China’s Xi speaks with Trump by phone, discusses Taiwan and bilateral ties

Darden Restaurants (NYSE:DRI) reported strong sales growth in its first quarter fiscal 2026 results presentation on September 18, 2025, but faces significant margin pressures across most of its restaurant brands. Despite posting impressive top-line numbers, the stock fell 7.57% in premarket trading to $192.99, suggesting investors remain concerned about profitability challenges in an inflationary environment.

Quarterly Performance Highlights

Darden delivered total sales of $3.0 billion in Q1, representing a 10.4% increase year-over-year, with same-restaurant sales growth of 4.7%. The company reported adjusted diluted net earnings per share from continuing operations of $1.97 and adjusted EBITDA of $439 million. During the quarter, Darden returned $358 million to shareholders.

As shown in the following financial highlights:

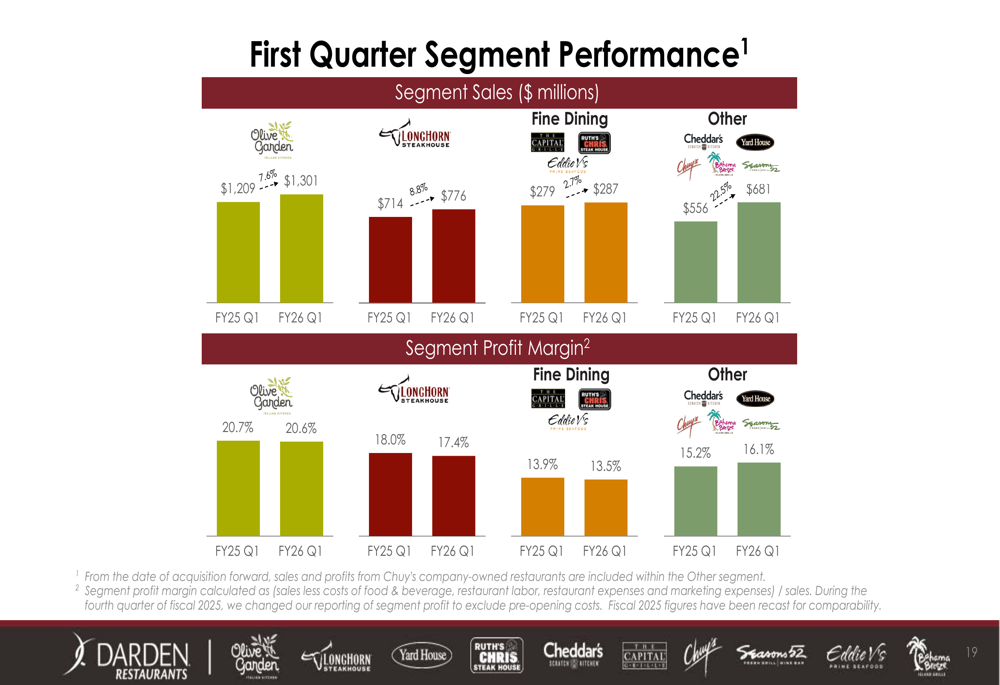

The company's segment performance showed mixed results across its restaurant portfolio. Olive Garden, Darden's largest brand, generated $1.3 billion in sales, up 7.6% from the prior year, while maintaining a relatively stable profit margin of 20.6%. LongHorn Steakhouse saw sales increase 8.8% to $776 million, though its profit margin contracted from 18.0% to 17.4% year-over-year.

The segment breakdown reveals both growth opportunities and profitability challenges:

The Fine Dining segment, which includes The Capital Grille, Ruth's Chris, and Eddie V's, experienced more modest growth of 2.7%, reaching $287 million in sales, with margins declining from 13.9% to 13.5%. The "Other" segment, which includes Yard House, Cheddar's, Chuy's, Bahama Breeze, and Seasons 52, showed the strongest profit margin improvement, increasing from 15.2% to 16.1% while delivering substantial sales growth.

Strategic Initiatives

Darden continues to leverage its portfolio of ten restaurant brands, emphasizing culinary innovation and service excellence as core competitive advantages. The company highlighted its significant scale, extensive data insights, and rigorous strategic planning as key differentiators in the competitive restaurant landscape.

The company's strategic positioning is illustrated in this overview:

Olive Garden, Darden's flagship brand, has launched several strategic initiatives including a partnership with Uber Direct Delivery, offering one million free deliveries to customers. The brand is also introducing lighter portion entrees to appeal to health-conscious diners while maintaining its value proposition with the "Never-Ending First Course" of soup or salad and breadsticks.

LongHorn Steakhouse continues to strengthen its market position, now ranked first by consumers for food quality, service, atmosphere, and value. This recognition underscores the brand's successful execution of its core steakhouse concept.

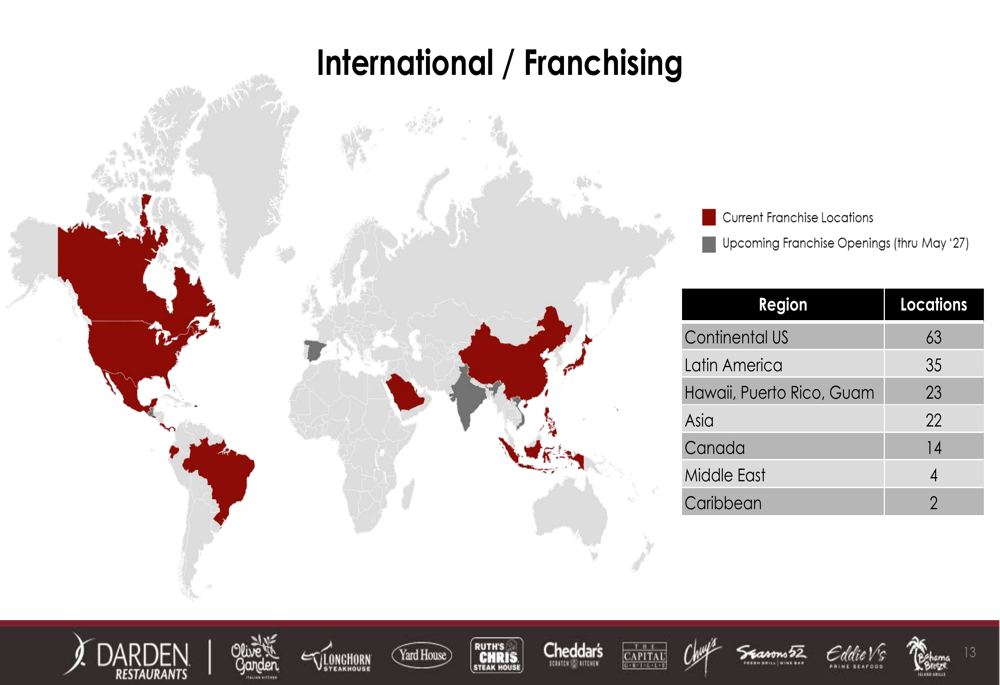

Darden is also expanding its international presence through franchising, with locations across multiple global regions. The company's global footprint is visualized in this map:

Beyond business growth, Darden emphasized its commitment to social responsibility through its partnership with Feeding America, having donated over 50 food trucks to food banks since January 2021.

Detailed Financial Analysis

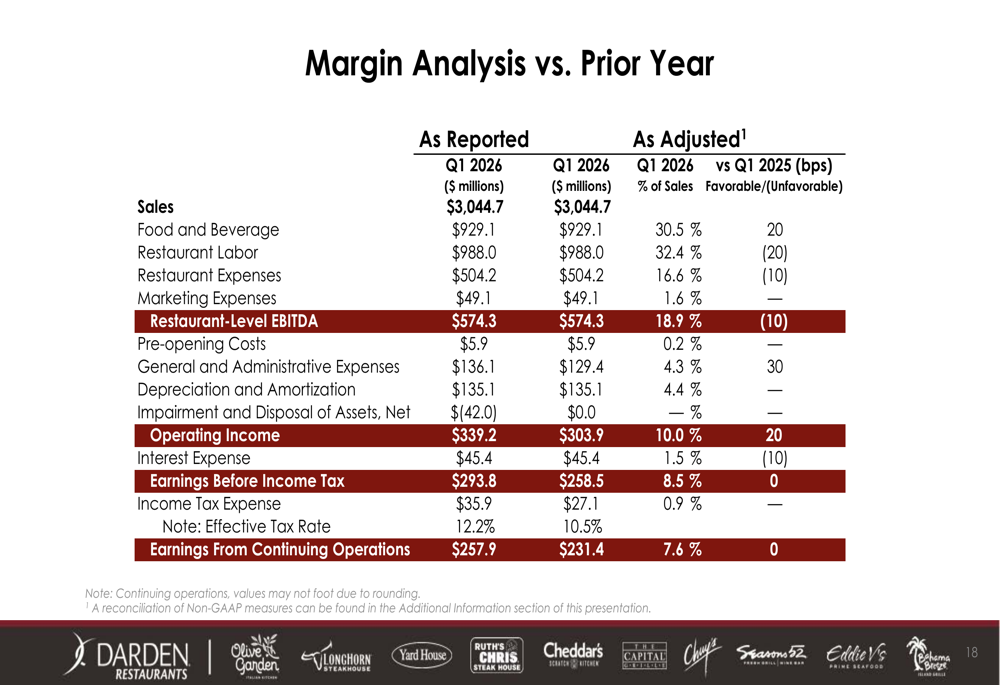

A closer examination of Darden's margin structure reveals the impact of ongoing inflationary pressures. While sales have grown substantially, restaurant-level EBITDA margins remained under pressure at 18.9% of sales.

The margin analysis provides insight into cost pressures:

Food and beverage costs represented 30.5% of sales, while restaurant labor costs accounted for 32.4%. These figures highlight the dual challenge of managing food inflation and labor costs in the current economic environment.

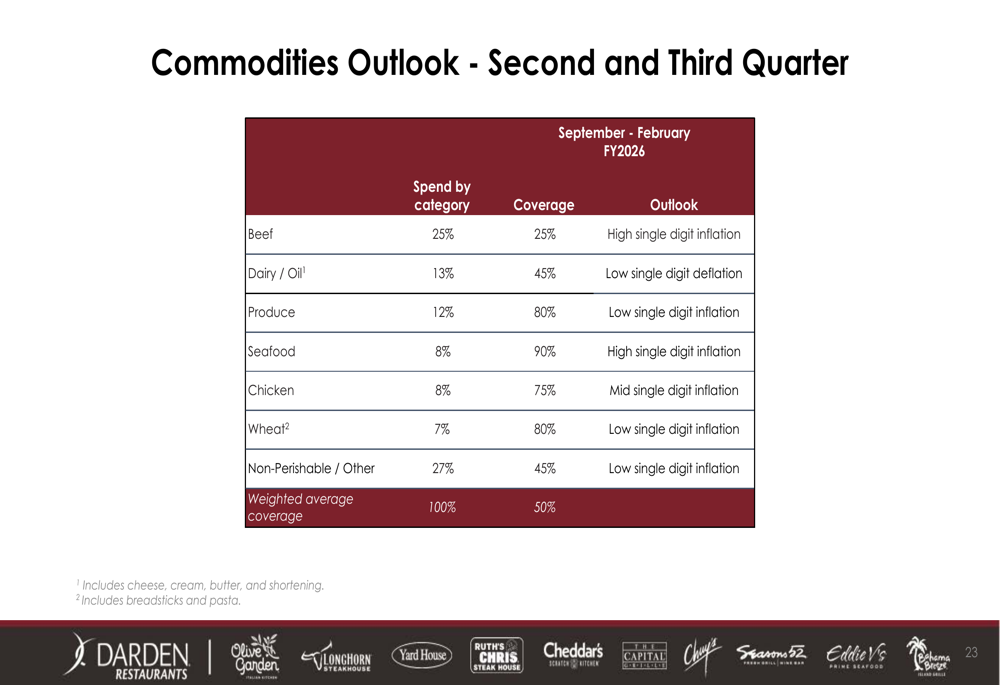

Looking ahead to Q2 and Q3 of fiscal 2026, Darden expects continued inflationary pressures across most commodity categories. Beef, which represents 25% of the company's commodity spend, is projected to see high single-digit inflation, while seafood is facing similar pressure. The company has varying levels of coverage across its commodity basket, ranging from 25% for beef to 90% for seafood.

Forward-Looking Statements

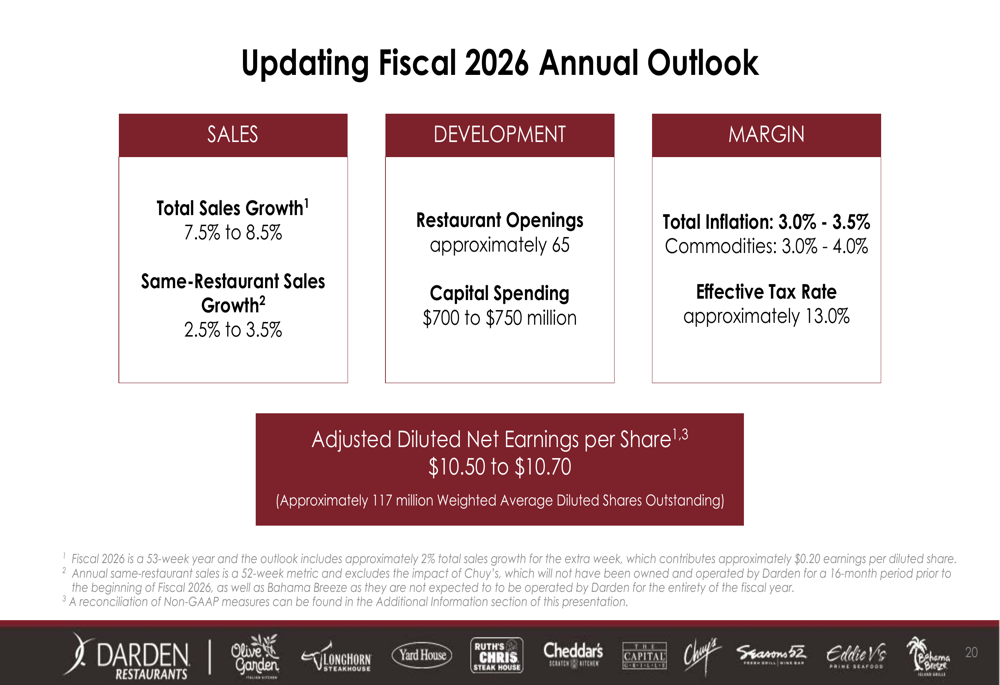

Despite the margin challenges, Darden provided an optimistic outlook for fiscal 2026, projecting total sales growth of 7.5% to 8.5% and same-restaurant sales growth of 2.5% to 3.5%. The company plans to open approximately 65 new restaurants and expects capital spending of $700 to $750 million.

Darden's detailed guidance for fiscal 2026 is outlined below:

The company anticipates total inflation of 3.0% to 3.5% for the fiscal year, with commodities inflation ranging from 3.0% to 4.0%. Darden projects adjusted diluted net earnings per share of $10.50 to $10.70, based on approximately 117 million weighted average diluted shares outstanding.

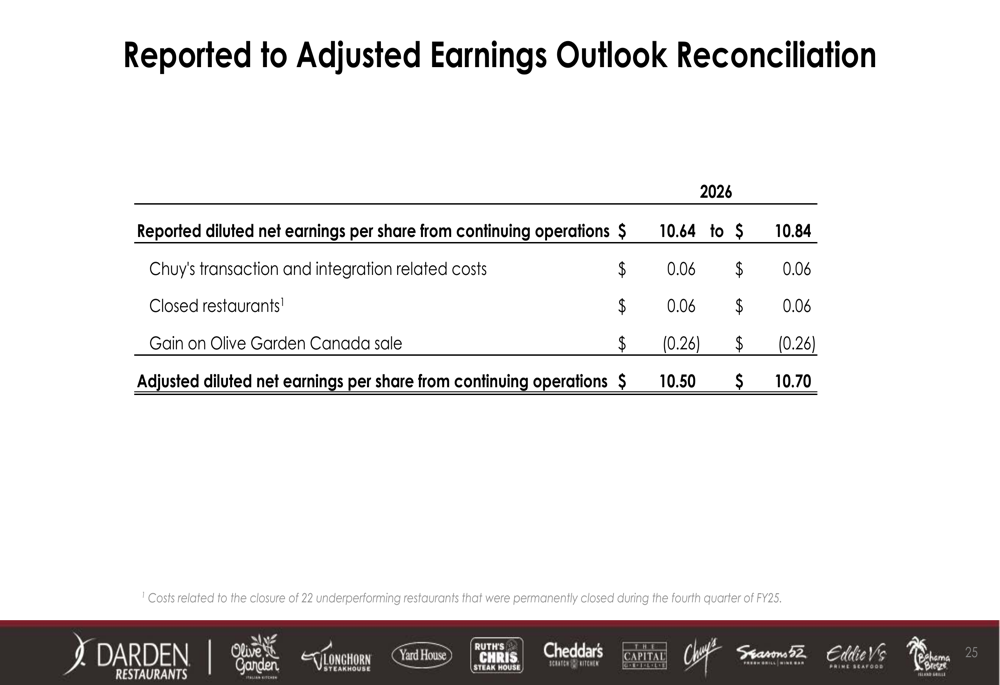

The earnings outlook includes several adjustments, including costs related to the Chuy's transaction and integration, closed restaurants, and a gain on the Olive Garden Canada sale. These adjustments bridge the gap between reported earnings per share of $10.64-$10.84 and adjusted earnings per share of $10.50-$10.70.

While Darden's sales growth remains impressive, the market reaction suggests investors are concerned about the company's ability to maintain profitability in the face of persistent inflation and competitive pressures. Management will need to demonstrate continued execution on both top-line growth and cost management to regain investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.