Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Customers Bancorp, Inc. (NYSE:CUBI) released its Q2 2025 investor presentation on July 25, highlighting continued momentum across key performance metrics. The bank reported solid earnings growth driven by margin expansion, robust loan growth, and improved operational efficiency.

The presentation comes as CUBI shares have shown recent strength, with the stock trading at $62.55 as of July 24, 2025, within its 52-week range of $40.75 to $68.49. Following a Q1 earnings beat where EPS exceeded forecasts by $0.22, investors have been watching closely for signs of continued momentum.

Quarterly Performance Highlights

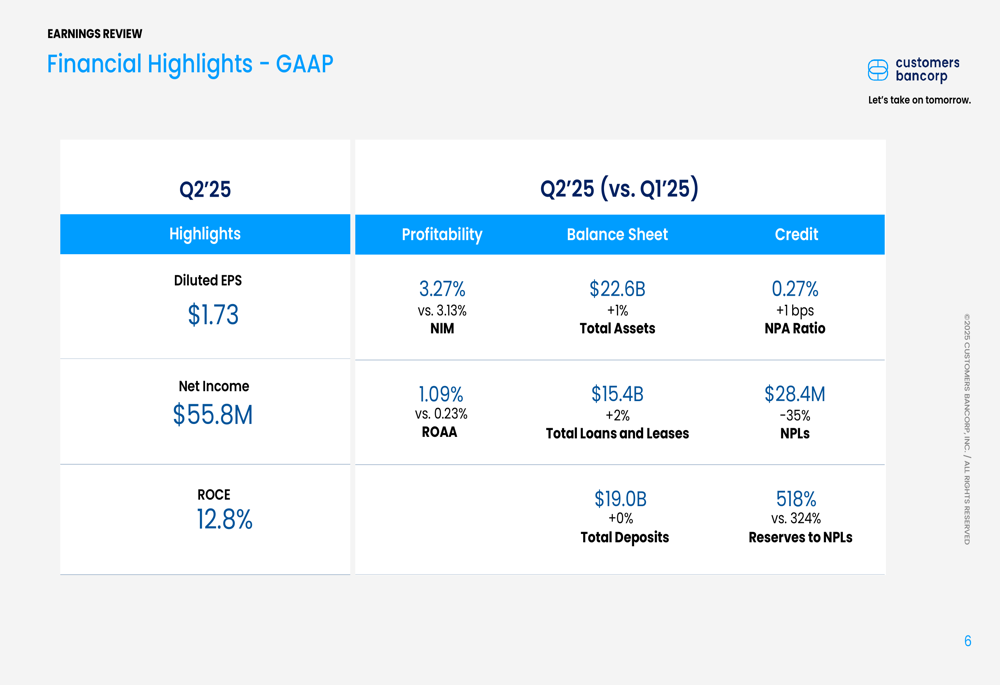

Customers Bancorp reported GAAP diluted EPS of $1.73 and core EPS of $1.80 for Q2 2025, continuing the positive trend from Q1’s $1.54 EPS. Net income reached $55.8 million with a return on common equity of 12.8%, while core earnings totaled $58.1 million with a core ROCE of 13.3%.

As shown in the following financial highlights, the bank’s performance metrics demonstrate solid improvement across multiple areas:

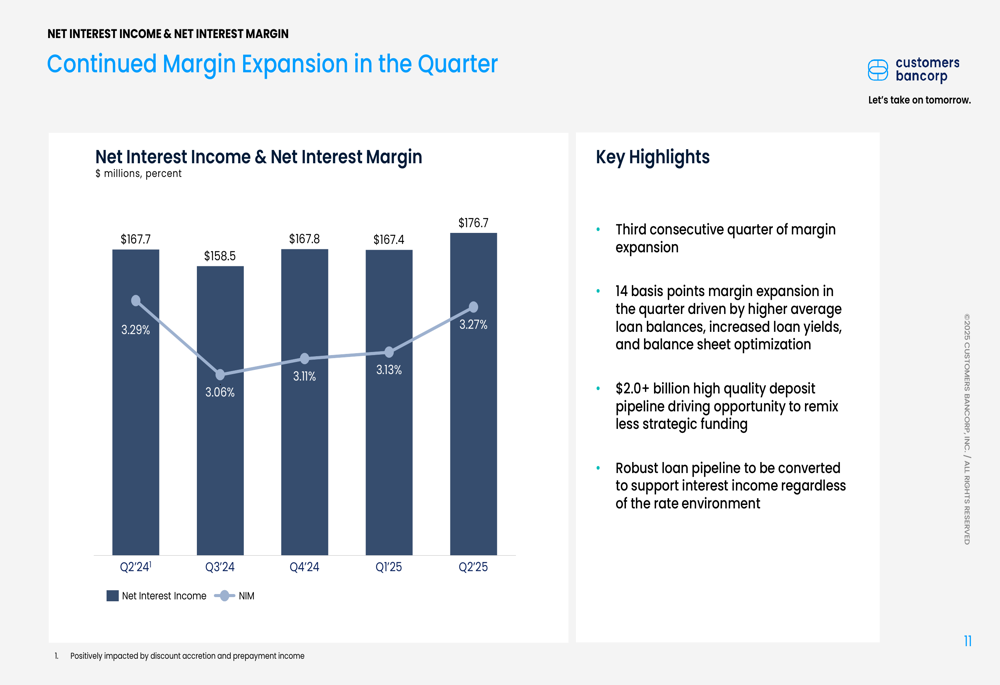

A key driver of the strong quarterly performance was the continued expansion of net interest margin (NIM), which increased to 3.27% from 3.13% in the previous quarter. This represents the third consecutive quarter of margin expansion, contributing to net interest income growth.

The following chart illustrates the bank’s margin expansion trajectory:

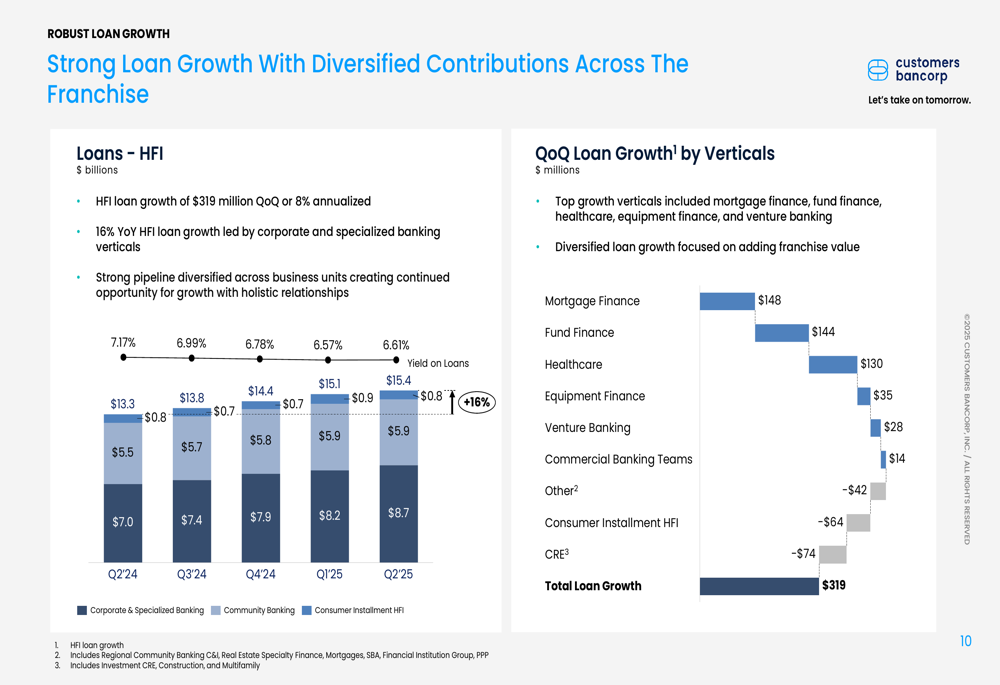

Loan growth remained robust at 8% annualized for the quarter, with year-over-year growth of 16%. The expansion was well-diversified across multiple verticals, with mortgage finance, fund finance, healthcare, equipment finance, and venture banking leading the growth.

As demonstrated in this breakdown of loan growth by vertical:

Strategic Initiatives and Growth Drivers

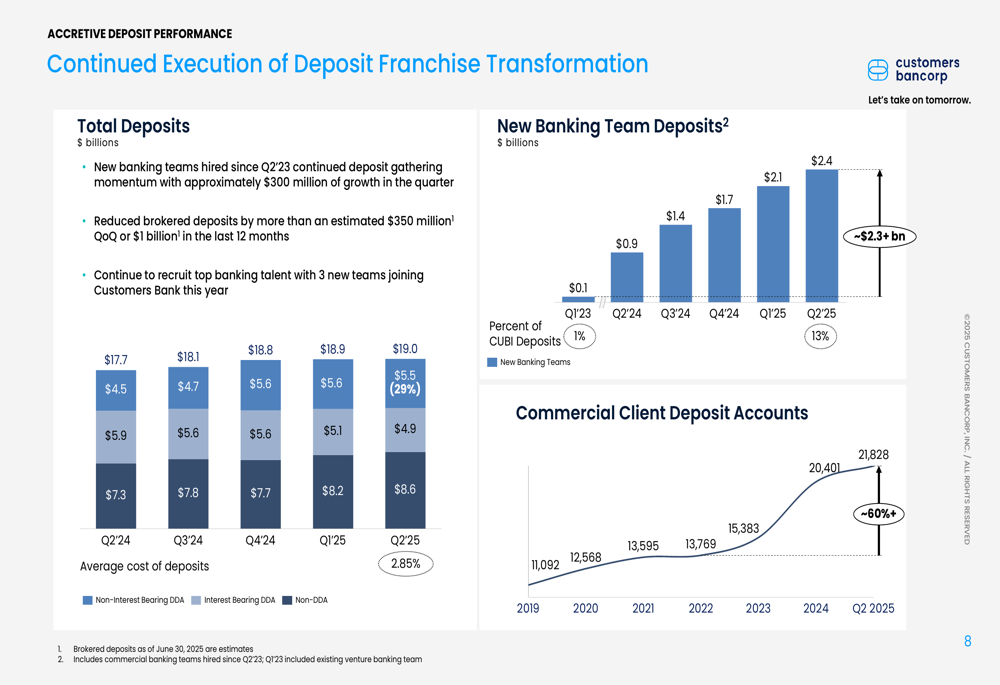

Customers Bancorp continues to execute on its deposit transformation strategy, with approximately $300 million of deposit growth from new banking teams and an estimated reduction of over $350 million in brokered deposits quarter-over-quarter. This shift toward relationship-based deposits supports the bank’s long-term funding stability.

The following visualization shows the progress in deposit transformation:

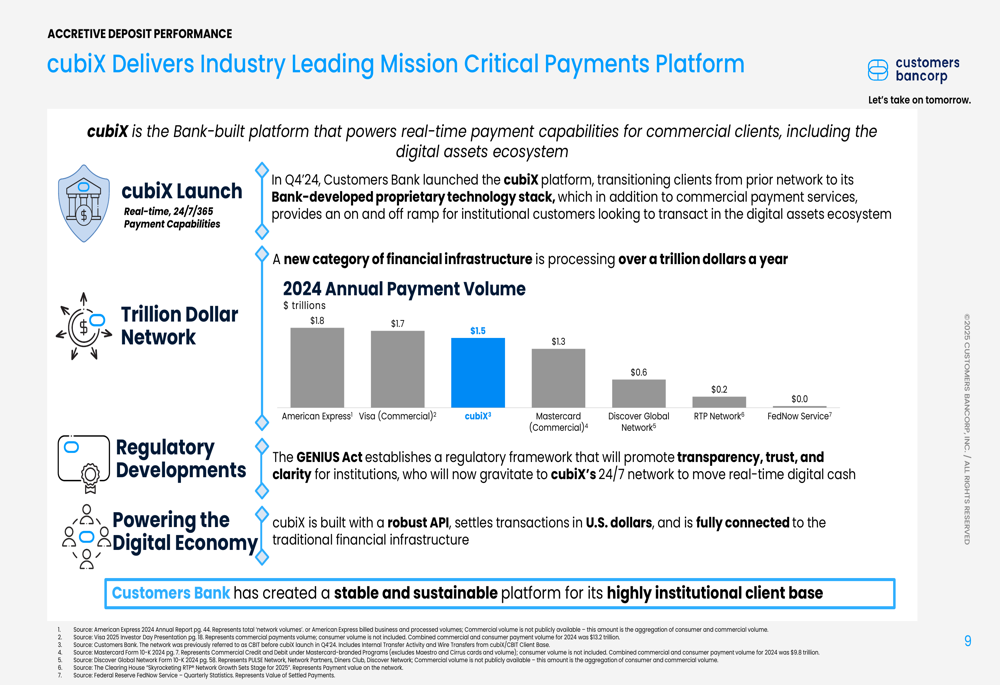

Perhaps the most notable strategic asset highlighted in the presentation is the bank’s cubix payments platform. Launched in Q4 2024, cubix has achieved remarkable scale, processing $1.7 trillion in annual payment volume. This places it in the same league as major payment networks like American Express (NYSE:AXP) ($1.8T), Visa (NYSE:V) ($1.5T), and Mastercard (NYSE:MA) ($1.3T).

As illustrated in this comparison of payment volumes:

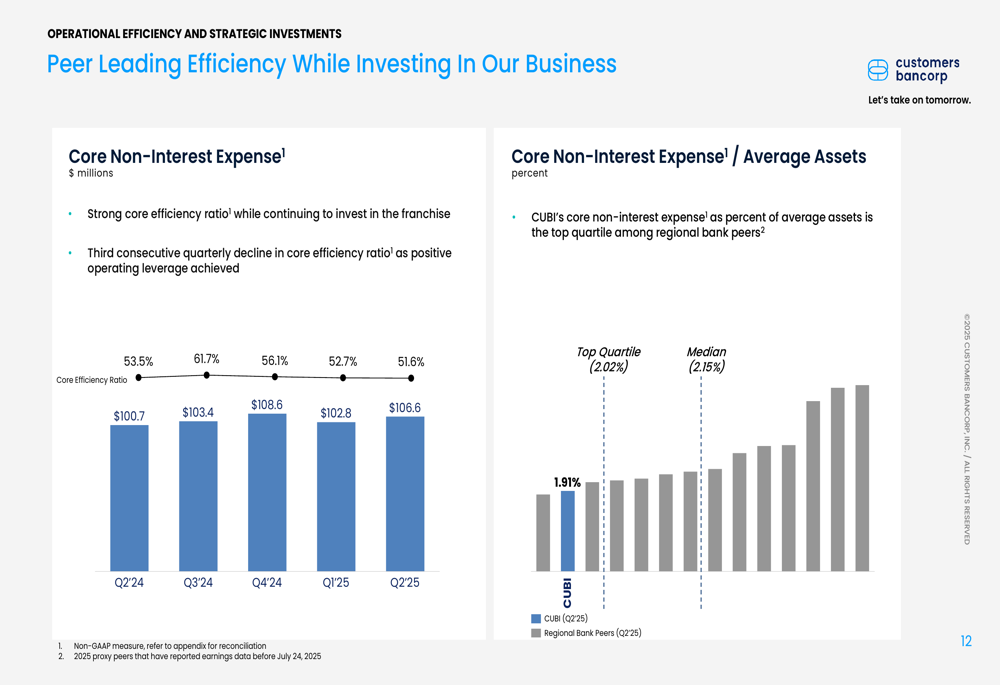

The bank’s efficiency initiatives are also yielding results, with the core efficiency ratio improving quarter-over-quarter as revenue growth outpaced non-interest expense growth. Customers Bancorp maintains one of the lowest core non-interest expense ratios among regional bank peers at 2.02% of average assets, compared to the peer median of 2.15%.

Competitive Positioning

Customers Bancorp has positioned itself as a tech-forward, diversified bank with strong growth metrics relative to peers. The presentation highlights that the bank ranks in the top 5 for five-year revenue CAGR and #15 for both five-year core EPS CAGR and tangible book value per share CAGR among peers.

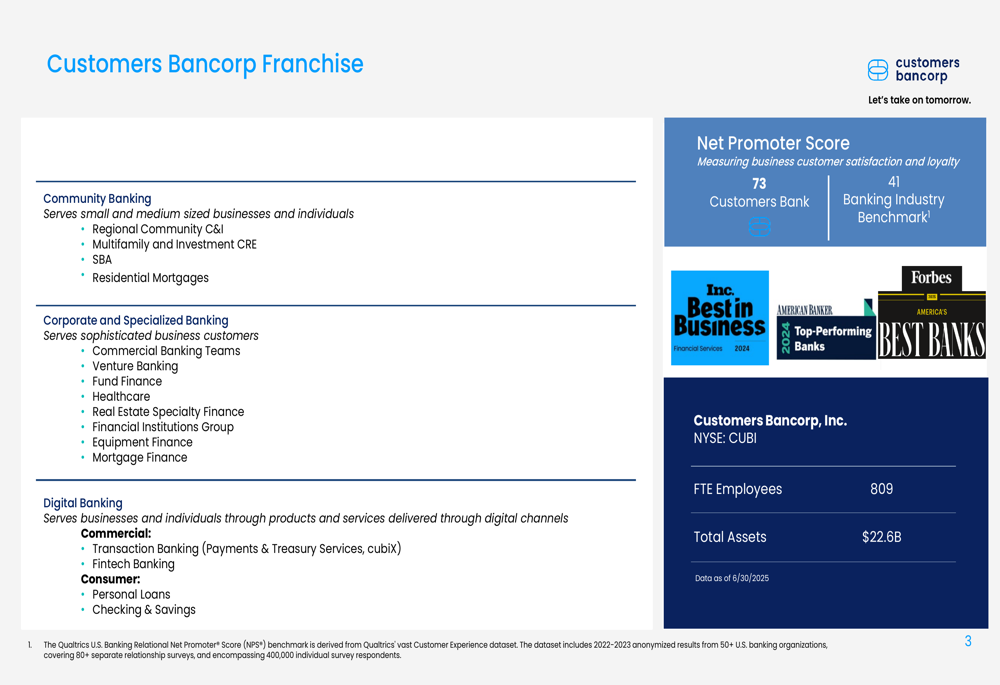

The bank’s franchise is structured around three primary segments: Community Banking, Corporate and Specialized Banking, and Digital Banking. This diversified approach has helped drive consistent growth and a Net Promoter Score of 73, significantly outperforming the banking industry benchmark of 41.

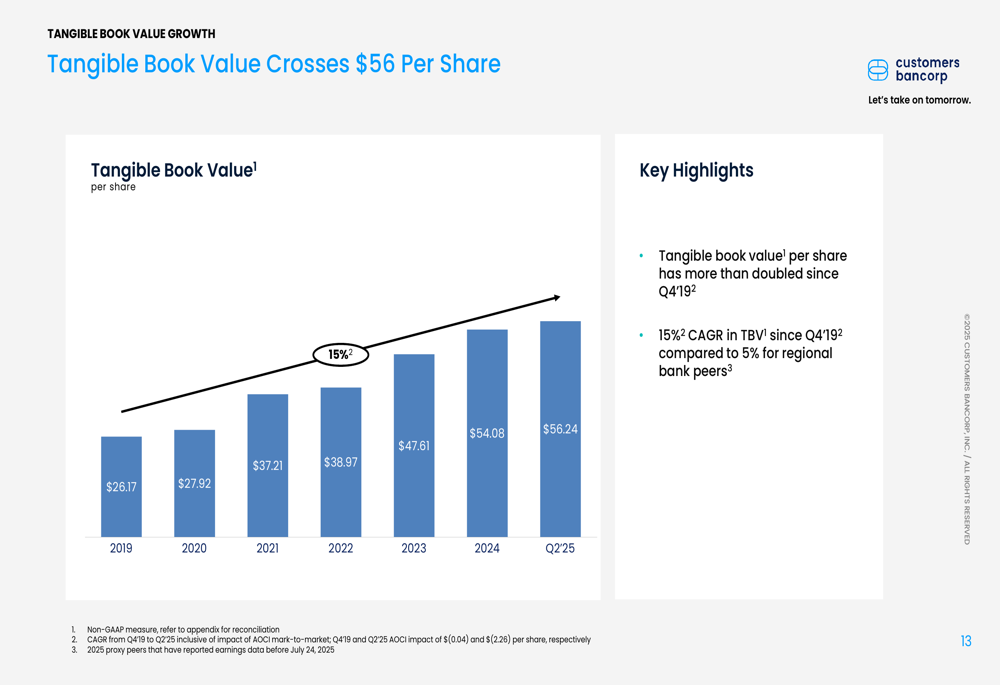

Tangible book value per share has more than doubled since Q4 2019, growing from $26.17 to $56.24 in Q2 2025. This represents a compound annual growth rate of 15%, compared to just 5% for regional bank peers.

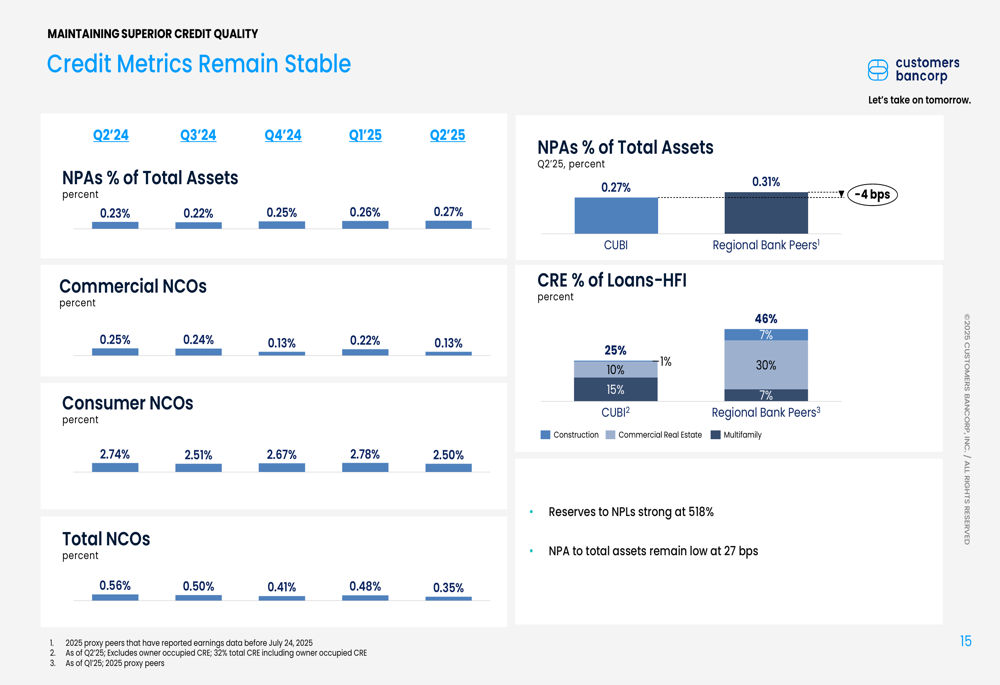

Credit quality remains strong, with a non-performing asset ratio of 0.27%, below the regional bank peer median. Reserves to non-performing loans stand at a robust 518%, reflecting the bank’s conservative risk management approach.

Management Outlook

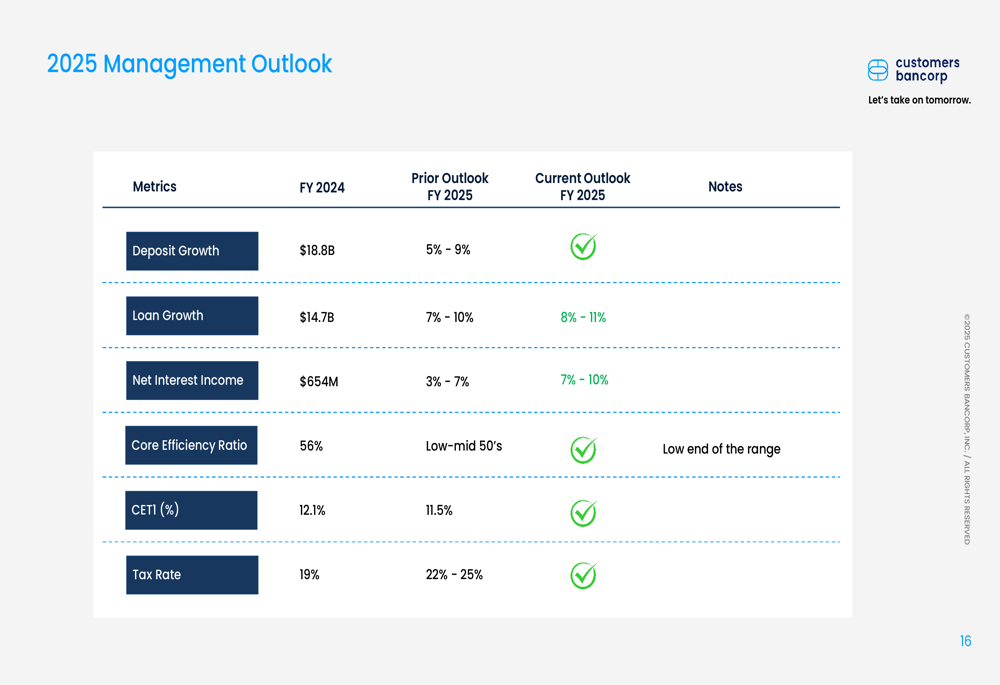

Looking ahead, Customers Bancorp management provided guidance for the remainder of 2025, projecting deposit growth of 5-9%, loan growth of 8-11%, and net interest income growth of 7-10%. The bank expects to maintain its core efficiency ratio in the low-to-mid 50s range, with a CET1 capital ratio target of approximately 11.5%.

This outlook aligns with the bank’s Q1 earnings call, where executives reaffirmed full-year loan growth guidance and projected a 3-7% year-over-year increase in net interest income. The consistent guidance suggests management’s confidence in the sustainability of current growth trends.

While the Q1 earnings report showed revenue falling short of expectations at $167.4 million versus the forecasted $190.3 million, the Q2 presentation emphasizes positive operating leverage and continued margin expansion, suggesting potential improvement in top-line performance.

The bank’s strategic focus on relationship banking, specialized vertical markets, and its increasingly significant cubix payments platform positions Customers Bancorp to potentially capitalize on both traditional banking growth and digital payment opportunities in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.