Bubble Wrap maker Sealed Air surges on report of buyout talks

Data Communications Management Ltd (TSX:DCM) presented its second quarter 2025 results on August 7, 2025, revealing a company navigating challenging market conditions with improved profitability metrics despite revenue declines. The presentation highlighted the company’s focus on operational efficiency, strategic growth initiatives, and capital allocation priorities in an uncertain economic environment.

Quarterly Performance Highlights

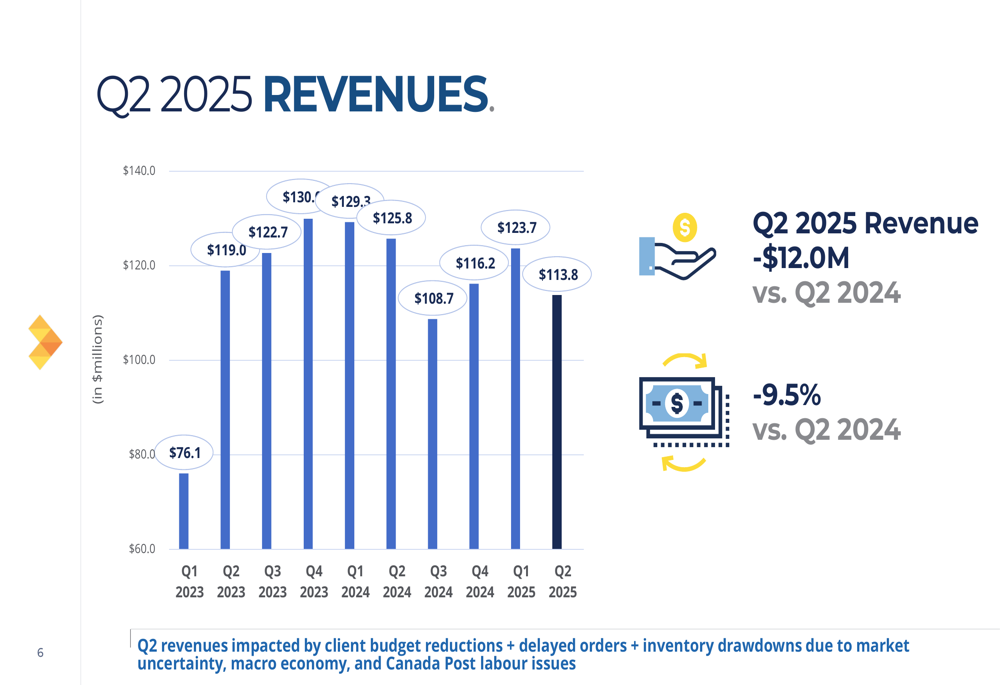

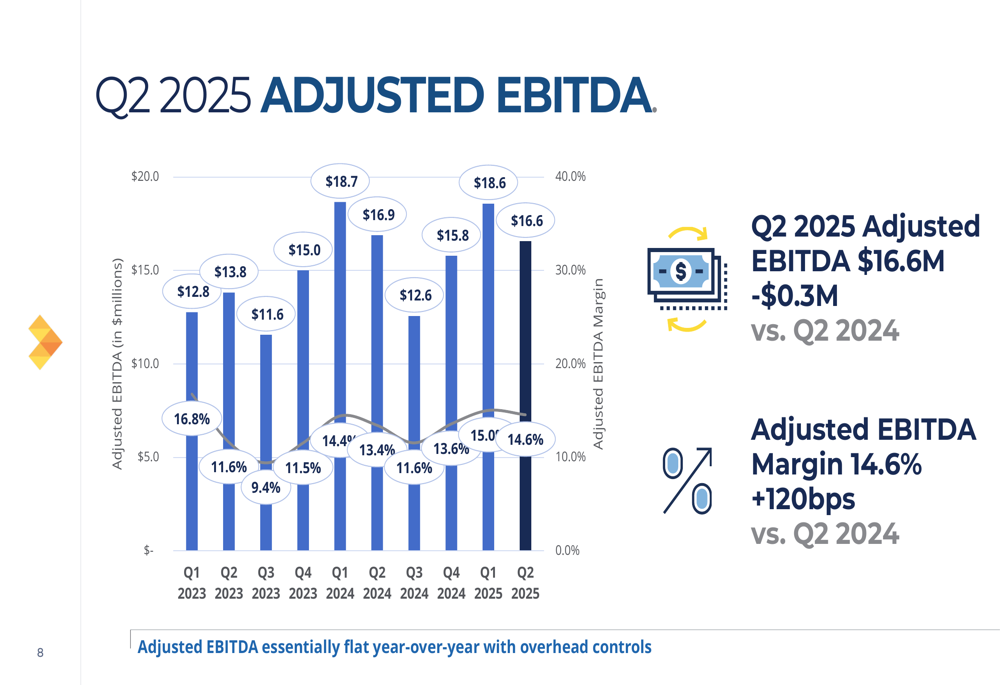

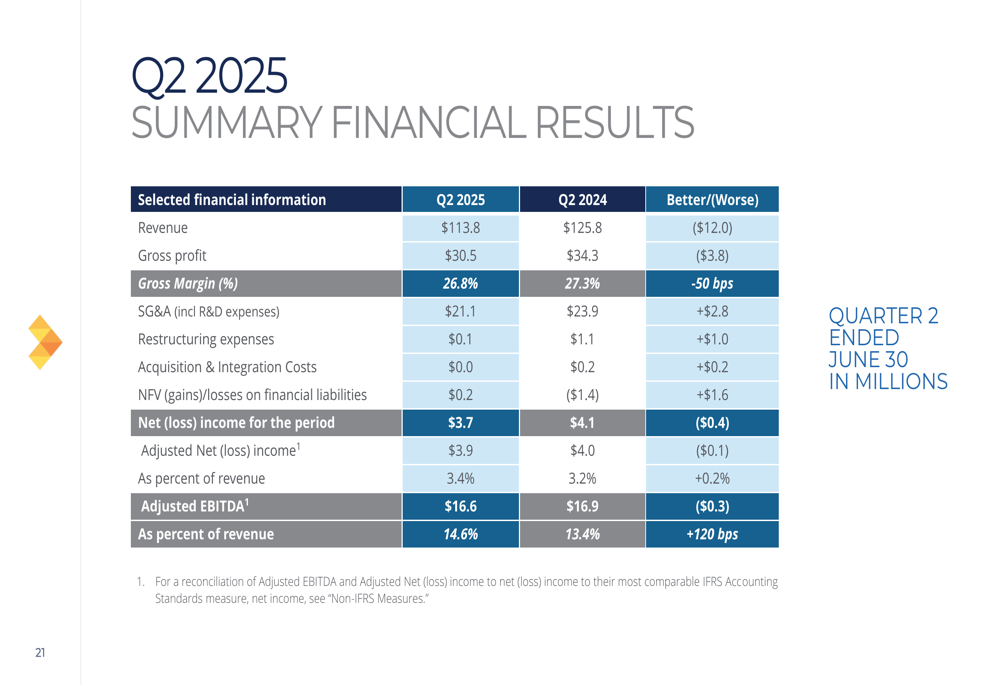

DCM reported Q2 2025 revenue of $113.8 million, representing a 9.5% decrease compared to $125.8 million in Q2 2024. Despite this revenue decline, the company improved its Adjusted EBITDA margin to 14.6%, up from 13.4% in the same period last year, though Adjusted EBITDA decreased slightly to $16.6 million from $16.9 million.

As shown in the following comprehensive overview of Q2 2025 results:

The company attributed the revenue decline to macro headwinds, including economic and tariff uncertainty negatively impacting business confidence, as well as direct and indirect effects from Canada Post labor disruptions. Management emphasized they are controlling overhead costs to mitigate the impact of lower client spending.

The quarterly revenue trend illustrates the challenges DCM has faced over recent quarters:

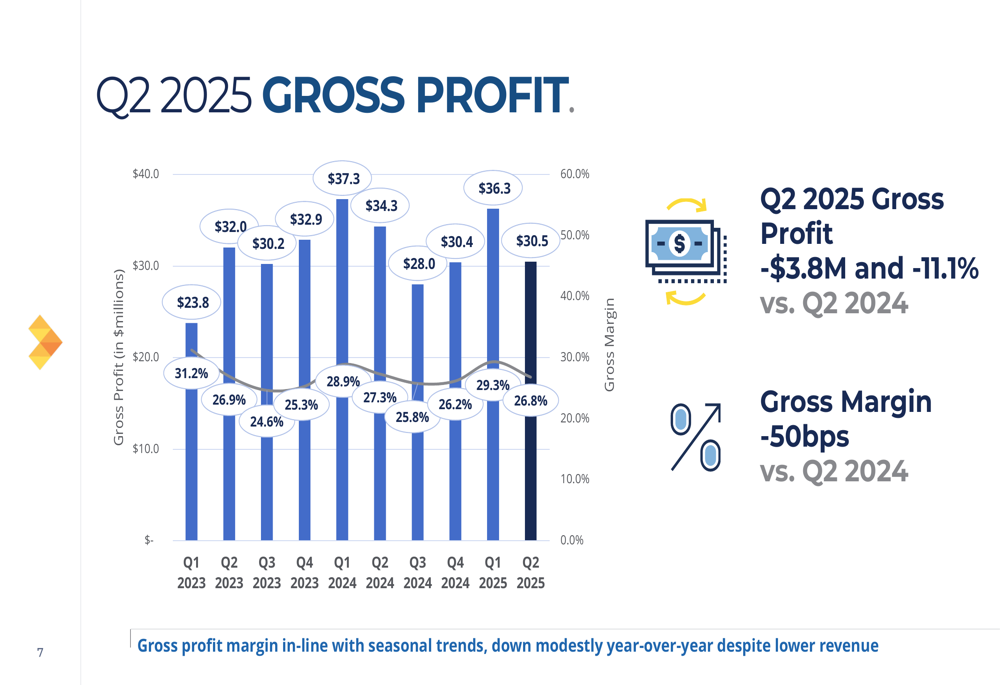

Despite revenue pressures, DCM maintained relatively stable gross margins at 26.8%, compared to 27.3% in Q2 2024. The company’s gross profit was $30.5 million, down from $34.3 million in the prior year period.

As shown in the following chart tracking gross profit and margin trends:

The company’s ability to maintain profitability metrics despite revenue challenges was highlighted in the Adjusted EBITDA performance:

Segment Performance Analysis

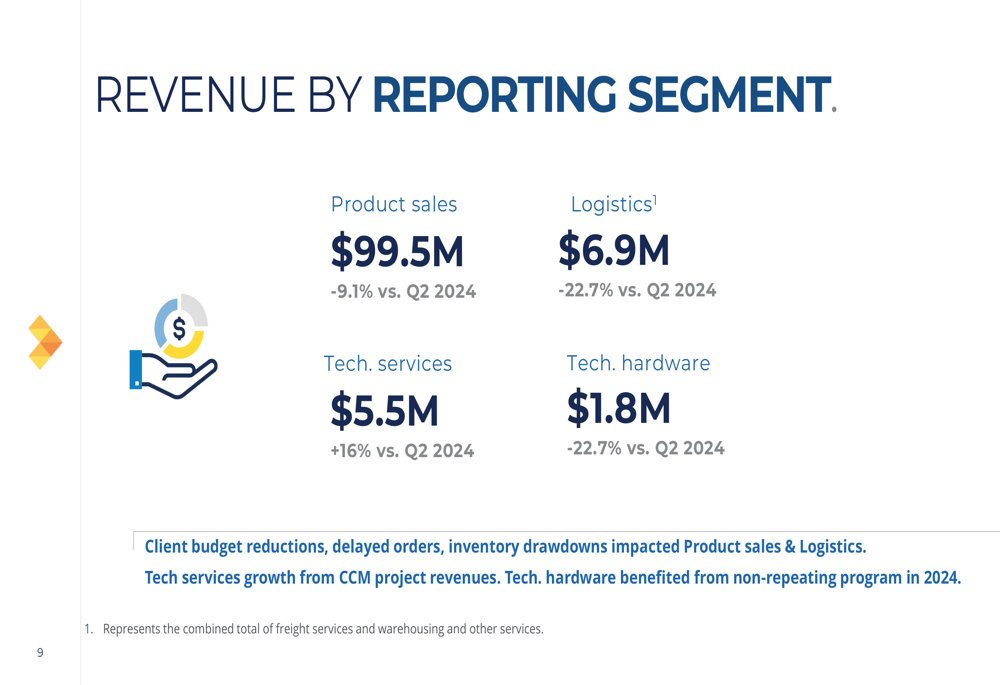

DCM’s performance varied significantly across business segments, with technology services emerging as a bright spot amid broader declines. The company reported Product Sales of $99.5 million (-9.1% year-over-year), Logistics revenue of $6.9 million (-22.7%), Technology Services revenue of $5.5 million (+16%), and Technology Hardware revenue of $1.8 million (-22.7%).

As illustrated in the segment breakdown:

The growth in Technology Services was attributed to CCM (Customer Communications Management) project revenues, highlighting the company’s strategic shift toward higher-margin digital solutions. Meanwhile, traditional product sales and logistics were impacted by client budget reductions, delayed orders, and inventory drawdowns.

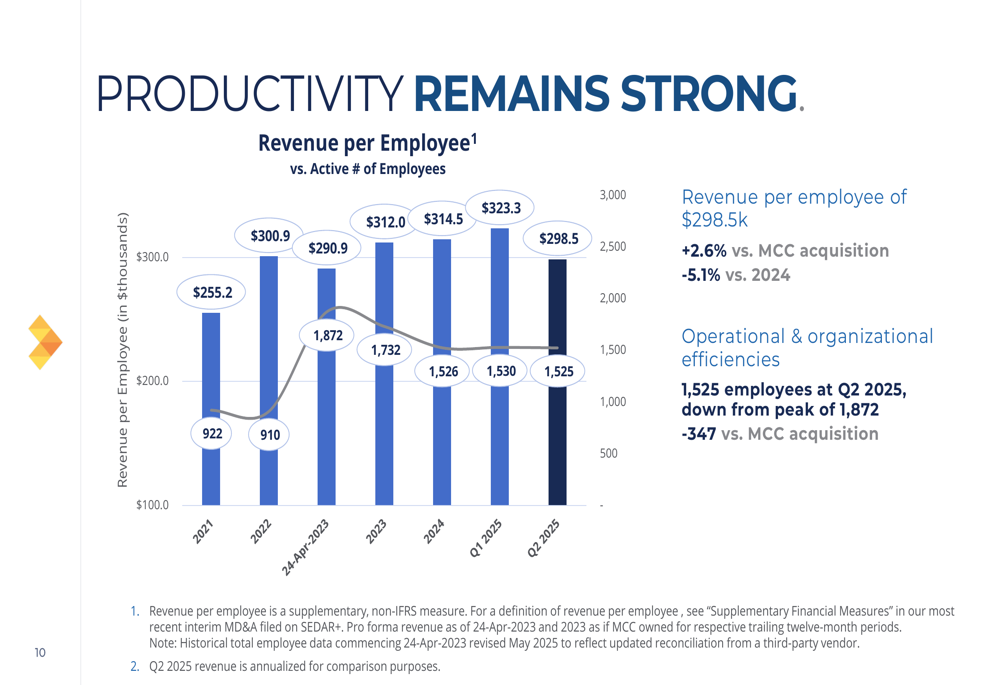

Despite revenue challenges, DCM maintained strong productivity metrics with revenue per employee of $298.5k, representing a 2.6% increase versus the MCC acquisition period, though down 5.1% compared to 2024.

The following chart demonstrates the company’s employee productivity trends:

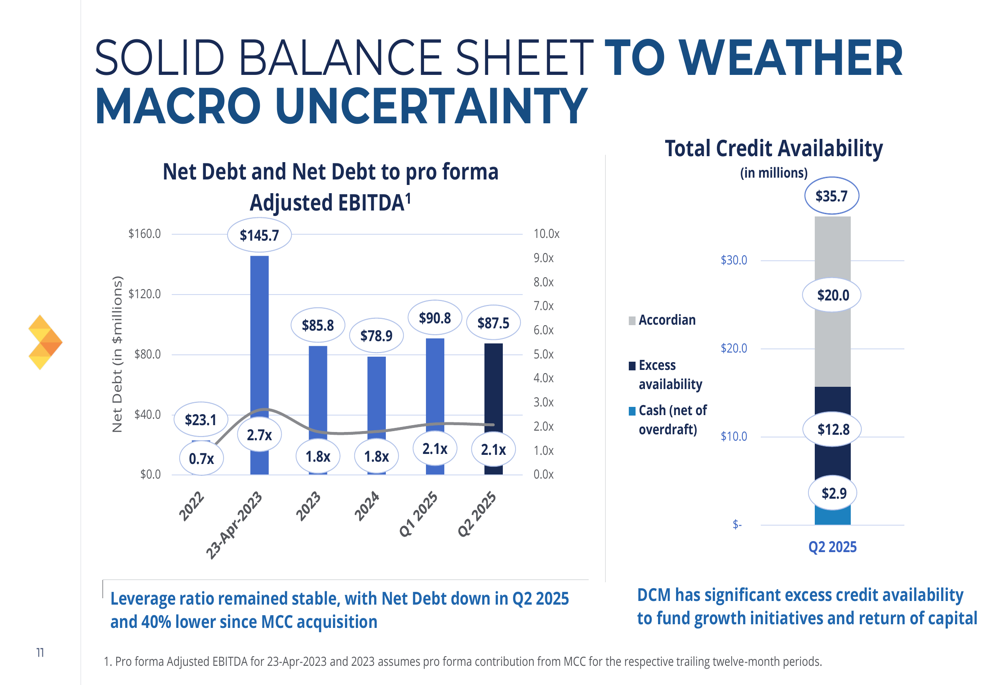

Balance Sheet and Capital Allocation

DCM emphasized its financial stability with a strengthened balance sheet, noting that net debt has decreased by 40% since the MCC acquisition. The company maintains significant excess credit availability to fund growth initiatives and capital returns to shareholders.

The following chart illustrates the company’s debt reduction progress:

In terms of shareholder returns, DCM highlighted its dividend program, which includes a special dividend of $0.20 per share and a quarterly dividend of $0.025 per share, resulting in a dividend yield of 6.5% based on the August 6, 2025 closing price.

This dividend yield appears attractive given current market conditions, though investors should note that DCM’s stock price has been under pressure. According to available data, the stock closed at $1.51 on August 14, 2025, down 0.66% for the day, and significantly below its 52-week high of $3.04.

Strategic Initiatives and Outlook

Looking forward, DCM emphasized its focus on growth initiatives, highlighting what it described as the "deepest new business pipeline we have seen" with 27% of opportunities coming from new logos. The company reported no material client losses and noted accelerating win rates in RFPs compared to 2024.

As shown in the following growth strategy overview:

For 2025, the company outlined four key priorities: maintaining focus on profitable organic growth, delivering returns on new capital investments, driving gross margin improvement through operating efficiencies, and demonstrating agility to navigate an uncertain environment.

The company also highlighted its M&A strategy, noting that industry dynamics are creating more opportunities with increased activity. Management stated they are well-capitalized to pursue these opportunities with $36 million in available capital.

It’s worth noting that while the presentation emphasized "solid operating performance," the company actually missed analyst expectations for both revenue and earnings per share in Q2 2025. According to available data, DCM reported EPS of $0.07, below the forecasted $0.08, while revenue of $113.79 million fell short of the expected $124.34 million.

Despite these misses, CEO Richard Kellam maintained an optimistic tone, stating, "We’ve delivered solid performance amidst some pretty challenging market conditions," while emphasizing the company’s readiness for strategic acquisitions.

The comprehensive financial results for Q2 2025 are summarized in the following table:

With its focus on operational efficiency, strategic growth initiatives in technology services, and a solid balance sheet, DCM is positioning itself to weather current market uncertainties while preparing for future growth opportunities through both organic expansion and potential acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.