S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Crocs Inc. (NASDAQ:CROX) released its first quarter 2025 investor presentation on May 8, revealing better-than-expected results despite a challenging macroeconomic environment. The casual footwear giant has withdrawn its full-year 2025 guidance due to uncertainties in the global trade landscape, even as its core Crocs brand continues to show strength, particularly in international markets.

Quarterly Performance Highlights

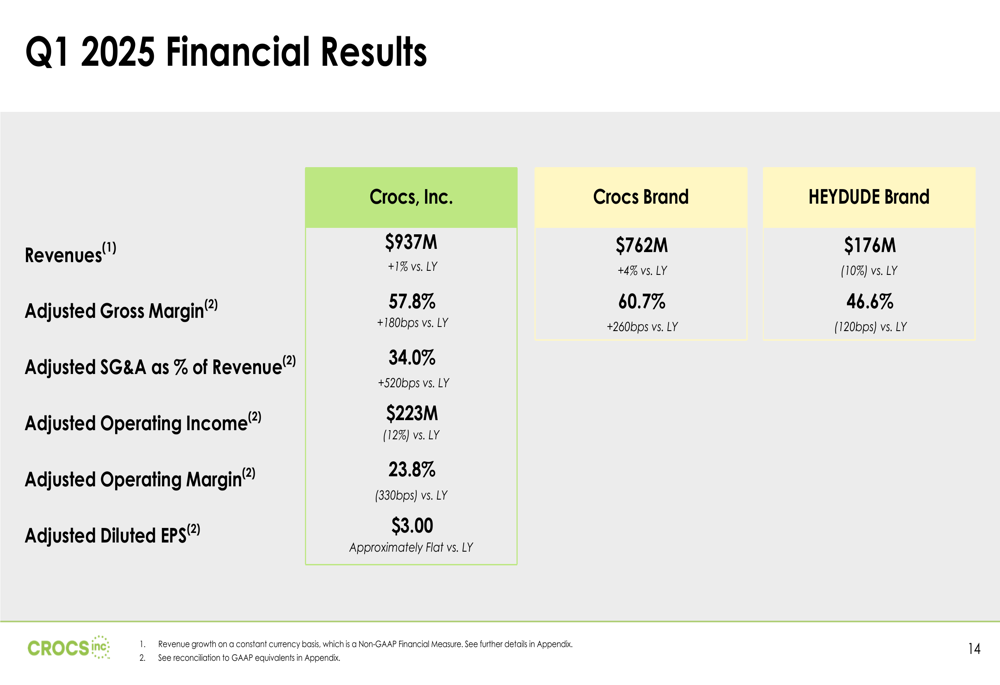

Crocs reported Q1 2025 revenue of $937 million, representing a modest 1% year-over-year increase, while delivering an adjusted diluted earnings per share of $3.00, approximately flat compared to the prior year. The company’s adjusted gross margin improved significantly to 57.8%, up 180 basis points from Q1 2024.

"We are pleased to report better-than-expected first quarter results despite the volatile macroeconomic backdrop," said Andrew Rees, Chief Executive Officer. "Both our Crocs and HEYDUDE brands contributed to strong margins, earnings per share, and cash flow generation."

The company’s performance shows a continuation of trends observed in the previous quarter, though at a more moderate pace. In Q4 2024, Crocs had reported stronger results with revenue of $990 million and EPS of $2.52, which had triggered an 18.55% stock surge. By comparison, CROX is trading up 3.71% in premarket activity following the Q1 results.

As shown in the following comprehensive financial summary:

Detailed Financial Analysis

The Q1 results revealed divergent performance between the company’s two brands. The Crocs brand demonstrated solid growth with revenue of $762 million, up 4% year-over-year, while HEYDUDE experienced a 10% decline to $176 million. This brand disparity highlights the challenges and opportunities facing the company.

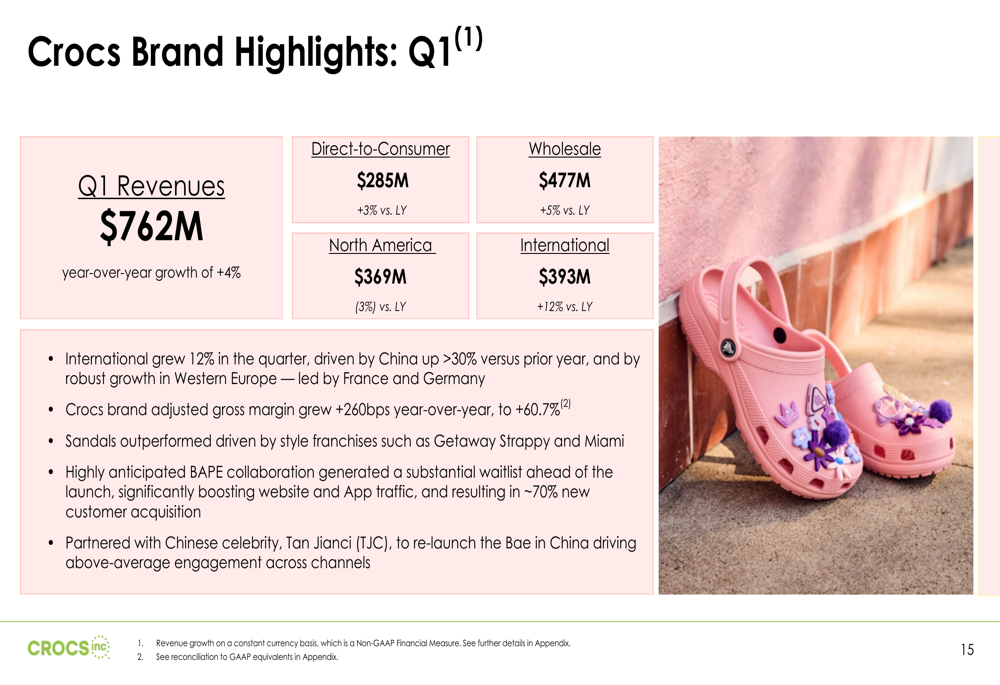

The Crocs brand showed particular strength in international markets, which grew 12% year-over-year to $393 million, offsetting a 3% decline in North America to $369 million. The brand’s gross margin improved significantly to 60.7%, up 260 basis points from the previous year.

The following slide details the Crocs brand performance:

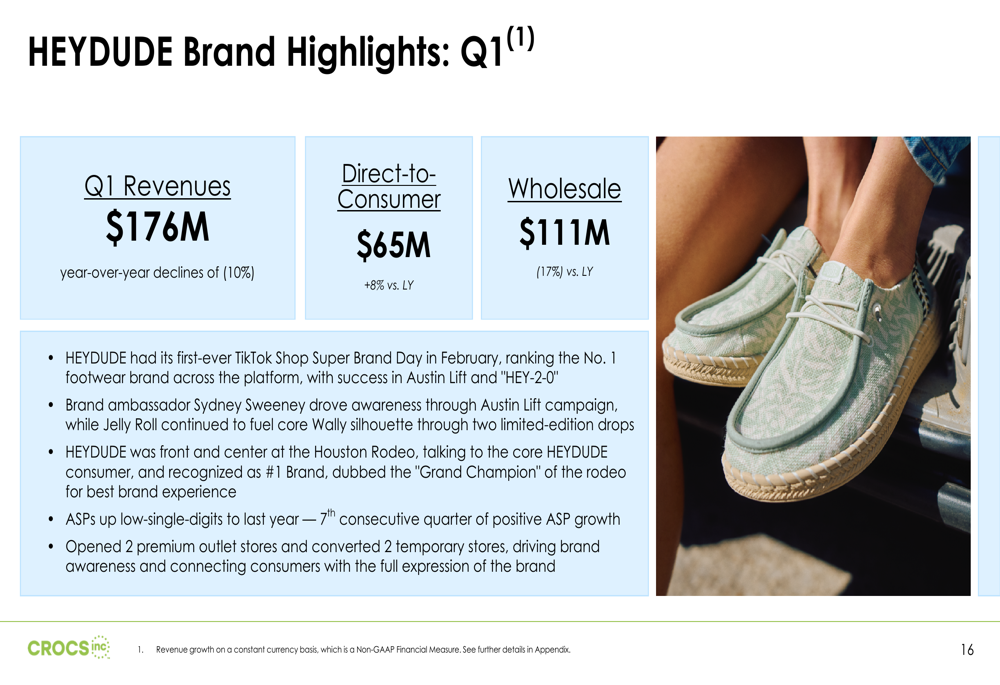

Meanwhile, HEYDUDE’s performance reflected ongoing challenges, with wholesale revenue declining 17% to $111 million. However, the brand’s direct-to-consumer channel showed promising growth of 8% to $65 million, suggesting that HEYDUDE’s consumer appeal remains strong despite wholesale distribution challenges.

The HEYDUDE brand highlights are illustrated here:

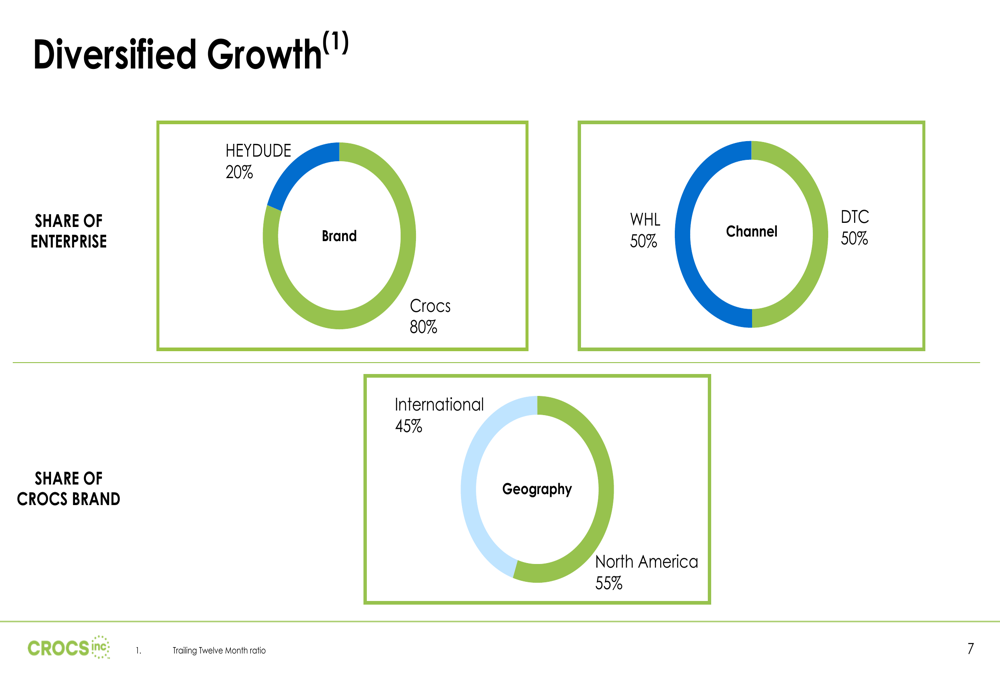

From a channel perspective, Crocs maintains a balanced approach with wholesale and direct-to-consumer each representing approximately 50% of enterprise revenue. This diversification provides resilience against channel-specific disruptions.

The company’s diversified growth strategy is visualized in the following chart:

Despite solid top-line performance, Crocs faced increased operational costs, with adjusted SG&A as a percentage of revenue rising significantly to 34.0%, an increase of 520 basis points year-over-year. This contributed to a 12% decline in adjusted operating income to $223 million and a 330 basis point contraction in adjusted operating margin to 23.8%.

Strategic Initiatives

Crocs outlined its investment thesis and growth strategies for both brands in the presentation. The company positions itself as a global leader in casual footwear with two iconic brands addressing a total addressable market exceeding $160 billion.

The strategic framework emphasizes:

For the Crocs brand specifically, the company is focusing on driving brand relevance through icon iterations, gaining market share outside of clogs, leveraging digital marketing, and expanding globally. The international growth evident in Q1 results aligns with this strategic direction.

For HEYDUDE, Crocs aims to create a brand community connecting with youth female culture while maintaining its male fan base, build core products, and stabilize North American business while laying groundwork for international expansion.

The company’s capital allocation priorities remain focused on investing in its brands, reducing debt to maintain a net leverage target range of 1.0x to 1.5x, and opportunistically repurchasing shares under its existing $1.3 billion buyback authorization.

These priorities are detailed in the following slide:

Forward-Looking Statements

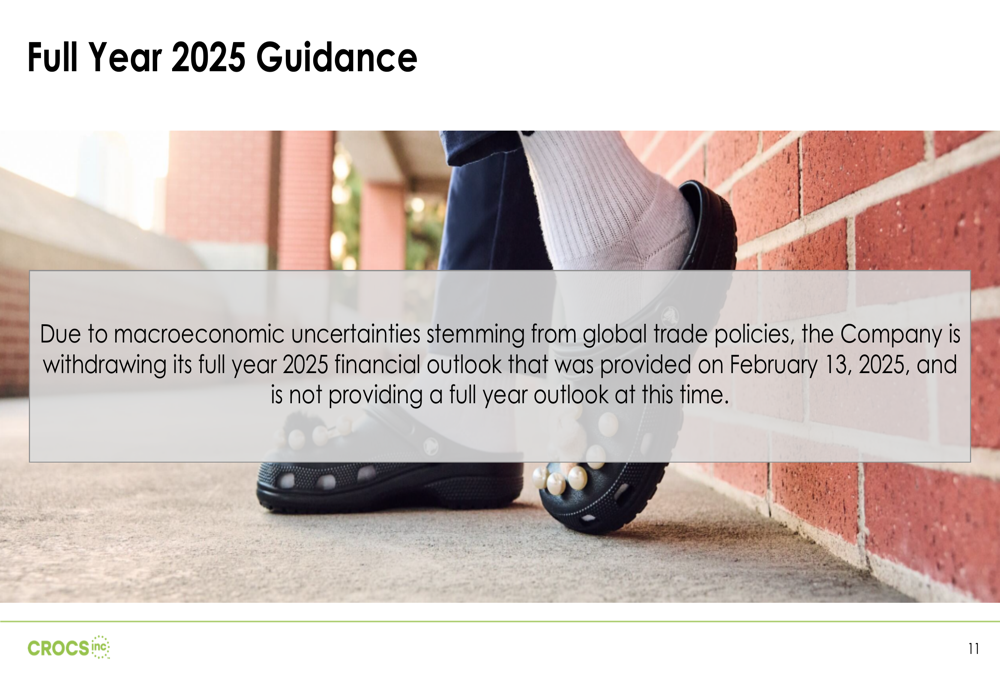

In a significant development, Crocs has withdrawn its full-year 2025 financial outlook that was provided on February 13, 2025. The company cited "macroeconomic uncertainties stemming from global trade policies" as the reason for this decision.

This withdrawal comes after the company had previously projected enterprise revenue growth of 2-2.5% for 2025, with the Crocs brand expected to grow by approximately 4.5% and the HEYDUDE brand anticipated to decline by 7-9%.

The decision to withdraw guidance suggests heightened uncertainty about the impact of evolving trade policies on the company’s supply chain, pricing, and market access. Despite these uncertainties, management expressed confidence in the company’s ability to navigate challenges and potentially gain market share.

"We remain committed to delivering value to our shareholders, consumers, and customers," Rees stated. "We believe we are well-positioned to gain market share in this environment."

Investors will likely look for additional clarity on these trade-related concerns and their potential impact on Crocs’ operations during the company’s earnings call and in subsequent communications.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.