Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

CVB Financial Corp (NASDAQ:CVBF), the largest financial institution headquartered in California’s Inland Empire region, presented its first quarter 2025 results on April 24, 2025, highlighting its continued profitability streak and strong capital position despite challenging market conditions.

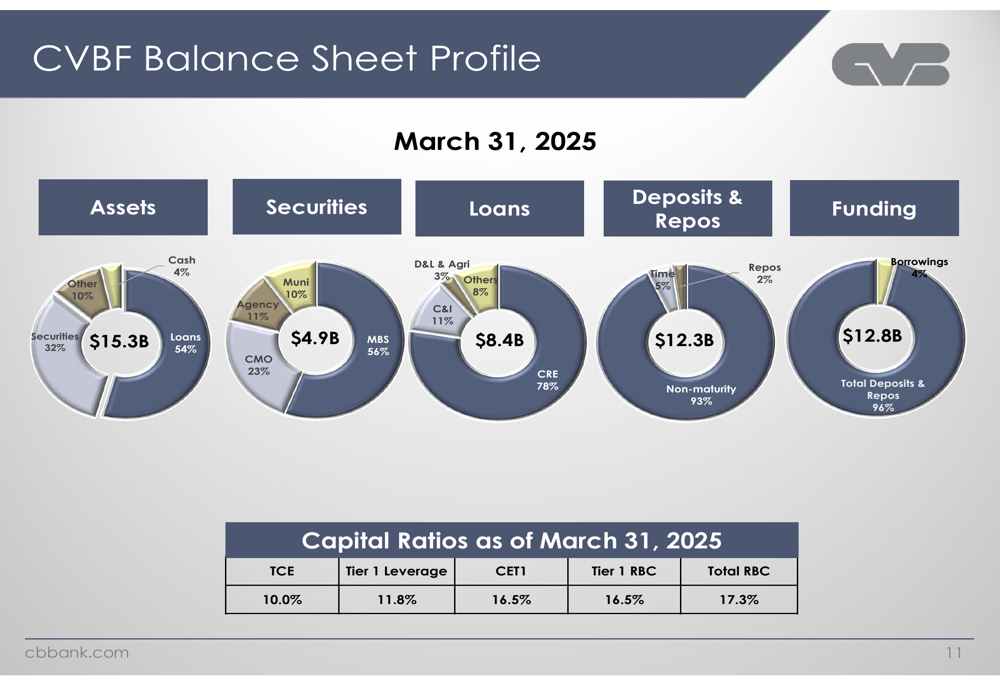

The bank, with $15.3 billion in total assets, reported net income of $51.1 million and earnings per share of $0.36 for Q1 2025, maintaining its remarkable 48-year profitability streak spanning 192 consecutive quarters. This performance comes amid a banking environment characterized by deposit competition, margin pressures, and cautious loan demand.

CVBF shares closed at $18.78 on April 23, 2025, up 2.01% for the day, though premarket trading on April 24 showed a 4.1% decline to $18.01 ahead of the presentation.

Quarterly Performance Highlights

CVB Financial reported Q1 2025 net income of $51.1 million, slightly higher than the $50.9 million reported in Q4 2024 and up from $48.6 million in Q1 2024. Earnings per share remained stable at $0.36, consistent with the previous quarter.

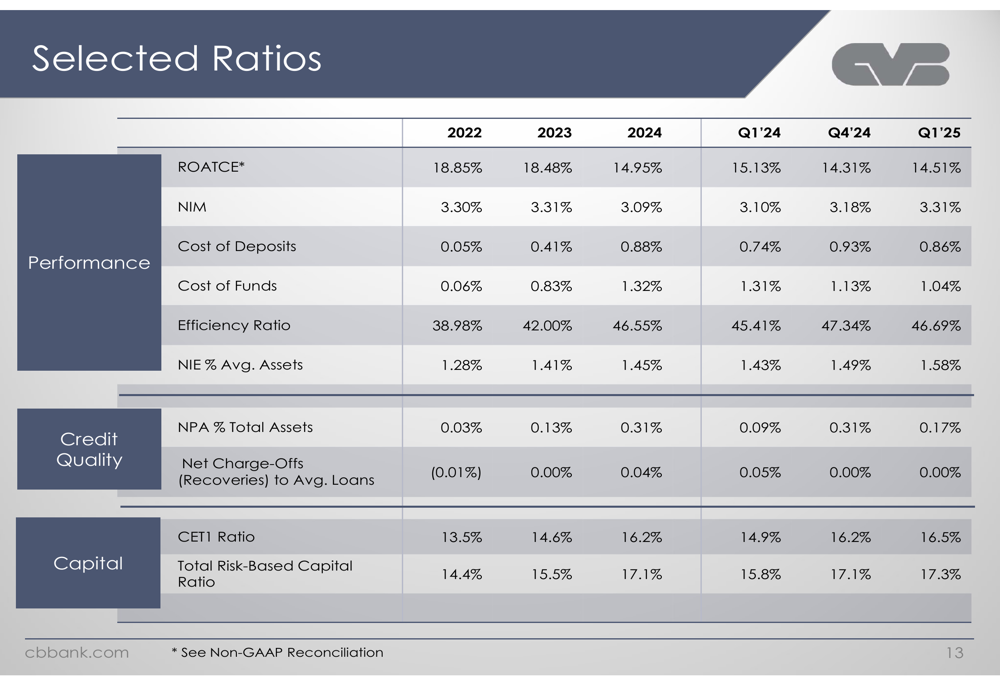

The bank’s profitability metrics remained strong, with a Return on Average Tangible Common Equity (ROATCE) of 14.51% and Return on Average Assets (ROAA) of 1.37% for Q1 2025. The efficiency ratio improved to 46.7% from 47.3% in the previous quarter.

As shown in the following chart of quarterly financial ratios, CVB Financial has maintained solid performance metrics over recent years, though with some moderation from the peak levels seen in 2022:

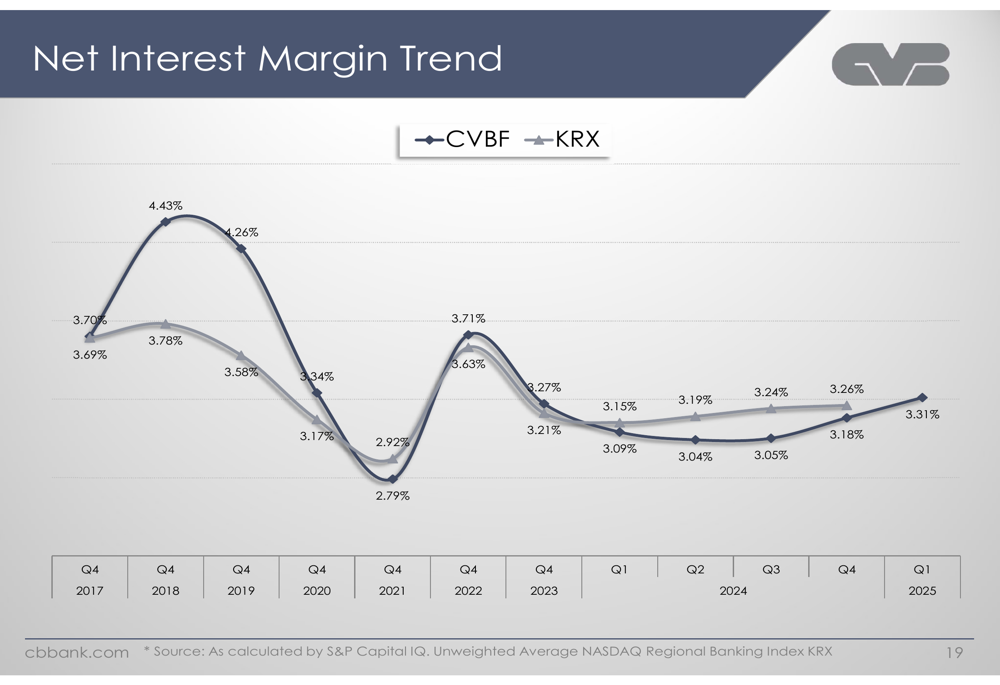

Net Interest Income remained stable at $110.4 million in Q1 2025, unchanged from Q4 2024. However, the Net Interest Margin (NIM) improved to 3.31% from 3.18% in the previous quarter, reversing a declining trend seen in previous periods.

The following chart illustrates how CVB Financial’s Net Interest Margin has consistently outperformed the NASDAQ Regional Banking Index (KRX) average over time:

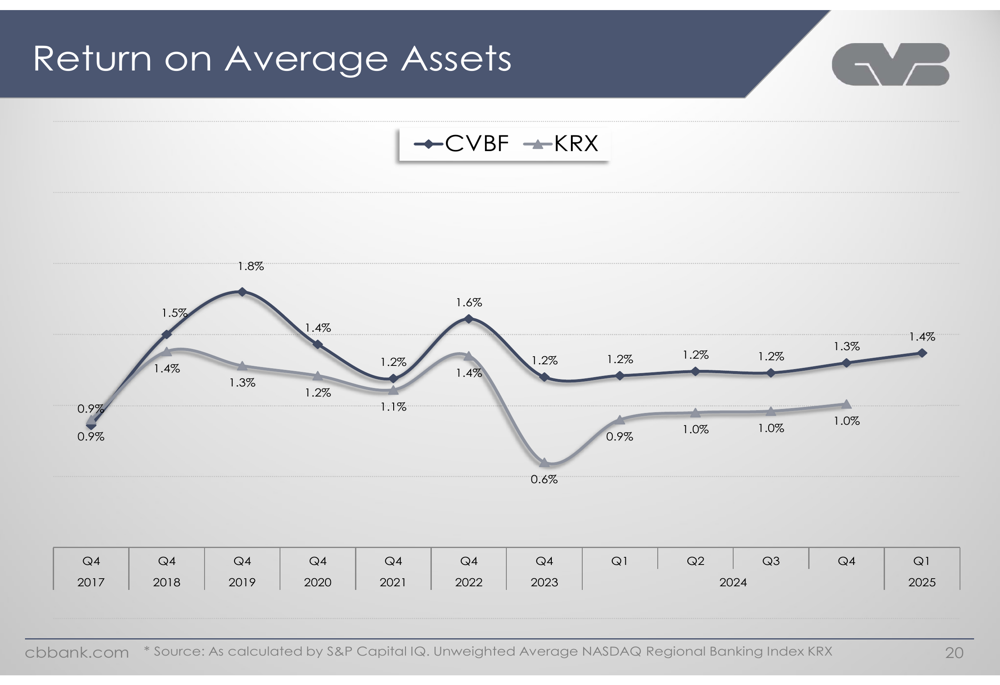

Similarly, CVB Financial’s Return on Average Assets has maintained a significant premium over the industry average, despite the challenging banking environment:

The bank’s Return on Average Tangible Common Equity also continues to outperform the industry benchmark:

Deposit Base and Funding

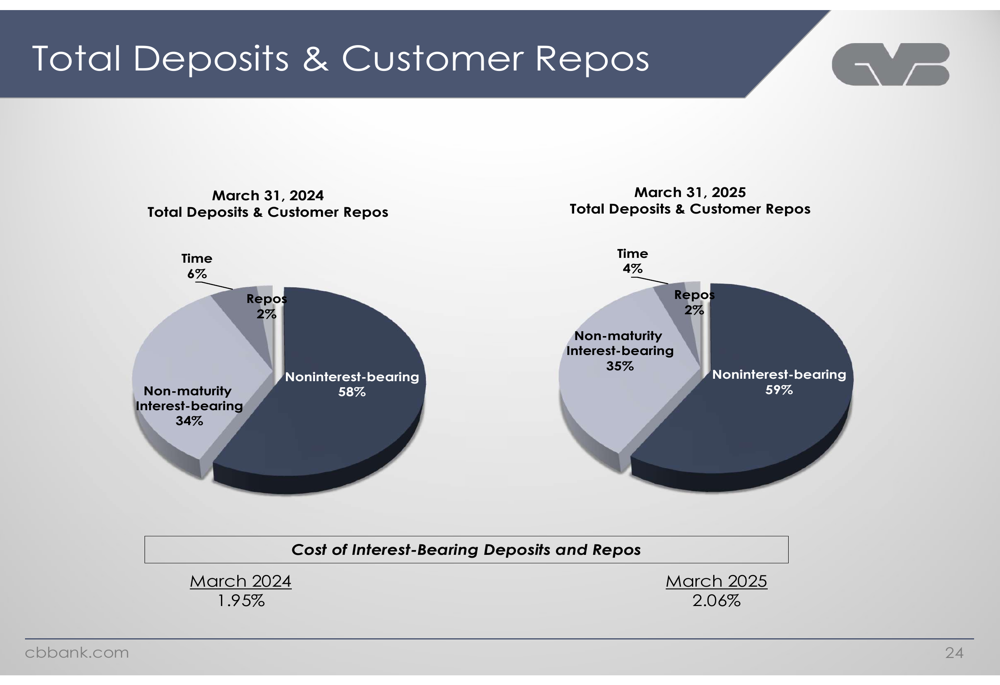

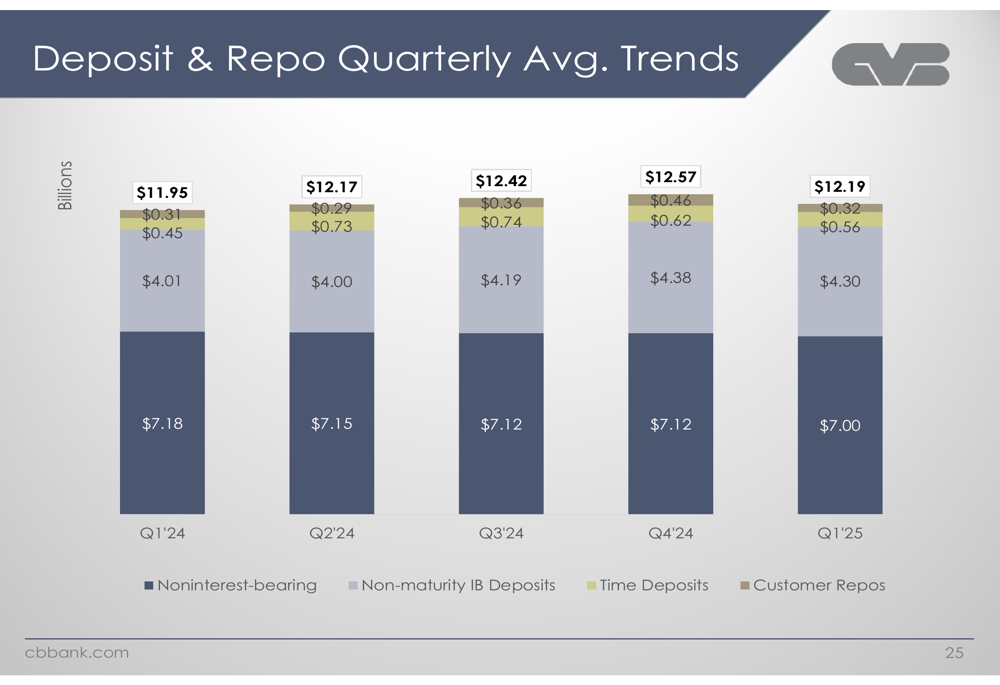

A key strength for CVB Financial continues to be its robust deposit franchise, particularly its high proportion of noninterest-bearing deposits, which represented 59% of total deposits as of March 31, 2025, up from 58% at the end of 2024.

The bank’s deposit composition has remained relatively stable year-over-year, with noninterest-bearing deposits increasing slightly from 58% to 59% of the total, while time deposits decreased from 6% to 4%:

Looking at quarterly trends, total deposits and customer repos averaged $12.19 billion in Q1 2025, down slightly from $12.57 billion in Q4 2024. Noninterest-bearing deposits averaged $7.00 billion, showing a slight decrease from previous quarters:

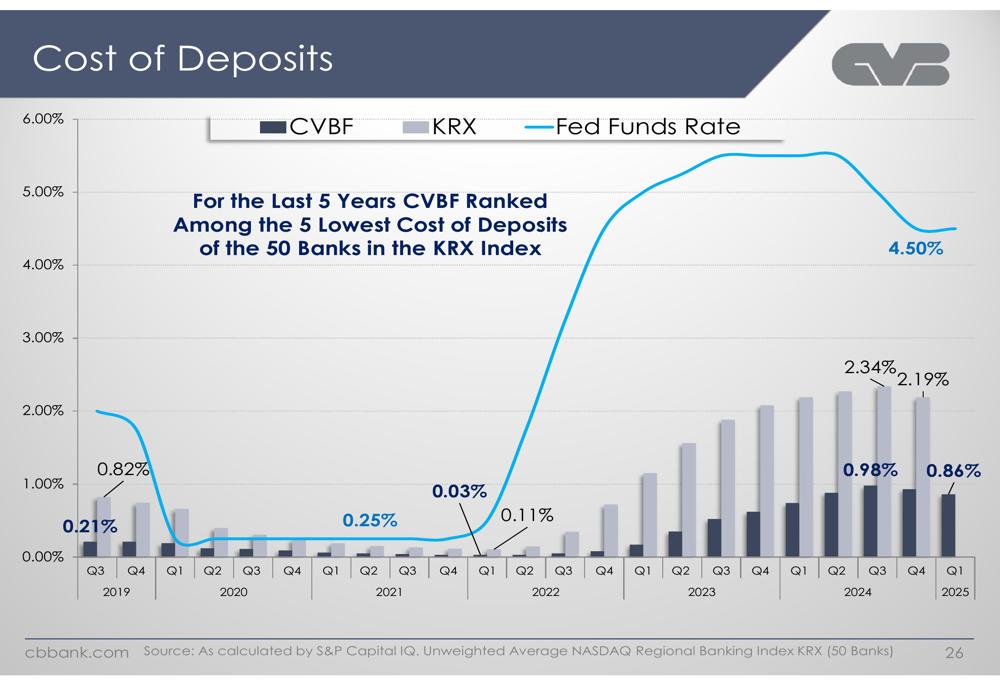

CVB Financial maintains one of the lowest cost of deposits among its peers, consistently ranking among the five lowest in the 50-bank KRX Index over the past five years. This competitive advantage has been particularly valuable during the rising rate environment:

Loan Portfolio and Credit Quality

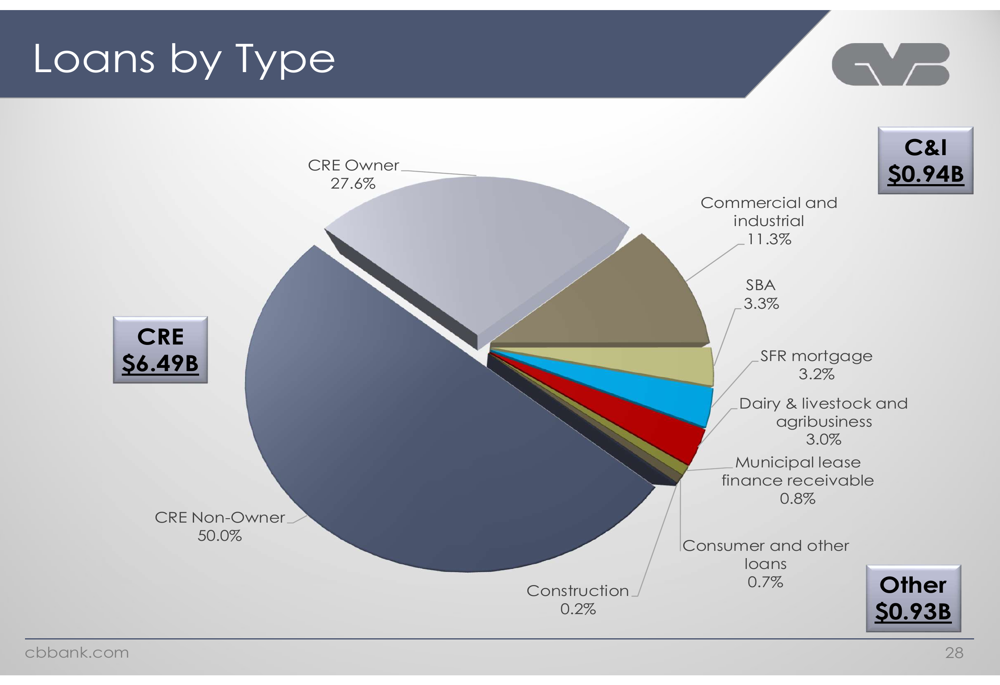

The bank’s loan portfolio totaled $8.4 billion as of March 31, 2025, with commercial real estate (CRE) loans representing 77.6% of the total portfolio. Commercial and industrial loans accounted for 11.3%, while dairy, livestock, and agribusiness loans made up 3.0%.

The following chart shows the breakdown of CVB Financial’s loan portfolio by type:

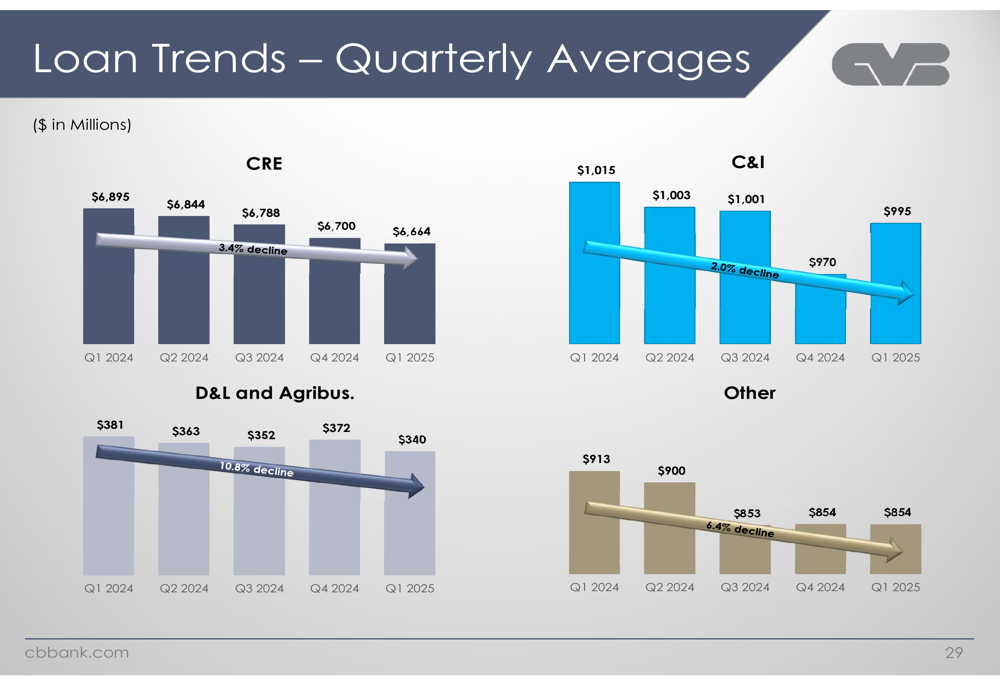

Loan trends show declining balances across all major categories, reflecting the bank’s cautious approach in the current economic environment. Commercial real estate loans, the largest component, declined 3.4% from Q1 2024 to Q1 2025:

Credit quality remains strong, with Q1 2025 net recoveries of $130,000 and nonperforming assets to total assets ratio of 0.17%, down from 0.31% in Q4 2024. The bank recaptured $2 million in provision for credit losses during the quarter.

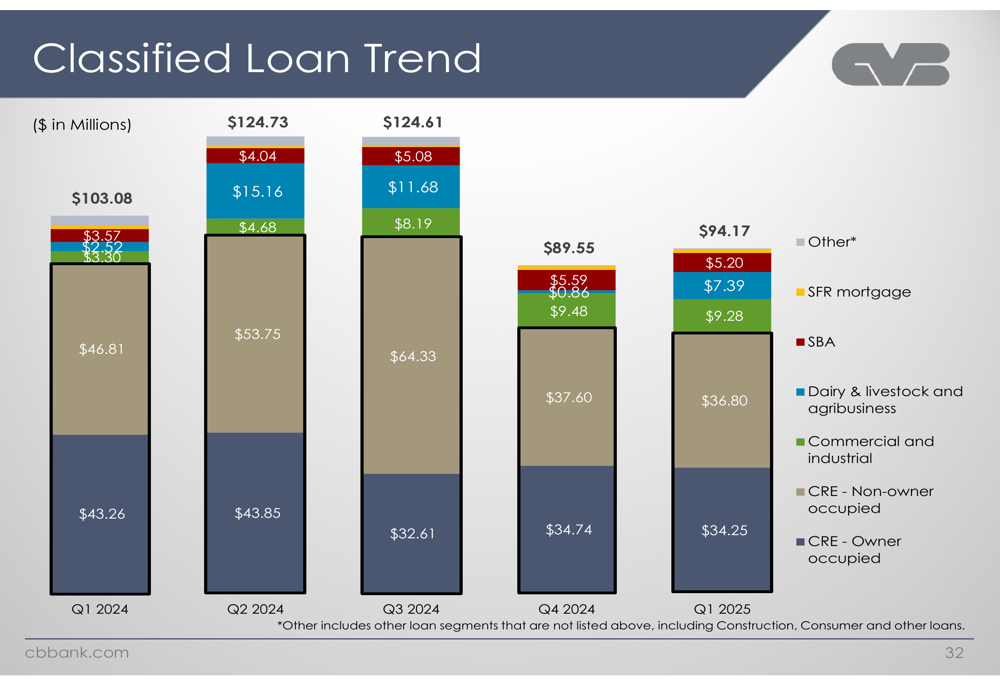

Classified loans totaled $94.2 million or 1.13% of total loans, showing some fluctuation but remaining at manageable levels:

Capital Position and Shareholder Returns

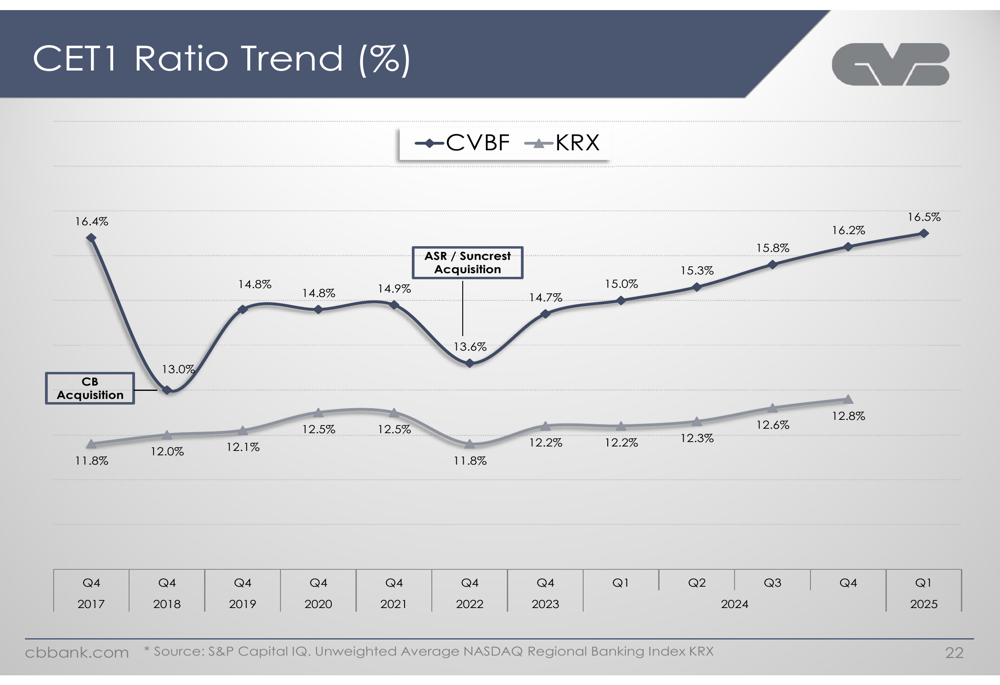

CVB Financial maintains a robust capital position, with a Common Equity Tier 1 (CET1) ratio of 16.5% and a total risk-based capital ratio of 17.3% as of March 31, 2025. The tangible common equity ratio stood at 10.0%.

The following chart illustrates how CVB Financial’s CET1 ratio compares favorably to the industry average:

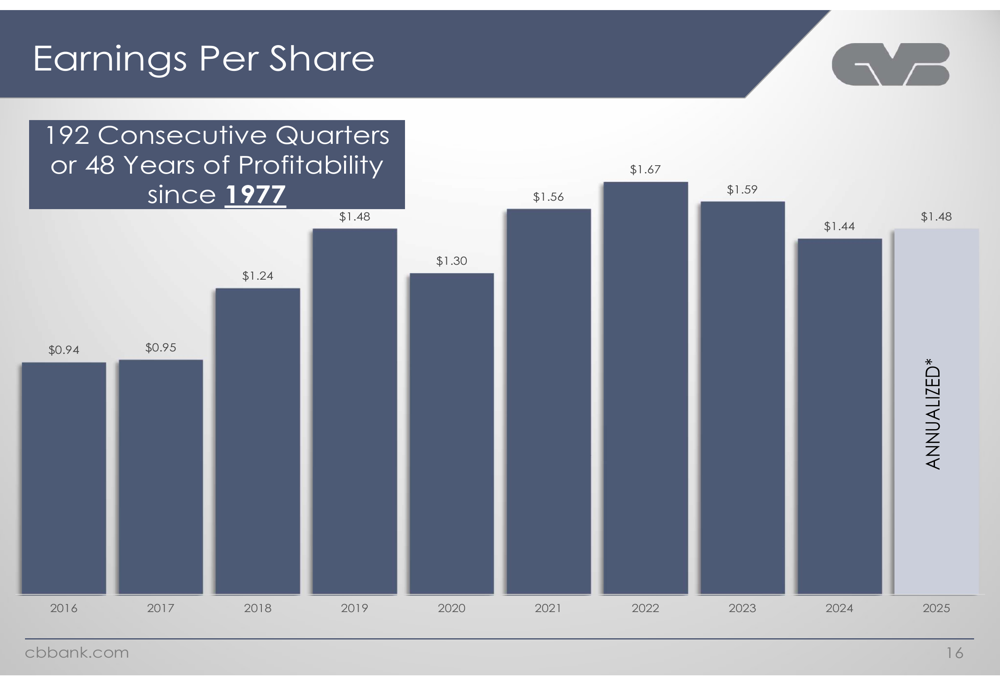

The bank’s earnings per share has shown some moderation in recent years after peaking at $1.67 in 2022, with 2025 annualized EPS projected at $1.48 based on Q1 results:

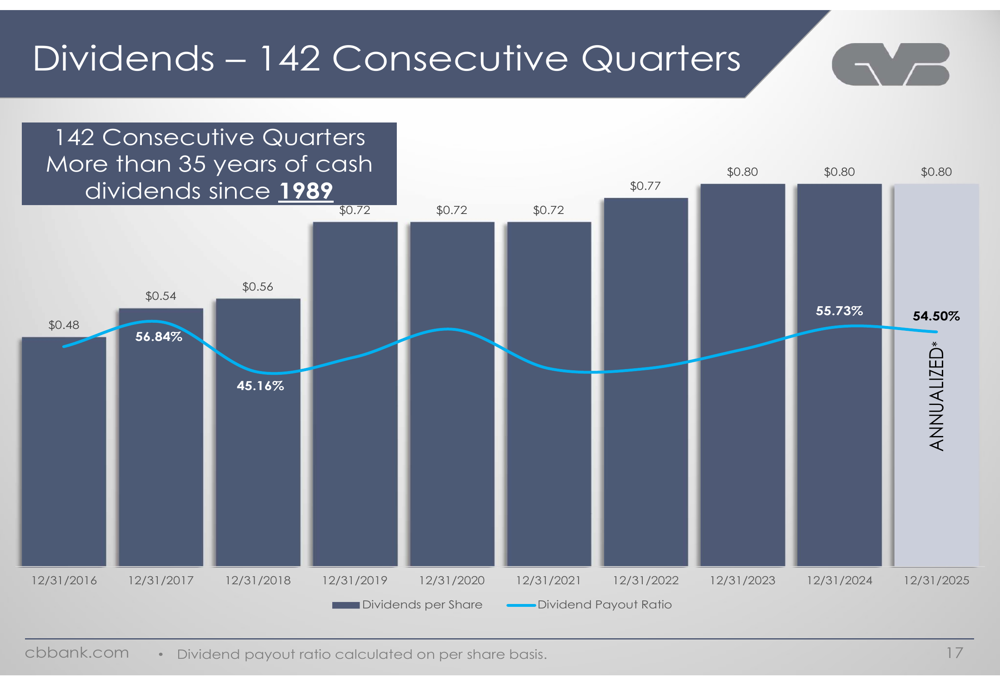

A hallmark of CVB Financial’s shareholder return strategy has been its consistent dividend payments, now spanning 142 consecutive quarters or more than 35 years. The current annualized dividend of $0.80 per share represents a significant increase from $0.48 in 2016:

Strategic Initiatives and Outlook

CVB Financial continues to focus on its target market of privately-held and family-owned businesses throughout California with annual revenues between $1-300 million. The bank’s growth strategy encompasses three key areas: de novo expansion, same-store sales growth, and strategic acquisitions.

For acquisitions, the bank is targeting institutions with $1-10 billion in assets in California markets, as well as banking teams in both existing and new markets. This disciplined approach to growth has served the bank well over its nearly five decades of continuous profitability.

Looking ahead, CVB Financial faces both opportunities and challenges. While its strong deposit franchise and capital position provide stability, the declining loan trends across all categories suggest cautious growth expectations in the near term. The bank’s consistent outperformance on key metrics like net interest margin and cost of deposits should continue to provide competitive advantages in the current banking environment.

The bank’s balance sheet remains well-positioned, with a diversified asset mix and strong capital ratios, as illustrated in this comprehensive overview:

With its long track record of profitability, strong capital position, and stable deposit base, CVB Financial appears well-equipped to navigate the evolving banking landscape while continuing to deliver value to shareholders through consistent dividends and prudent growth strategies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.