Gold prices edge lower; heading for weekly losses ahead of U.S.-Russia talks

Deere & Company (NYSE:DE) revealed significant declines across all major business segments in its third-quarter 2025 earnings presentation on August 14. The agricultural equipment manufacturer reported a 9% drop in net sales and a 26% decline in net income compared to the same period last year, with shares falling sharply in premarket trading.

Quarterly Performance Highlights

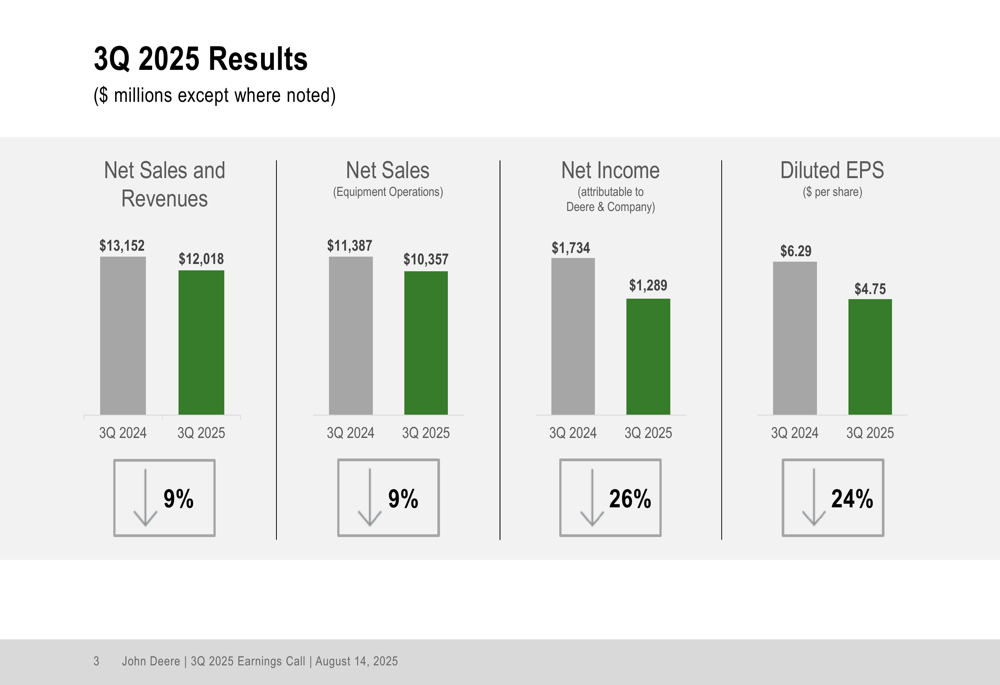

Deere reported net sales and revenues of $12.02 billion for Q3 2025, down 9% from $13.15 billion in Q3 2024. Net income attributable to Deere & Company fell 26% to $1.29 billion, while diluted earnings per share decreased 24% to $4.75 from $6.29 in the prior year.

The results mark a significant reversal from the company’s Q2 2025 performance, when Deere exceeded market expectations with an EPS of $6.64 against a forecast of $5.56.

As shown in the following financial summary chart:

Deere’s equipment operations net sales specifically declined 9% to $10.36 billion. The company’s stock was trading down 7.12% at $477 in premarket activity, reflecting investor disappointment with the results.

Segment Performance Analysis

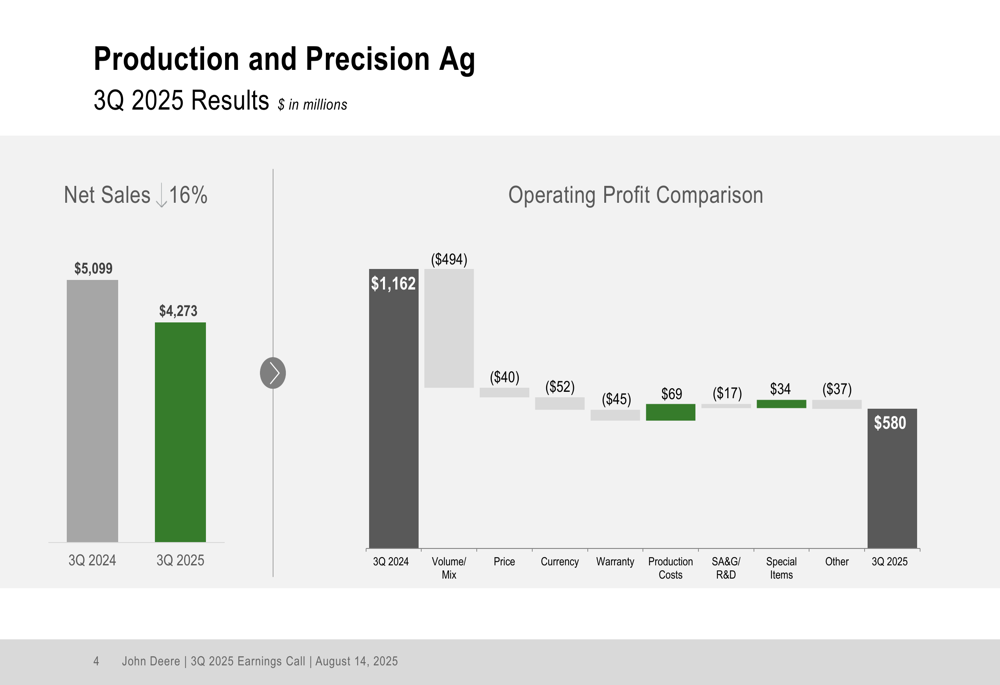

The Production and Precision Agriculture segment, Deere’s largest business unit, experienced the most significant decline with net sales down 16% and operating profit plummeting 50% to $580 million from $1.16 billion in Q3 2024. Volume and mix were the primary negative factors, accounting for a $494 million reduction in operating profit.

As illustrated in this waterfall chart showing the various factors affecting the segment’s performance:

The Small Agriculture and Turf segment showed more resilience with net sales down just 1% and operating profit of $485 million, a slight 2% decrease from $496 million in the prior year. Positive contributions from pricing, currency effects, warranty improvements, and production costs nearly offset negative factors.

The Construction and Forestry segment reported a 5% decline in net sales, while operating profit fell 47% to $237 million from $448 million. Price realization was a significant negative factor, reducing operating profit by $160 million.

The Financial Services segment was the only bright spot, with net income increasing to $205 million from $153 million in Q3 2024, representing a 34% improvement.

Industry Outlook

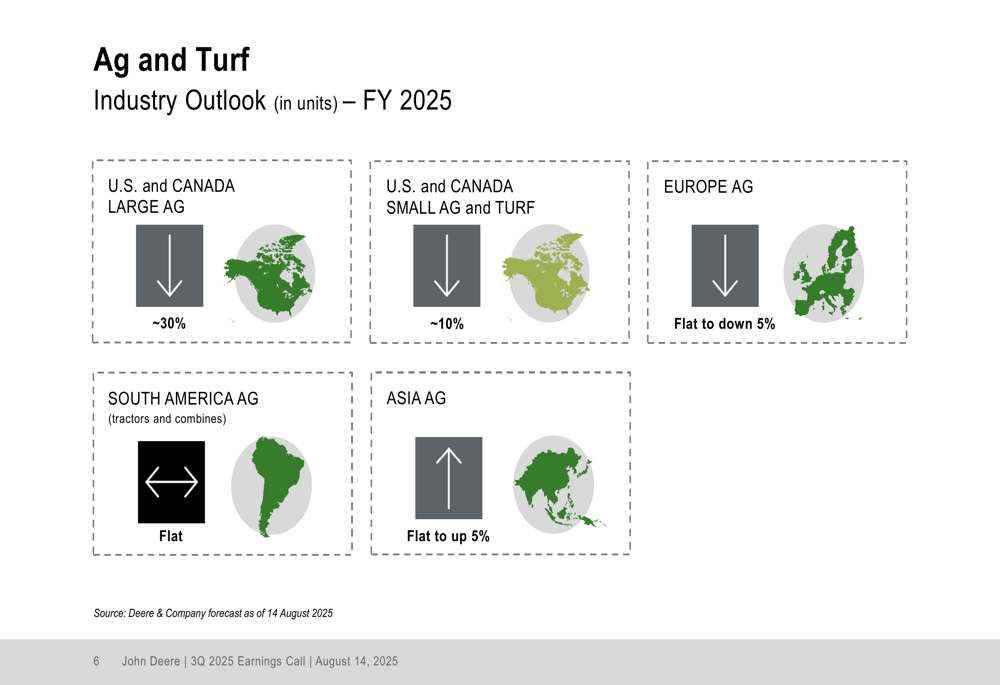

Deere’s presentation painted a challenging picture for agricultural equipment markets, particularly in North America. The company expects U.S. and Canada Large Ag equipment sales to decline approximately 30% for fiscal year 2025, while Small Ag and Turf equipment in the same region is projected to decrease by about 10%.

The following regional outlook highlights these market challenges:

European agricultural equipment markets are expected to be flat to down 5%, while South American markets are forecast to remain flat. Asian agricultural markets show the only positive outlook, with expectations of flat to 5% growth.

In the construction sector, Deere projects U.S. and Canada construction equipment sales to decline approximately 10%, while compact construction equipment is expected to be flat to down 5%. Global forestry equipment is forecast to be flat to down 5%, and global roadbuilding equipment sales are expected to remain flat.

Forward Guidance

Despite the challenging quarter, Deere maintained its full-year 2025 outlook, projecting net income attributable to the company in the range of $4.75 billion to $5.25 billion. The company expects net operating cash flow between $4.5 billion and $5.5 billion, with an effective tax rate of 19-21%.

The company’s full-year guidance is summarized in this outlook slide:

For its individual segments, Deere forecasts:

- Production and Precision Ag: Net sales down 15-20% with operating margins of 15.5-17.0%

- Small Ag and Turf: Net sales down approximately 10% with operating margins of 12.0-13.5%

- Construction and Forestry: Net sales down 10-15% with operating margins of 8.5-10.0%

- Financial Services: Net income of approximately $770 million, up from $696 million in FY 2024

Cash Allocation Strategy

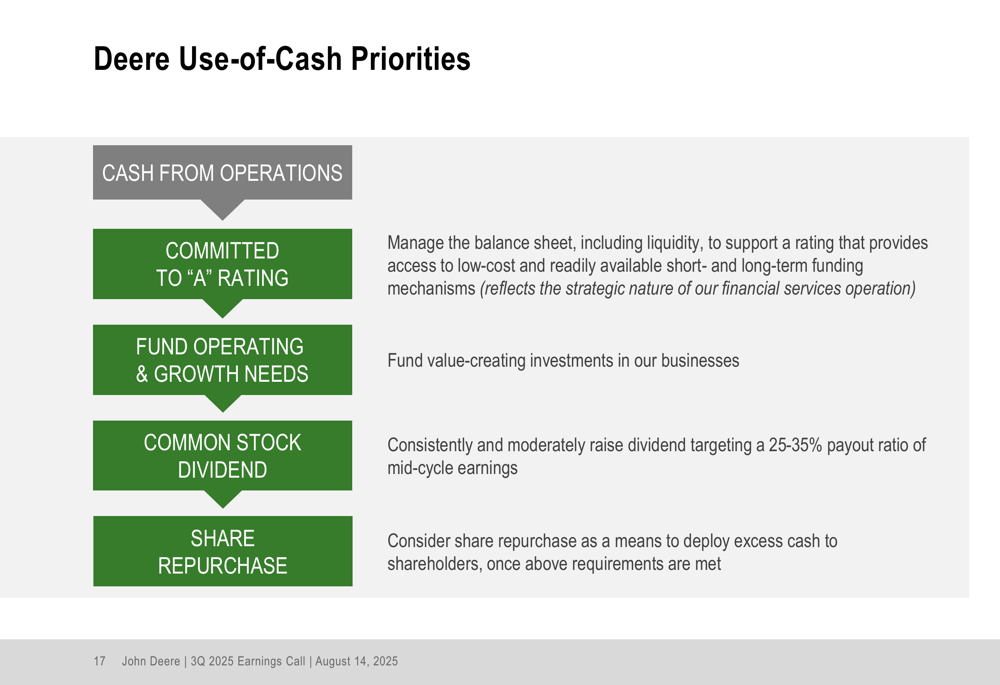

Deere reiterated its capital allocation priorities, emphasizing its commitment to maintaining an "A" credit rating while funding operational and growth needs. The company plans to continue its dividend strategy with a target payout ratio of 25-35% of mid-cycle earnings, and will consider share repurchases as a means to deploy excess cash once other requirements are met.

The company’s use-of-cash priorities are outlined in this slide:

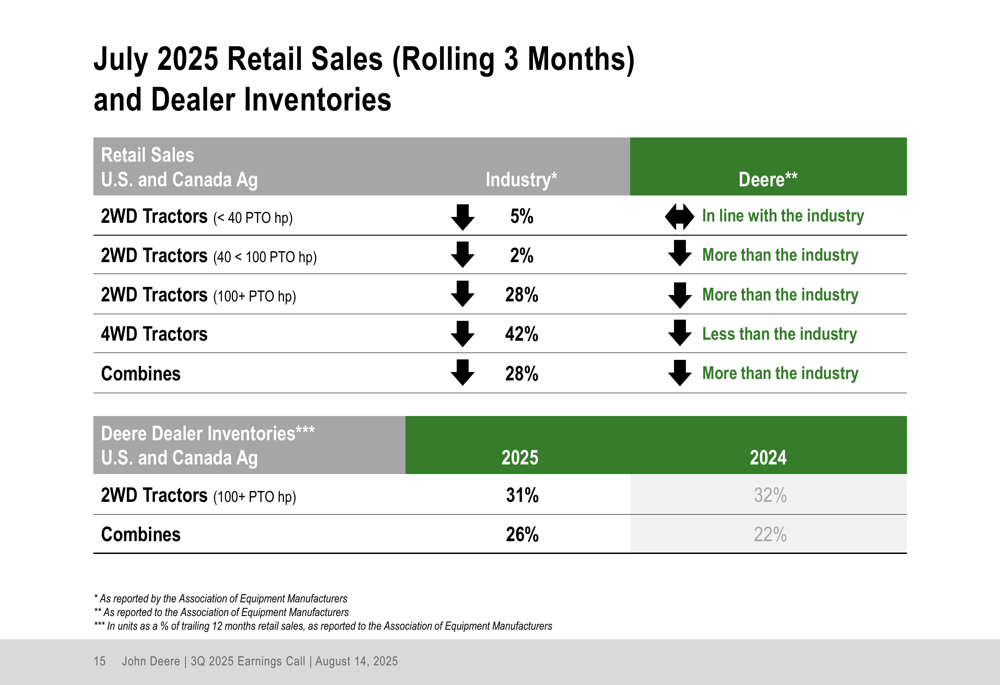

Market Position

Deere provided data on its retail sales and dealer inventories, showing mixed performance across product categories. In the large tractor segment (100+ PTO hp), Deere outperformed the industry, which was down 28%. Similarly, in combines, Deere performed better than the industry average, which was also down 28%.

Dealer inventories for large tractors stood at 31% for 2025, slightly down from 32% in 2024, while combine inventories increased to 26% from 22% in the prior year.

This retail sales and inventory data provides important context for Deere’s market position:

The company’s next earnings call is scheduled for November 26, 2025, when it will report its fourth-quarter and full-year 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.