Interactive Brokers shares jump as it secures spot in S&P 500

Introduction & Market Context

Curbline Properties Corp (CURB) presented its second quarter 2025 earnings results on July 28, 2025, highlighting continued expansion through strategic acquisitions and solid operational performance. The company’s stock closed at $22.86 prior to the earnings release, up 2.23% on the day, reflecting positive investor sentiment as the company continues its growth trajectory in the convenience retail property sector.

The Q2 results demonstrate Curbline’s commitment to its strategy of acquiring convenience properties in wealthy U.S. submarkets, with significant investment activity both during and after the quarter. The company’s focus on high-traffic locations in affluent areas appears to be yielding strong operational results, as evidenced by robust same-property NOI growth and impressive leasing spreads.

Quarterly Performance Highlights

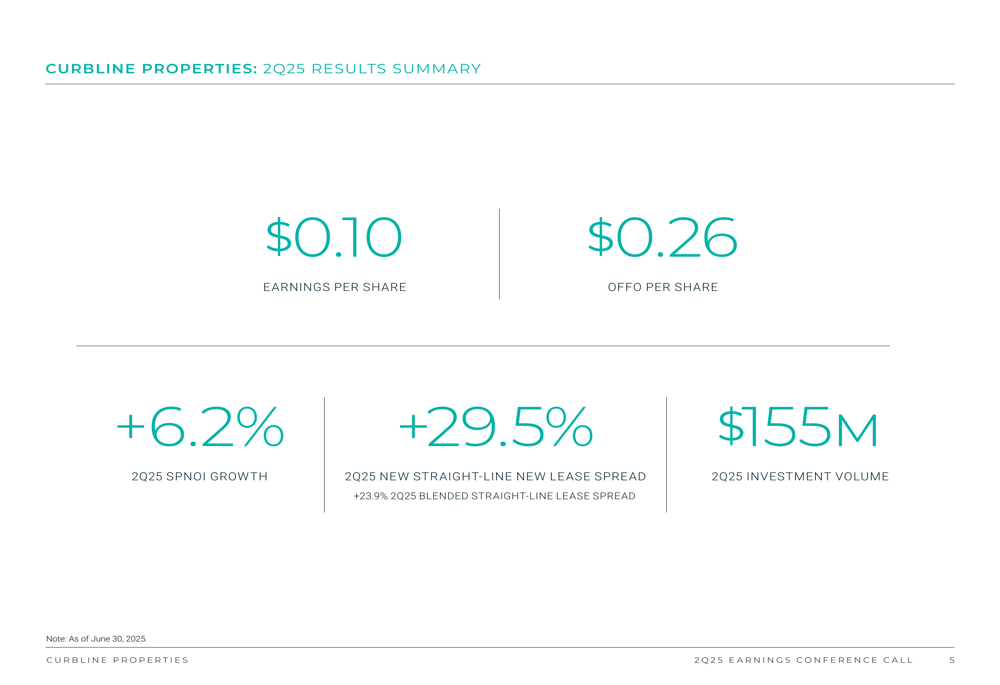

Curbline reported earnings per share of $0.10 for Q2 2025, consistent with the previous quarter’s performance. Operating funds from operations (OFFO) per share came in at $0.26, while same-property net operating income (SPNOI) grew by 6.2% year-over-year, demonstrating the strength of the company’s existing portfolio.

The company’s leasing activity showed particularly strong results, with straight-line new lease spreads of 29.5% and blended straight-line lease spreads of 23.9% during the quarter. The overall leased rate stood at 96.1%, up 10 basis points sequentially, highlighting the demand for Curbline’s retail spaces.

Operational efficiency remained strong, with tenant improvements and capital expenditures representing just 7% of NOI in Q2 2025 and 6% year-to-date. The company also reported that trailing twelve months net effective rents equaled 92% of base rent, indicating minimal leakage between gross and net rents.

Acquisition Strategy

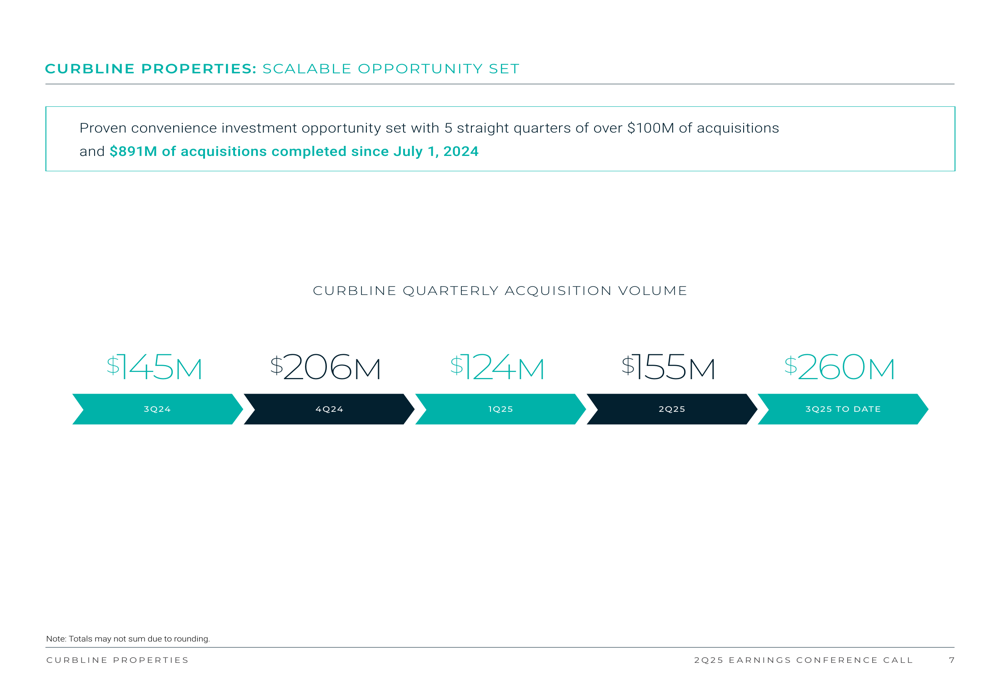

Curbline’s growth strategy continues to be driven by acquisitions, with the company reporting $155 million in property investments during Q2 2025, representing 19 properties. More impressively, the company has already acquired an additional 29 properties for $260 million in Q3 to date, including a significant 23-property portfolio for $159 million.

This acquisition momentum marks the fifth consecutive quarter with over $100 million in acquisitions, bringing the total acquisition volume to $891 million since July 1, 2024. The consistency of this investment activity demonstrates Curbline’s ability to source and close deals in its target market.

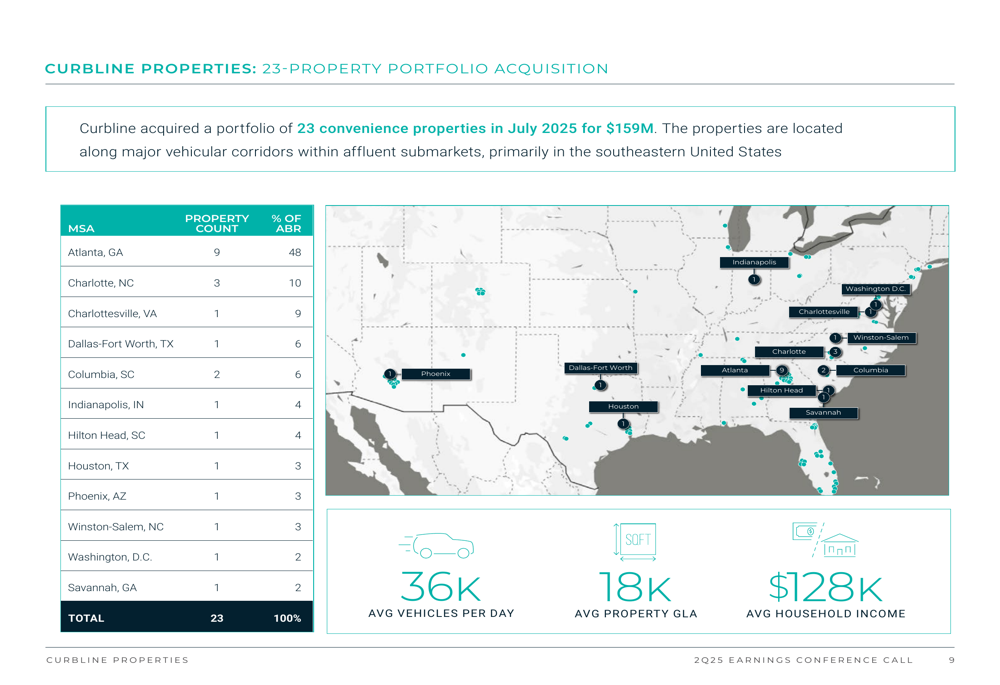

The recently acquired 23-property portfolio is primarily located in the southeastern United States, with 48% of annualized base rent (ABR) coming from properties in Atlanta, Georgia. The portfolio features properties situated along major vehicular corridors in affluent submarkets, with average household incomes of $128,000 and average daily traffic of 36,000 vehicles.

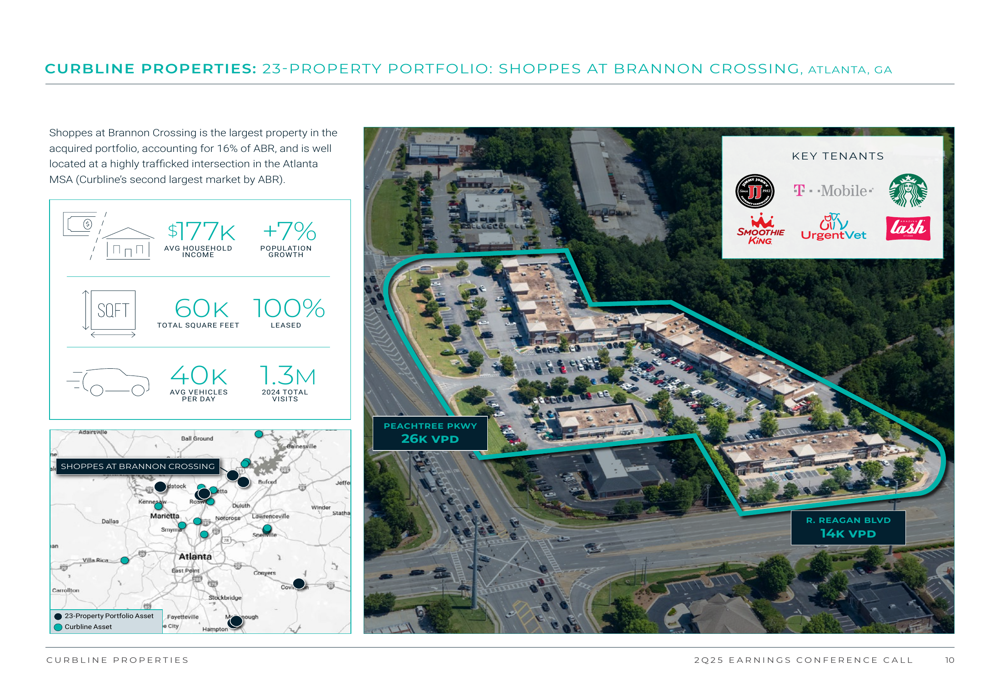

Among the notable properties in this portfolio is Shoppes at Brannon Crossing, the largest property in the acquired portfolio, accounting for 16% of ABR. Located at a high-traffic intersection in the Atlanta MSA, this fully leased 60,000 square foot property serves an area with an average household income of $177,000 and experiences approximately 1.3 million visits annually.

Balance Sheet & Liquidity

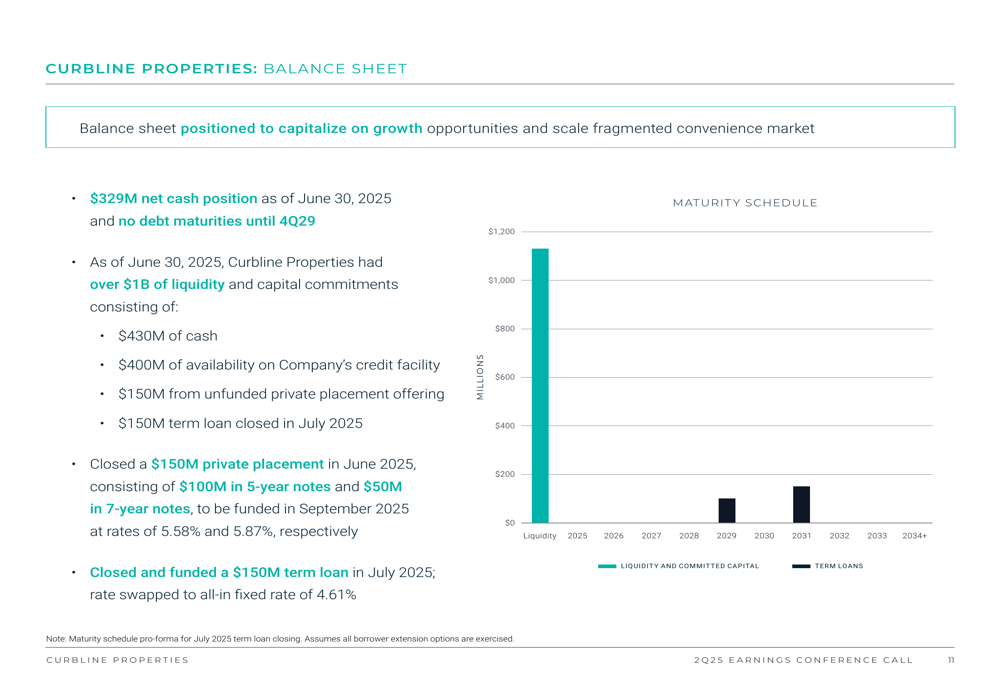

Curbline maintains a strong financial position with over $1 billion in liquidity and capital commitments. As of June 30, 2025, the company reported a net cash position of $329 million and no debt maturities until the fourth quarter of 2029, providing significant flexibility for continued acquisitions and operations.

The company’s liquidity consists of $430 million in cash, $400 million available on its credit facility, and $300 million from debt proceeds. In June 2025, Curbline secured a $150 million private placement, comprising $100 million in 5-year notes and $50 million in 7-year notes, to be funded in September 2025 at rates of 5.58% and 5.87%, respectively. Additionally, a $150 million term loan was closed and funded in July 2025, with the rate swapped to an all-in fixed rate of 4.61%.

Further strengthening its financial credibility, Curbline received a BBB credit rating from Fitch during the quarter, validating the company’s financial management and growth strategy.

Forward Guidance

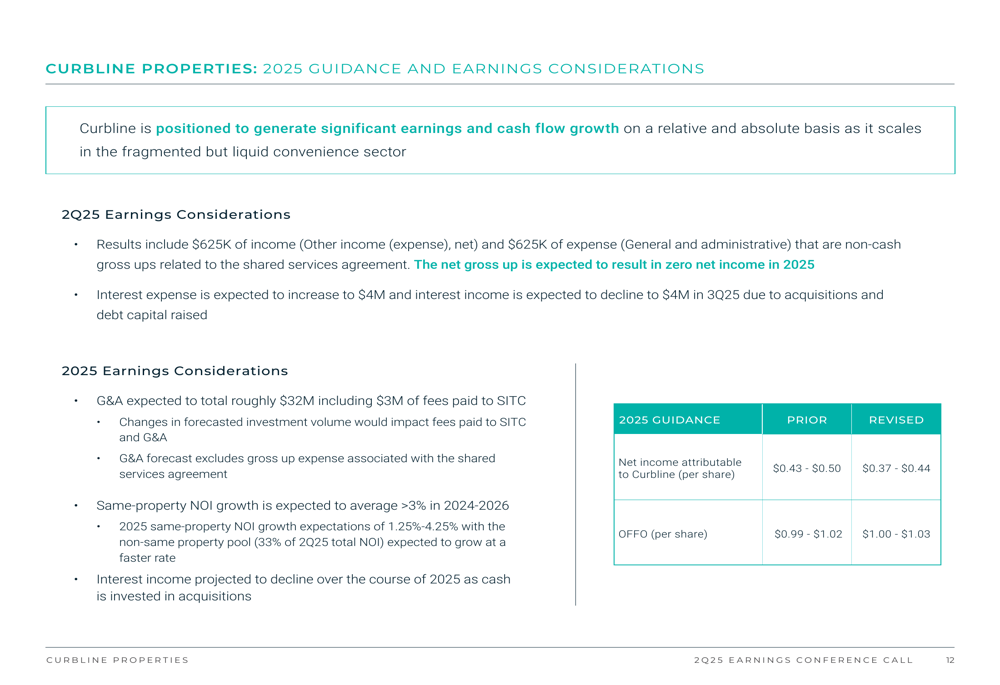

Curbline has revised its 2025 guidance, adjusting net income attributable to Curbline per share from $0.43-0.50 to $0.37-0.44, while slightly increasing OFFO per share guidance from $0.99-1.02 to $1.00-1.03. The company noted that the net gross up related to the shared services agreement is expected to result in zero net income impact in 2025.

Looking ahead, Curbline expects interest expense to increase to $4 million and interest income to decline to $4 million in Q3 2025 due to recent acquisitions and debt capital raised. Despite these changes, the company remains positioned to generate significant earnings and cash flow growth.

Conclusion

Curbline Properties’ Q2 2025 results demonstrate the company’s continued execution of its growth strategy through strategic acquisitions while maintaining strong operational performance. With a robust pipeline of acquisition opportunities, significant liquidity, and solid same-property NOI growth, Curbline appears well-positioned to continue its expansion in the convenience retail property sector.

The company’s focus on properties in affluent submarkets with strong demographics and high traffic counts provides a solid foundation for sustained growth, while its strong balance sheet offers flexibility to capitalize on future opportunities. As Curbline continues to scale its portfolio, investors will be watching closely to see if the company can maintain its impressive leasing spreads and NOI growth while successfully integrating its recent acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.