Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Crane Co. (NYSE:CR) presented its first quarter 2025 earnings results on April 29, 2025, showcasing strong performance across its business segments. The company reported significant year-over-year growth in sales, operating profit, and margins, continuing the positive momentum seen in its previous quarter. The results come as Crane maintains its focus on aerospace, defense, and process flow technologies markets, with particularly strong demand in the aerospace sector.

The company’s stock showed positive movement in premarket trading, up 4.27% to $155.02, reflecting investor confidence in the quarterly results and maintained full-year guidance.

Quarterly Performance Highlights

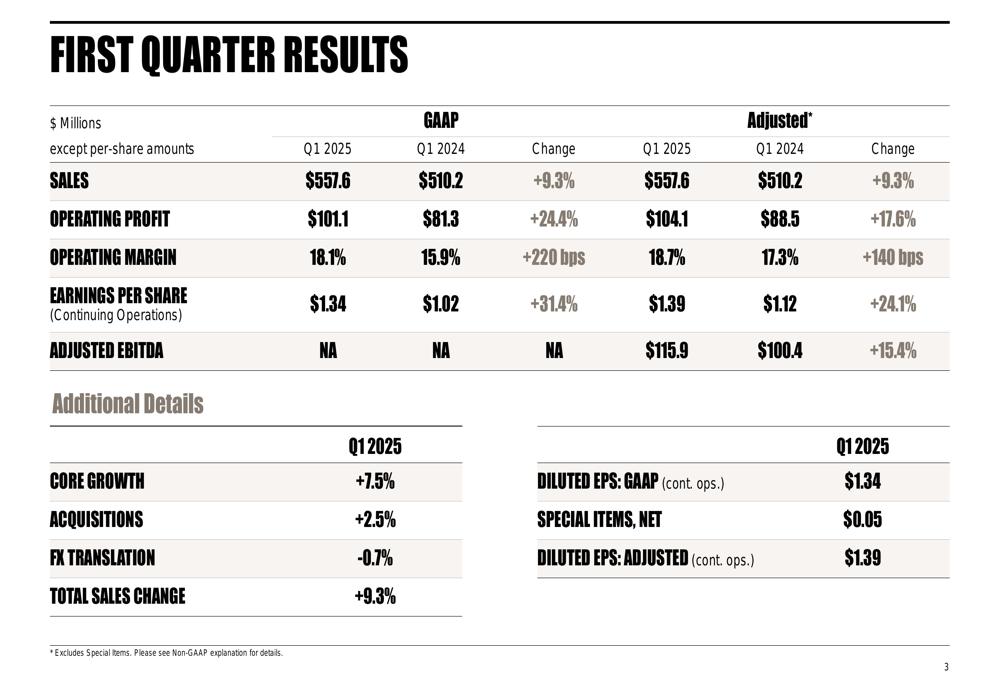

Crane delivered robust financial results for Q1 2025, with sales reaching $557.6 million, a 9.3% increase compared to $510.2 million in Q1 2024. This growth was primarily driven by 7.5% core growth and 2.5% contribution from acquisitions, partially offset by a 0.7% foreign exchange headwind.

The company’s adjusted operating profit rose 17.6% to $104.1 million, with adjusted operating margin expanding 140 basis points to 18.7%. Adjusted earnings per share from continuing operations increased 24.1% to $1.39, compared to $1.12 in the same period last year.

As shown in the following comprehensive financial results table:

Adjusted EBITDA for the quarter reached $115.9 million, representing a 15.4% increase from $100.4 million in Q1 2024. The strong quarterly performance demonstrates Crane’s ability to drive growth while expanding margins, despite ongoing global economic uncertainties.

Segment Analysis

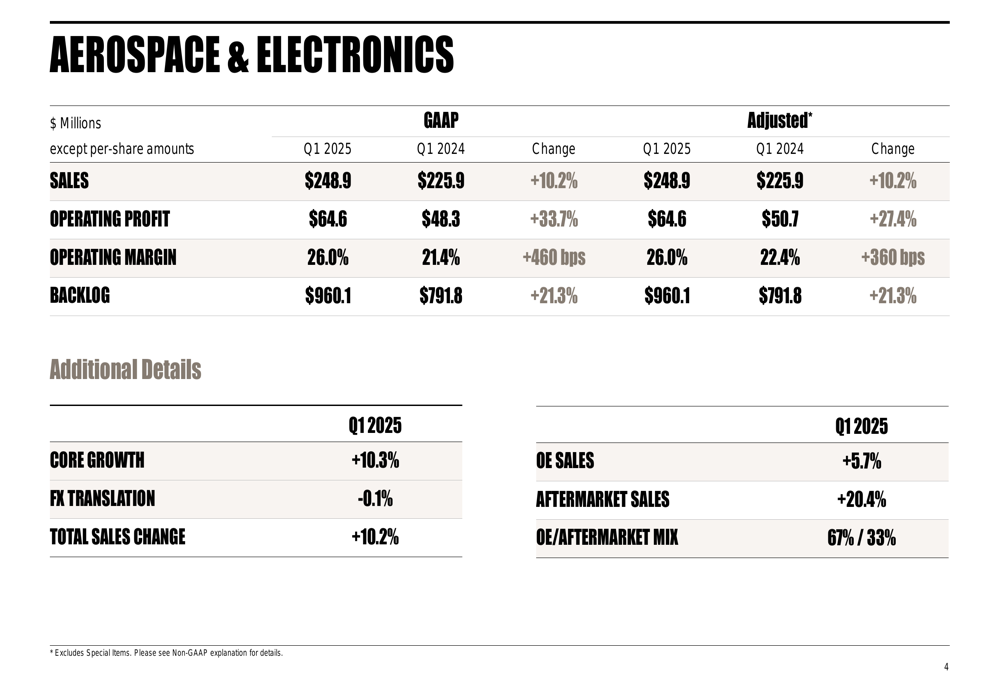

Crane’s Aerospace & Electronics segment was the standout performer in Q1 2025, with sales of $248.9 million, up 10.2% year-over-year. The segment’s operating profit surged 33.7% to $64.6 million, with operating margin expanding an impressive 460 basis points to 26.0%. The segment’s backlog grew 21.3% to $960.1 million, indicating strong future demand.

Particularly noteworthy was the 20.4% growth in aftermarket sales, compared to 5.7% growth in original equipment sales. The segment maintained a 67%/33% mix between OE and aftermarket sales.

The following chart illustrates the Aerospace & Electronics segment’s strong performance:

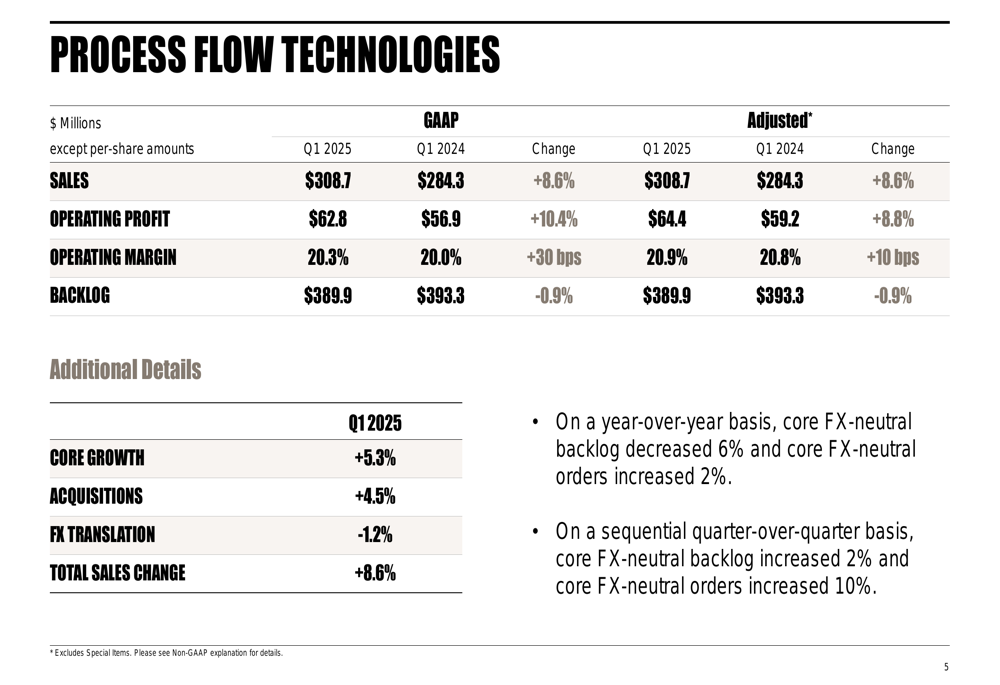

The Process Flow Technologies segment also delivered solid results, with sales increasing 8.6% to $308.7 million. Adjusted operating profit for this segment rose 8.8% to $64.4 million, with adjusted operating margin expanding slightly by 10 basis points to 20.9%. Unlike the Aerospace segment, this division saw a slight 0.9% decrease in backlog to $389.9 million.

The segment’s growth was composed of 5.3% core growth and 4.5% from acquisitions, partially offset by a 1.2% foreign exchange headwind. On a sequential quarter-over-quarter basis, core FX-neutral backlog increased 2% and orders increased 10%, showing improving momentum.

The Process Flow Technologies segment performance is detailed in the following chart:

Financial Position & Capital Allocation

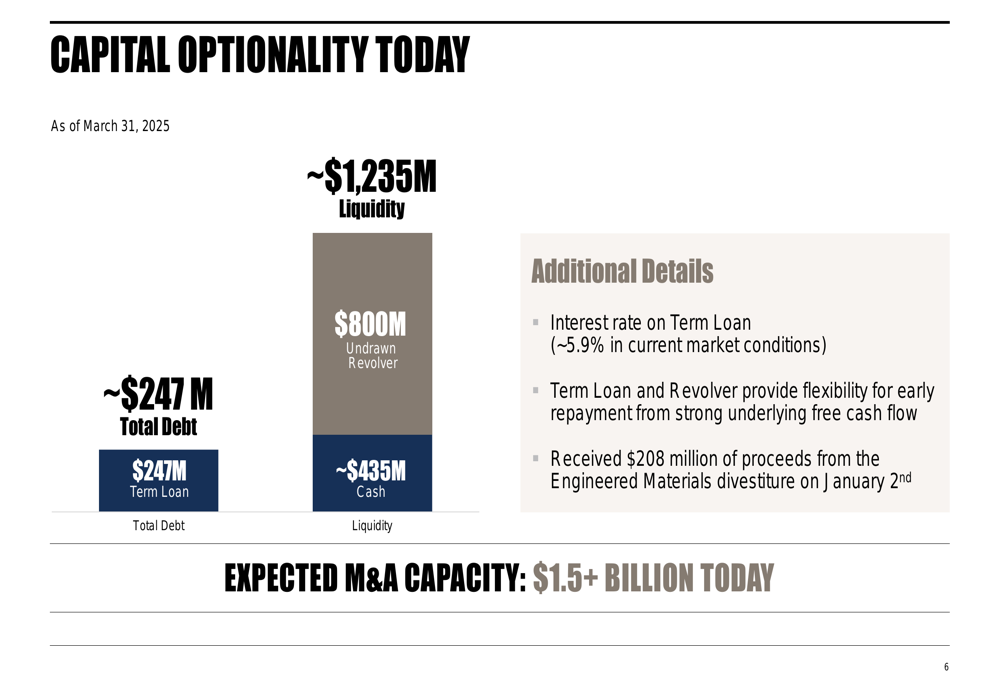

Crane maintained a strong financial position at the end of Q1 2025, with approximately $1,235 million in total liquidity, consisting of $800 million in undrawn revolving credit and approximately $435 million in cash. The company’s total debt stood at approximately $247 million, comprised entirely of a term loan with an interest rate of about 5.9%.

The company received $208 million in proceeds from the Engineered Materials divestiture on January 2nd, further strengthening its financial flexibility. With its current balance sheet strength, Crane estimates it has over $1.5 billion in M&A capacity available for strategic acquisitions.

The following chart details Crane’s capital position:

This strong financial position provides Crane with significant optionality for capital deployment, including potential acquisitions, investments in organic growth initiatives, and returns to shareholders.

Forward Guidance & Strategic Outlook

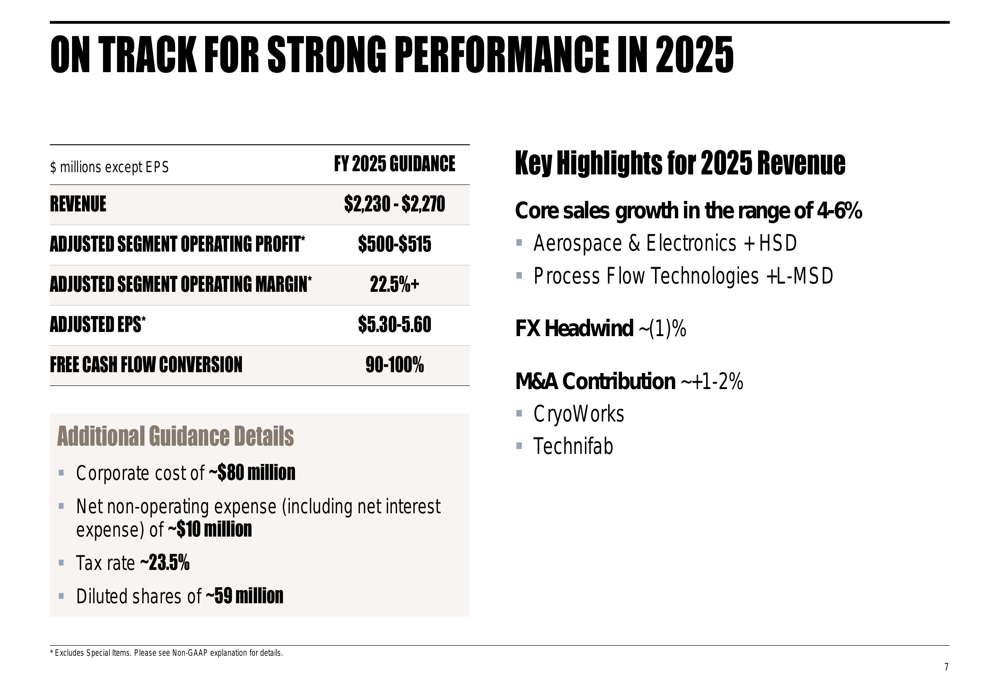

Crane maintained its full-year 2025 guidance, projecting revenue between $2,230 million and $2,270 million, with adjusted segment operating profit of $500-$515 million. The company expects adjusted EPS in the range of $5.30-$5.60, consistent with the outlook provided in its previous quarter.

For 2025, Crane anticipates core sales growth of 4-6%, driven by high single-digit growth in Aerospace & Electronics and low to mid-single-digit growth in Process Flow Technologies. The company expects a 1% foreign exchange headwind and a 1-2% contribution from the CryoWorks and Technifab acquisitions.

The company’s 2025 guidance is summarized in the following chart:

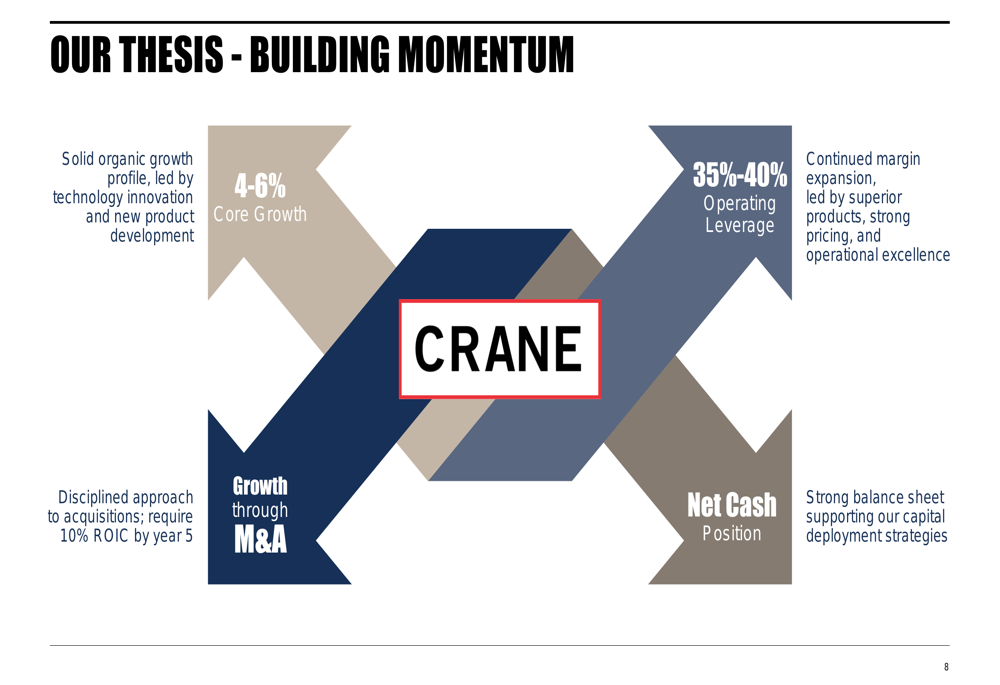

Strategically, Crane is focused on building momentum through four key pillars: organic growth through technology innovation and new product development, disciplined acquisitions targeting 10% ROIC by year five, margin expansion through superior products and operational excellence, and maintaining a strong balance sheet to support capital deployment.

The company’s strategic thesis is illustrated in the following chart:

Crane’s Q1 2025 results demonstrate continued execution against these strategic priorities, with strong organic growth, margin expansion, and a solid financial position supporting future growth initiatives. The company appears well-positioned to capitalize on strong demand in its key markets, particularly in aerospace and defense, while maintaining financial flexibility for strategic acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.