Instacart downgraded as competition tightening grip on online grocery

Introduction & Market Context

CPI Card Group Inc . (NASDAQ:PMTS) presented its second quarter 2025 results on August 8, 2025, revealing a mixed performance characterized by solid sales growth but significant profit challenges. The stock reacted negatively to the results, falling 6.02% in premarket trading to $17.50, approaching its 52-week low of $17.27.

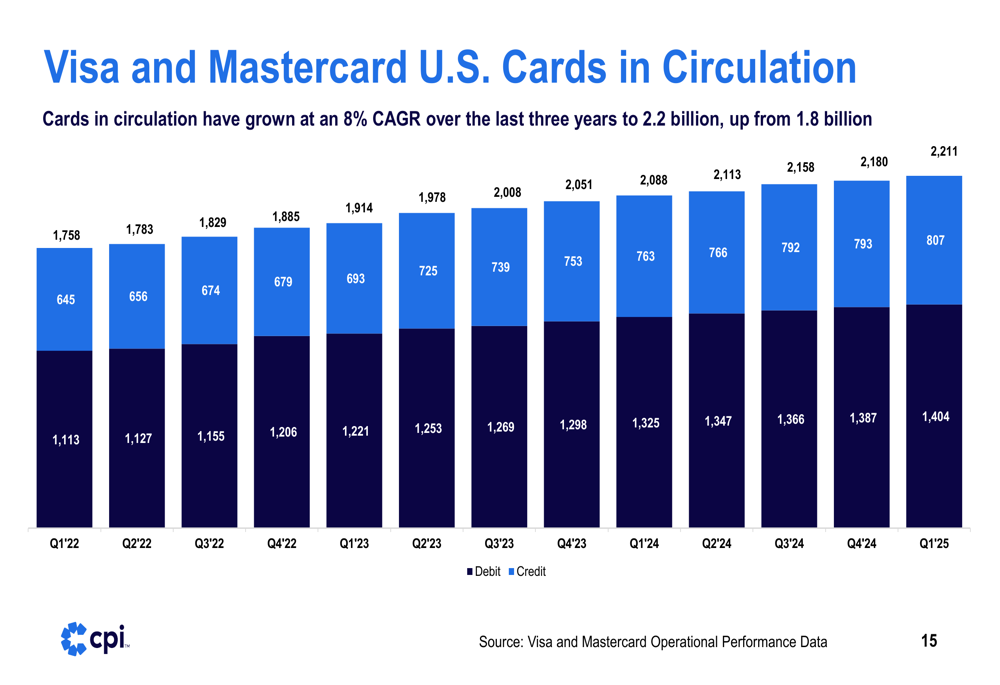

The payment card manufacturer continues to benefit from strong secular trends in the card industry, with Visa (NYSE:V) and Mastercard (NYSE:MA) U.S. cards in circulation growing at an 8% CAGR over the past three years, reaching 2.2 billion cards by Q1 2025.

As shown in the following chart of card circulation growth:

Quarterly Performance Highlights

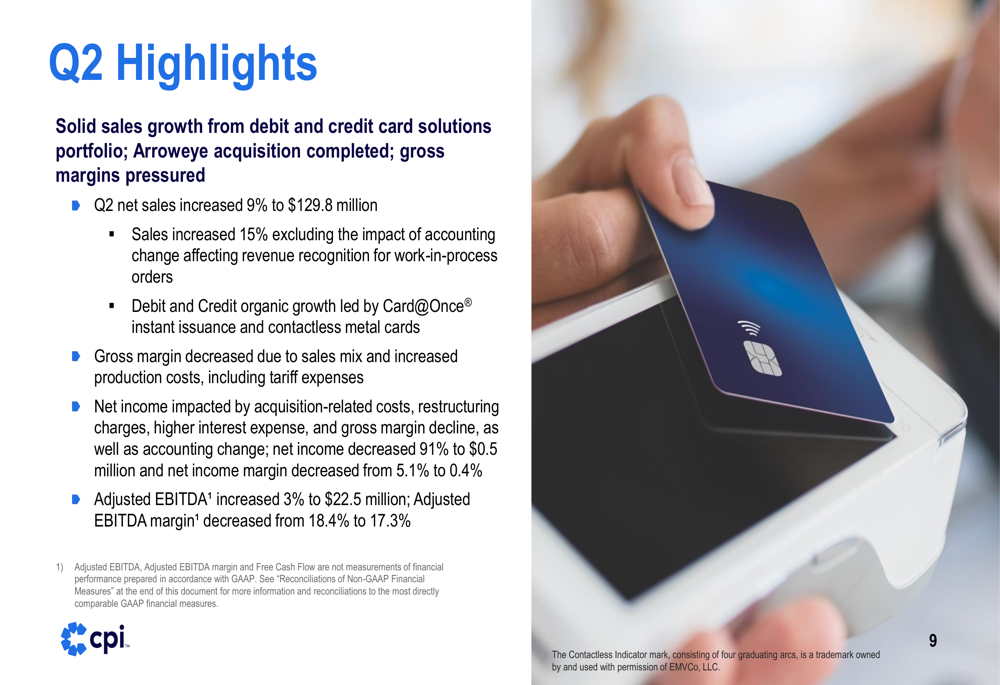

CPI Card Group reported Q2 2025 net sales of $129.8 million, a 9% increase year-over-year. When excluding the impact of an accounting change affecting revenue recognition for work-in-process orders, sales increased by 15%. This growth was primarily driven by the company’s debit and credit card solutions portfolio and the recently completed Arroweye acquisition.

Despite the sales growth, profitability metrics declined sharply. Net income decreased 91% to $0.5 million, with diluted EPS also falling 91% to just $0.04. Adjusted EBITDA increased 3% to $22.5 million, but the adjusted EBITDA margin contracted from 18.4% to 17.3%.

The company’s Q2 performance summary is illustrated in the following slide:

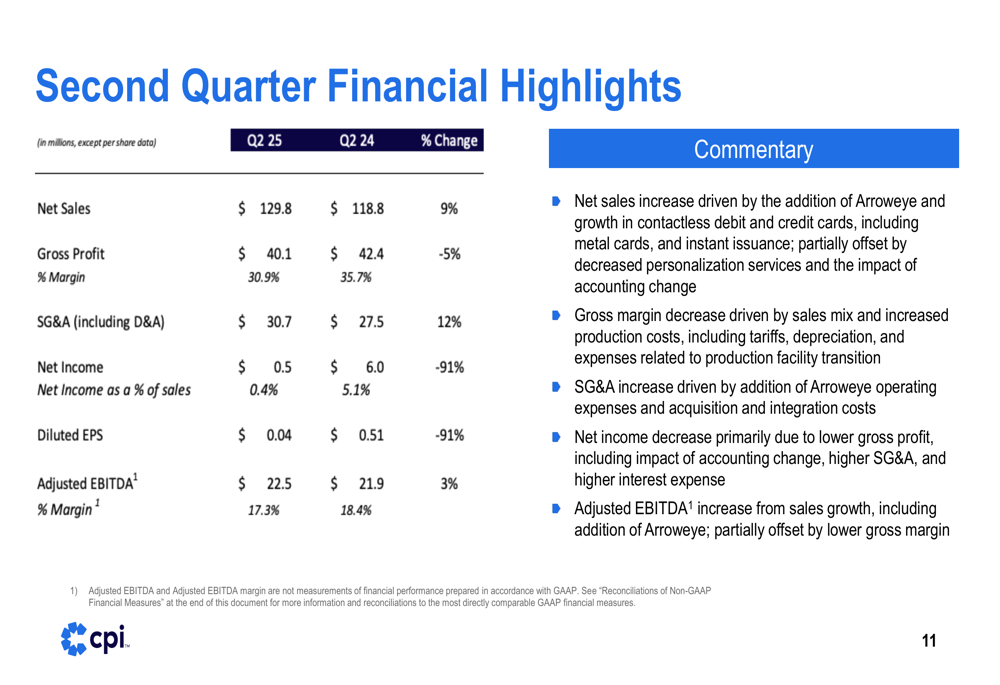

The financial highlights for the second quarter show the stark contrast between revenue growth and profit decline:

Detailed Financial Analysis

CPI’s performance varied significantly between its two main segments. The Debit and Credit segment saw net sales increase from $95.6 million in Q2 2024 to $110.8 million in Q2 2025, though operating income for this segment decreased from $25.4 million to $23.1 million. The Prepaid Debit segment experienced more substantial challenges, with net sales decreasing from $23.8 million to $19.2 million and operating income declining from $6.9 million to $4.2 million.

The segment performance breakdown is shown in the following chart:

Gross profit for the quarter decreased 5% year-over-year, with margin pressures attributed to sales mix and increased production costs, including tariff expenses. SG&A expenses increased 12%, further pressuring the bottom line.

These results continue a concerning trend observed in Q1 2025, when the company reported a decrease in gross profit margin to 33.2% from 37.1% year-over-year, along with operational inefficiencies at its new Indiana facility.

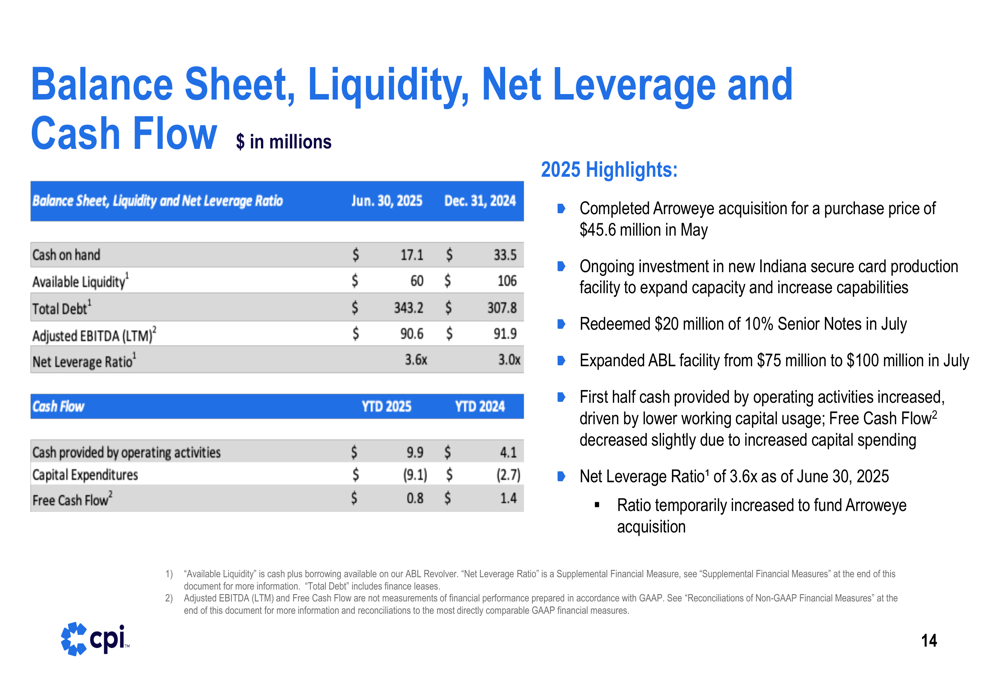

The company’s balance sheet shows available liquidity of $60 million as of June 30, 2025, with total debt of $343.2 million and a net leverage ratio of 3.6x. Free cash flow for the first half of 2025 was just $0.8 million.

Strategic Initiatives

A key strategic development in Q2 was the completion of the Arroweye acquisition for $45.6 million in May 2025. The company describes Arroweye as "off to a strong start," though this acquisition appears to be the corrected name of what was referred to as "AeroEye Solutions" in the Q1 earnings call.

Arroweye expands CPI’s addressable markets by serving complementary customer segments including prepaid program managers, fintechs, banks, and credit unions. The acquisition targets diverse use cases beyond CPI’s primary focus on debit and credit for financial institutions.

The strategic rationale for the Arroweye acquisition is explained in this slide:

CPI continues to invest in long-term growth initiatives, including:

- Card@Once instant issuance

- Entry into closed-loop prepaid packages market in the U.S.

- Expanded healthcare payment card solutions

- Growing interest in other digital solutions

- Sales of metal cards

Forward-Looking Statements

CPI Card Group updated its 2025 outlook, projecting low double-digit to mid-teens increase in net sales, primarily reflecting the addition of Arroweye. The company expects adjusted EBITDA to increase by mid-to-high single digits. Notably, this outlook does not fully reflect potential tariff impacts, which remains a concern for investors.

The company’s updated guidance is shown in the following slide:

Management maintains that long-term growth trends remain intact, citing the growth in U.S. cards in circulation, the recurring nature of the business, and trends toward adoption of higher value contactless cards and secure packaging solutions.

However, investors appear concerned about the company’s ability to translate sales growth into profits, as evidenced by the stock’s premarket decline. With a 52-week trading range of $17.27 to $35.19, PMTS (TSX:PMTS) shares are now trading near the bottom of that range, reflecting growing skepticism about the company’s near-term profitability outlook amid ongoing margin pressures and integration costs associated with the Arroweye acquisition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.