September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

Danaher Corporation (NYSE:DHR) released its first quarter 2025 earnings presentation on April 22, 2025, revealing mixed financial results across its business segments. The life sciences and diagnostics company reported a slight revenue decline but showed particular strength in its Biotechnology segment. Danaher’s stock responded positively in premarket trading, up 2.72% to $190, suggesting investors were encouraged by certain aspects of the results despite the overall modest performance.

The company continues to position itself as a focused life sciences and diagnostics innovator, emphasizing its differentiated science and technology portfolio and the Danaher Business System (DBS) as key competitive advantages in navigating a dynamic operating environment.

Quarterly Performance Highlights

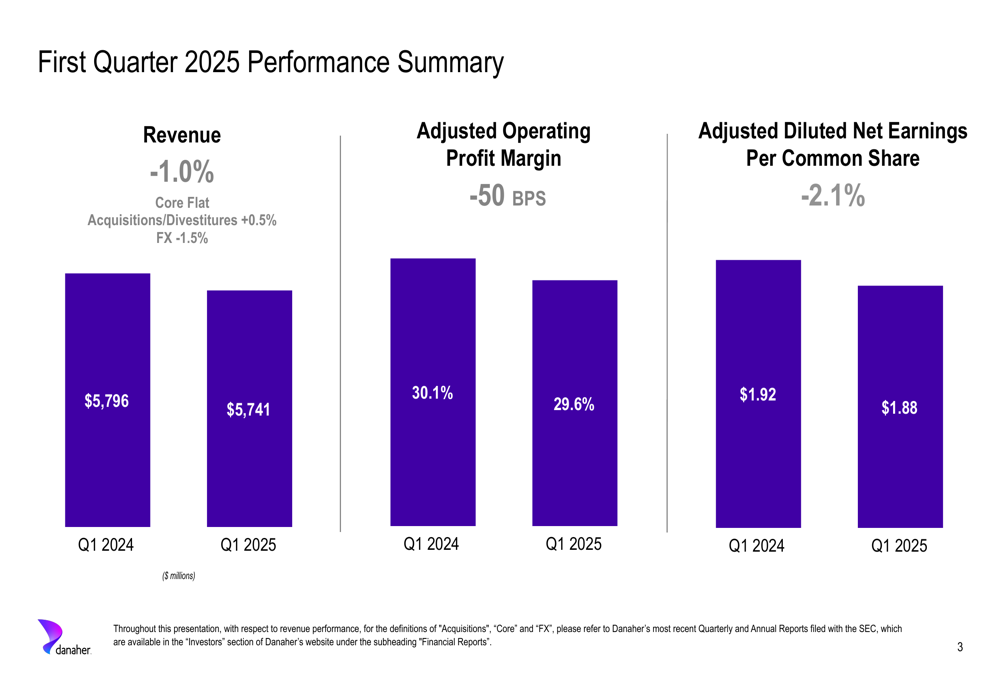

For the first quarter of 2025, Danaher reported total revenue of $5,741 million, representing a decrease of 1.0% compared to the same period last year. Core growth was flat, with acquisitions and divestitures contributing +0.5% and foreign exchange creating a -1.5% headwind.

The company’s adjusted operating profit margin came in at 29.6%, a decrease of 50 basis points compared to 30.1% in Q1 2024. Adjusted diluted net earnings per common share were $1.88, down 2.1% from $1.92 in the prior-year period.

As shown in the following summary of first quarter performance metrics:

Segment Analysis

Danaher’s performance varied significantly across its three main business segments, with Biotechnology emerging as the clear standout performer.

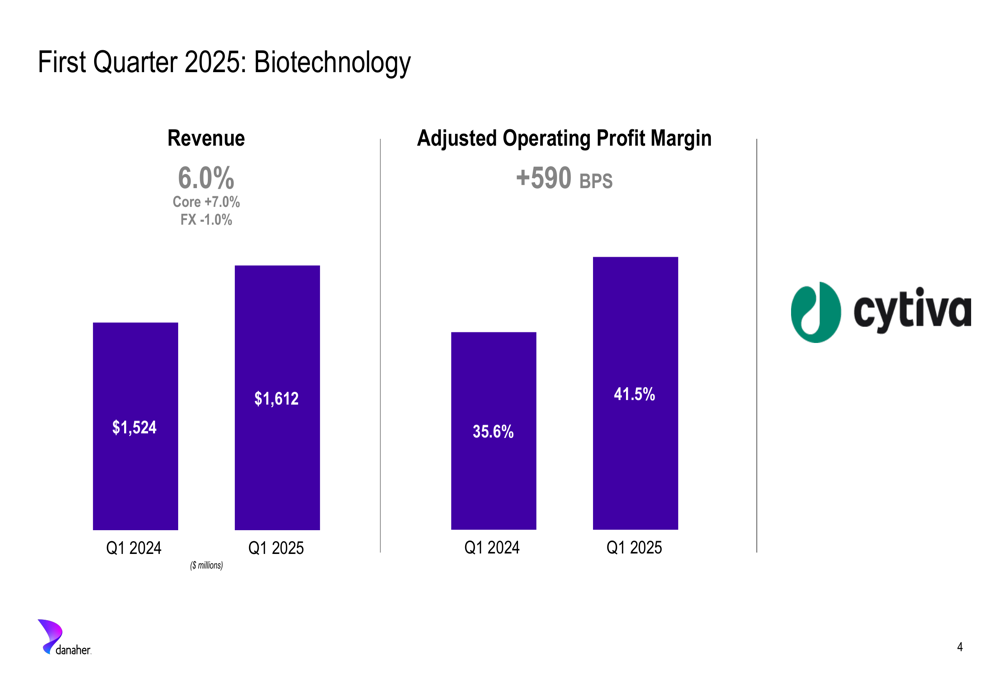

The Biotechnology segment, which includes the Cytiva brand, delivered revenue of $1,612 million, representing a solid increase of 6.0%. Core growth was even stronger at 7.0%, partially offset by a -1.0% foreign exchange impact. Most impressively, the segment’s adjusted operating profit margin expanded dramatically to 41.5%, an increase of 590 basis points compared to 35.6% in Q1 2024.

The following chart illustrates the Biotechnology segment’s performance:

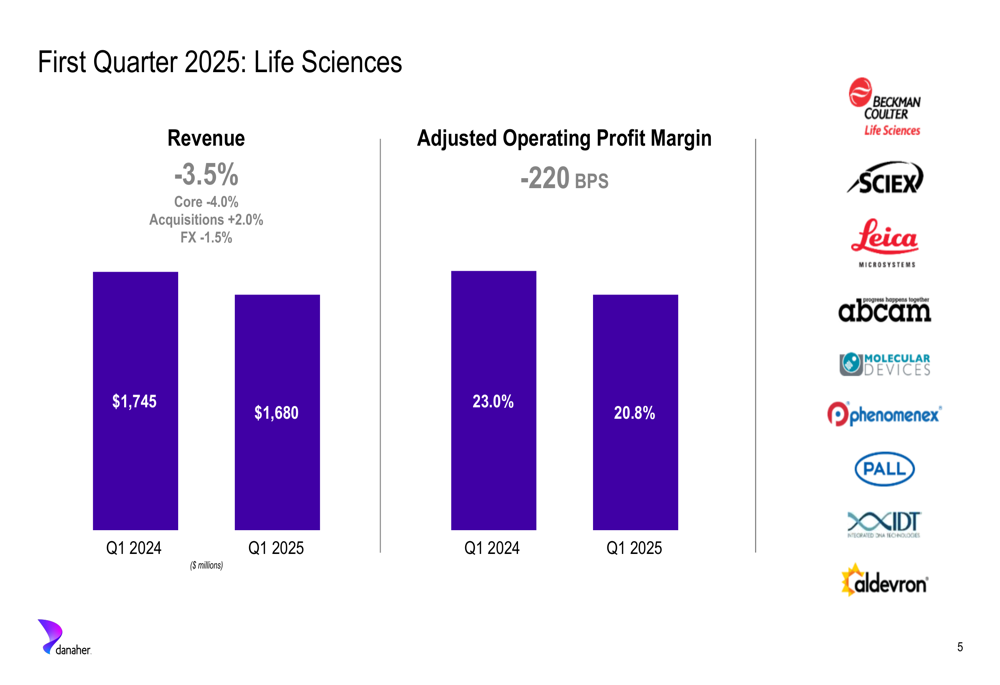

In contrast, the Life Sciences segment faced more significant challenges. Revenue declined by 3.5% to $1,680 million, with core growth down 4.0%. Acquisitions contributed 2.0% growth, but this was more than offset by a -1.5% foreign exchange impact. The segment’s adjusted operating profit margin contracted to 20.8%, a decrease of 220 basis points from 23.0% in Q1 2024.

The Life Sciences segment performance is detailed in this chart:

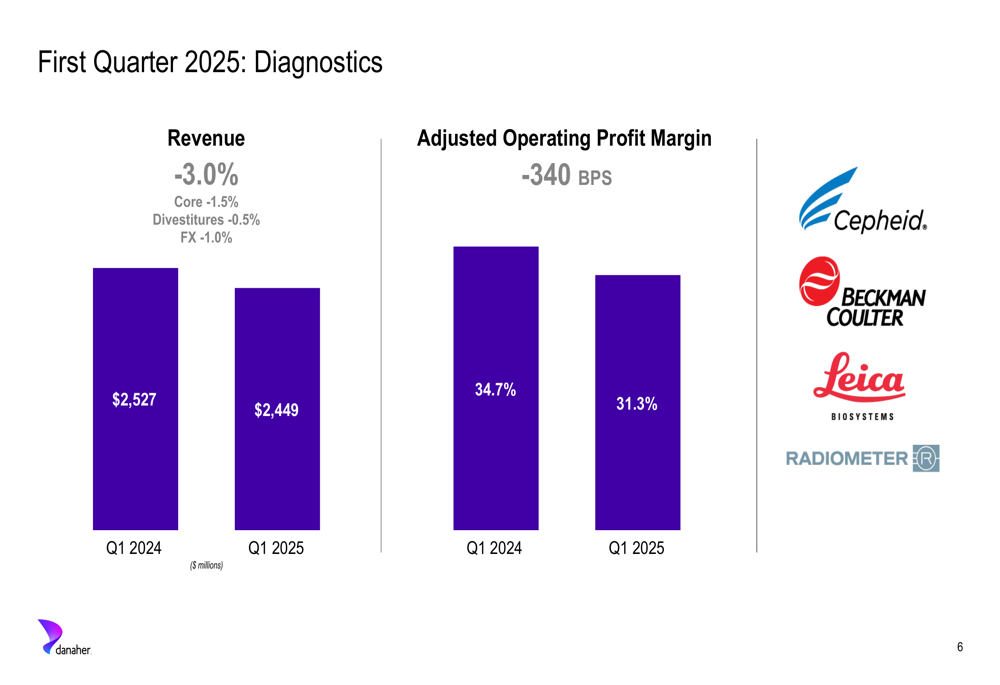

The Diagnostics segment also experienced headwinds, with revenue decreasing by 3.0% to $2,449 million. Core growth declined by 1.5%, with divestitures and foreign exchange contributing -0.5% and -1.0%, respectively. The segment’s adjusted operating profit margin fell to 31.3%, down 340 basis points from 34.7% in Q1 2024.

The following chart provides a detailed view of the Diagnostics segment performance:

Detailed Financial Analysis

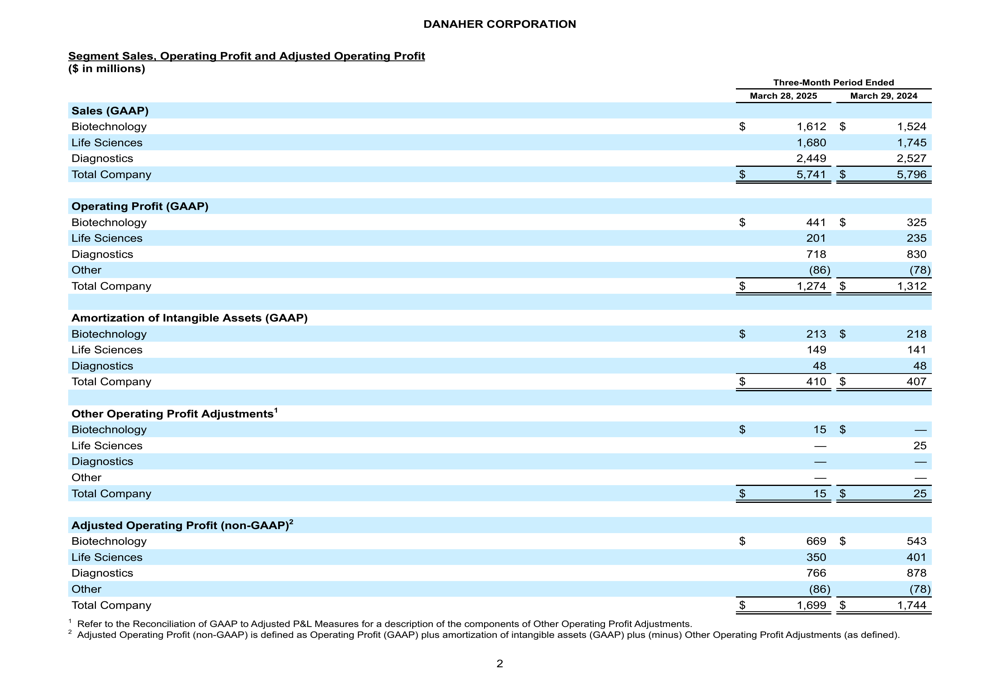

A deeper look at Danaher’s financial performance reveals additional insights into the company’s operations. The segment breakdown shows that Diagnostics remains the largest contributor to revenue at $2,449 million (42.7% of total), followed by Life Sciences at $1,680 million (29.3%) and Biotechnology at $1,612 million (28.1%).

Despite the overall revenue decline, Danaher maintained relatively strong profitability metrics. The company’s segment-level operating profit margins show significant variation, with Biotechnology leading at 41.5%, followed by Diagnostics at 31.3% and Life Sciences at 20.8%.

The following table provides a comprehensive view of segment sales, operating profit, and adjusted operating profit:

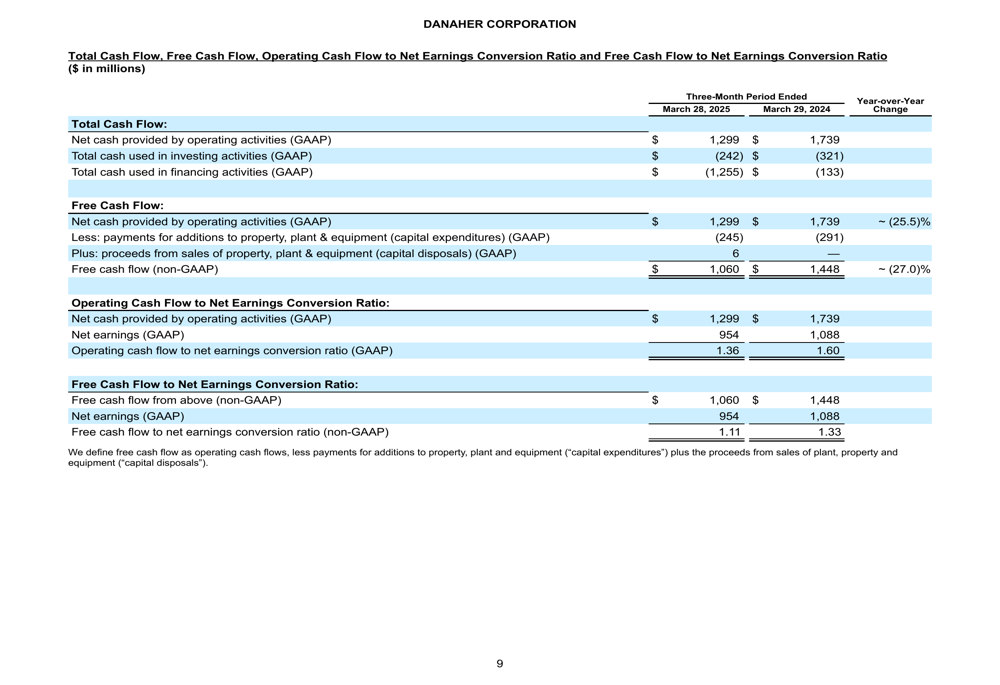

Cash flow performance remains a key strength for Danaher, as shown in the following breakdown of cash flow metrics:

Forward-Looking Statements

While the presentation slides did not include detailed forward guidance, the company’s previous earnings call from Q4 2024 had projected a low single-digit decline in core revenue for Q1 2025, which aligns with the flat core growth reported in this presentation.

For the full year 2025, Danaher had previously projected approximately 3% core revenue growth, with an approximately 2% revenue headwind due to the strengthening of the U.S. Dollar. The company had also expected a full-year adjusted operating profit margin of approximately 28.5%.

The Q1 2025 results suggest that Danaher is generally tracking in line with these projections, with the Biotechnology segment potentially outperforming expectations while Life Sciences and Diagnostics face more significant challenges.

Market Reaction & Analyst Perspectives

The market’s initial reaction to Danaher’s Q1 2025 results appears positive, with the stock rising 2.72% in premarket trading to $190. This suggests investors may be focusing on the strong performance in the Biotechnology segment and potentially viewing the overall results as in line with or slightly better than expectations.

The divergent performance across segments highlights both opportunities and challenges for Danaher. The robust growth and margin expansion in Biotechnology demonstrate the company’s strength in this critical area, while the headwinds in Life Sciences and Diagnostics may require additional strategic focus.

As Danaher continues to navigate a dynamic operating environment, its emphasis on innovation, operational excellence through the Danaher Business System, and strategic capital deployment will likely remain key factors in its ability to deliver long-term shareholder value.

The company’s transformation into a focused life sciences and diagnostics innovator positions it to capitalize on secular growth trends in these markets, though near-term challenges in certain segments may require continued attention to maintain overall growth momentum.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.