Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Costco Wholesale Corp (NASDAQ:COST) released its third-quarter fiscal 2025 results on May 29, showing continued momentum with strong sales growth and margin expansion. The retailer reported net sales of $62.0 billion, representing an 8.0% increase year-over-year, while comparable sales grew 5.7% (8.0% when adjusted for gasoline prices and foreign exchange impacts). The company’s stock closed at $1,008.49 on the day of the announcement, with after-hours trading showing a slight gain of 0.12%.

The Q3 results follow a mixed second quarter where Costco beat revenue expectations but missed on earnings per share. The latest quarter shows improvement in profitability metrics, with EPS growing 13.2% year-over-year.

Quarterly Performance Highlights

Costco’s third-quarter performance was driven by healthy traffic growth of 5.2% across its warehouses, while average ticket size increased by 0.4% (2.7% when adjusted). The company’s e-commerce business continued its strong trajectory with comparable sales growth of 14.8% (15.7% adjusted).

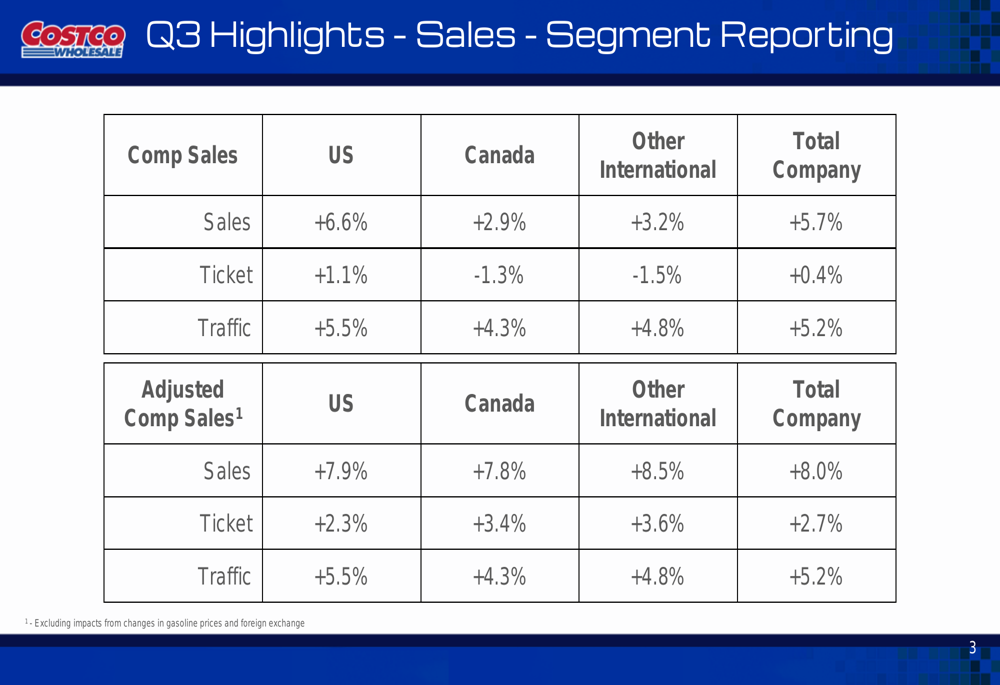

As shown in the following sales highlights slide:

Breaking down performance by geographic segment, Costco saw strong growth across all regions. U.S. operations led with comparable sales growth of 6.6% (7.9% adjusted), while Canada and Other International markets posted 2.9% and 3.2% growth respectively (7.8% and 8.5% when adjusted). Traffic growth was particularly strong in the U.S. at 5.5%.

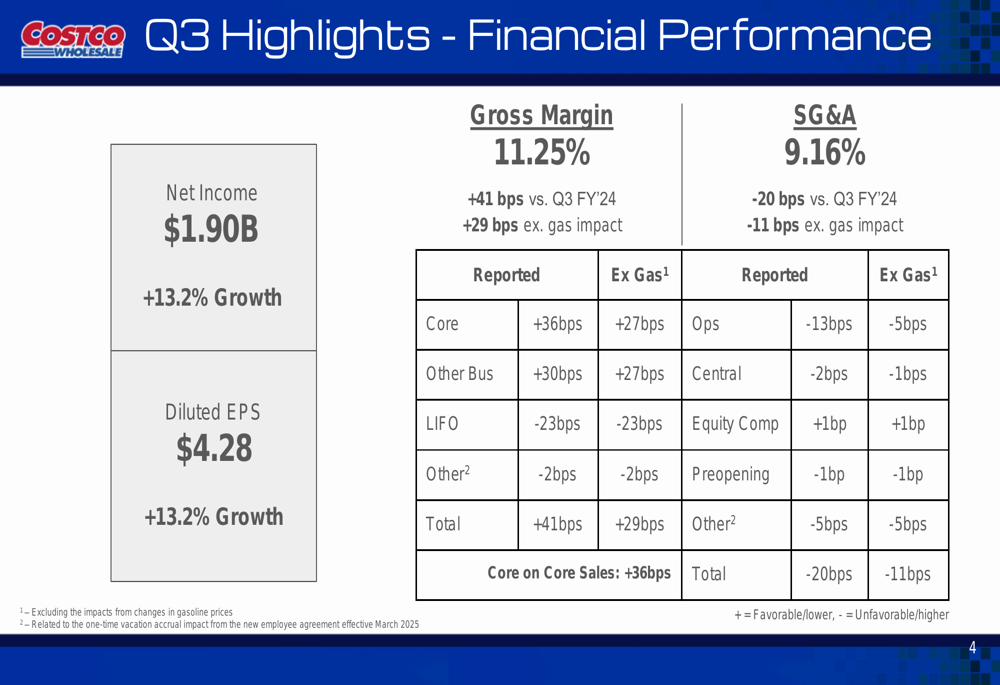

On the profitability front, Costco reported net income of $1.90 billion, up 13.2% from the previous year, with diluted earnings per share also increasing 13.2% to $4.28. Gross margin improved by 41 basis points to 11.25% compared to Q3 FY2024, while SG&A expenses as a percentage of sales decreased by 20 basis points to 9.16%.

The following financial performance slide details the margin improvements:

Membership and Digital Performance

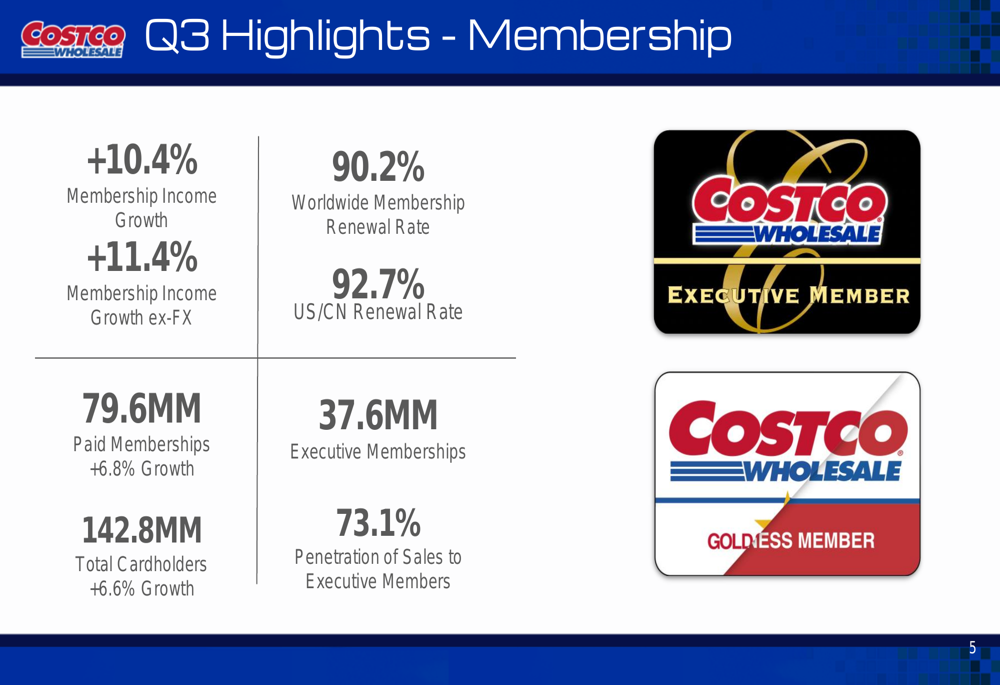

Membership remains a critical component of Costco’s business model, with membership income growing 10.4% (11.4% excluding foreign exchange impacts) in the third quarter. The company maintained impressive renewal rates, with worldwide membership renewals at 90.2% and U.S./Canada renewals at 92.7%.

Costco’s membership base continues to expand, with paid memberships reaching 79.6 million (up 6.8%) and total cardholders growing to 142.8 million (up 6.6%). Executive memberships, which generate higher revenue per member, now account for 37.6 million members and represent 73.1% of sales.

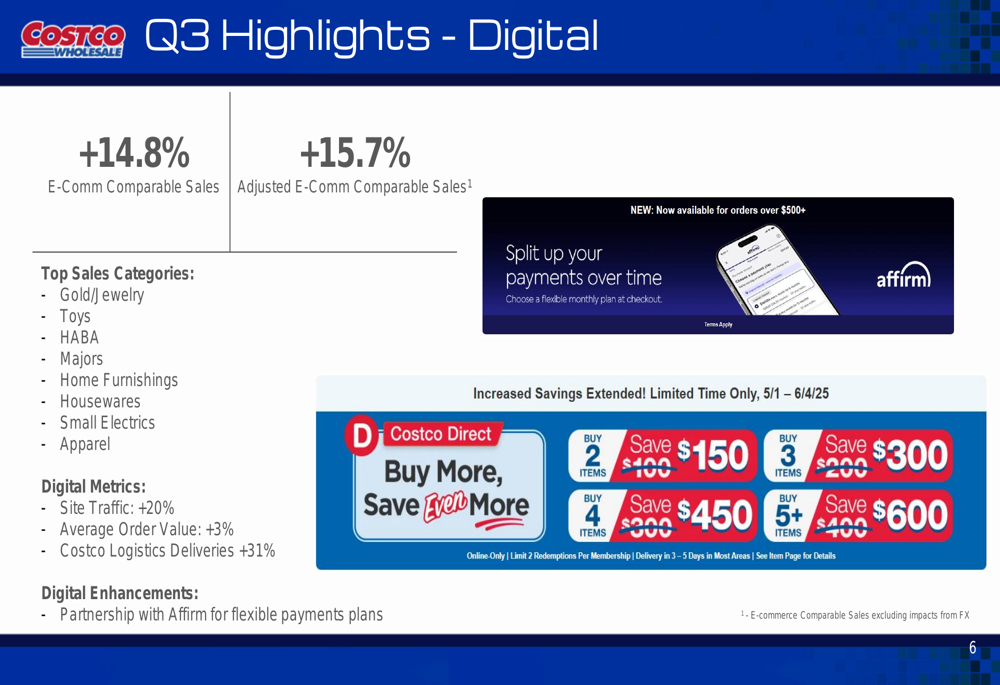

The digital segment showed particularly strong results, with e-commerce comparable sales growing 14.8%. Site traffic increased by 20%, while average order value rose 3%. Costco Logistics, which handles delivery of bulky items, saw deliveries increase by 31%. Top-performing categories in e-commerce included gold/jewelry, toys, health and beauty aids, major appliances, home furnishings, housewares, and small electrics.

The company also highlighted its new partnership with Affirm to provide flexible payment plans, enhancing the digital shopping experience:

Expansion Strategy

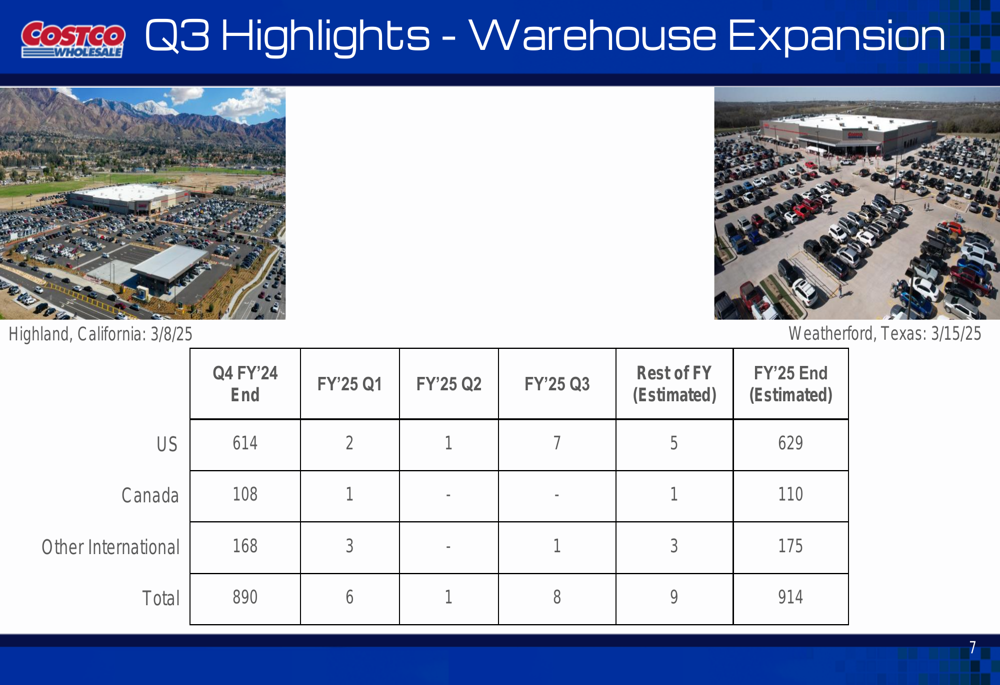

Costco continues to execute its warehouse expansion strategy, planning to add a total of 24 new locations in fiscal year 2025. This would bring the total warehouse count from 890 at the end of FY2024 to 914 by the end of FY2025. The expansion includes 15 new U.S. locations, 2 in Canada, and 7 in other international markets.

The company opened 8 new warehouses in Q3, including locations in Highland, California and Weatherford, Texas, with 9 more planned for the remainder of the fiscal year:

Strategic Initiatives and Forward-Looking Statements

Costco is focusing on enhancing member value through price reductions on key Kirkland Signature products. Examples highlighted in the presentation include price cuts on organic extra virgin olive oil, chocolate macadamia clusters, and organic mixed nut butter. The company is also expanding its Kirkland Signature product line with new offerings in categories like mini muffin bites, smoked pork ribs, sugar cookies, and apparel.

Looking ahead, Costco appears well-positioned to continue its growth trajectory, with strong membership metrics and expansion plans supporting future revenue growth. The company’s ability to drive both traffic and ticket size, along with its growing e-commerce business, provides multiple avenues for continued sales increases.

While the presentation doesn’t explicitly address potential challenges, the previous earnings call noted concerns about tariff impacts, foreign exchange volatility, and inflationary pressures, particularly in fresh foods. However, Costco’s strong balance sheet, with more cash than debt, provides financial flexibility to navigate these challenges while continuing to invest in growth initiatives.

The company’s focus on value and quality, along with strategic expansion of its Kirkland Signature offerings, remains central to its competitive positioning in the retail sector. With membership renewal rates exceeding 90% and continued growth in the high-margin executive membership tier, Costco’s subscription-based business model continues to demonstrate resilience and stability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.