Street Calls of the Week

Introduction & Market Context

Cushman & Wakefield (NYSE:CWK) released its first quarter 2025 earnings presentation on April 29, revealing significant improvement in its transaction business and overall profitability. The global real estate services firm reported fee revenue growth of 4% year-over-year, driven by strong performance in Leasing and Capital Markets, while maintaining steady performance in its Services segment.

The company’s stock, which closed at $9.01 on April 28, showed a positive premarket reaction, rising 4.88% to $9.45, as investors responded favorably to the improved performance metrics and positive outlook for the remainder of 2025.

Quarterly Performance Highlights

Cushman & Wakefield reported fee revenue of $1.54 billion for Q1 2025, representing a 4% increase in local currency compared to Q1 2024. The company’s Adjusted EBITDA reached $96 million, a substantial 24% increase from the prior year, while Adjusted EBITDA margin expanded by 103 basis points to 6.2%.

As shown in the following summary of first quarter highlights:

The improvement in profitability translated to adjusted earnings per share of $0.09 for Q1 2025, compared to $0.00 in the same period last year. This significant improvement reflects the company’s success in growing revenue while maintaining cost discipline.

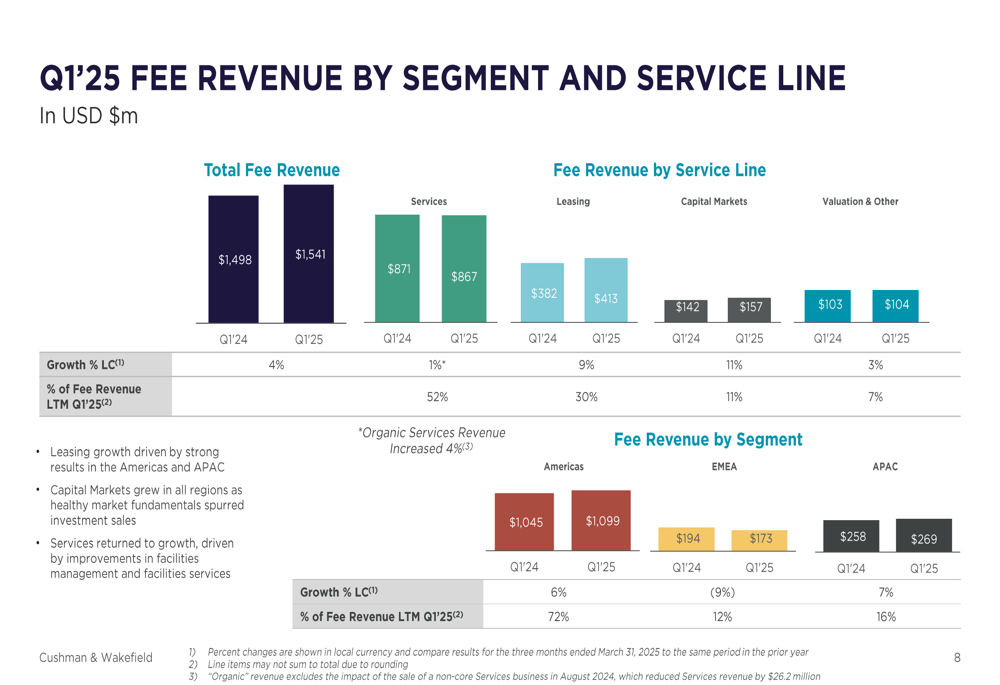

The company’s transaction business showed particularly strong results, with Leasing revenue increasing 9% and Capital Markets revenue growing 11% compared to Q1 2024. The Services segment, which represents over half of the company’s revenue, grew 1% overall, with organic Services revenue increasing 4% when excluding the impact of a divested non-core business.

The breakdown of fee revenue by segment and service line illustrates the company’s diversified revenue streams:

Segment Analysis

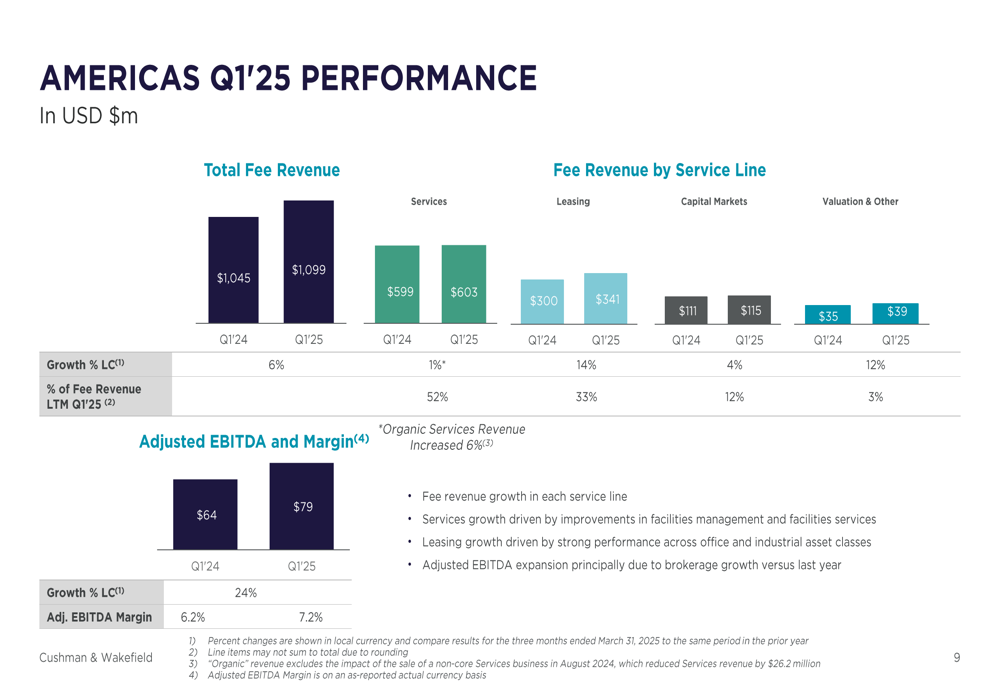

Americas Performance

The Americas segment, which accounts for approximately 72% of Cushman & Wakefield’s total fee revenue, delivered strong performance with 6% growth in local currency. This growth was broad-based across all service lines, with particularly robust results in Leasing (14% growth) and Valuation & Other (12% growth).

The segment’s Adjusted EBITDA increased by 24% to $79 million, with margin expansion of 100 basis points to 7.2%. This improvement was primarily driven by higher brokerage revenue compared to the previous year.

The following chart details the Americas segment’s performance:

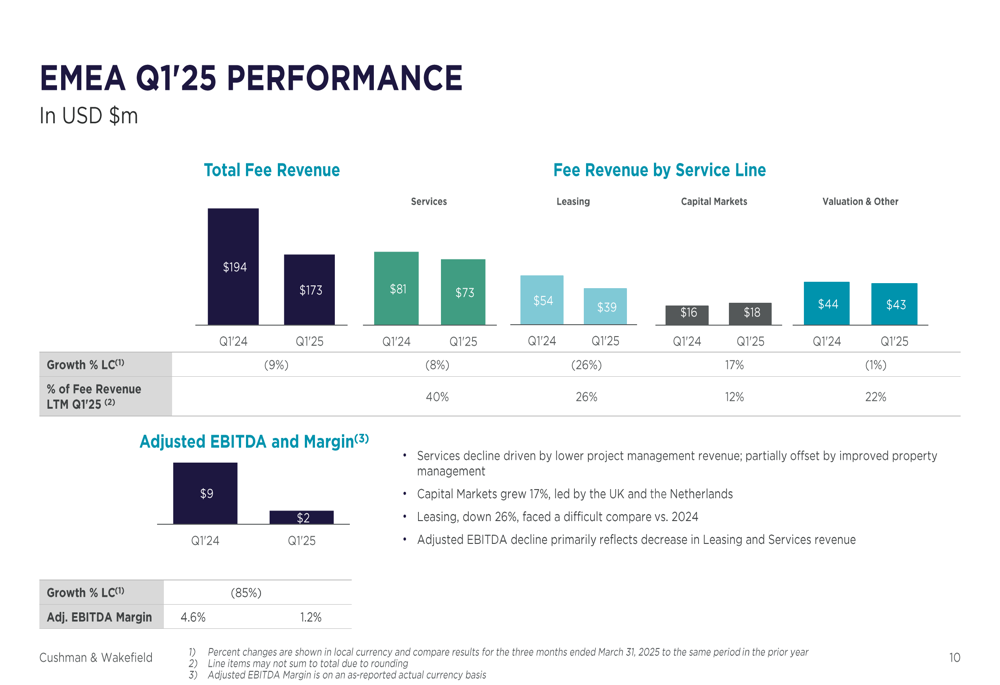

EMEA Performance

In contrast to the strong performance in the Americas, the Europe, Middle East, and Africa (EMEA) segment faced challenges in Q1 2025. Fee revenue declined by 9% in local currency, with significant weakness in Leasing (-26%) and Services (-8%). The only bright spot was Capital Markets, which grew 17% led by strength in the UK and Netherlands.

The segment’s Adjusted EBITDA fell sharply to $2 million from $9 million in the prior year, with margin contraction to 1.2% from 4.6%. This decline primarily reflects the decrease in Leasing and Services revenue.

The EMEA segment’s performance is illustrated in the following breakdown:

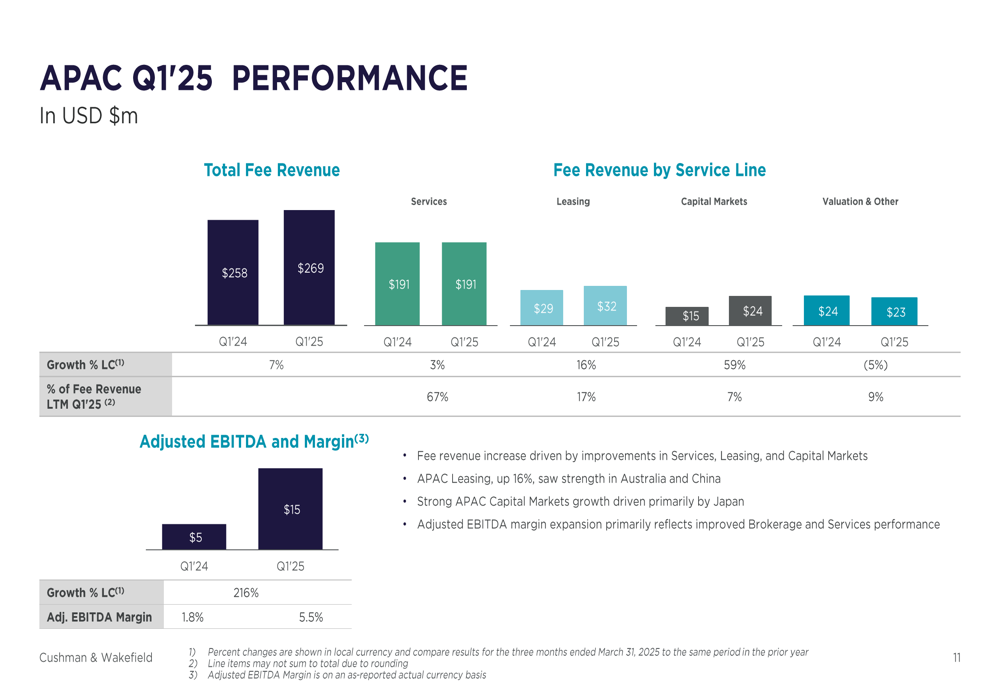

APAC Performance

The Asia-Pacific (APAC) segment showed strong recovery, with fee revenue increasing 7% in local currency. The growth was driven by improvements across multiple service lines, with Capital Markets surging 59% and Leasing growing 16%. Services revenue increased by a more modest 3%.

Most impressive was the segment’s profitability improvement, with Adjusted EBITDA more than tripling to $15 million from $5 million in Q1 2024, representing a 216% increase in local currency. The Adjusted EBITDA margin expanded significantly to 5.5% from 1.8% in the prior year.

The following chart details the APAC segment’s performance:

Capital Structure and Debt Management

Cushman & Wakefield continued its focus on debt management during the quarter, repaying an additional $25 million of debt and repricing $1.0 billion of term loan debt maturing in 2030. The debt repricing reduced the applicable interest rate by 25 basis points, which should contribute to lower interest expenses going forward.

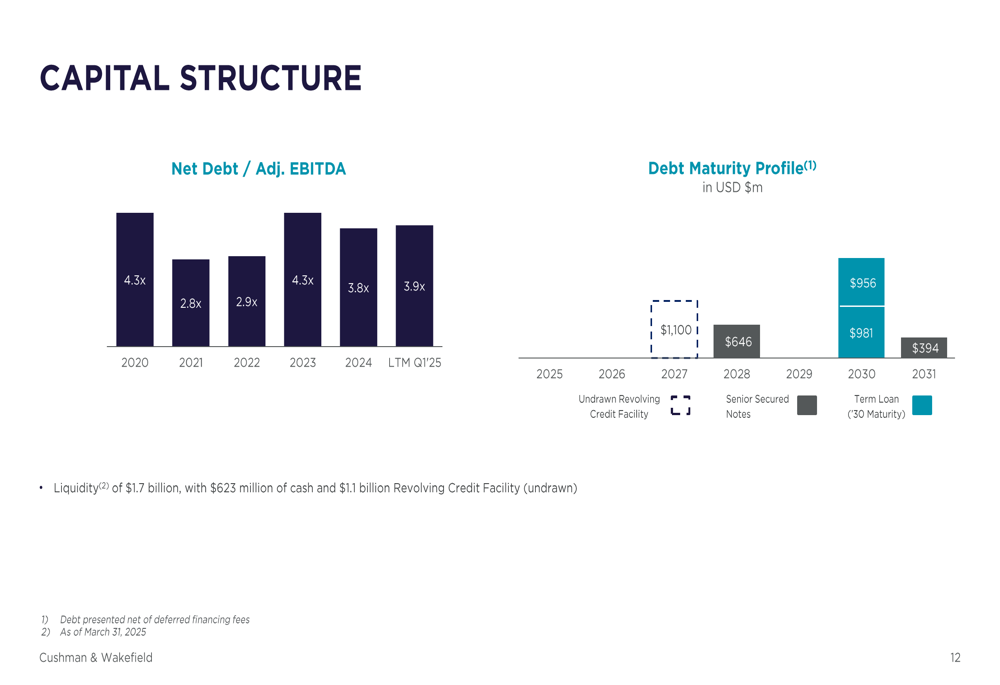

The company’s net debt to Adjusted EBITDA ratio stood at 3.9x as of March 31, 2025, slightly higher than the 3.8x reported at the end of 2024, but improved from 4.3x at the end of 2023. Liquidity remained strong at $1.7 billion, consisting of $623 million in cash and $1.1 billion in undrawn revolving credit facility availability.

The company’s debt maturity profile and leverage ratio are illustrated in the following chart:

The debt maturity profile shows limited near-term maturities, with the bulk of the company’s debt not maturing until 2030 and beyond, providing financial flexibility for the coming years.

Forward-Looking Statements

Looking ahead to the remainder of 2025, Cushman & Wakefield provided a positive outlook across its business segments. The company expects mid-single-digit growth in Leasing revenue for the full year, with Capital Markets revenue growth accelerating compared to 2024. Services revenue is also projected to achieve mid-single-digit growth for the year.

The company’s guidance for 2025 includes:

This outlook aligns with the company’s performance in recent quarters, including the Q3 2024 results where Cushman & Wakefield reported a fourth consecutive quarter of year-over-year leasing growth and the first increase in Capital Markets revenue in the Americas since Q2 2022.

The continued recovery in transaction markets, combined with the stability provided by the Services business, positions Cushman & Wakefield for improved financial performance throughout 2025, assuming market conditions remain favorable. The company’s focus on deleveraging and operational efficiency should further support profitability improvement and value creation for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.