Intel stock spikes after report of possible US government stake

Introduction & Market Context

CSG Systems International (NASDAQ:CSGS) released its Q1 2025 earnings presentation on May 7, 2025, highlighting strong profitability improvements despite modest revenue growth. The company’s shares closed at $60.44 and rose 1.72% in after-hours trading to $62.25, reflecting positive market reception to the results and raised guidance.

The business solutions provider continues to execute on its strategy of diversifying beyond its traditional cable and telecom customer base while focusing on operational efficiencies to drive margin expansion and shareholder returns.

Quarterly Performance Highlights

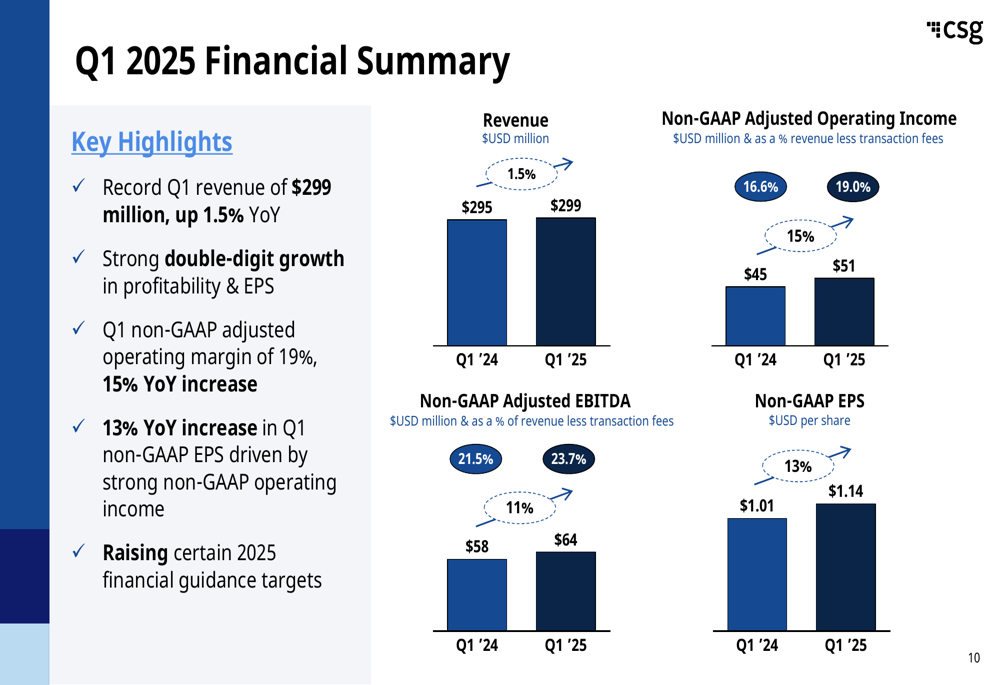

CSG reported record Q1 revenue of $299 million, representing a 1.5% year-over-year increase. More impressively, the company achieved substantial profit growth with non-GAAP adjusted operating income of $51 million, translating to a 19.0% margin – a 240 basis point improvement compared to the same period last year.

Non-GAAP earnings per share reached $1.14, up 13% year-over-year, driven primarily by the strong operating income performance. Non-GAAP adjusted EBITDA was $64 million, representing a 23.7% margin.

As shown in the following chart detailing CSG’s Q1 2025 financial performance:

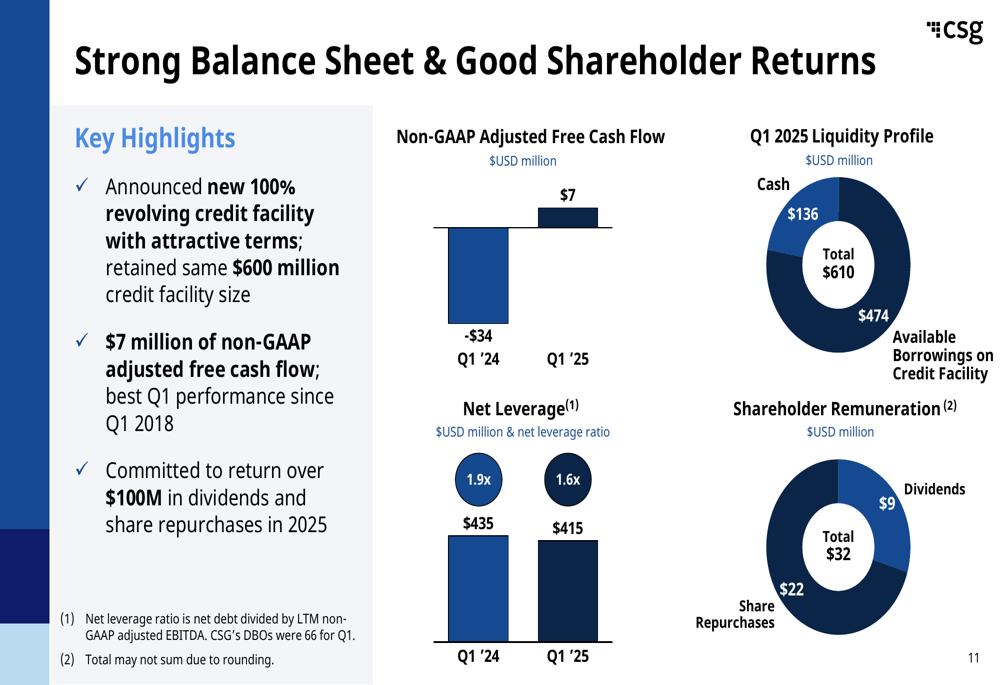

The company’s adjusted free cash flow showed significant improvement, reaching $7 million in Q1 2025 compared to negative $34 million in Q1 2024. According to management, this represents the best first-quarter free cash flow performance since 2018.

Revenue Diversification Strategy

A key pillar of CSG’s long-term strategy has been reducing its dependence on the cable and pay TV sectors. The company has made substantial progress in this area, with 33% of Q1 revenue now coming from industries outside cable and telecom, up from just 23% in fiscal 2017.

The following visualization illustrates this transformation in CSG’s revenue mix:

The diversification strategy has been driven by growth in CSG’s SaaS products, particularly in data-driven customer experience and payments solutions. The company emphasizes that it can leverage similar customer business needs across different verticals, allowing it to expand its addressable market while maintaining operational focus.

Profitability and Cash Flow Improvements

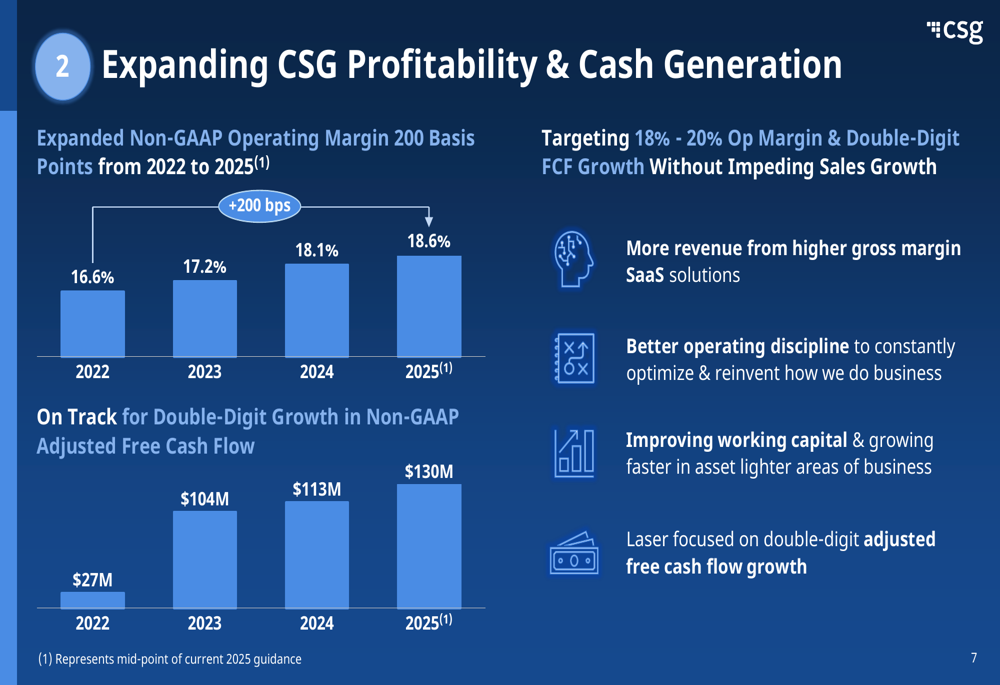

CSG has consistently improved its profitability metrics over the past several years. The company has expanded its non-GAAP operating margin by 200 basis points since 2022, from 16.6% to a projected 18.6% in 2025. This improvement has been accompanied by double-digit growth in adjusted free cash flow, which is expected to reach $130 million in 2025, up from just $27 million in 2022.

The following chart demonstrates this consistent improvement in profitability and cash generation:

Management attributes these improvements to several factors, including a shift toward higher-margin SaaS solutions, better operating discipline, improved working capital management, and growth in asset-lighter areas of the business.

Shareholder Returns and M&A Activity

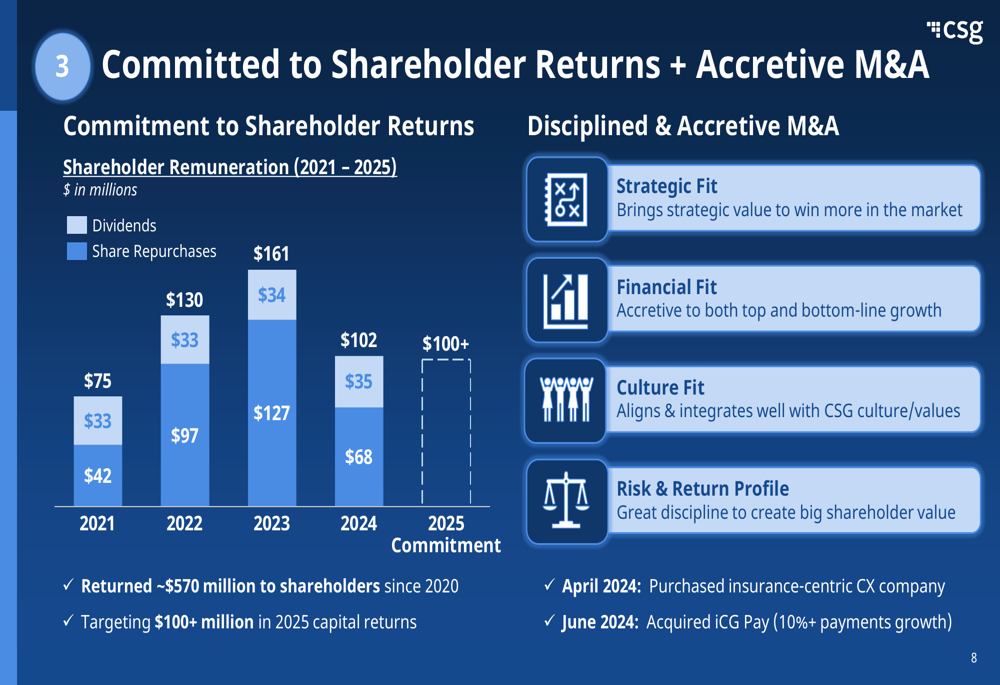

CSG maintains a strong commitment to shareholder returns while pursuing strategic acquisitions. The company has returned approximately $570 million to shareholders since 2020 through dividends and share repurchases. In Q1 2025 alone, CSG returned $32 million to shareholders ($9 million in dividends and $22 million in share repurchases).

The company also announced its 12th consecutive annual dividend increase, with a 7% increase for 2025. CSG has committed to returning over $100 million to shareholders in 2025.

As shown in the following chart detailing CSG’s shareholder remuneration history:

On the M&A front, CSG has been active in 2024, acquiring an insurance-centric customer experience company in April and iCG Pay in June, the latter supporting the company’s payments growth strategy. Management emphasized their disciplined approach to acquisitions, focusing on strategic fit, financial accretion, cultural alignment, and risk-return profile.

Strong Balance Sheet

CSG maintains a solid financial position with improving leverage metrics. The company announced a new 100% revolving credit facility with the same $600 million capacity but more attractive terms. Net leverage decreased from 1.9x in Q1 2024 to 1.6x in Q1 2025, with net debt declining from $435 million to $415 million.

The company’s Q1 2025 liquidity profile includes $136 million in cash and $474 million in available borrowings on its credit facility, providing substantial flexibility for future investments and shareholder returns.

As illustrated in the following financial strength indicators:

Forward-Looking Statements

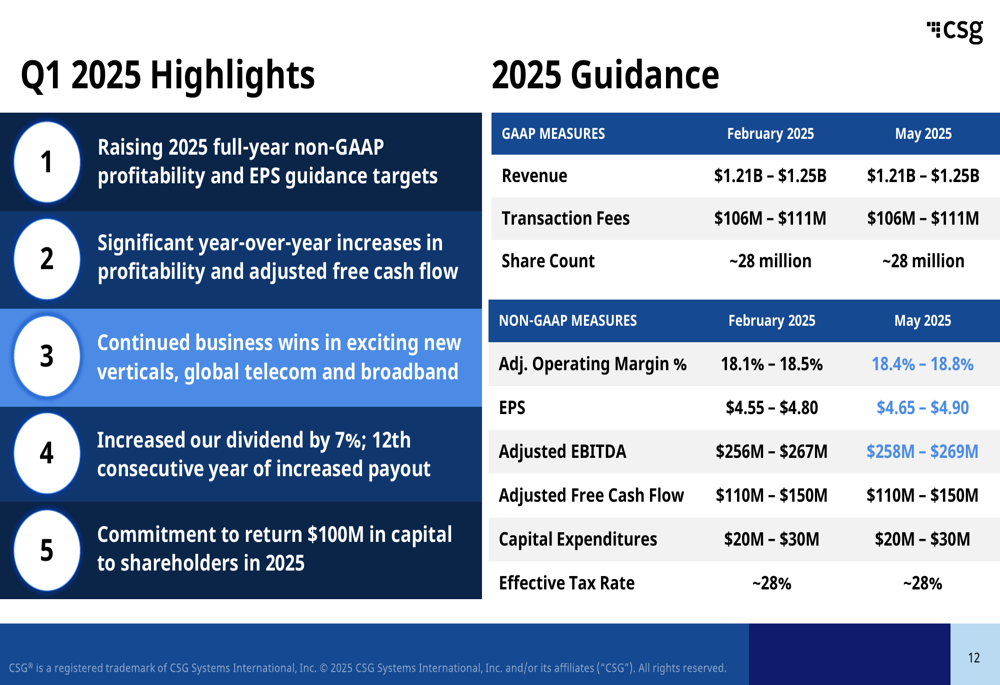

Based on its strong Q1 performance, CSG has raised certain elements of its 2025 financial guidance. The company now expects:

- Revenue of $1.21 billion to $1.25 billion

- Non-GAAP adjusted operating margin of 18.4% to 18.8% (raised from previous guidance)

- Non-GAAP EPS of $4.65 to $4.90 (raised from previous guidance)

- Adjusted EBITDA of $258 million to $269 million

- Adjusted free cash flow of $110 million to $150 million

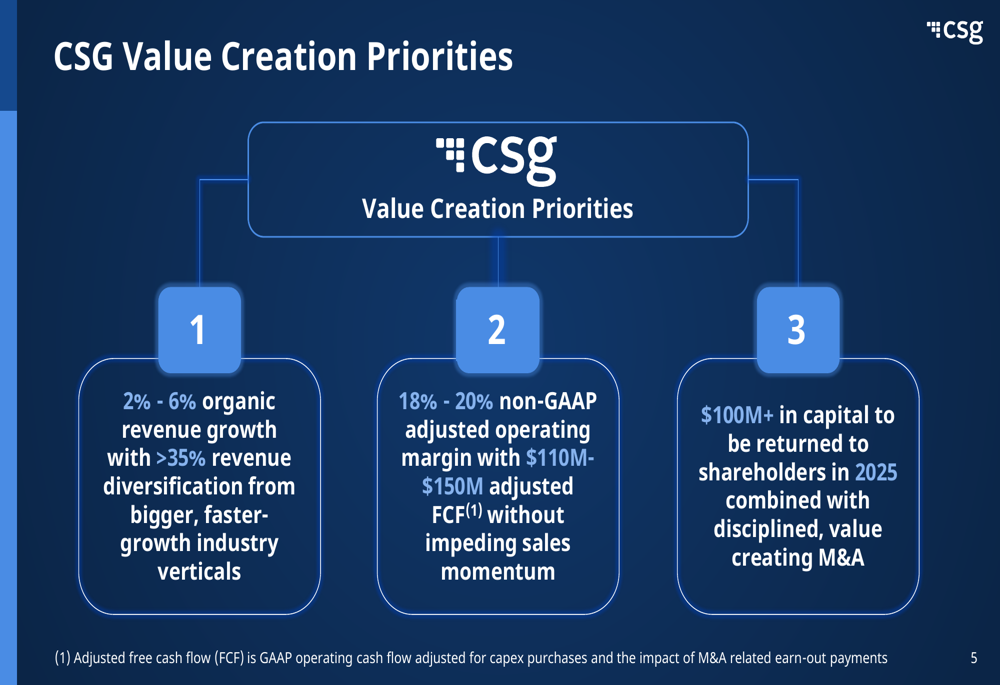

The company’s value creation priorities remain focused on:

1. Achieving 2%-6% organic revenue growth with over 35% revenue diversification from faster-growth industry verticals

2. Maintaining 18%-20% non-GAAP adjusted operating margins with $110M-$150M adjusted free cash flow

3. Returning $100M+ to shareholders in 2025 while pursuing disciplined, value-creating M&A

As detailed in the company’s strategic priorities framework:

CSG’s updated 2025 guidance reflects management’s confidence in continued execution of its strategy:

The company appears well-positioned to continue its trajectory of modest revenue growth, expanding profitability, and consistent shareholder returns as it executes on its diversification strategy and operational improvements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.