Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

CTT Correios de Portugal SA (LISBON:ELI:CTT) presented its second quarter 2025 results on July 28, showing accelerating growth across key metrics as the company continues its transformation from a traditional postal operator into a diversified e-commerce logistics player.

The company’s stock closed at €7.56 on July 28, down 0.92% for the day, but remains significantly above its 52-week low of €4.02 and near its 52-week high of €8.14, indicating investor confidence in the company’s strategic direction despite some daily volatility.

The results represent a significant turnaround from Q1 2025, when the company reported a 25.9% decline in net income that triggered an 11.14% stock price drop. This quarter’s strong performance suggests CTT’s strategic initiatives and acquisitions are beginning to deliver the anticipated benefits.

Quarterly Performance Highlights

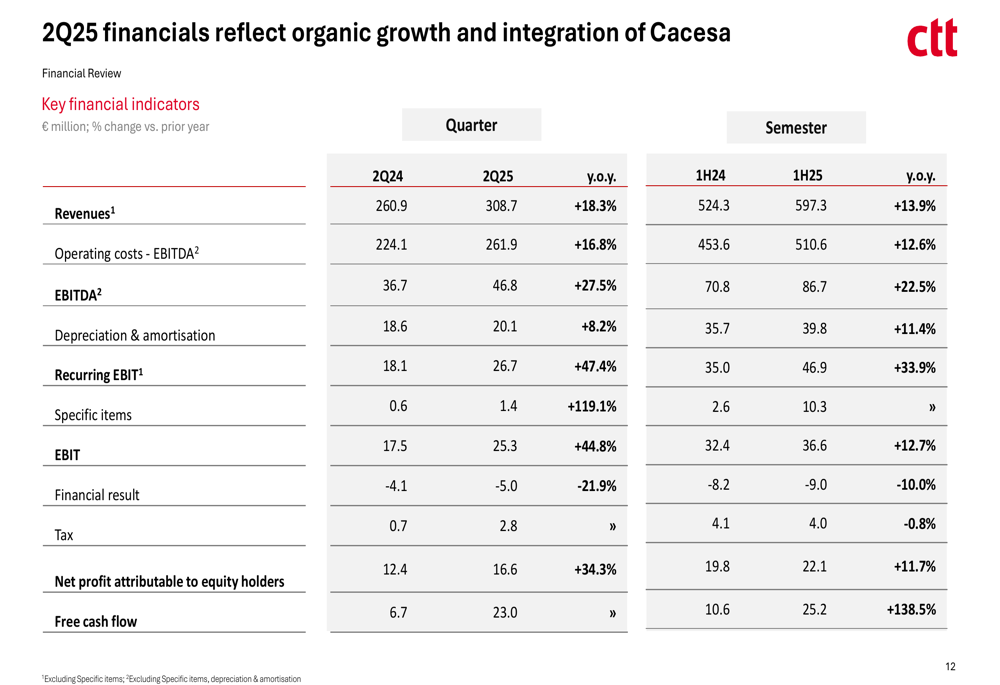

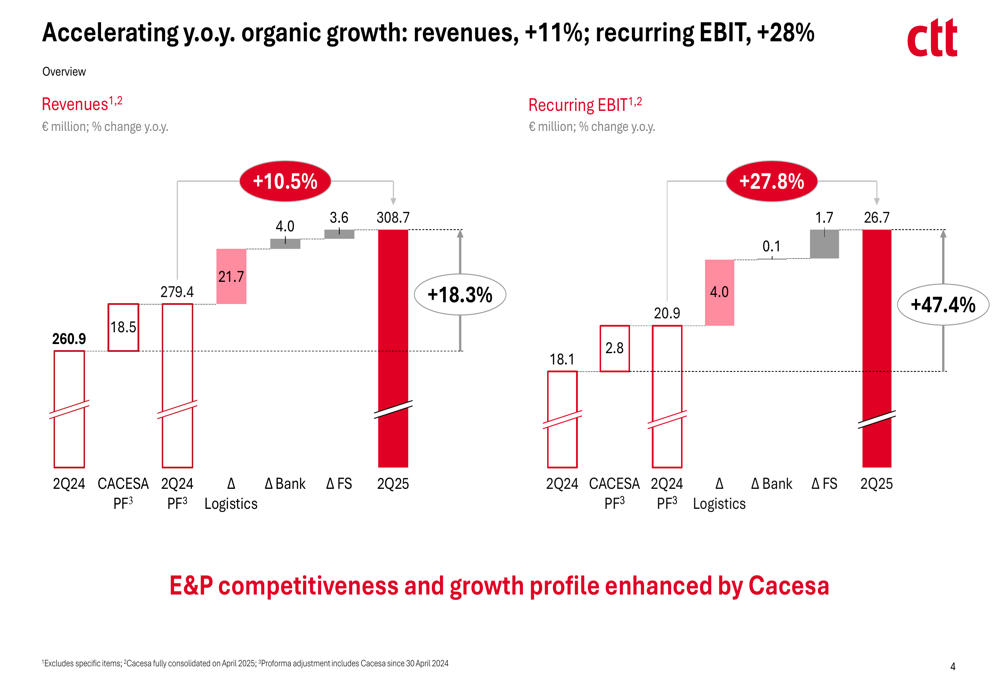

CTT reported substantial growth across all key financial metrics for Q2 2025, with revenues increasing by 18.3% year-over-year to €308.7 million and recurring EBIT jumping 47.4% to €26.7 million. Net profit rose 34.3% to €16.6 million, while free cash flow showed significant improvement.

As shown in the following comprehensive financial overview from the presentation:

The company’s operating costs increased by 16.8% to €261.9 million, primarily due to the integration of Cacesa and investments in quality improvements. Despite these higher costs, EBITDA grew by 27.5% to €46.8 million, demonstrating improved operational efficiency.

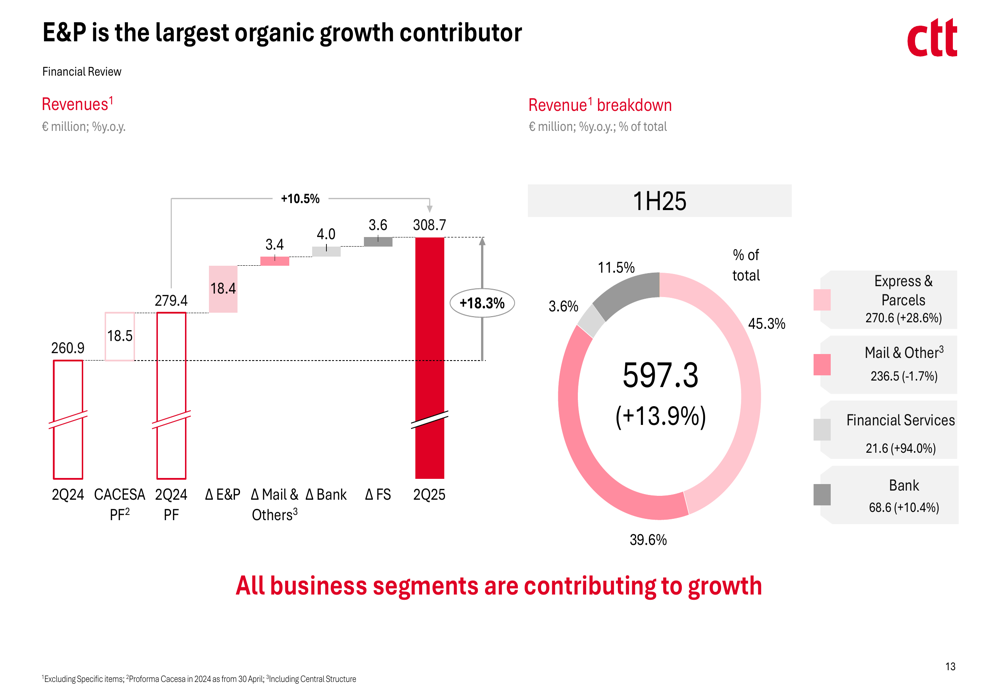

CTT’s revenue growth was driven primarily by its Express & Parcels (E&P) segment, which now represents 45.3% of total revenue. The following chart illustrates the company’s revenue breakdown and growth drivers:

Segment Performance Analysis

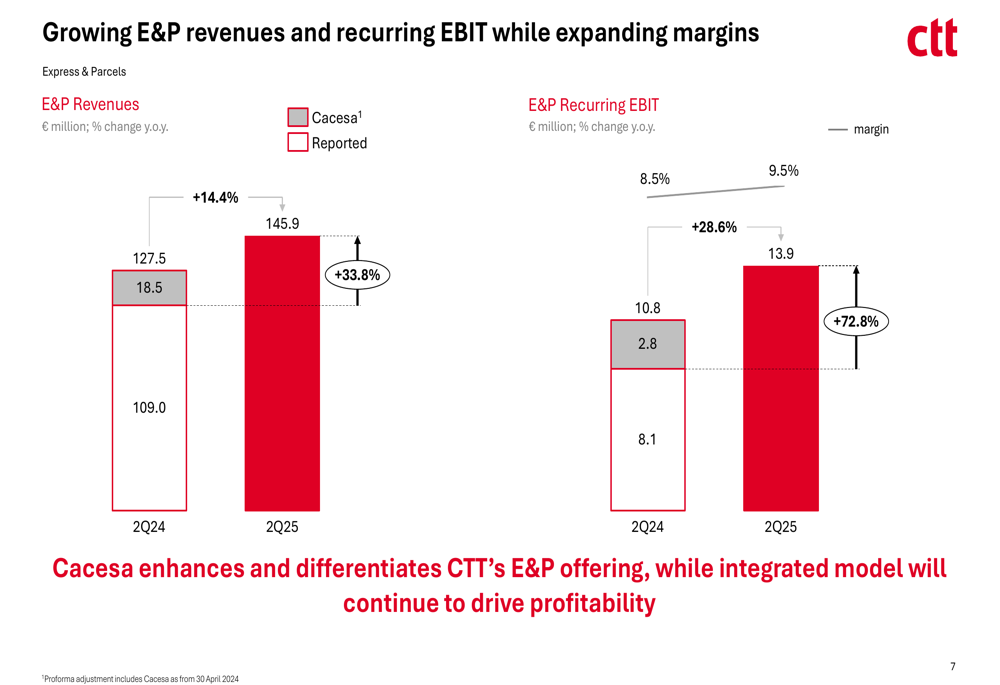

The Express & Parcels segment emerged as CTT’s growth engine, with revenues increasing by 14.4% to €145.9 million in Q2 2025. More importantly, recurring EBIT in this segment grew by 28.6% to €13.9 million, with margins improving from 8.5% to 9.5%.

The following chart details the E&P segment’s performance:

The Mail segment continues to face structural challenges with addressed mail volumes declining by 10.5%. However, overall Mail & Other revenues increased by 2.9% to €118.7 million, bolstered by €8.6 million from election-related services in May 2025. The segment’s recurring EBIT improved by 1.6 percentage points despite the volume challenges.

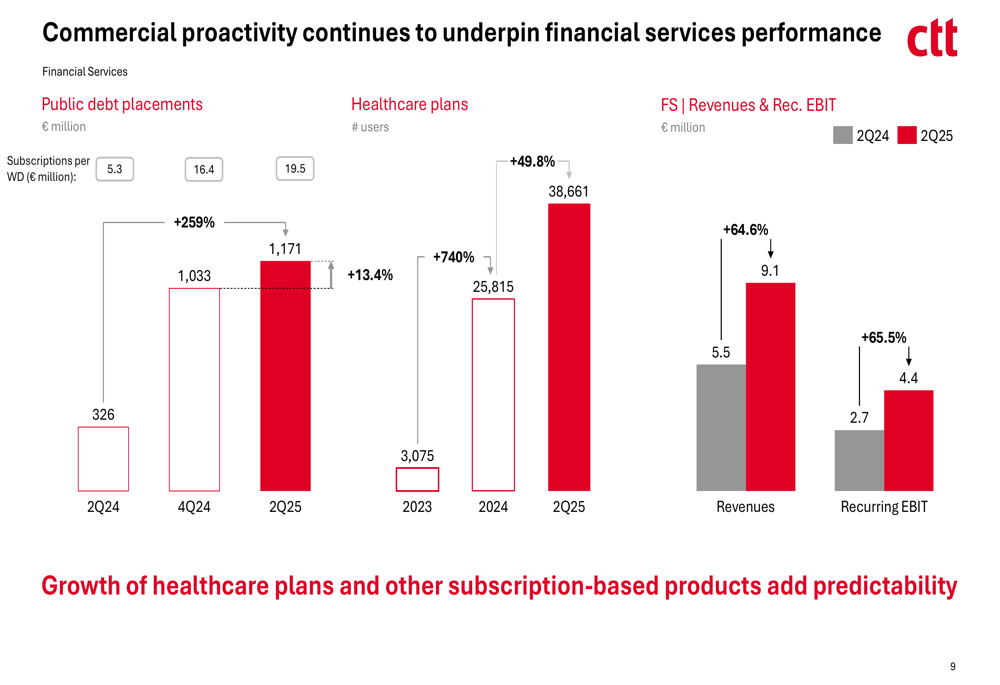

Financial Services showed remarkable growth with revenues increasing by 64.6% to €9.1 million and recurring EBIT growing by 65.5% to €4.4 million. Public debt placements surged 259% compared to Q2 2024, while healthcare plans grew by 740% to 38,661 users.

The following chart illustrates the strong performance in Financial Services:

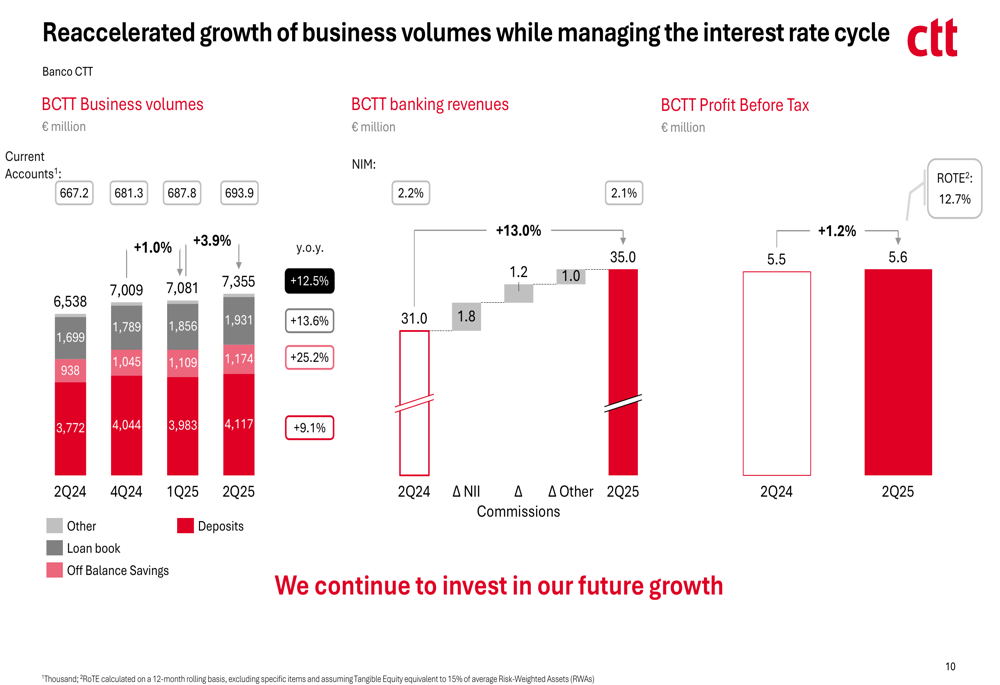

Banco CTT also demonstrated positive momentum with reaccelerating growth in business volumes, which increased by 3.9% to €7,355 million. The bank maintained a healthy net interest margin of 2.2% and achieved a return on equity of 12.7%.

The following chart shows the bank’s performance metrics:

Strategic Initiatives and Acquisitions

A key element of CTT’s growth strategy is the integration of Cacesa, which is enhancing the company’s Express & Parcels offering. Cacesa contributed €18.5 million to revenues and €2.8 million to recurring EBIT in Q2 2025. The integration is progressing well, with unified sales strategies and alignment of operational processes.

The following chart shows how Cacesa is contributing to CTT’s accelerating growth:

CTT completed the €25 million acquisition of SBB on April 17, 2025, and continues to work toward completing the DHL acquisition by year-end, pending antitrust review. These strategic moves are part of CTT’s transformation into a leading e-commerce logistics player in its markets.

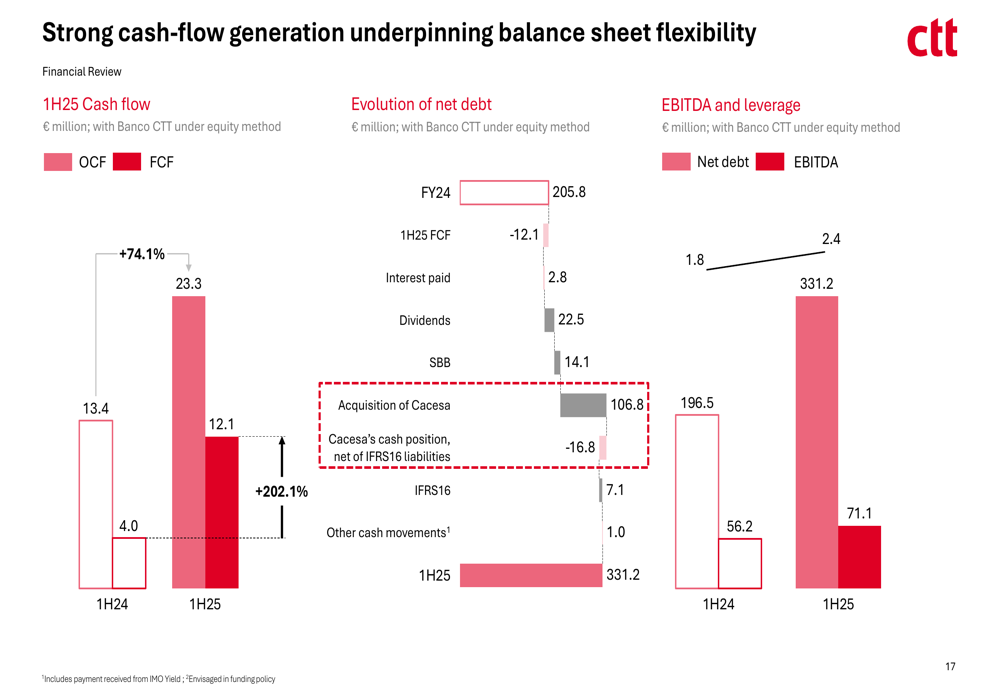

The company’s current leverage stands at 2.4x net debt to EBITDA following the Cacesa acquisition, slightly higher than the 2.1x projected in the Q1 2025 earnings call, but still within manageable levels given the strong cash flow generation.

Forward-Looking Statements

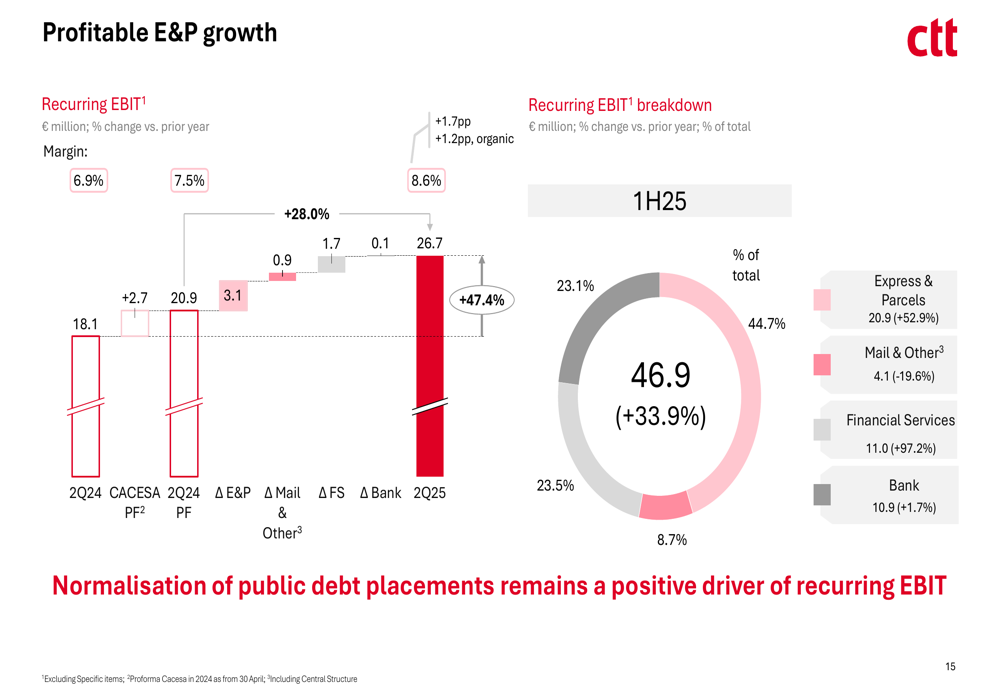

CTT reaffirmed its guidance for organic recurring EBIT to exceed €100 million in 2025, consistent with previous communications. The company expects to continue benefiting from its diversified business model, with E&P reaccelerating and improving profitability.

The following slide highlights CTT’s profitable E&P growth and recurring EBIT breakdown by segment:

Management emphasized that despite some volatility in Mail revenues and "lumpiness" in Mail EBIT, the company will continue to deploy cost-cutting initiatives in this segment while focusing on growth opportunities in e-commerce logistics, financial services, and banking.

CTT’s cash flow generation remains strong, providing flexibility for both strategic investments and potential shareholder returns. The following chart illustrates the company’s cash flow performance:

With its reinforced position as an e-commerce logistics player, differentiated service portfolio, and improving profitability, CTT appears well-positioned to continue its growth trajectory through the remainder of 2025 and beyond, despite ongoing challenges in its traditional mail business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.