million.

In Specialty Materials, Q2 net sales increased 9% year-over-year to $545 million, primarily driven by continued adoption of premium glass innovations for mobile devices. The Automotive segment is focusing on executing the "More Corning" growth strategy, with plans to triple the Automotive Glass Solutions business by the end of 2026.

The company maintains a strong balance sheet with one of the longest debt tenors in the S&P 500 and only approximately $1.5 billion in debt coming due over the next 5 years, providing flexibility for continued investment in growth opportunities while returning excess cash to shareholders.

As Corning continues to execute its Springboard plan, the company appears well-positioned to capitalize on secular trends in GenAI, solar, and automotive glass, driving sustained growth and margin expansion through 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.