AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Cyber_Folks SA (WSE:CBF) presented its Q2 2025 financial results on September 2, 2025, showcasing record quarterly performance with revenues exceeding PLN 212 million. The Polish tech company, which provides hosting, e-commerce, and marketing solutions to approximately 400,000 clients globally, continues its long-standing pattern of 30-40% annual growth despite temporary pressure on net profit from recent strategic acquisitions.

The company’s stock closed at PLN 173.60 on September 3, 2025, up 0.93% following the presentation, reflecting market confidence in the company’s growth trajectory despite acquisition-related costs.

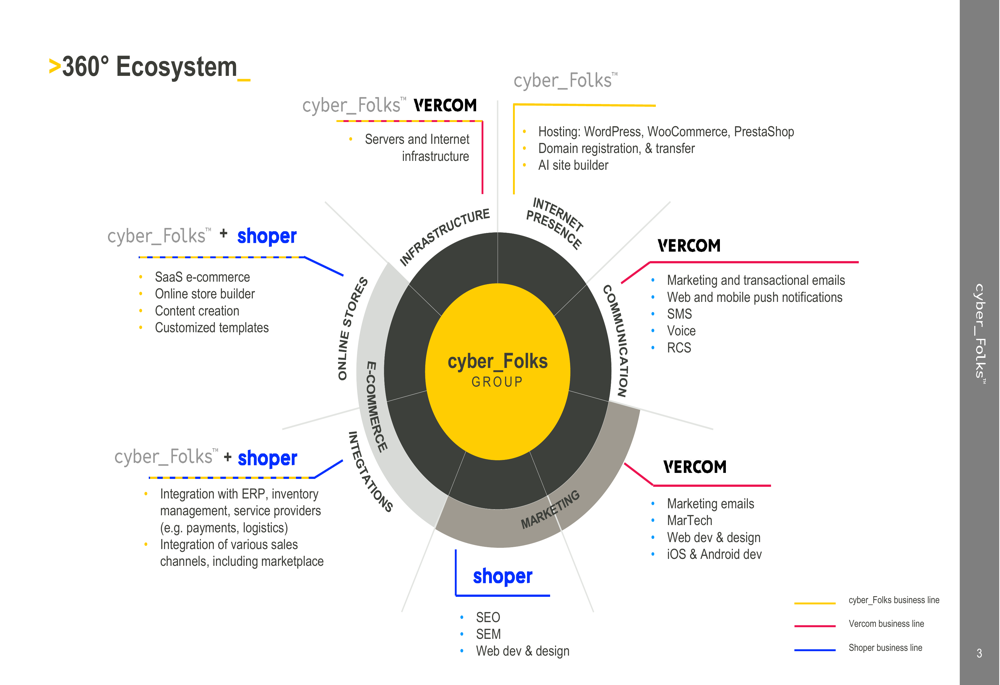

As shown in the following comprehensive ecosystem diagram, Cyber_Folks has built an integrated suite of digital services spanning infrastructure, e-commerce, and marketing technologies:

Quarterly Performance Highlights

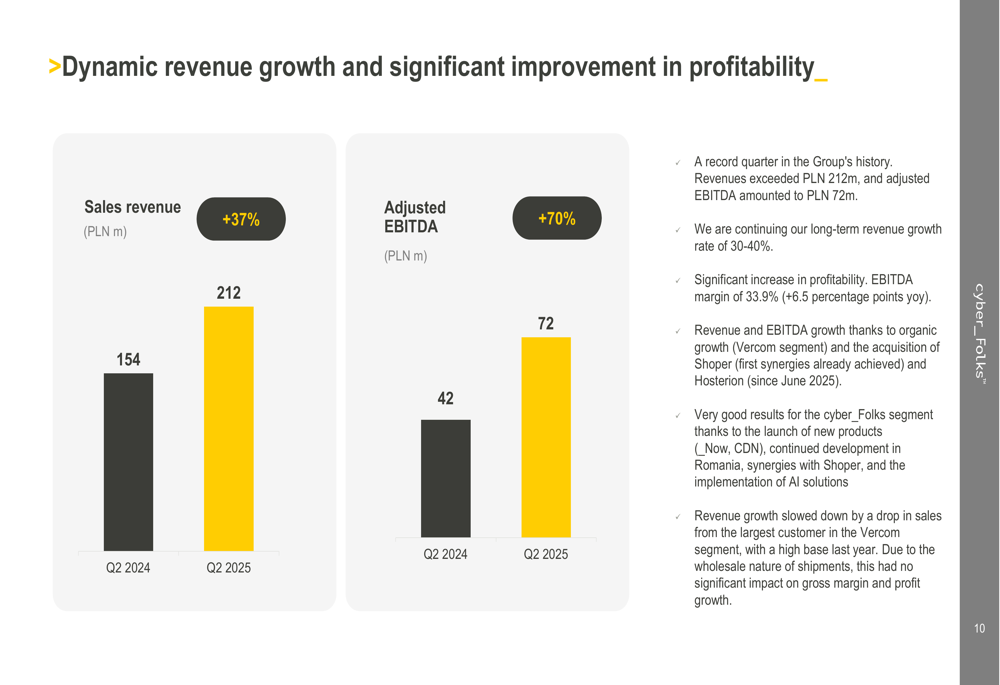

Cyber_Folks reported exceptional Q2 2025 results with sales revenue reaching PLN 212 million, a 37% increase year-over-year, while adjusted EBITDA surged 70% to PLN 72 million. The company’s EBITDA margin expanded significantly to 33.9%, representing a 6.5 percentage point improvement compared to the same period last year.

The following chart illustrates the company’s dynamic revenue and profitability growth for Q2 2025:

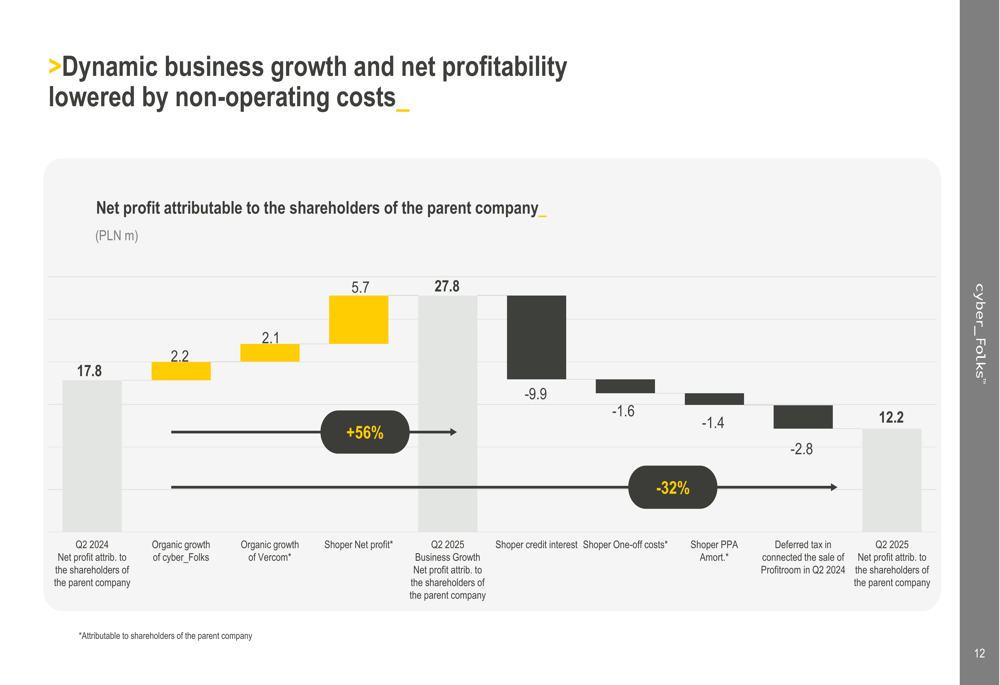

However, net profit attributable to shareholders declined 32% year-over-year to PLN 12.2 million, primarily due to costs associated with the Shoper acquisition, including credit interest (PLN 9.9 million), one-off costs (PLN 1.6 million), and PPA amortization (PLN 1.4 million). Excluding these acquisition-related expenses, the underlying business growth resulted in a net profit of PLN 27.8 million, representing a 56% increase from Q2 2024.

The following waterfall chart breaks down the components affecting net profit:

Detailed Financial Analysis

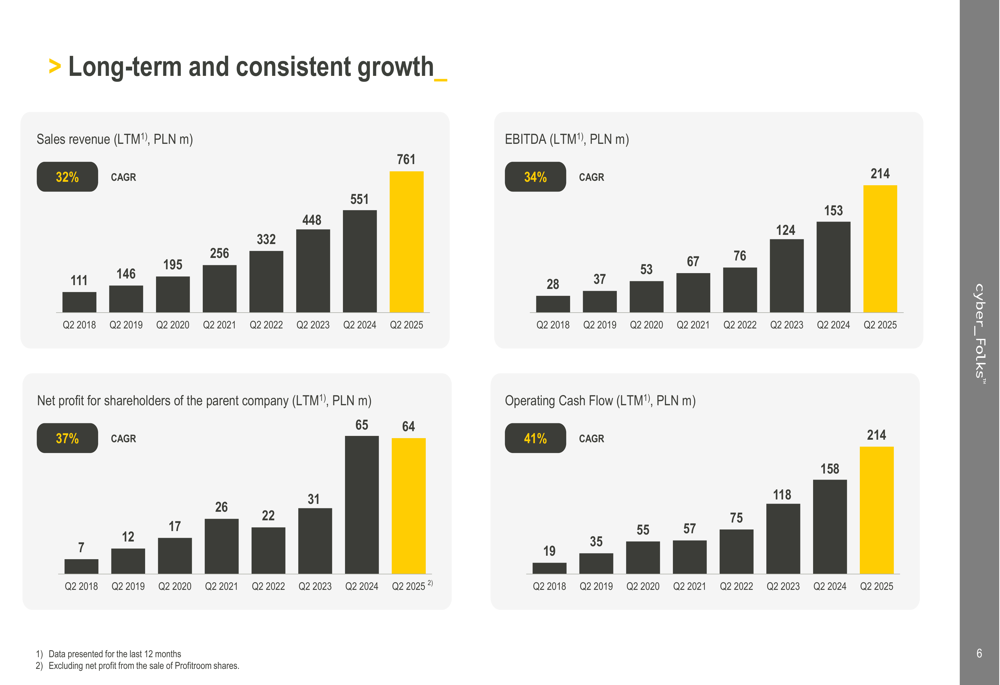

Cyber_Folks has maintained impressive long-term growth across all key financial metrics. Since Q2 2018, the company has achieved a 32% CAGR in sales revenue, 34% in EBITDA, 37% in net profit, and 41% in operating cash flow.

This consistent performance is visualized in the following multi-year financial overview:

The company’s cash generation capacity has been particularly strong, with operating cash flow reaching PLN 214.3 million for the last twelve months ending Q2 2025, maintaining the company’s 41% CAGR since 2019.

Despite recent acquisitions, Cyber_Folks maintains a manageable debt profile with a Net debt/Adjusted EBITDA ratio of 2.3x as of Q2 2025, calculated on a proforma basis including Shoper’s EBITDA contribution. This represents an increase from 0.5x in 2024 but remains within comfortable levels for a growth-oriented technology company.

Strategic Initiatives

Cyber_Folks’ growth strategy centers on both organic expansion and strategic acquisitions. The company recently acquired Hosterion, a leading Romanian hosting provider, for EUR 5.7 million, strengthening its position in the CEE region. Hosterion manages over 12,000 hosting accounts and approximately 13,000 active customers, contributing PLN 0.81 million in revenue and PLN 0.26 million in EBITDA for June 2025 alone.

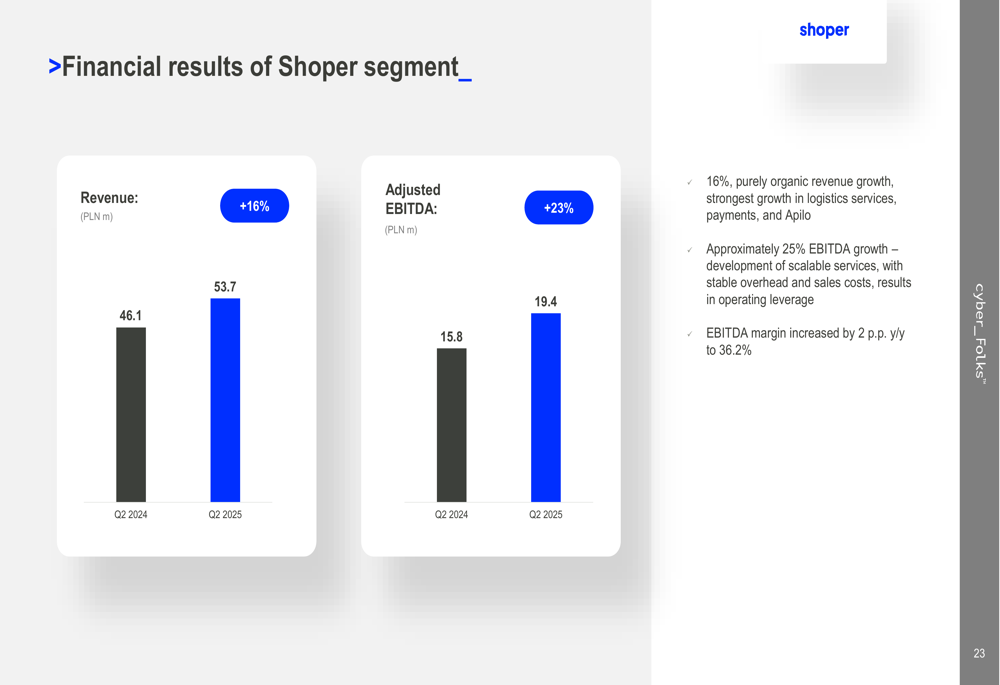

The more significant acquisition of Shoper, Poland’s largest e-commerce platform, has already shown positive results with 16% organic revenue growth and 23% EBITDA growth in Q2 2025. Shoper’s GMV (Gross Merchandise Value) reached PLN 5.2 billion in Q2 2025, with PLN 2 billion achieved in June 2025 alone.

The performance of the Shoper segment is detailed in the following chart:

Cyber_Folks’ core hosting segment also demonstrated strong performance with 16% revenue growth and 27% EBITDA growth year-over-year. The Vercom segment, which provides marketing and communication solutions, achieved 12% revenue growth and 21% EBITDA growth when excluding its largest customer.

The company has established strategic partnerships with global technology leaders, including Microsoft, which generates over 100 customer leads per month, helping Cyber_Folks land several enterprise customers globally.

Forward-Looking Statements

Cyber_Folks aims to maintain its position as the CEE leader in e-commerce SaaS while becoming one of Europe’s leading technology companies. The company expects the Shoper acquisition to have a positive impact on EPS over time, despite current interest costs. Quarterly interest costs from the Shoper acquisition loan are projected to decline from PLN 9.9 million in Q2 2025 to PLN 4.5 million by Q2 2030.

The company continues its shareholder-friendly dividend policy, with total transfers to shareholders in 2025 reaching PLN 38.3 million, including PLN 28.3 million in dividends. This represents a 58% CAGR in dividends and share buybacks since 2020, making Cyber_Folks one of 30 companies in the WIGdiv index dedicated to companies that regularly pay dividends.

Management expressed confidence in maintaining similar dividend growth rates in the coming years, supported by the company’s strong cash generation capacity and long-term growth trajectory, as illustrated in the company’s exponential revenue growth chart:

With its comprehensive ecosystem of digital services, consistent financial performance, and strategic acquisitions, Cyber_Folks appears well-positioned to continue its growth trajectory while gradually overcoming the temporary impact of acquisition-related costs on bottom-line results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.