Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

CoStar Group (NASDAQ:CSGP) released its second quarter 2025 investor presentation on July 22, showing accelerated growth and improved performance metrics following a challenging first quarter. The real estate information and marketplace provider reported its 57th consecutive quarter of double-digit revenue growth, with shares currently trading near $93, close to its 52-week high of $93.75.

The company’s Q2 results demonstrate a significant improvement from Q1 2025, when CoStar missed earnings expectations with a loss of $0.04 per share against forecasts of $0.12 EPS. This recovery suggests the company is successfully navigating the challenges it faced earlier in the year while continuing its expansion across both commercial and residential real estate information markets.

Quarterly Performance Highlights

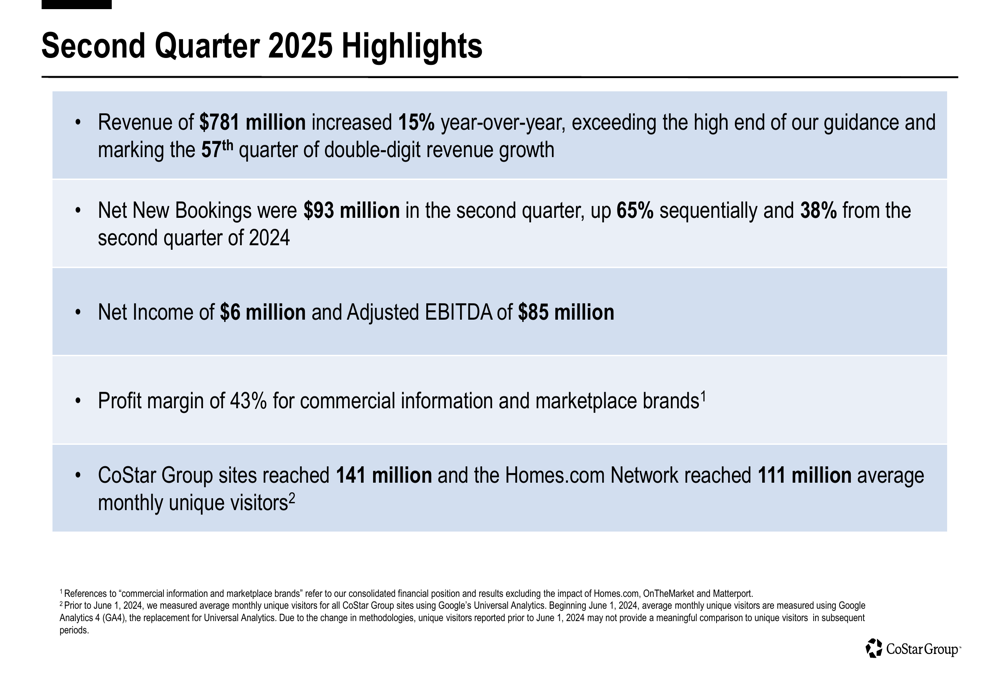

CoStar reported Q2 2025 revenue of $781 million, representing a 15% year-over-year increase, up from the 12% growth rate reported in Q1. This acceleration in revenue growth demonstrates strengthening business momentum as the year progresses.

As shown in the following comprehensive summary of key Q2 metrics:

Particularly notable is the substantial improvement in Net New Bookings, which reached $93 million in Q2, up 65% sequentially from Q1 and 38% year-over-year. This metric is especially important as it serves as a leading indicator for future revenue growth.

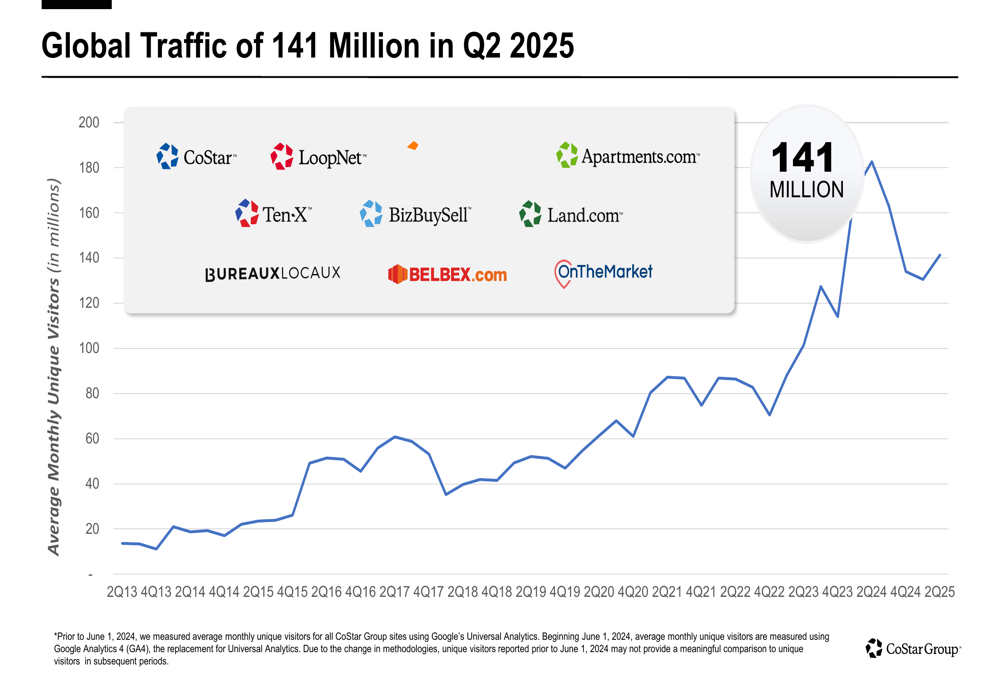

The company’s digital reach continues to expand impressively, with CoStar Group sites attracting 141 million average monthly unique visitors during the quarter. The growth trajectory of this traffic is illustrated in the following chart:

The Homes.com Network also showed strong performance with 111 million average monthly unique visitors, highlighting CoStar’s growing presence in the residential real estate market alongside its established commercial real estate information business.

Detailed Financial Analysis

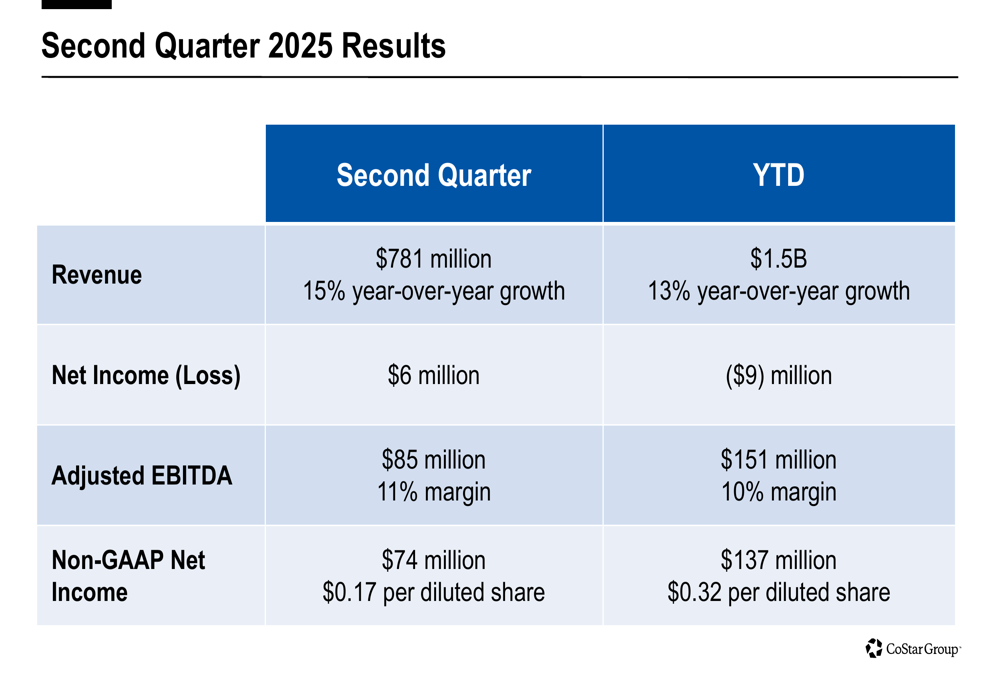

CoStar’s financial results for Q2 2025 show modest profitability with net income of $6 million, a significant improvement from the net loss reported in Q1. Adjusted EBITDA reached $85 million with an 11% margin, also showing substantial progress from the $66 million reported in the previous quarter.

The detailed financial results are presented in the following table:

A key strength in CoStar’s business model continues to be the high profitability of its established commercial information and marketplace brands, which maintained a robust 43% profit margin. This provides the company with a stable foundation to fund growth initiatives in newer segments.

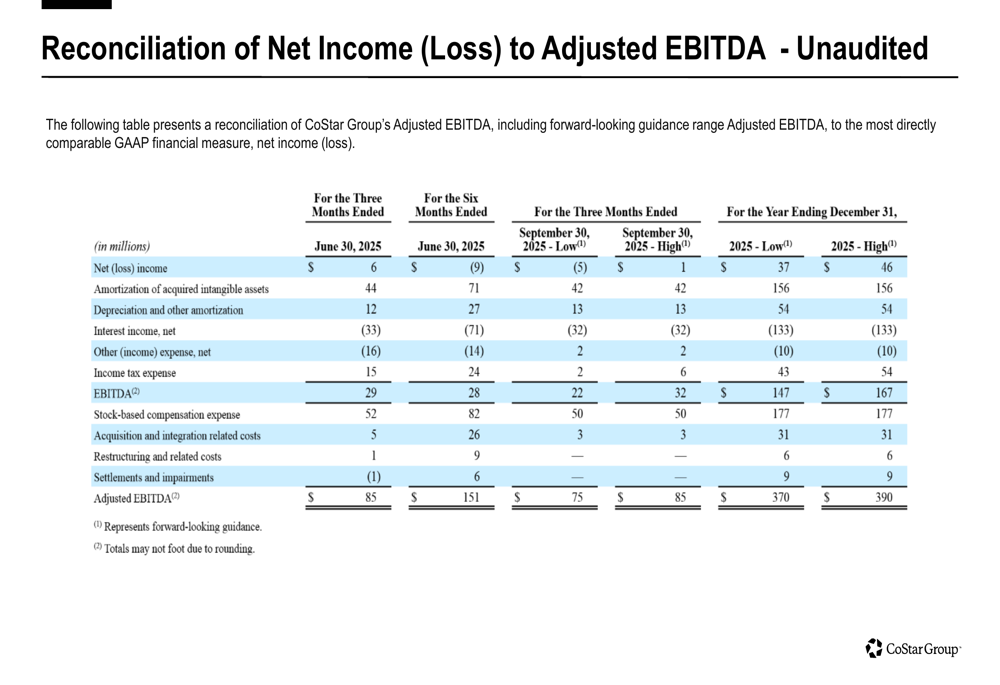

The reconciliation between GAAP and non-GAAP metrics reveals that stock-based compensation and amortization of acquired intangible assets remain significant factors affecting reported earnings:

Forward-Looking Statements

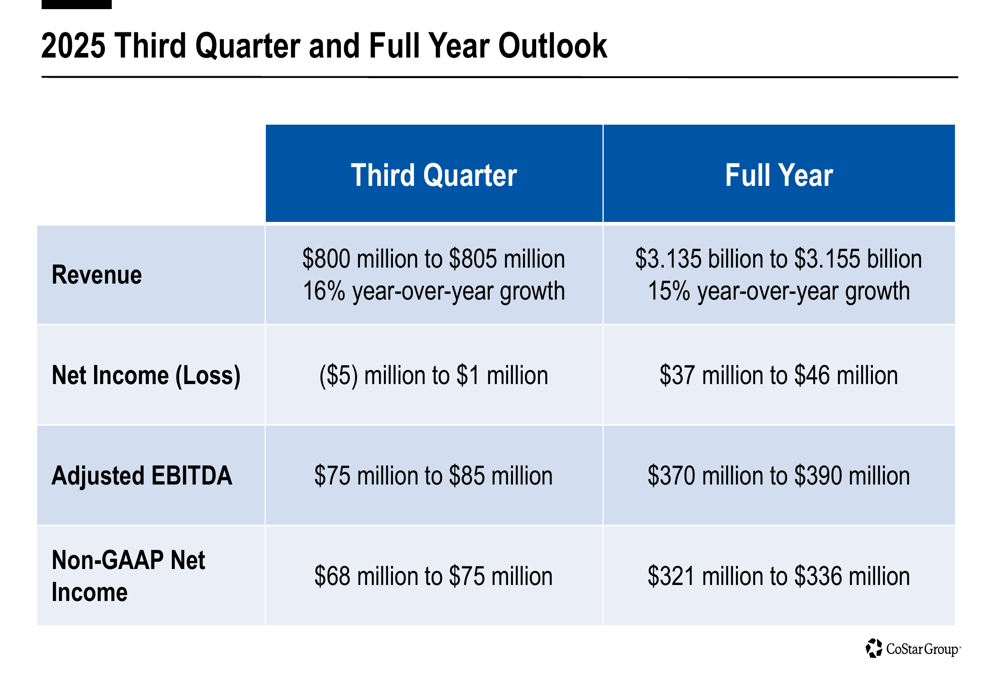

CoStar’s outlook for the remainder of 2025 projects continued strong performance, with third-quarter revenue expected to reach $800-805 million, representing 16% year-over-year growth. For the full year, the company anticipates revenue of $3.135-3.155 billion, maintaining 15% growth compared to 2024.

The detailed guidance for both Q3 and full-year 2025 is presented in the following table:

While Q3 is expected to show a potential small net loss of up to $5 million, the company projects returning to more substantial profitability by year-end, with full-year net income forecast between $37-46 million. Adjusted EBITDA is expected to reach $370-390 million for the full year, representing a significant improvement in the second half compared to the first half of 2025.

This forward guidance aligns with CEO Andy Florence’s comments from the Q1 earnings call, where he expressed optimism that "as market conditions improve over the next few years, the headwinds we’ve experienced will shift to tailwinds and CoStar will return to double-digit growth."

Strategic Investment Returns

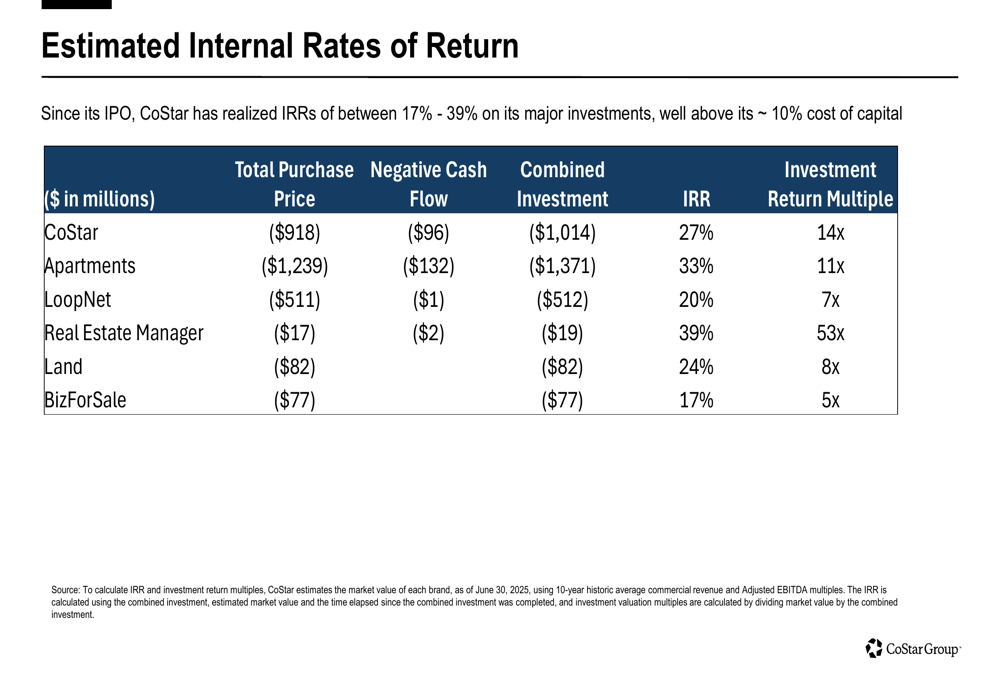

One of the most compelling aspects of CoStar’s presentation is the analysis of historical returns on major investments. The company has consistently generated internal rates of return (IRR) between 17% and 39% on its strategic investments since its IPO, significantly exceeding its approximately 10% cost of capital.

The following table details the performance of these investments:

Particularly impressive is the 39% IRR achieved on the Real Estate Manager investment, which has generated a 53x return multiple. The company’s core CoStar business has delivered a 27% IRR with a 14x return multiple, while the Apartments business has produced a 33% IRR with an 11x return multiple.

These strong historical returns provide context for CoStar’s current investment strategy, including its continued expansion in the residential real estate market through Homes.com and recent acquisitions like Matterport (NASDAQ:MTTR), which was mentioned in the Q1 earnings discussion.

Conclusion

CoStar Group’s Q2 2025 presentation depicts a company regaining momentum after facing challenges earlier in the year. The acceleration in revenue growth, significant improvement in Net New Bookings, and continued expansion of digital traffic all point to strengthening business fundamentals.

While near-term profitability remains modest as the company continues to invest in growth initiatives, the strong historical returns on previous investments suggest this strategy has created substantial value over time. With the stock trading near its 52-week high, investors appear to be focusing on CoStar’s long-term growth potential rather than short-term earnings volatility.

As the company progresses through the second half of 2025, key metrics to watch will include whether the strong booking trends translate into accelerated revenue growth and if margins begin to expand as projected in the full-year guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.