Gold prices hover near 6-week high amid softer dollar, Fed rate cut bets

Introduction & Market Context

CP All PCL (BKK:CPALL), the operator of 7-Eleven convenience stores in Thailand and neighboring countries, presented its Q2 2025 business performance briefing on August 13, 2025. The company reported robust financial results despite facing headwinds in same-store sales growth, highlighting the effectiveness of its expansion strategy and operational efficiency improvements.

The presentation emphasized CP All's continued focus on store network expansion, product mix optimization, and sustainability initiatives, including solar panels and electric vehicle infrastructure at its stores.

Quarterly Performance Highlights

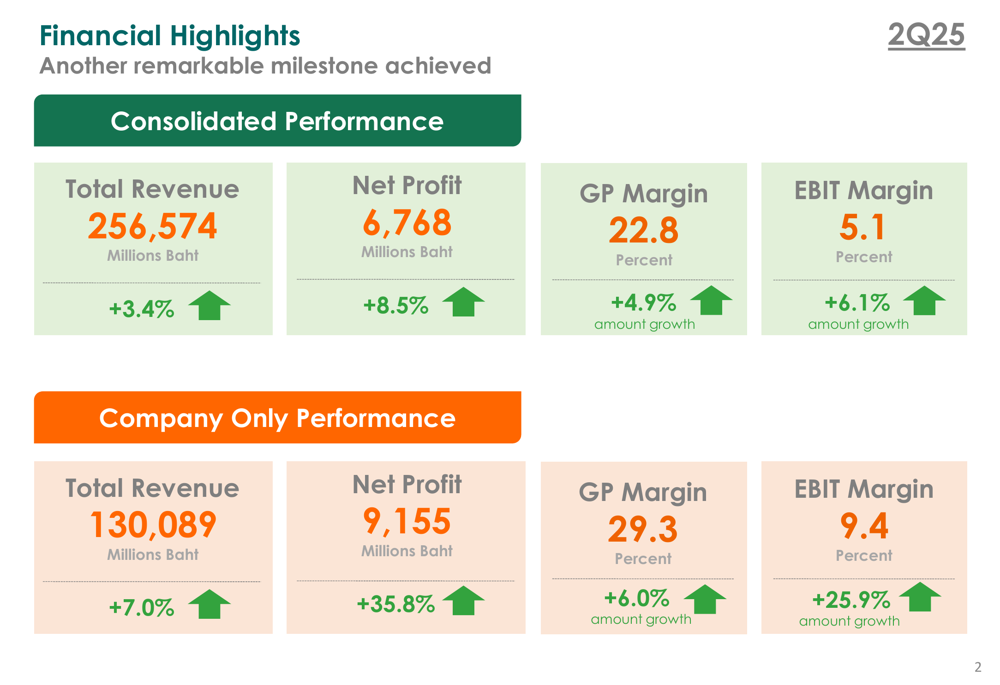

CP All reported impressive financial results for Q2 2025, with consolidated revenue reaching 256,574 million baht, a 3.4% increase year-over-year. More notably, consolidated net profit grew by 8.5% to 6,768 million baht. The company's standalone performance was even more impressive, with revenue increasing 7.0% to 130,089 million baht and net profit surging 35.8% to 9,155 million baht.

As shown in the following financial highlights chart:

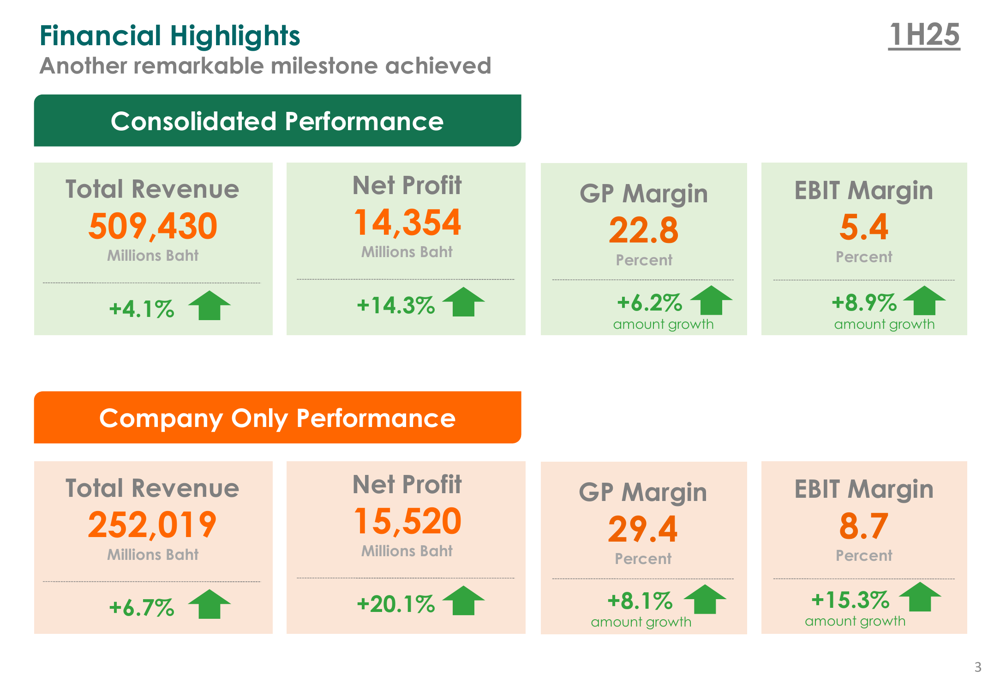

For the first half of 2025, the company maintained strong momentum with consolidated revenue of 509,430 million baht (+4.1%) and net profit of 14,354 million baht (+14.3%). Company-only performance for 1H25 showed revenue of 252,019 million baht (+6.7%) and net profit of 15,520 million baht (+20.1%).

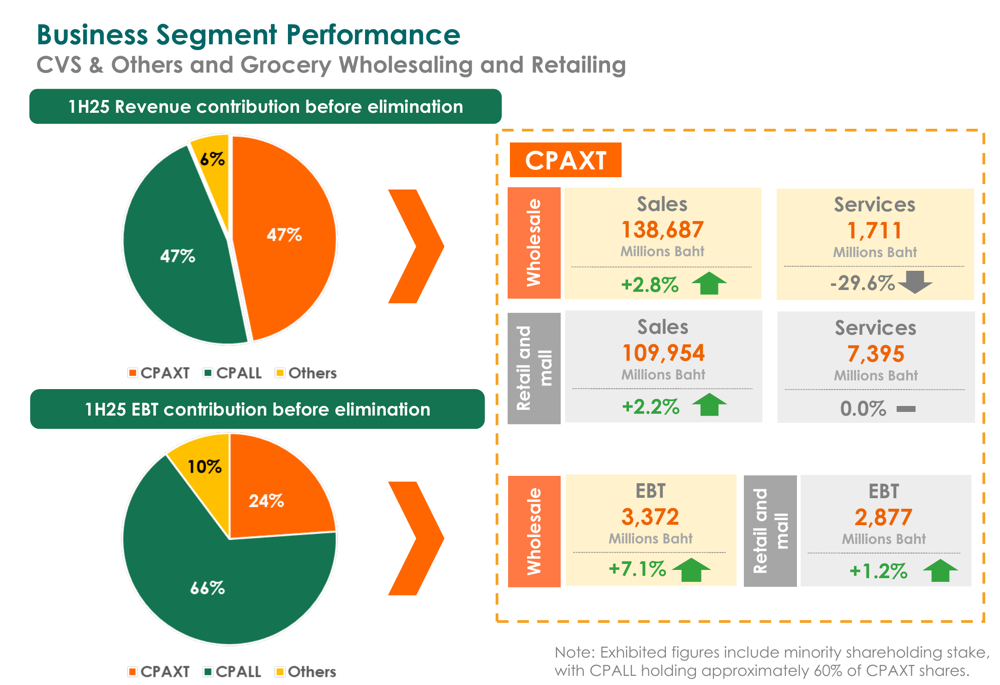

The company's business segments showed varied performance. For 1H25, CP All's CVS (Convenience Store) segment contributed 47% of revenue before elimination, while CPAXT (CP All's subsidiary focused on grocery wholesaling and retailing) also contributed 47%. However, CPAXT dominated the earnings before tax (EBT) contribution at 66%, compared to CP All's 24%.

Store Expansion Strategy

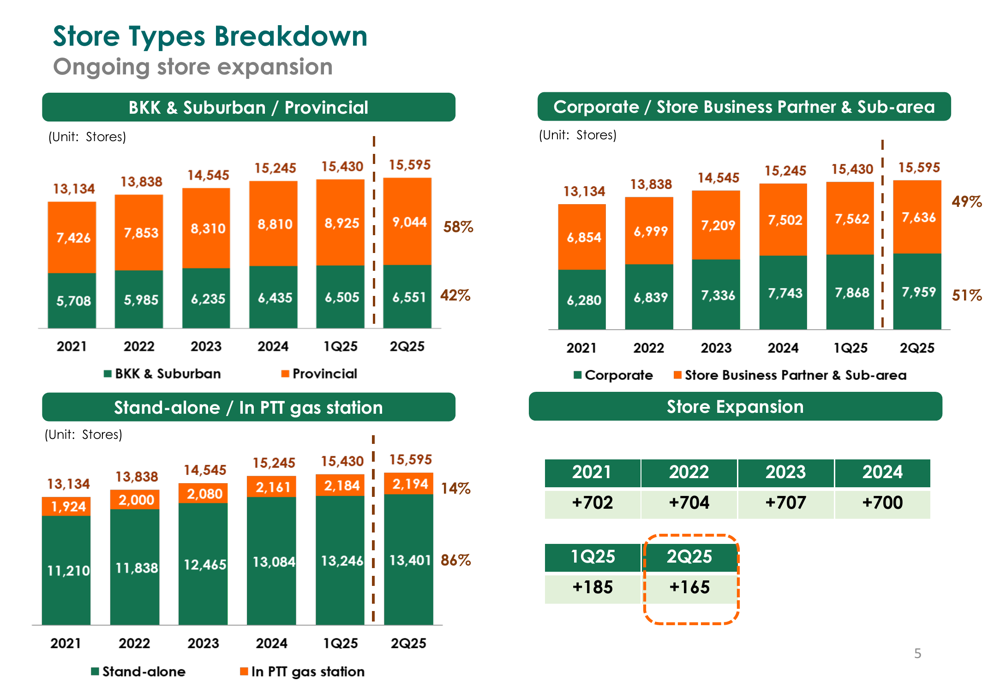

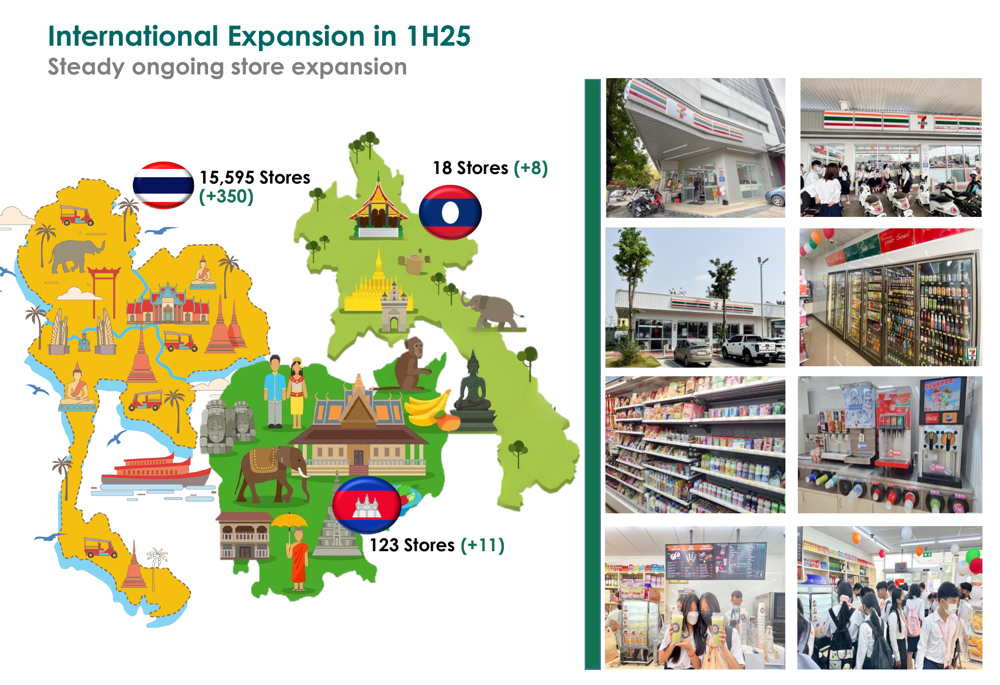

CP All continued its aggressive store expansion strategy, reaching 15,595 stores in Thailand by Q2 2025, adding 165 new stores during the quarter and 350 stores in the first half of 2025. The company maintains a balanced approach to store ownership, with 7,636 corporate stores and 7,959 store business partner and sub-area locations.

The following chart illustrates CP All's consistent store expansion trajectory:

The company is also making progress in its international expansion, with 18 stores in Laos (adding 8 in 1H25) and 123 stores in Cambodia (adding 11 in 1H25). This international growth represents a strategic priority for CP All as it seeks growth opportunities beyond Thailand's increasingly saturated market.

Same-Store Sales and Product Mix Analysis

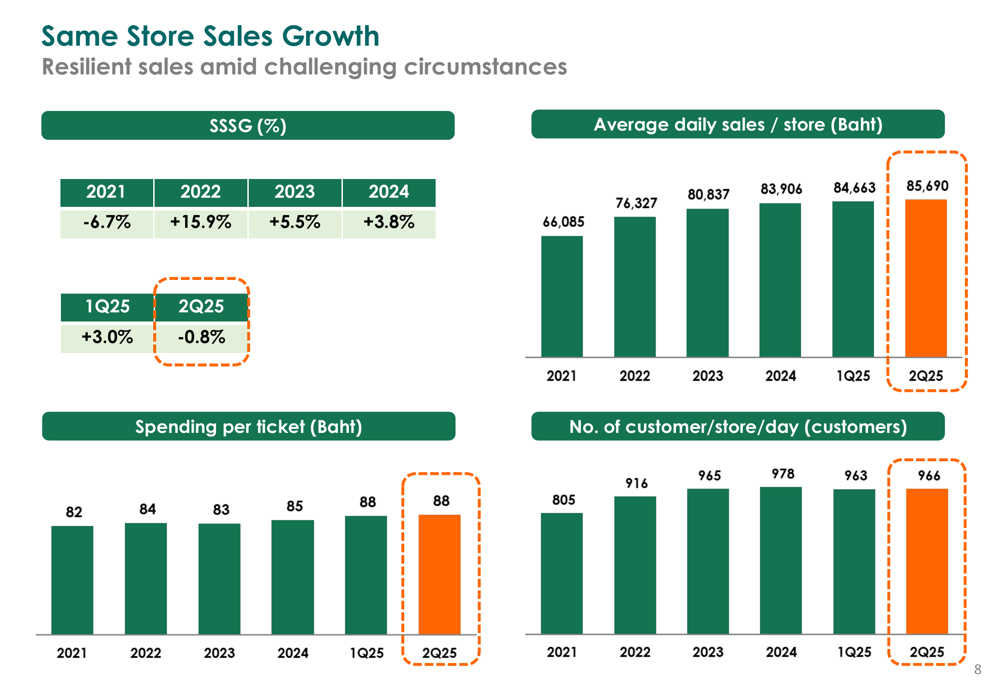

Despite the overall revenue growth, CP All faced challenges in same-store sales growth (SSSG), which turned negative at -0.8% in Q2 2025, down from +3.0% in Q1 2025. This marks a significant shift from the positive SSSG trend observed in previous years. However, average daily sales per store continued to increase, reaching 85,690 baht in Q2 2025.

The following chart shows the SSSG trend and related metrics:

CP All's offline-to-online (O2O) strategy maintained a stable contribution of 11% to total sales in 1H25, unchanged from 2024 but showing significant growth from 8% in 2021. This reflects the company's ongoing efforts to adapt to changing consumer preferences and digital retail trends.

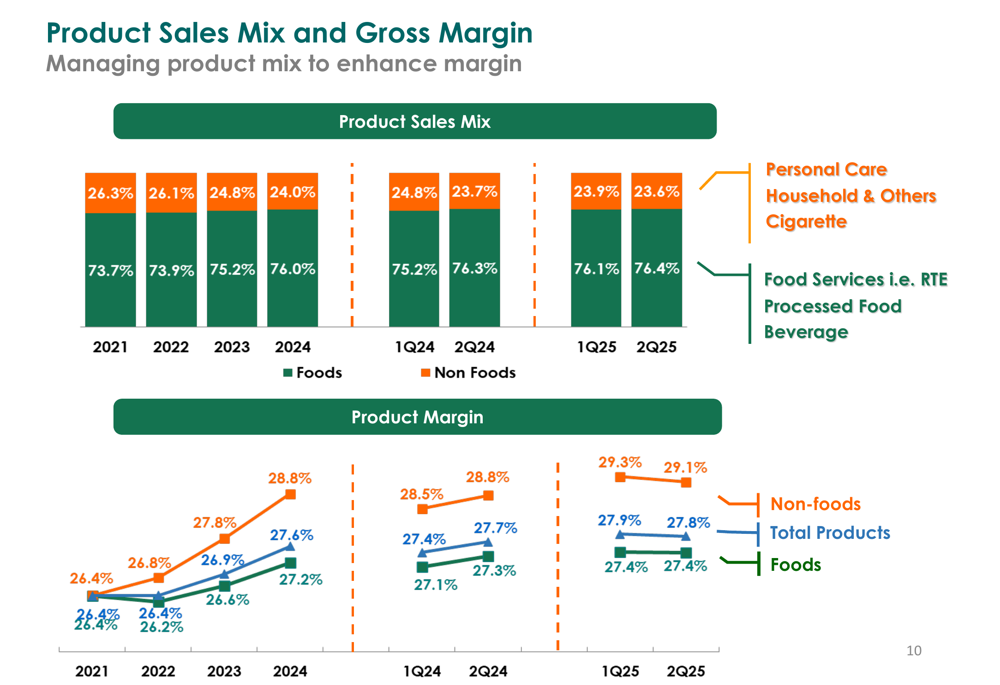

In terms of product mix, CP All continued to shift toward food items, which accounted for 76.4% of sales in Q2 2025, up from 76.1% in Q1 2025 and 73.7% in 2021. This strategic focus on food has helped maintain strong gross margins, with total product margin at 27.8% in Q2 2025.

Profitability and Financial Position

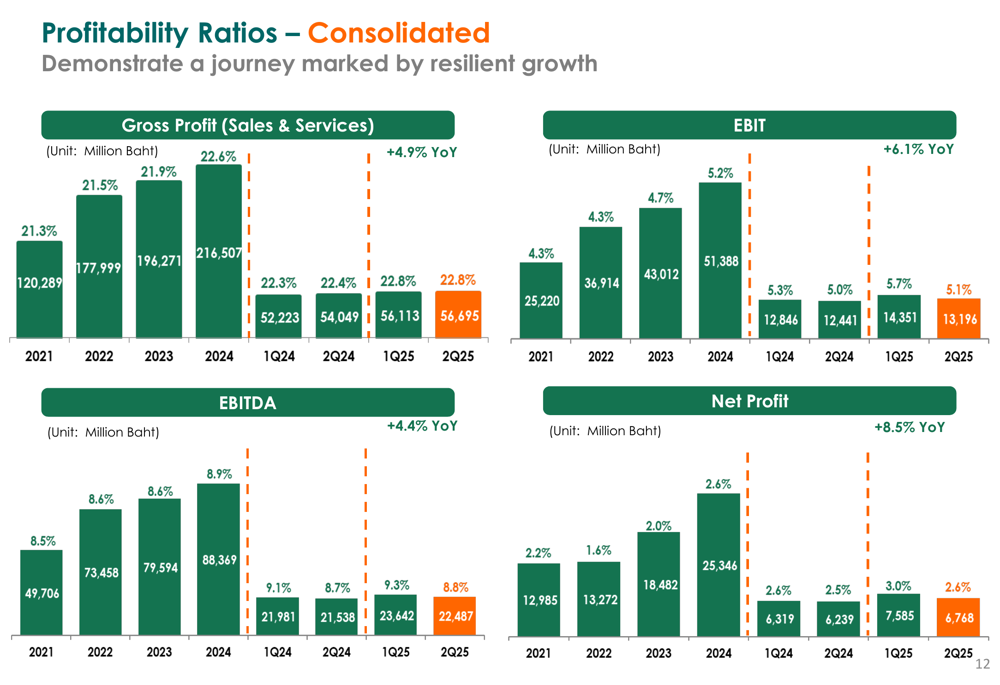

CP All's profitability metrics showed consistent improvement over time. Consolidated gross profit reached 56,695 million baht in Q2 2025, while EBITDA was 22,487 million baht and net profit was 6,768 million baht.

The following chart illustrates the company's consolidated profitability trends:

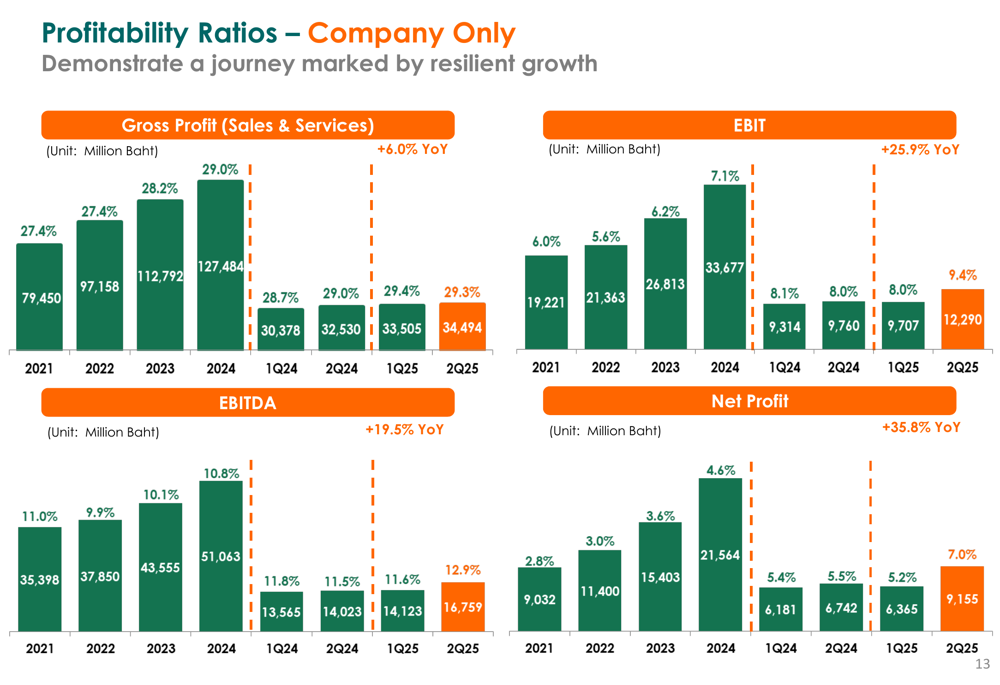

Company-only profitability metrics were even more impressive, with gross profit of 34,494 million baht, EBITDA of 16,759 million baht, and net profit of 9,155 million baht in Q2 2025.

The company maintained a strong financial position with consolidated interest-bearing debt of 316,151 million baht as of June 30, 2025. Net debt to adjusted equity stood at 0.83x, well below the bond covenant limit of 2.0x. CP All's efficient working capital management continued to be a strength, with a negative cash cycle of 25.7 days on a consolidated basis and 33.9 days for the CVS segment.

Forward-Looking Statements

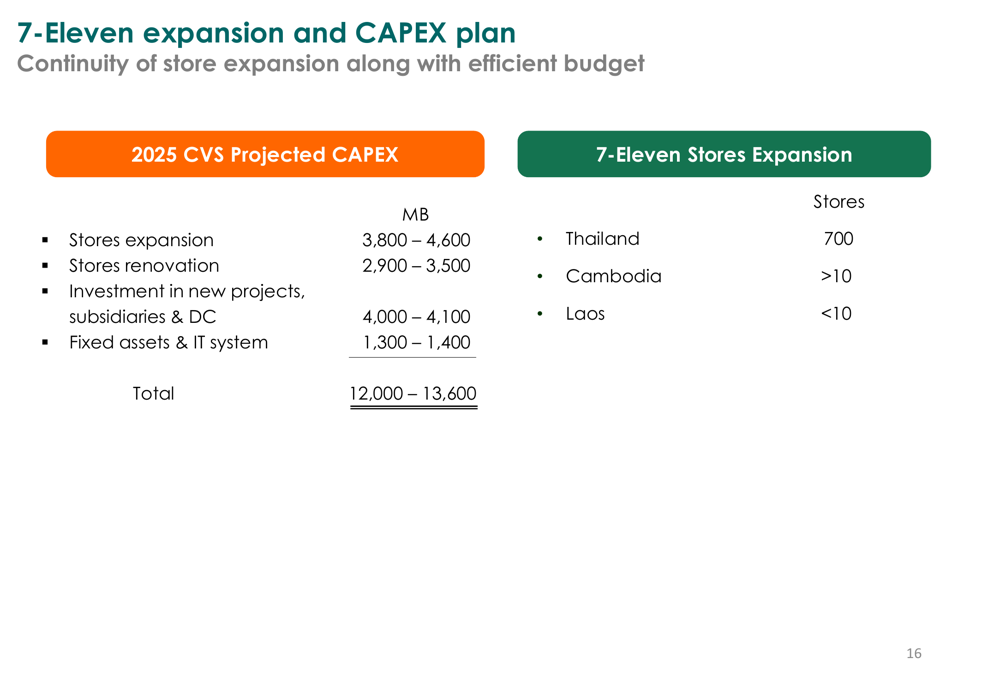

For 2025, CP All outlined an ambitious CAPEX plan of 12,000-13,600 million baht, with the largest allocations going to store expansion (3,800-4,600 million baht) and store renovation (2,900-3,500 million baht). The company plans to add 700 new stores in Thailand, along with continued expansion in Cambodia (>10 stores) and Laos (<10 stores).

CP All's focus on sustainability was also evident in the presentation, with references to solar panels, electric vehicle charging stations, and other green initiatives that align with the company's inclusion in the Dow Jones Sustainability Indices.

Despite the negative SSSG in Q2 2025, CP All's overall financial performance remains strong, driven by its continued store expansion, product mix optimization, and operational efficiency improvements. The company's strategic focus on food items and digital integration positions it well to navigate changing consumer preferences and competitive pressures in the convenience store sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.