Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

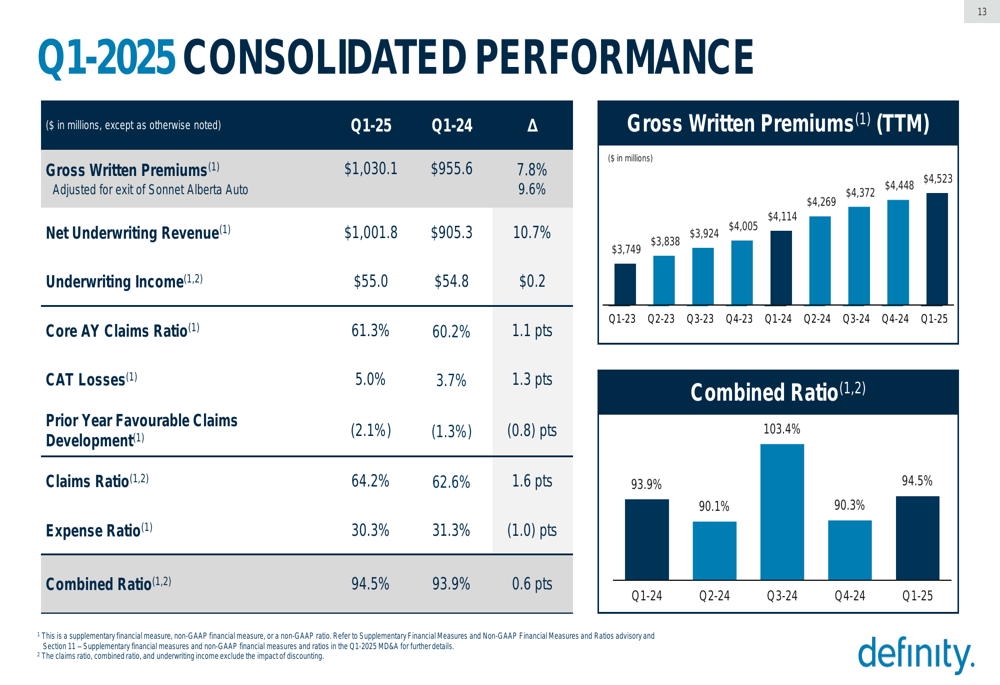

Definity Financial Corporation (TSX:DFY) presented its first quarter 2025 financial results on May 9, showing continued premium growth across all segments while maintaining profitability targets despite increased catastrophe losses. The Canadian property and casualty insurer reported a 9.6% year-over-year increase in gross written premiums, adjusted for exited lines, reaching $1.03 billion.

The company’s stock closed at $69.21 on May 8, down 0.75% for the day but trading near its 52-week high of $70.00, reflecting investor confidence in Definity’s growth trajectory and financial stability.

Quarterly Performance Highlights

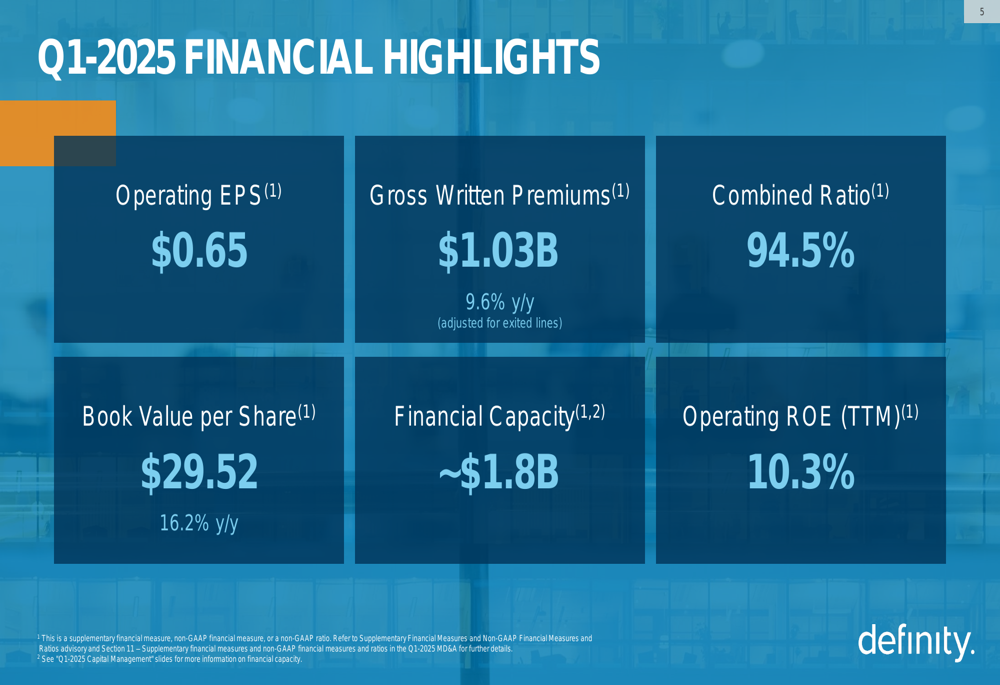

Definity reported operating earnings per share of $0.65 for Q1 2025, unchanged from the same period last year, while maintaining a combined ratio of 94.5%, slightly higher than the 93.9% recorded in Q1 2024. The company’s book value per share grew impressively by 16.2% year-over-year to $29.52.

As shown in the following financial highlights slide, Definity’s operating return on equity improved to 10.3% on a trailing twelve-month basis, up from 9.5% a year earlier:

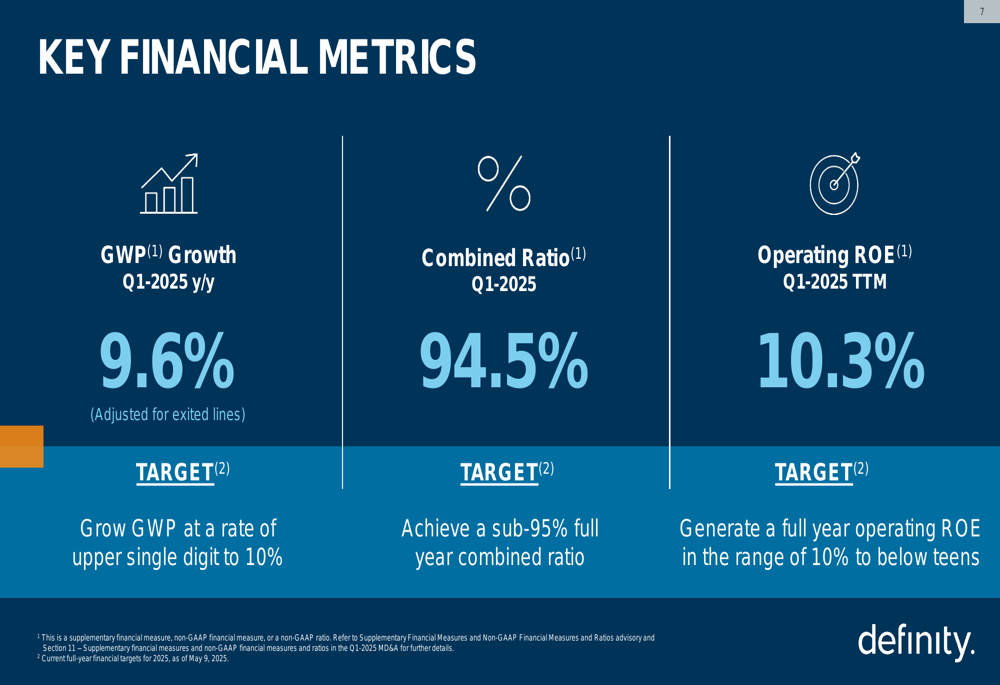

The company’s performance remains aligned with its strategic targets, as illustrated in this comparison of actual results against stated goals:

Segment Analysis

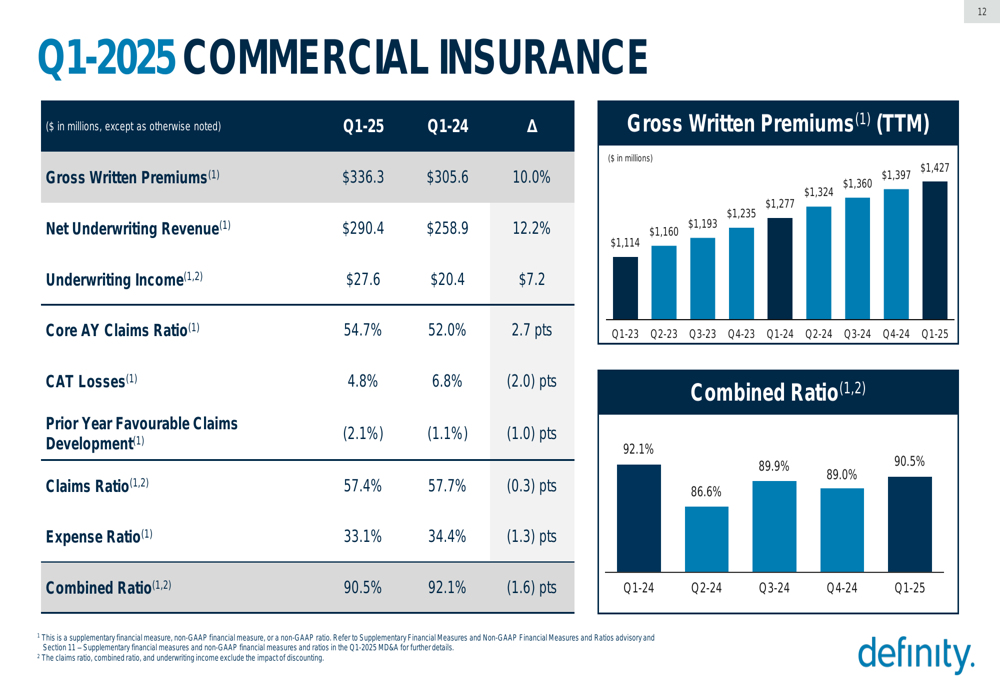

Definity’s Commercial Insurance segment emerged as the standout performer, with a combined ratio of 90.5%, improving from 92.1% in the prior year period. Gross written premiums in this segment increased by 10.0% to $336.3 million, while underwriting income grew by 35.3% to $27.6 million.

The following slide details the Commercial Insurance segment’s strong performance:

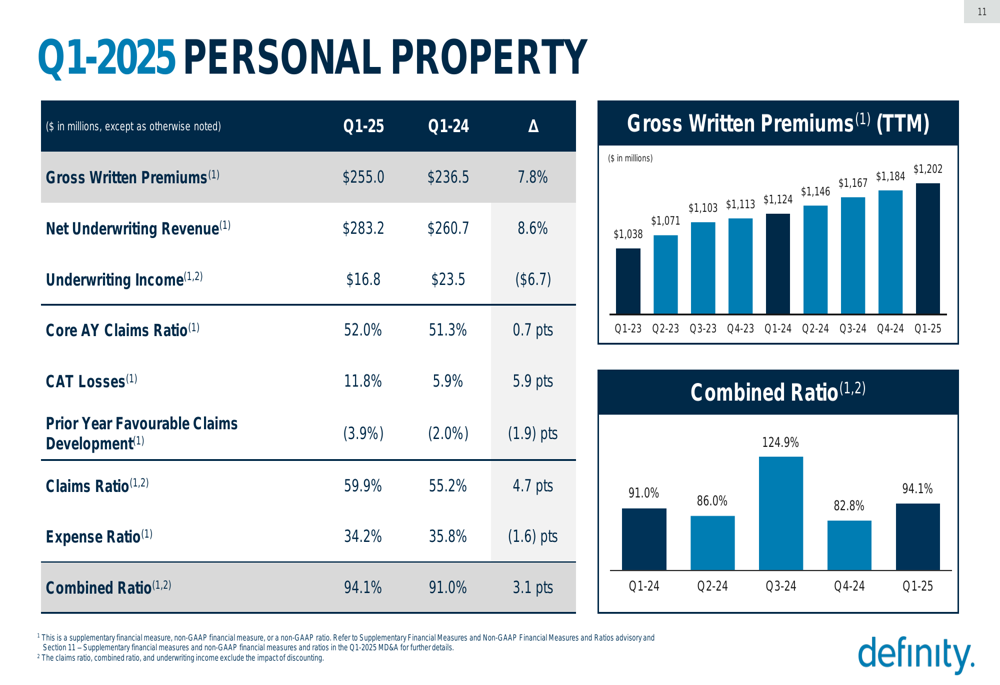

In contrast, the Personal Property segment faced challenges with catastrophe losses, which increased to 11.8% of net earned premiums compared to 5.9% in Q1 2024. This contributed to a deterioration in the segment’s combined ratio from 91.0% to 94.1%, despite premium growth of 7.8% to $255.0 million.

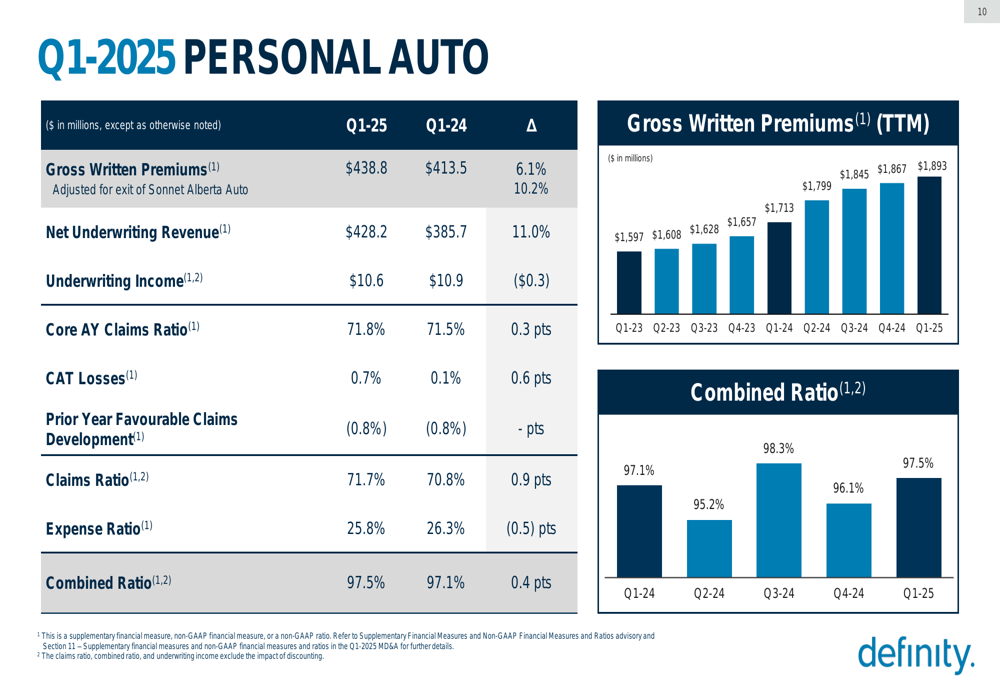

The Personal Auto segment maintained relatively stable performance with a combined ratio of 97.5%, slightly higher than the 97.1% reported in Q1 2024. Gross written premiums increased by 6.1% to $438.8 million.

On a consolidated basis, Definity’s underwriting income remained stable at $55.0 million despite higher catastrophe losses, which increased to 5.0% of net earned premiums from 3.7% in the prior year period.

Strategic Initiatives

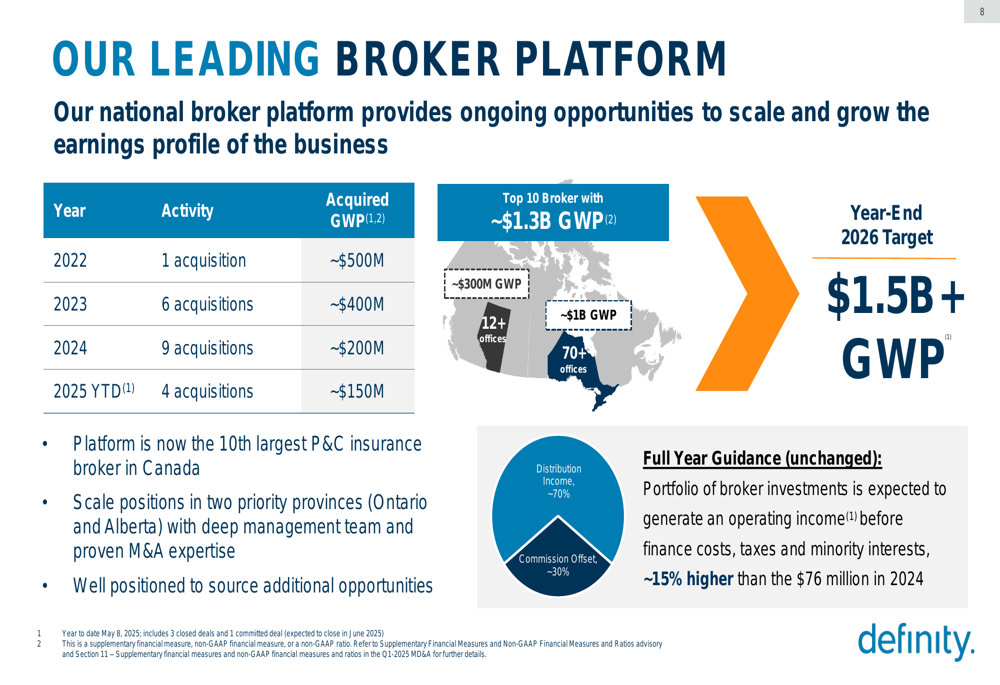

Definity continues to expand its broker platform, which has now become the 10th largest property and casualty insurance broker in Canada. The company has completed four acquisitions year-to-date in 2025, representing approximately $150 million in acquired gross written premiums.

The broker platform strategy is illustrated in the following slide:

President and CEO Rowan Saunders highlighted the company’s outlook for the Canadian insurance market, noting firm conditions in personal auto due to inflationary cost pressures and regulatory constraints, particularly in Alberta. The personal property segment also faces firm market conditions due to significant industry catastrophe losses and elevated inflation.

Capital Management & Outlook

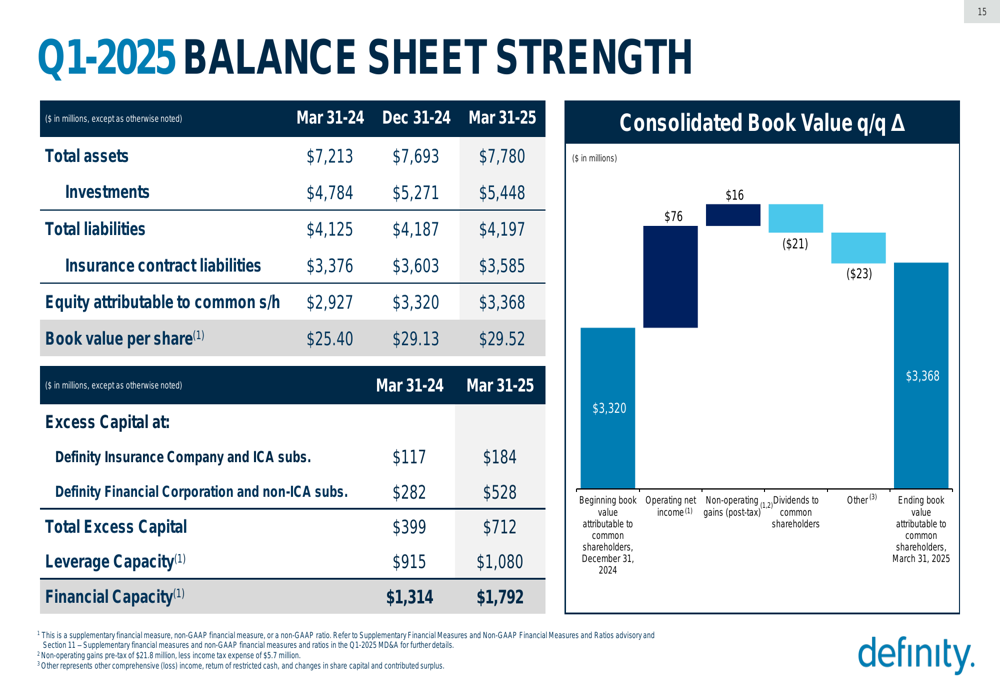

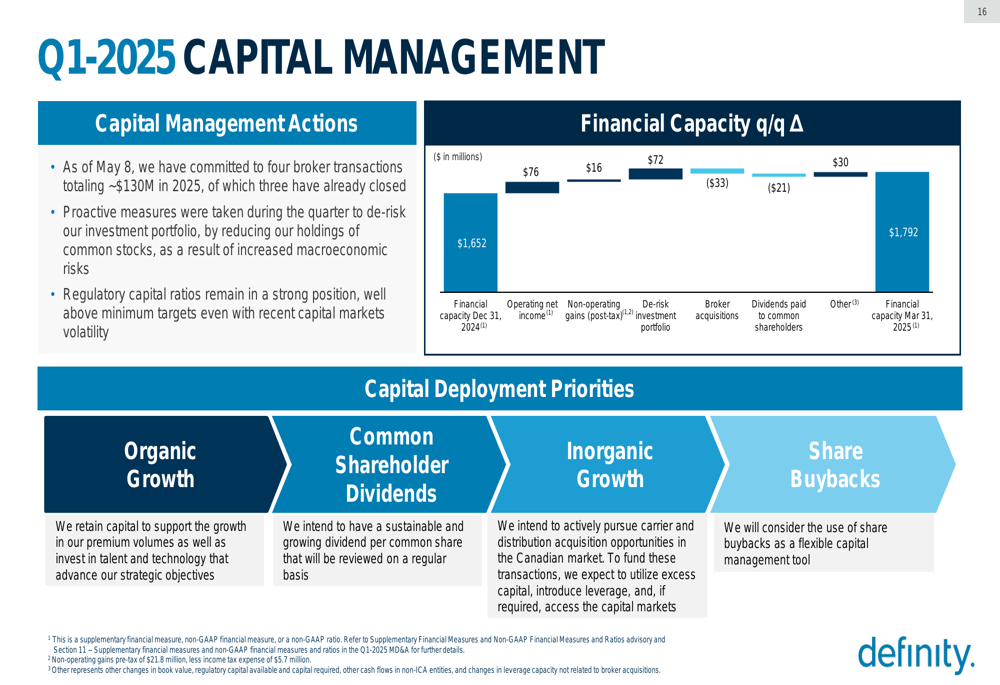

Definity maintains a strong balance sheet with total excess capital of $712 million as of March 31, 2025, up significantly from $399 million a year earlier. The company’s financial capacity increased to $1.79 billion from $1.31 billion in the prior year period.

The following slide illustrates Definity’s balance sheet strength:

Executive Vice-President and CFO Philip Mather outlined the company’s capital management priorities, including commitments to four broker transactions totaling approximately $130 million in 2025. The company is taking proactive measures to de-risk its investment portfolio while maintaining strong regulatory capital ratios.

Looking ahead, Definity reaffirmed its full-year targets, including growing gross written premiums at a rate of upper single digit to 10%, achieving a sub-95% combined ratio, and generating a full-year operating return on equity in the range of 10% to below teens.

The company’s broker platform is expected to generate operating income before finance costs, taxes, and minority interests approximately 15% higher than the $76 million recorded in 2024, with a year-end 2026 target of exceeding $1.5 billion in gross written premiums.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.