S&P500 rises as Nvidia lifts tech, Fed minutes points to more rate cuts ahead

Introduction & Market Context

CTT Correios de Portugal SA (LISBON:ELI:CTT) shares fell 11.92% following the release of its first quarter 2025 results on May 9, despite reporting strong operational performance. The Portuguese postal and logistics company posted significant revenue and EBIT growth, though net profit declined year-over-year.

The company’s results reflect the ongoing transformation of its business model, with continued growth in Express & Parcels and Financial Services offsetting structural declines in traditional mail services. CTT also announced the completion of its acquisition of Cacesa, strengthening its international position.

Quarterly Performance Highlights

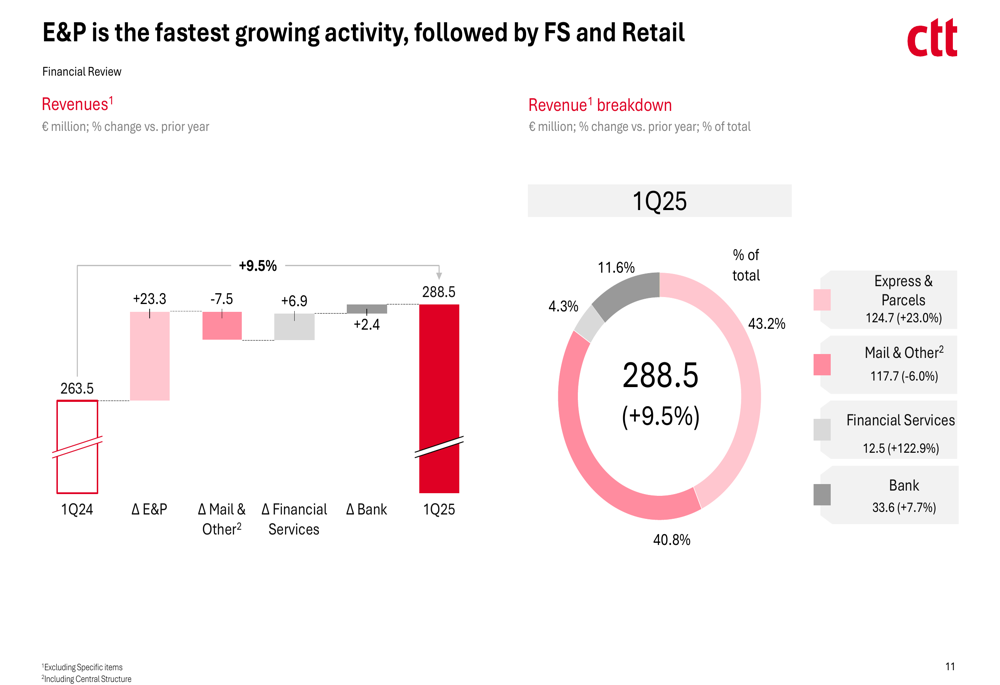

CTT reported revenues of €288.5 million in Q1 2025, representing a 9.5% increase compared to the same period last year. Recurring EBIT grew by 19.5% to €20.2 million, demonstrating improved operational efficiency despite rising costs.

As shown in the following financial performance summary, while top-line and operational metrics improved, net profit attributable to equity holders decreased by 25.9% to €5.5 million, and free cash flow declined by 41% to €2.3 million:

The revenue breakdown reveals Express & Parcels as the largest contributor at 43.2% of total revenue, followed by Mail & Other at 40.8%, Bank at 11.6%, and Financial Services at 4.3%. This distribution highlights CTT’s ongoing transition from a traditional postal operator to a diversified logistics and financial services provider.

As illustrated in this revenue breakdown by business segment:

Segment Analysis

Express & Parcels

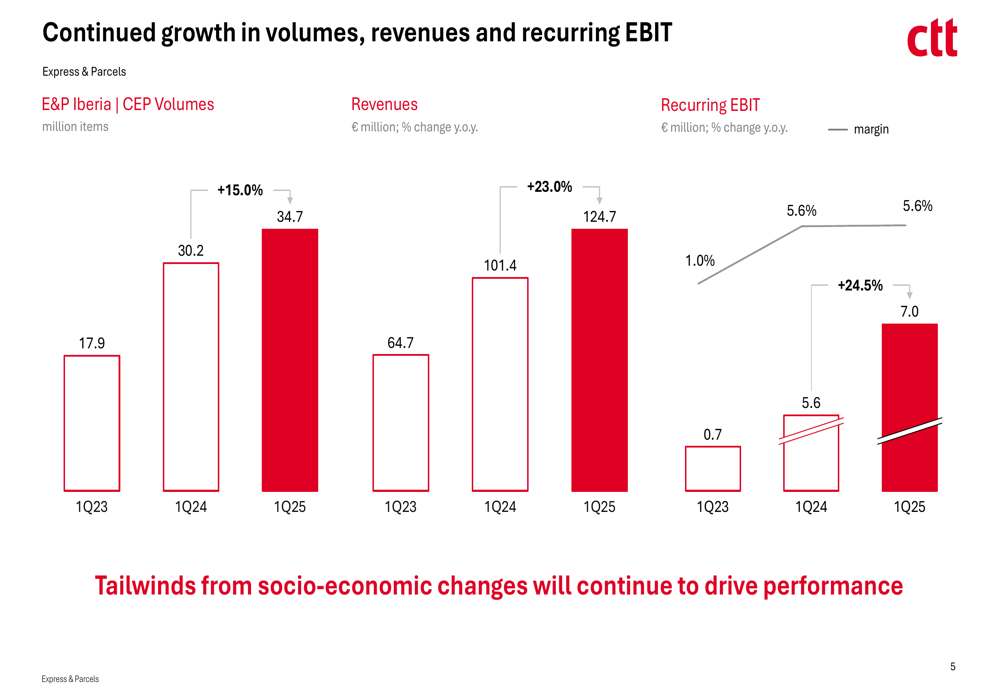

The Express & Parcels segment continued its strong performance, with volumes increasing to 34.7 million items in Q1 2025, up from 30.2 million in Q1 2024. This volume growth translated into a 23% revenue increase to €124.7 million, with recurring EBIT reaching €7.0 million, representing a 24.5% increase and a 5.6% margin.

The following chart demonstrates the consistent growth trajectory in this segment over the past three years:

Mail & Other

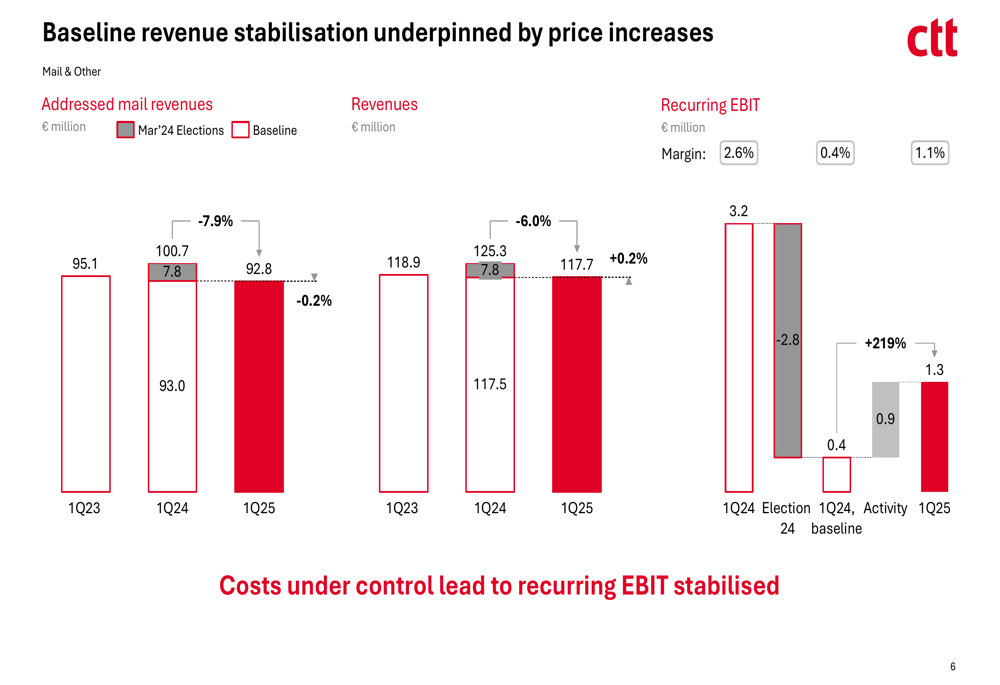

The traditional mail business continues to face structural challenges, with addressed mail revenues declining 7.9% year-over-year when excluding the impact of the March 2024 elections. Overall Mail & Other revenues decreased by 6.0% to €117.7 million. Despite this decline, the segment maintained positive recurring EBIT of €1.3 million, though this represents a significant decrease from the €3.2 million reported in Q1 2024.

As shown in the following chart, price increases have helped stabilize the baseline revenue despite volume declines:

Financial Services

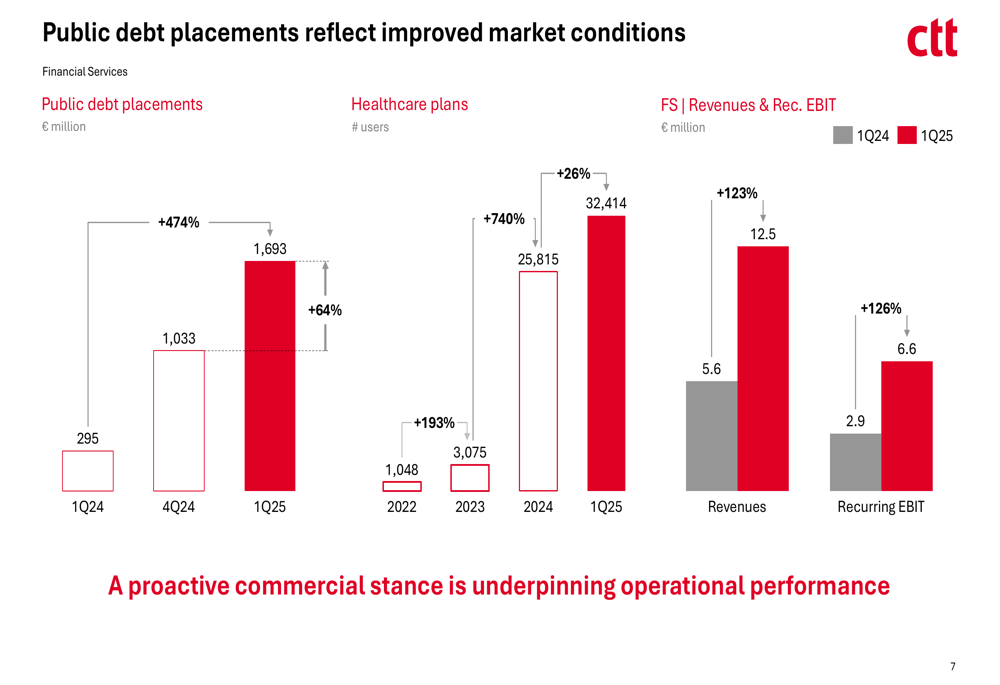

Financial Services emerged as a standout performer, with revenues more than doubling to €12.5 million (+123%) and recurring EBIT increasing by 126% to €6.6 million. This growth was primarily driven by public debt placements, which surged to €1,693 million in Q1 2025, a dramatic increase from €295 million in Q1 2024.

The following chart illustrates the exceptional growth in public debt placements and healthcare plan users:

Bank

Banco CTT continued its steady growth trajectory, with revenues increasing by 7.7% to €33.6 million. Business volumes grew to €7,081 billion, up from €6,192 billion in Q1 2024. The bank is investing in key platforms and retail stores to drive future growth.

Strategic Initiatives

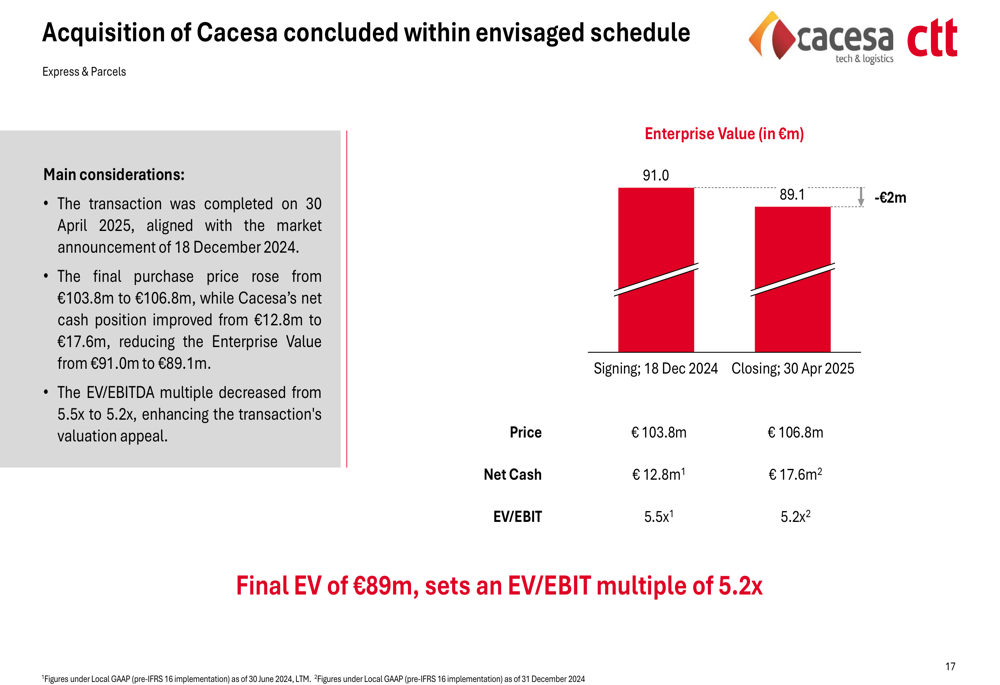

A key strategic development in the quarter was the completion of the Cacesa acquisition on April 30, 2025. The final purchase price was €106.8 million, slightly higher than the initially announced €103.8 million. However, due to Cacesa’s improved net cash position, the enterprise value (EV) decreased to €89 million, resulting in a more favorable EV/EBITDA multiple of 5.2x, down from the originally expected 5.5x.

The following slide details the final terms of the Cacesa acquisition:

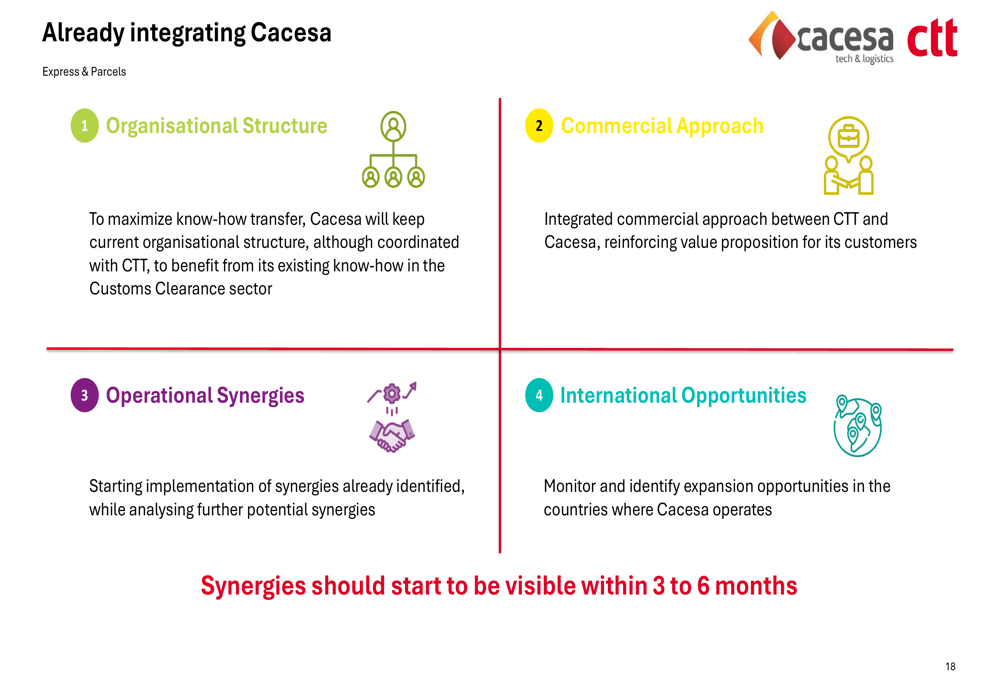

CTT outlined its integration plan for Cacesa, focusing on organizational structure, commercial approach, operational synergies, and international opportunities:

Operating Costs and EBIT Analysis

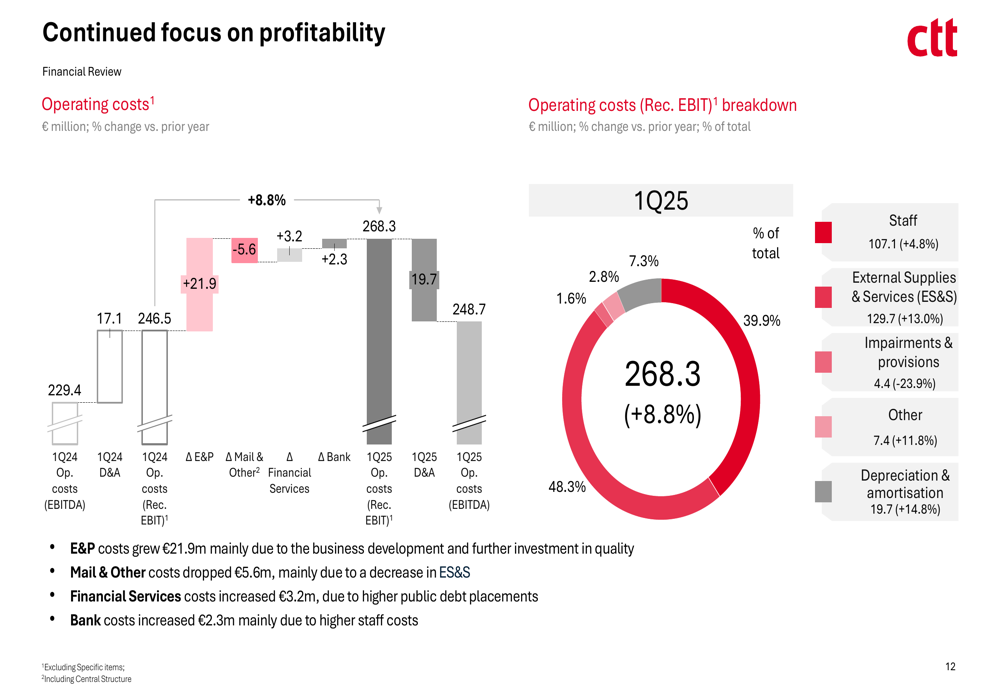

Operating costs increased by 8.4% to €248.7 million, with External Supplies & Services representing the largest component at 48.3% of total costs. Staff costs grew by 4.8% to €107.1 million, while depreciation and amortization increased by 14.8% to €19.7 million.

The cost breakdown by category is illustrated in the following chart:

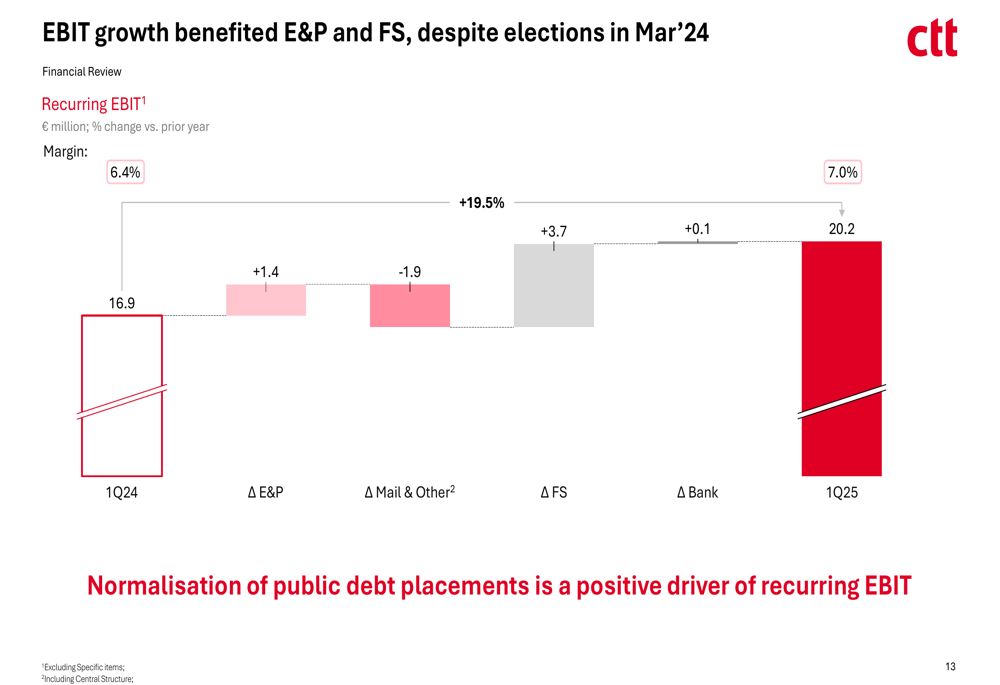

The growth in recurring EBIT was primarily driven by Financial Services, which contributed an additional €3.7 million. Express & Parcels added €1.4 million, while Mail & Other had a negative impact of -€1.9 million.

As shown in the EBIT growth analysis:

Forward-Looking Statements

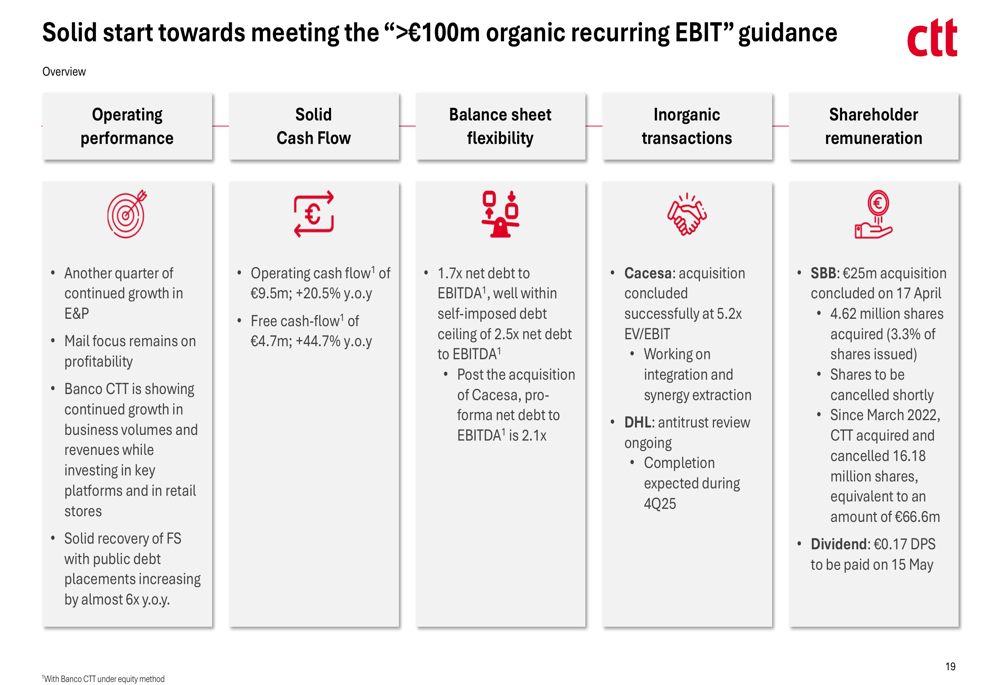

CTT reaffirmed its guidance of achieving over €100 million in organic recurring EBIT. The company emphasized that its solid cash flow generation and balance sheet flexibility position it well for both organic growth and potential additional acquisitions.

The company’s strategy continues to focus on growing its Express & Parcels and Financial Services businesses while managing the decline in traditional mail services. The integration of Cacesa is expected to strengthen CTT’s international presence and create operational synergies.

As summarized in CTT’s key takeaways:

Despite the positive operational performance and strategic developments, investors reacted negatively to the results, focusing on the decline in net profit and free cash flow. The stock closed at €6.80, down 11.92% from the previous close of €7.72, suggesting market concerns about the company’s bottom-line performance despite the improved operational metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.