September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

Coterra Energy Inc (NYSE:CTRA) delivered a strong second quarter performance in 2025, beating production guidance across key metrics and raising its full-year outlook. The company’s August 2025 earnings presentation highlighted its operational success, disciplined capital approach, and ability to generate significant free cash flow growth despite fluctuating commodity prices.

The oil and gas producer’s stock recently traded at $23.70, up 1.1% in the most recent session, though still well below its 52-week high of $29.95. This follows an 8.15% drop after Q1 results, when the company beat EPS expectations but missed slightly on revenue.

Quarterly Performance Highlights

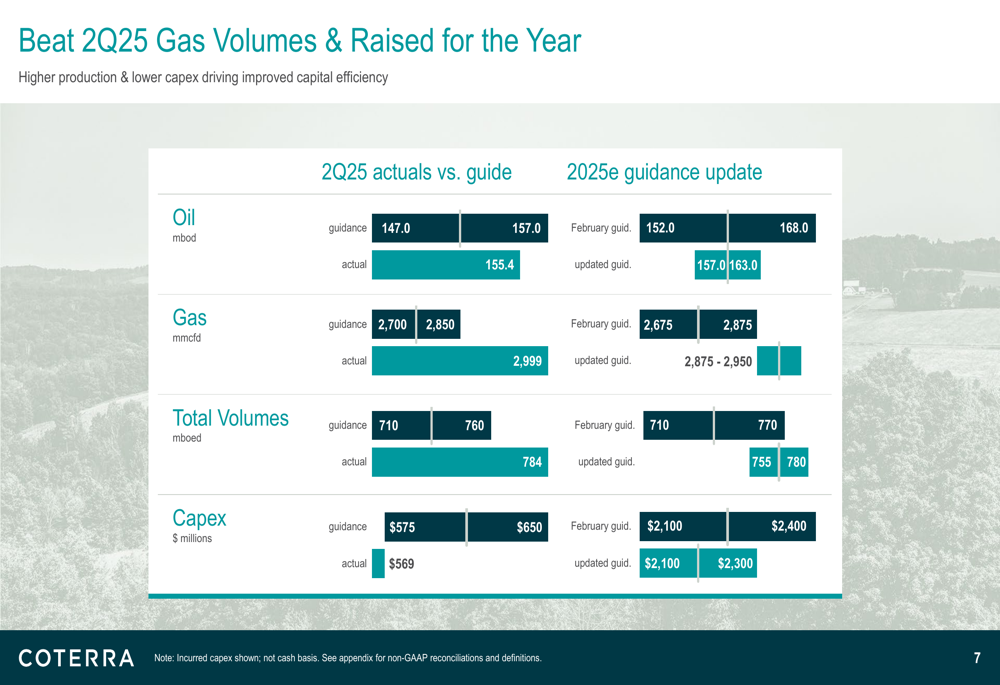

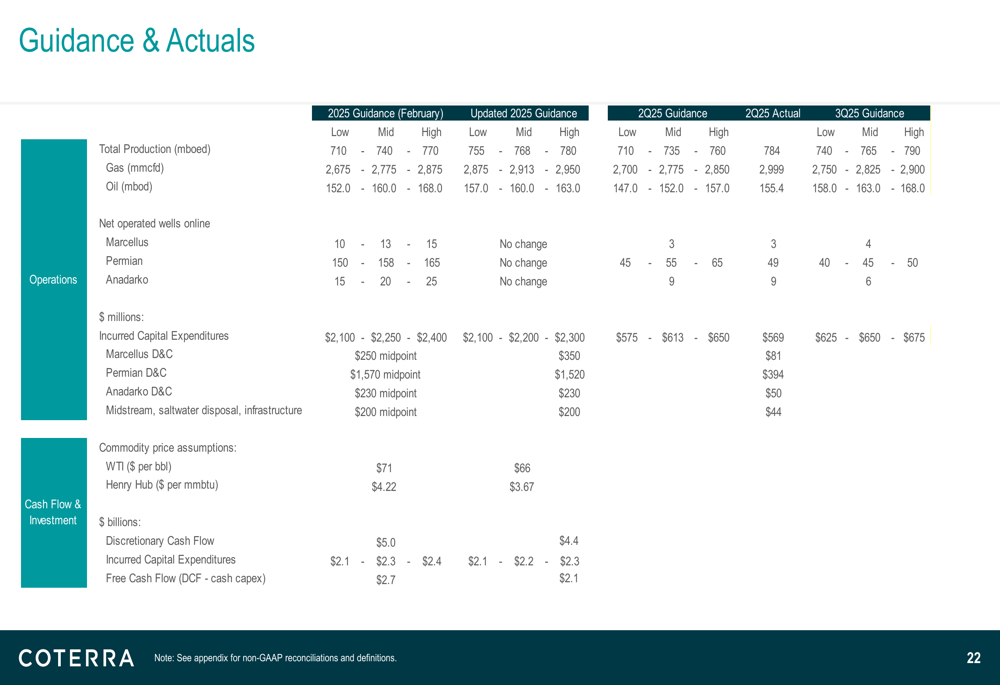

Coterra exceeded expectations across all production metrics in Q2 2025. The company beat the mid-point of oil production guidance and surpassed the high-end of both gas and BOE production guidance. Specifically, Q2 oil production reached 155.4 mbod versus guidance of 147.0-157.0 mbod, while gas production significantly outperformed at 2,999 mmcfd compared to guidance of 2,700-2,850 mmcfd.

As shown in the following detailed comparison of guidance versus actual results:

Total (EPA:TTEF) production reached 784 mboed, well above the guidance range of 710-760 mboed. The company also demonstrated capital discipline, with actual capex of $569 million coming in below the guidance range of $575-650 million.

Based on this strong performance, Coterra has raised its full-year 2025 production guidance. The updated BOE guidance represents a 4% increase at the midpoint compared to February guidance, with total production now expected to reach 755-780 mboed, up from the previous 710-770 mboed.

Capital Discipline & Financial Strategy

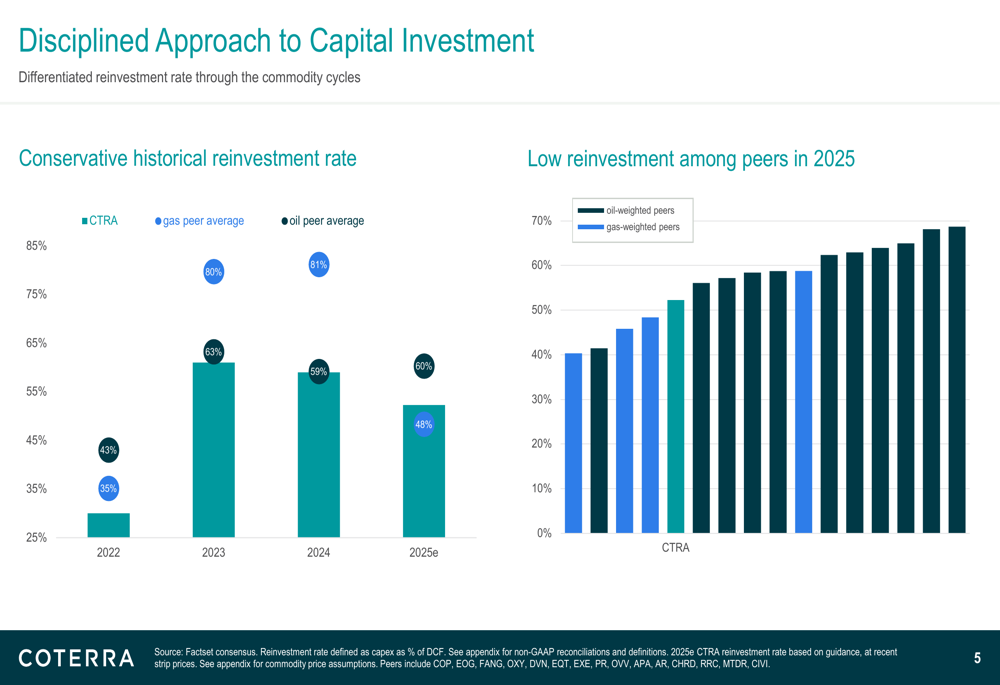

A key theme throughout Coterra’s presentation was its disciplined approach to capital allocation. The company highlighted its conservative reinvestment rate of 43% for 2025, which compares favorably to gas peer average of 63% and oil peer average of 48%.

The following chart illustrates Coterra’s disciplined capital approach compared to peers:

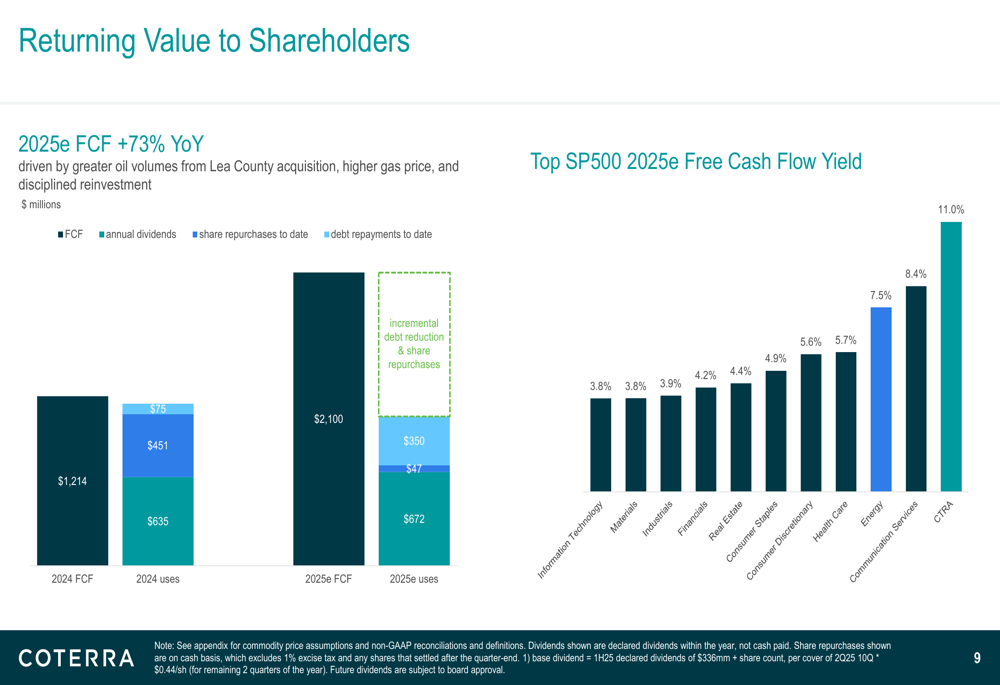

This capital discipline is expected to drive significant free cash flow growth in 2025. The company projects free cash flow of $2.1 billion for the year, representing a 73% increase year-over-year from $1.2 billion in 2024. This growth is attributed to greater oil volumes from the Lea County acquisition, higher gas prices, and disciplined reinvestment.

Coterra’s free cash flow allocation strategy emphasizes shareholder returns through dividends and share repurchases, as illustrated in this breakdown:

The company maintains a 3.6% dividend yield and plans to continue opportunistic share repurchases. Additionally, Coterra’s 2025 estimated free cash flow yield of 11.0% ranks among the highest in the S&P 500, providing an attractive value proposition for investors.

Strategic Initiatives

Coterra’s business strategy centers on a culture of excellence, data-driven problem solving, and a conservative financial approach. The company’s investment thesis highlights its consistent profitable growth, high-quality inventory, diversified portfolio, and durable free cash flow generation.

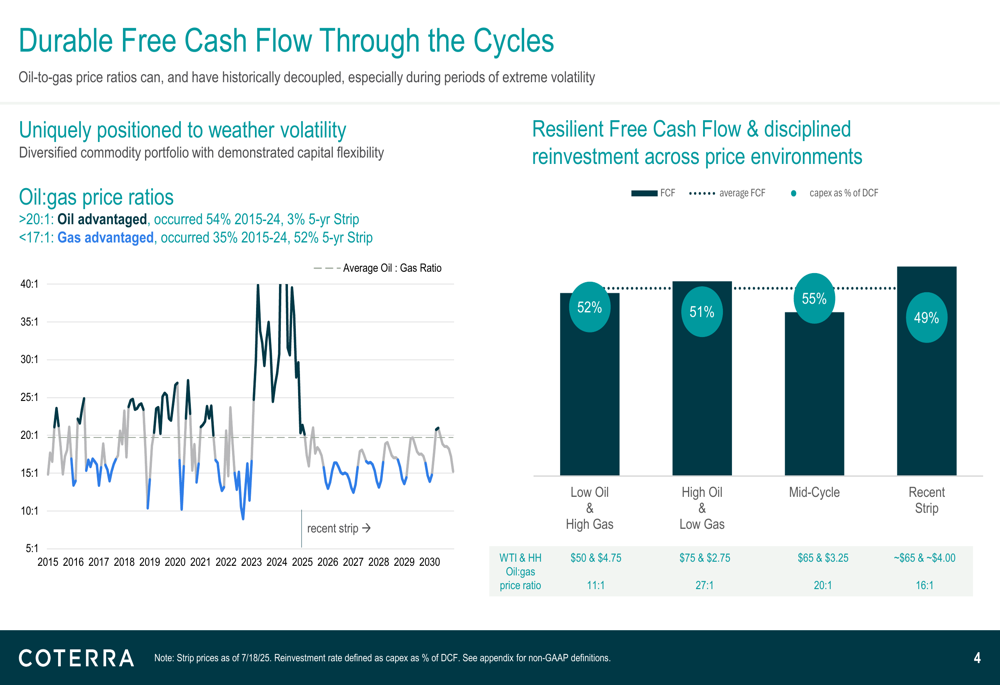

The company’s ability to generate free cash flow through different commodity price cycles is a key strategic advantage, as illustrated in this analysis of oil-to-gas price ratios:

This chart demonstrates how Coterra’s balanced exposure to both oil and natural gas allows it to maintain resilient free cash flow across various price environments. The company maintains a disciplined reinvestment rate of approximately 50% regardless of whether oil prices are high and gas prices are low, or vice versa.

Asset Portfolio & Operational Outlook

Coterra operates a diversified portfolio across three major basins: Permian, Marcellus, and Anadarko. The company estimates it has approximately 15 years of high-quality inventory across its asset base, with about $14 billion (45%) of its economic capex opportunities expected to generate 2.0x PVI10 or better.

For 2025, Coterra plans to maintain 9 rigs in the Permian during the second half of the year, while adding $100 million of activity in the Marcellus with 2 rigs in response to a positive gas outlook. In the Anadarko, the company completed its largest gas development (9 gross wells) in the basin to date in Q2, with its first 3-mile laterals (6 gross wells) expected to come online in Q4.

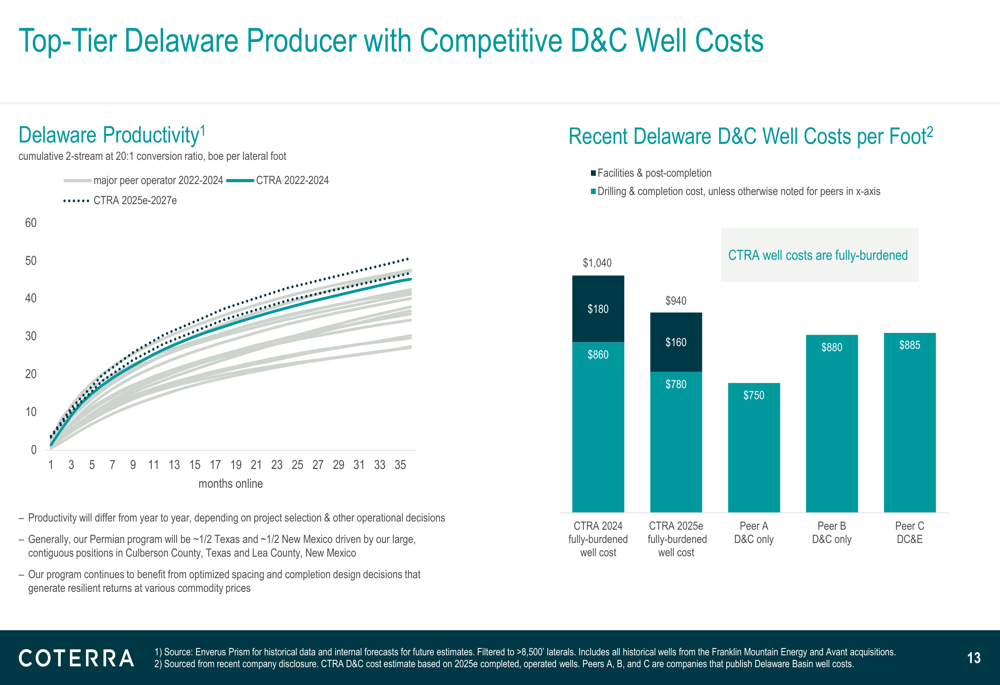

The company has achieved significant well cost reductions across all operating areas: Permian (-12% YoY), Marcellus (-23% YoY), and Anadarko (-18% YoY). These cost reductions, combined with optimized spacing and completion designs, are driving improved returns.

The following chart demonstrates Coterra’s competitive position in the Delaware Basin with top-tier productivity and competitive D&C well costs:

Financial Position

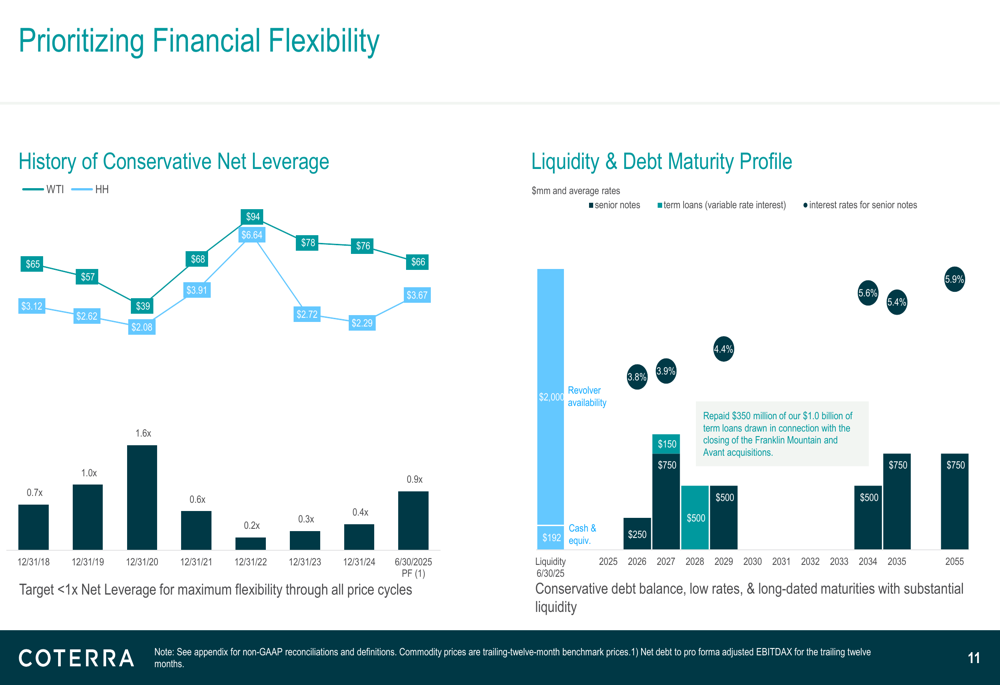

Coterra maintains a strong balance sheet with a conservative approach to leverage. The company’s pro forma leverage ratio is approximately 0.9x, well below its target of less than 1.0x net leverage.

The following chart illustrates Coterra’s history of conservative net leverage and debt maturity profile:

During the first half of 2025, Coterra retired $350 million of term loans related to the Franklin Mountain and Avant acquisitions, demonstrating its commitment to debt reduction. The company’s well-structured debt maturity profile, with no significant maturities until 2027, provides additional financial flexibility.

Forward-Looking Statements

Based on its strong Q2 performance, Coterra has updated its 2025 guidance as follows:

The company now expects to be near the high end of its $2.1 to $2.3 billion 2025 capital expenditure guidance range, reflecting increased gas activity. Despite this increase, Coterra maintains a disciplined reinvestment rate of approximately 52%.

To manage commodity price risk, Coterra has implemented a balanced hedging strategy. Approximately 50% of gas volumes are hedged with a weighted average floor of $3.08/MMBtu and ceiling price of $5.27/MMBtu, while about 44% of oil volumes are hedged with a ~$61/bbl floor and ~$79/bbl ceiling price.

Sustainability Initiatives

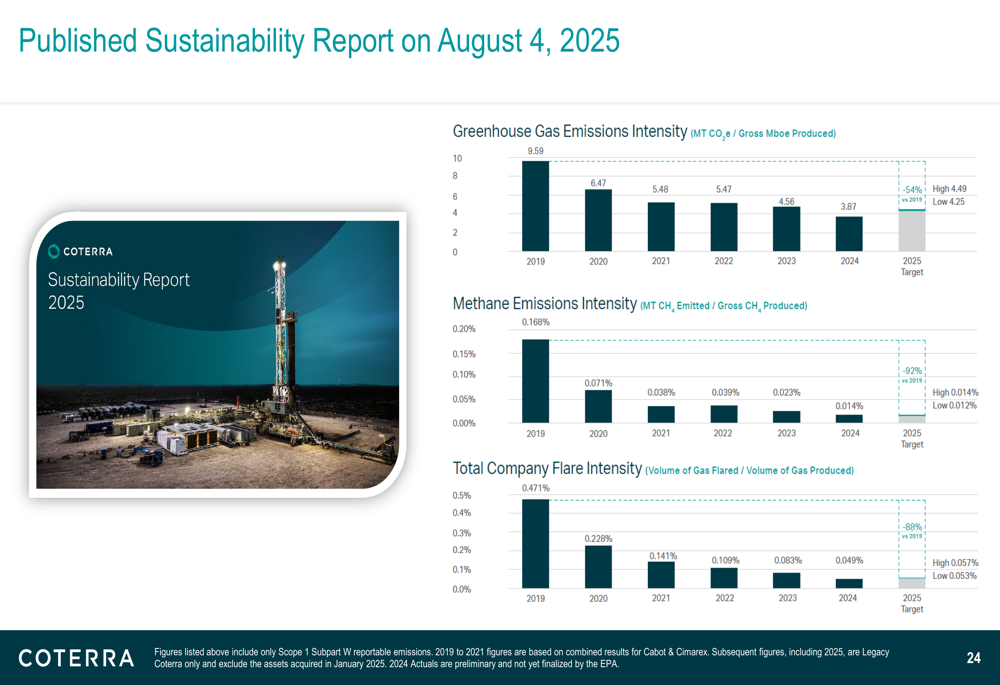

Coterra published its sustainability report on August 4, 2025, highlighting significant progress in reducing emissions. The company has achieved substantial reductions since 2019 across key metrics:

These improvements demonstrate Coterra’s commitment to environmental stewardship while maintaining operational excellence.

Conclusion

Coterra’s Q2 2025 presentation portrays a company executing effectively on its strategic priorities. The production beat and guidance raise reflect operational success, while the projected 73% increase in free cash flow demonstrates the value of the company’s disciplined capital approach. With a diversified asset base, strong balance sheet, and balanced exposure to both oil and gas markets, Coterra appears well-positioned to generate value for shareholders through various commodity price cycles.

Investors will likely focus on the company’s ability to maintain its operational momentum and deliver on its free cash flow projections, particularly given the recent stock price volatility following Q1 results. The significant increase in projected free cash flow, combined with the company’s commitment to shareholder returns and debt reduction, presents a compelling investment case despite the challenging energy market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.