Oil prices rise on US-China trade progress, supply jitters persist

Curtiss-Wright Corporation (NYSE:CW) reported robust first-quarter 2025 results on May 8, showcasing double-digit growth across key financial metrics and prompting management to raise its full-year outlook. The aerospace and defense technology provider demonstrated strength across all business segments, with particularly impressive performance in its defense electronics and naval divisions.

Quarterly Performance Highlights

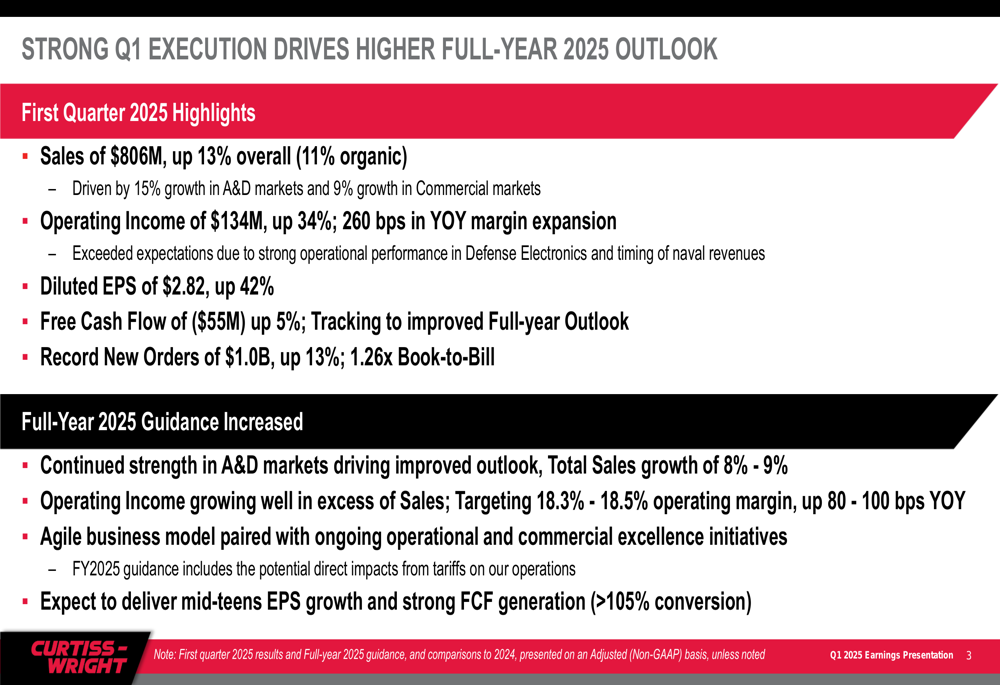

Curtiss-Wright delivered exceptional first-quarter results, with sales reaching $806 million, representing a 13% increase (11% organic) compared to the same period last year. The company’s aerospace and defense markets grew by 15%, while commercial markets expanded by 9%.

Operating income surged by 34% to $134 million, with operating margins expanding by 260 basis points year-over-year to 16.6%. Diluted earnings per share reached $2.82, marking a substantial 42% increase from Q1 2024.

As shown in the following summary of Q1 2025 performance:

The company also reported new orders of $1.0 billion, up 13% from the prior year, resulting in a book-to-bill ratio of 1.26x. Free cash flow was negative $55 million, which represents a 5% improvement compared to Q1 2024 and aligns with the company’s typical seasonal pattern.

Segment Analysis

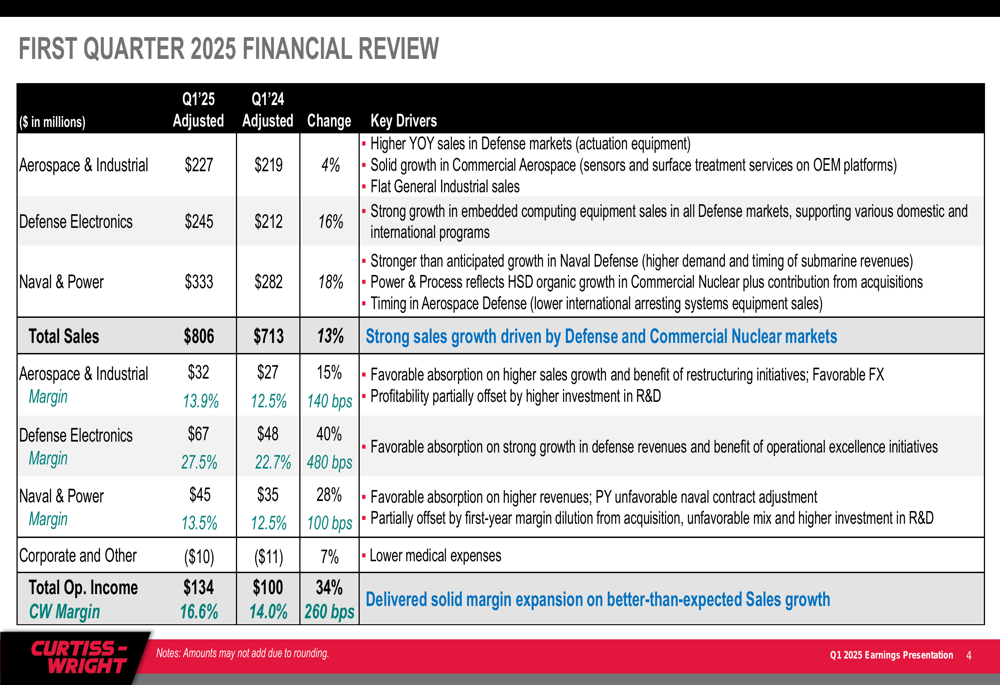

Curtiss-Wright’s performance was strong across all three business segments, with Defense Electronics leading the way in margin expansion. The segment breakdown reveals the drivers behind the company’s impressive quarterly results:

The Aerospace & Industrial segment posted sales of $227 million, up 4% year-over-year, with operating margin improving by 140 basis points to 13.9%. This growth was primarily driven by higher commercial aerospace OEM sales and improved operational performance.

Defense Electronics delivered the most significant margin improvement, with sales increasing 16% to $245 million and operating margin expanding by 480 basis points to 27.5%. Management attributed this exceptional performance to higher defense electronics and embedded computing sales, along with favorable absorption and operational excellence initiatives.

The Naval & Power segment saw the largest sales growth at 18%, reaching $333 million, with operating margin improving by 100 basis points to 13.5%. This growth was driven by higher naval defense revenues, particularly in submarine and aircraft carrier programs, as well as increased commercial nuclear power generation sales.

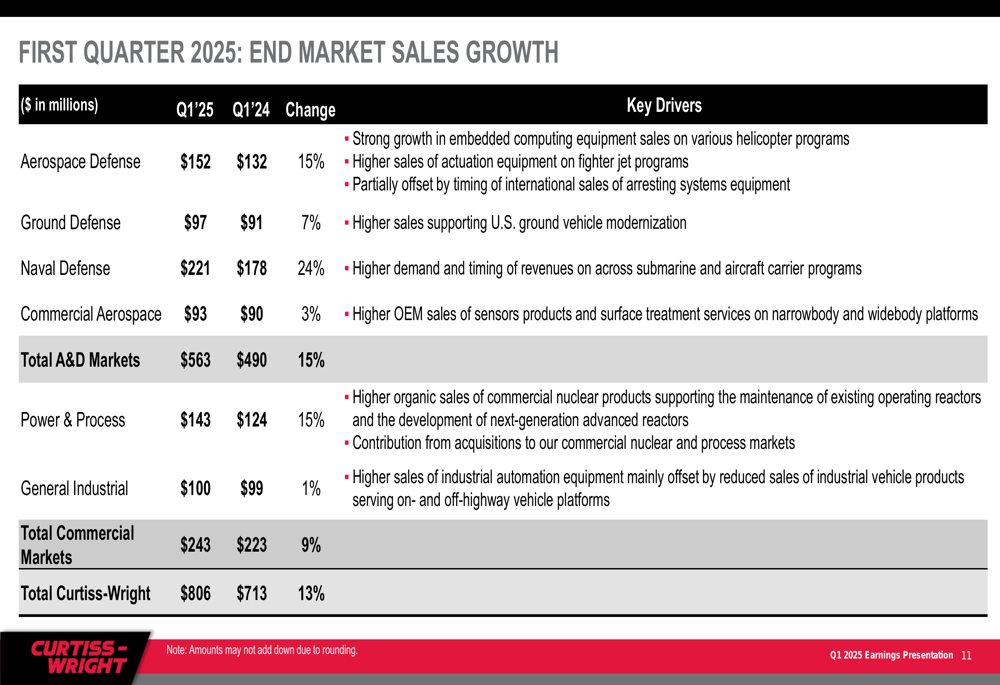

A detailed breakdown of end market performance shows particularly strong growth in naval defense and power & process markets:

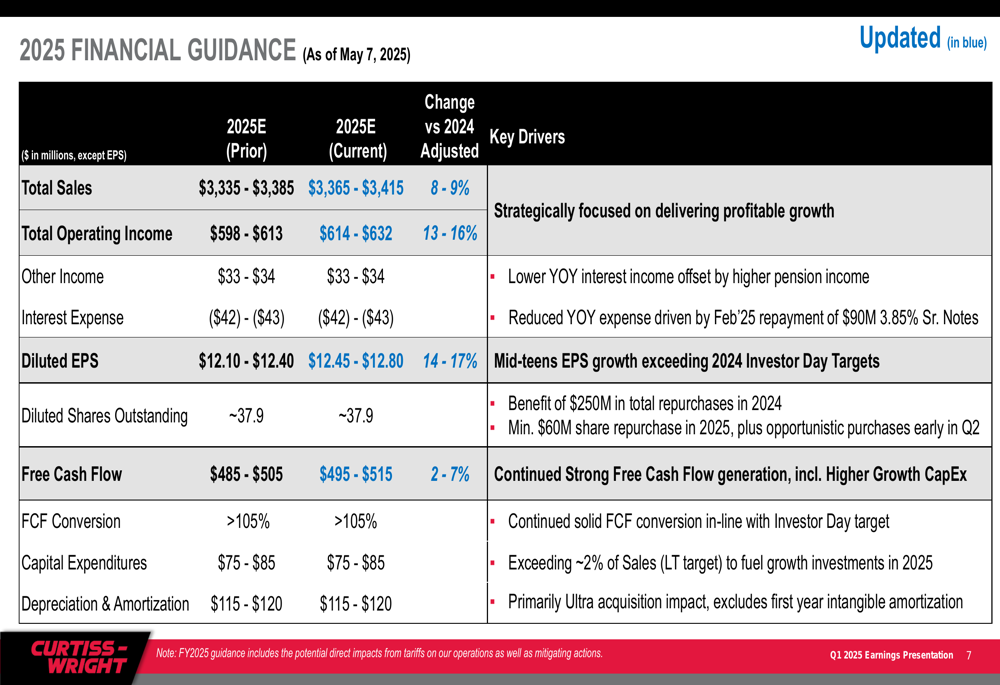

Updated 2025 Guidance

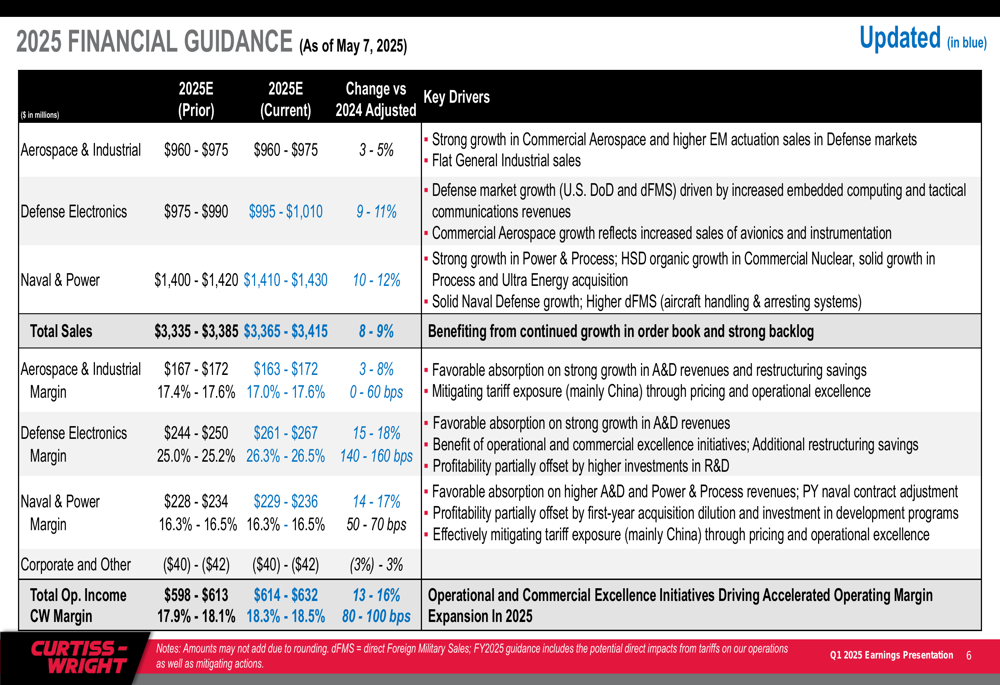

Following the strong first-quarter performance, Curtiss-Wright raised its full-year 2025 guidance. The company now expects total sales to reach $3.365-$3.415 billion, representing growth of 8-9% compared to 2024.

Operating income is projected to grow well in excess of sales, with the company targeting an operating margin of 18.3-18.5%, representing an 80-100 basis point improvement year-over-year. Diluted EPS is expected to reach $12.45-$12.80, reflecting growth of 14-17%.

The company also provided additional financial guidance details:

Free cash flow is projected to be $495-$515 million, up 2-7% from 2024, with free cash flow conversion exceeding 105%. Capital expenditures are expected to be $75-$85 million, with depreciation and amortization of $115-$120 million.

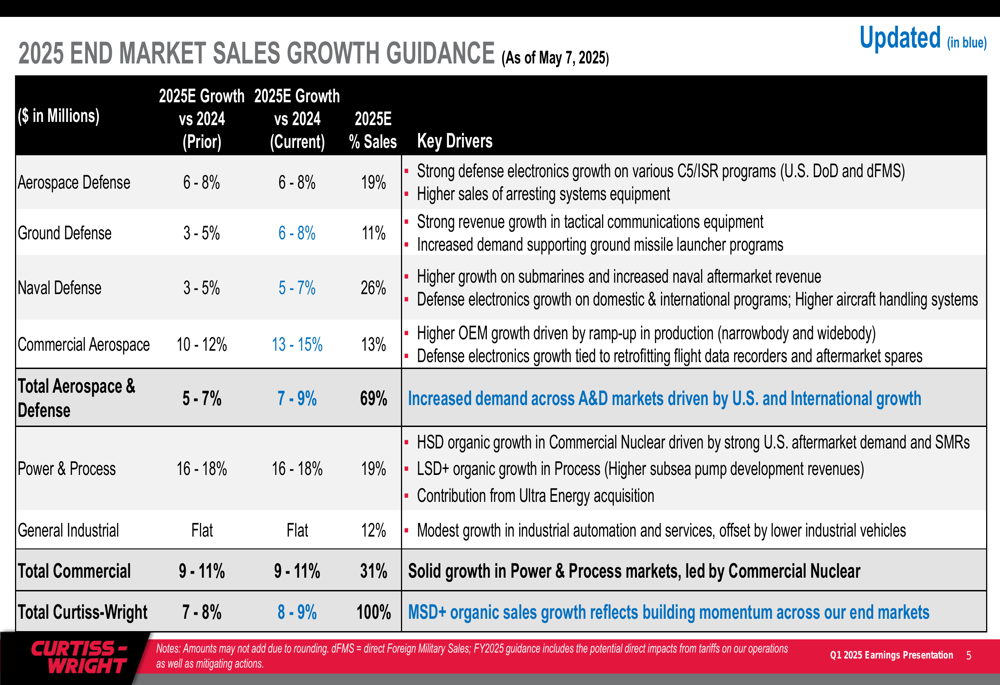

End Market Outlook

Curtiss-Wright’s updated end market sales growth guidance for 2025 reflects continued strength in aerospace and defense markets, which represent 69% of the company’s total sales:

The company expects aerospace defense and ground defense markets to grow 6-8%, while naval defense is projected to increase 5-7%. Commercial aerospace is forecast to see the strongest growth at 13-15%. In the commercial markets, power and process is expected to grow 16-18%, while general industrial is projected to remain flat.

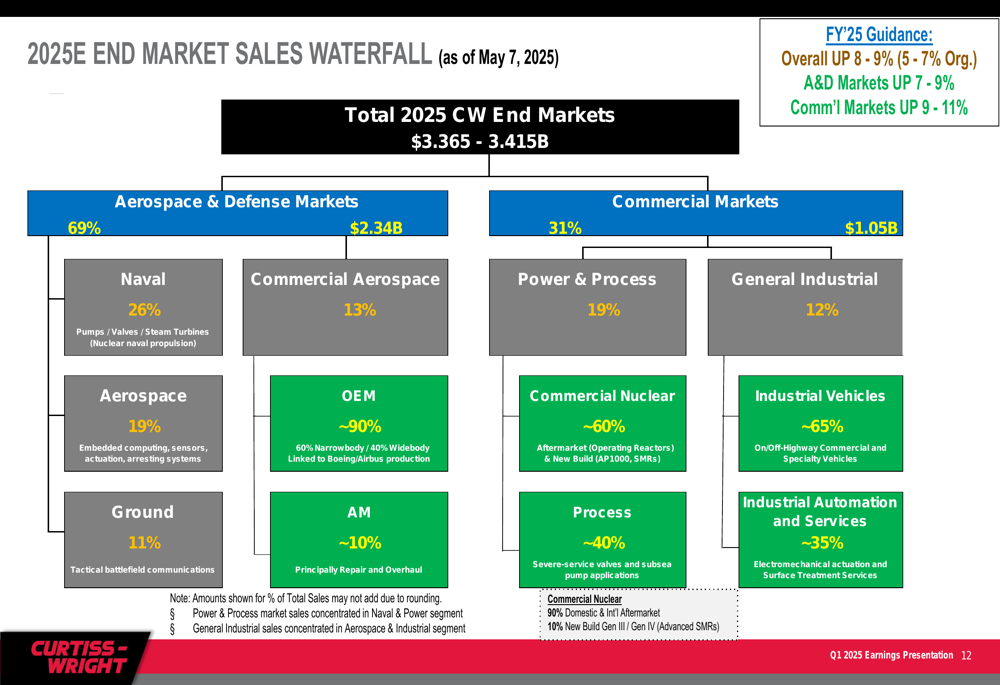

The waterfall chart below illustrates the company’s 2025 estimated end market sales distribution:

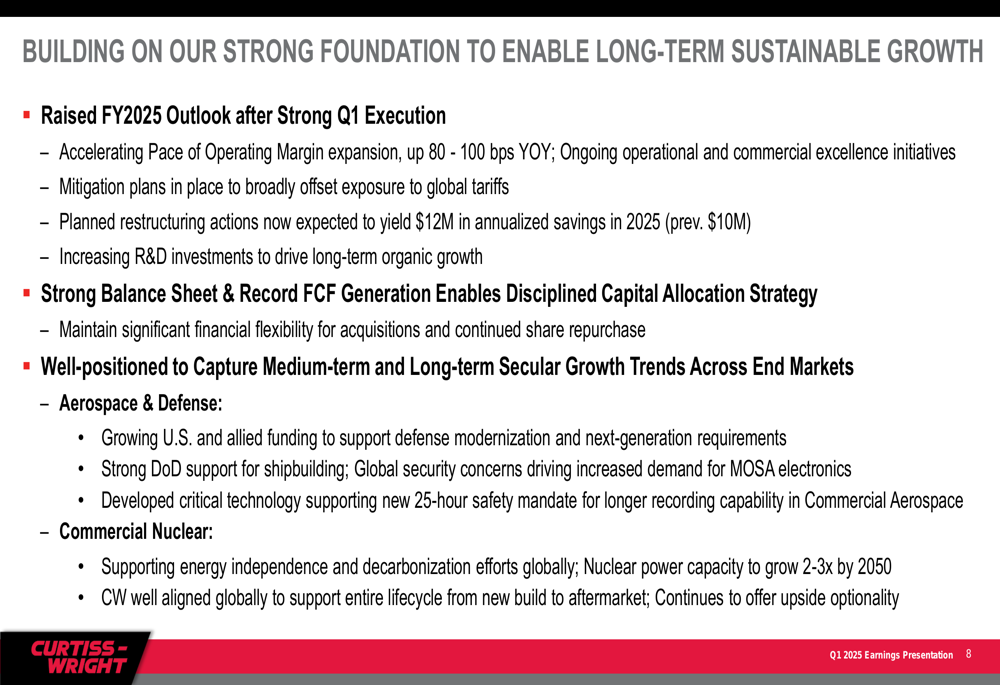

Strategic Positioning and Outlook

Curtiss-Wright’s management emphasized that the company is well-positioned to capture medium and long-term secular growth trends across its end markets, particularly in aerospace and defense. The company highlighted growing U.S. and allied defense funding, strong Department of Defense support for shipbuilding programs, and commercial nuclear projects supporting energy independence as key drivers for future growth.

The company’s strong balance sheet and record free cash flow generation enable a disciplined capital allocation strategy, which management believes will support long-term sustainable growth.

In premarket trading following the earnings release, Curtiss-Wright shares were up 1.8% to $368.55, reflecting positive investor reaction to the strong quarterly results and raised guidance. The stock has traded between $258.85 and $393.40 over the past 52 weeks.

Curtiss-Wright’s Q1 2025 performance demonstrates the company’s ability to execute effectively across its diverse portfolio of businesses, with particular strength in its defense-related segments. The raised full-year guidance suggests management’s confidence in maintaining this momentum throughout 2025, positioning the company for continued growth and shareholder value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.