Elastic launches GPU-accelerated inference service for AI workflows

Introduction & Market Context

Dell Technologies Inc (NYSE:DELL) reported its first quarter fiscal 2026 results on May 29, 2025, showcasing strong performance driven by accelerating artificial intelligence (AI) server demand and solid commercial PC growth. The company’s stock responded positively, rising 5.39% in after-hours trading to $119.76, following a slight 0.15% decline during regular trading hours.

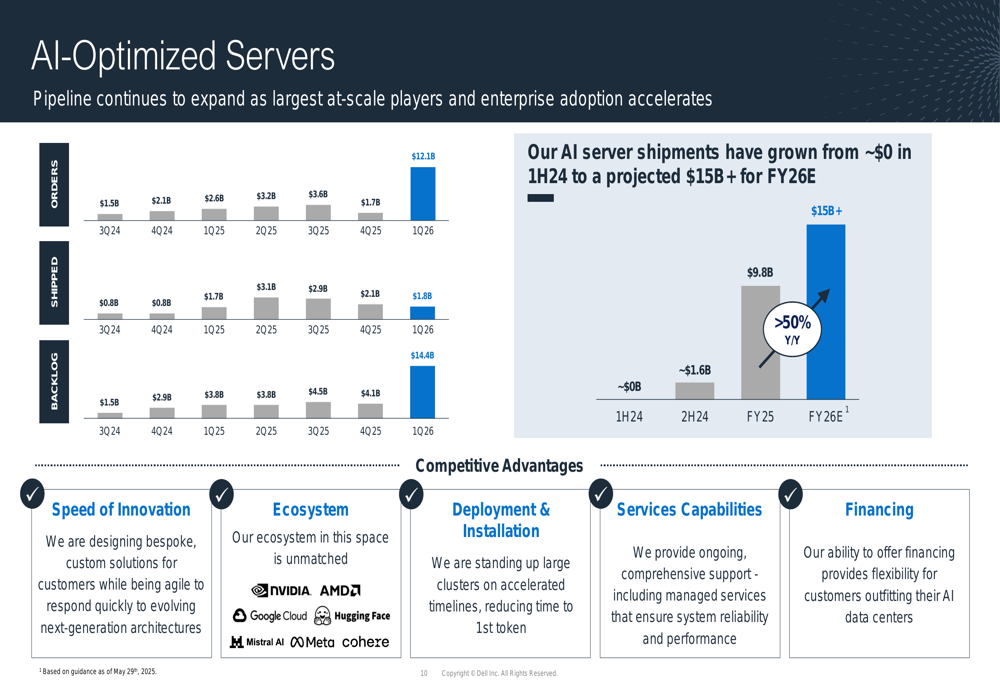

The quarter demonstrated Dell’s strategic positioning in the rapidly expanding AI infrastructure market, with AI-optimized server orders reaching $12.1 billion in Q1 alone—surpassing the company’s entire shipment volume for fiscal 2025. This performance comes amid growing enterprise adoption of AI technologies and Dell’s expanding footprint in both commercial and high-performance computing segments.

Quarterly Performance Highlights

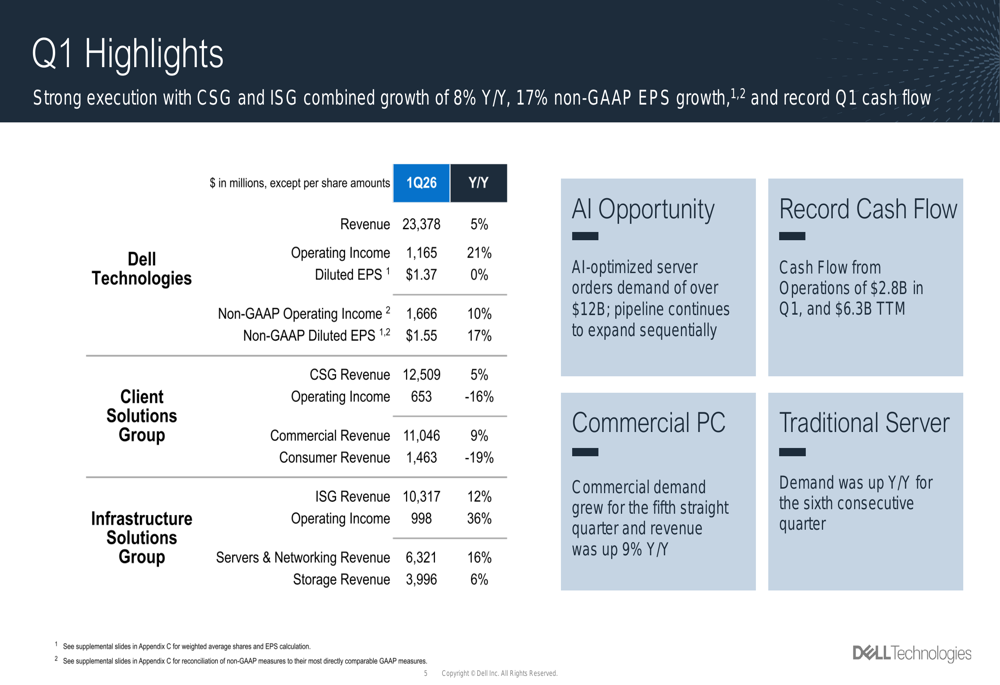

Dell reported Q1 FY26 revenue of $23.4 billion, representing a 5% year-over-year increase, with growth across its core markets. Non-GAAP diluted earnings per share reached $1.55, up 17% year-over-year, growing more than three times faster than revenue. GAAP diluted EPS remained flat at $1.37 compared to the same period last year.

As shown in the following detailed breakdown of Dell’s Q1 performance metrics:

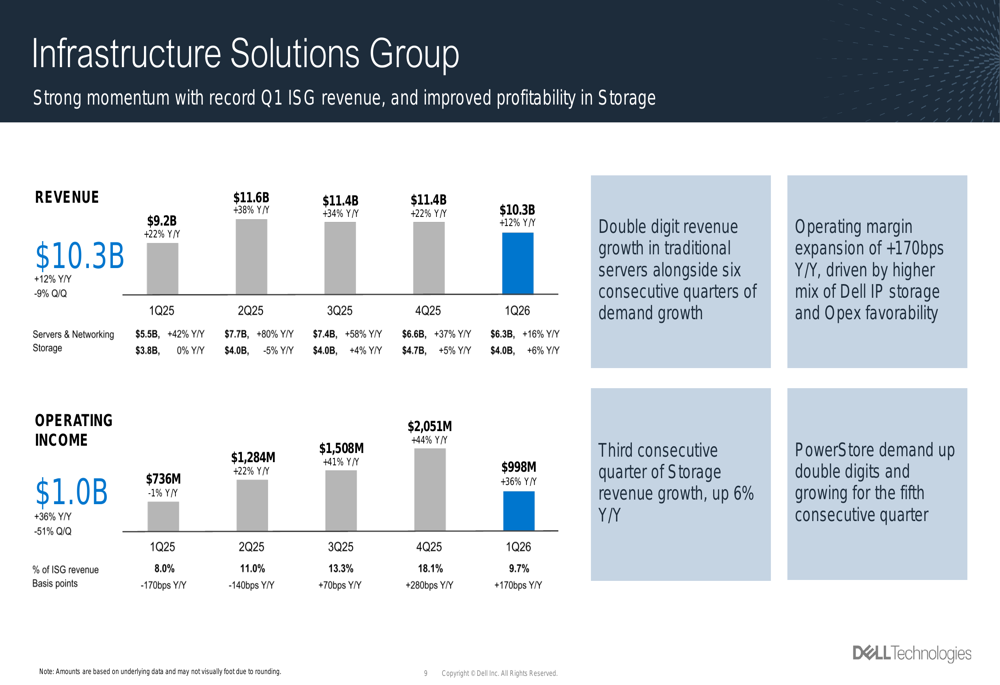

The Infrastructure Solutions Group (ISG) delivered particularly strong results with revenue of $10.3 billion, up 12% year-over-year, driven by 16% growth in servers and networking revenue ($6.3 billion) and 6% growth in storage revenue ($4.0 billion). ISG operating income increased 36% year-over-year to $998 million, representing 9.7% of ISG revenue—a 170 basis point improvement.

The Client Solutions Group (CSG) also performed well, with revenue of $12.5 billion, up 5% year-over-year. Commercial revenue grew 9% to $11.0 billion, marking the fifth consecutive quarter of year-over-year growth, while consumer revenue declined 19% to $1.5 billion.

AI Server Growth & Infrastructure Solutions Group

Dell’s Infrastructure Solutions Group demonstrated exceptional momentum, particularly in AI-optimized servers. The company reported record Q1 ISG revenue with improved profitability in storage, as shown in the following performance metrics:

The surge in AI server demand has created a substantial backlog for Dell. As illustrated in the following chart, AI-optimized server orders have grown dramatically over the past five quarters, from $1.5 billion in Q3 FY24 to $12.1 billion in Q1 FY26, while shipments have increased from $0.8 billion to $3.1 billion over the same period. This has resulted in a backlog of $14.4 billion exiting Q1 FY26.

Dell attributes its competitive advantage in AI servers to several factors, including speed of innovation, ecosystem partnerships, deployment and installation capabilities, services capabilities, and financing options. The company has also expanded its portfolio of integrated rack scalable systems for large-scale AI deployment, offering customers flexibility in rack style, thermal management, processor choice, and AI fabric.

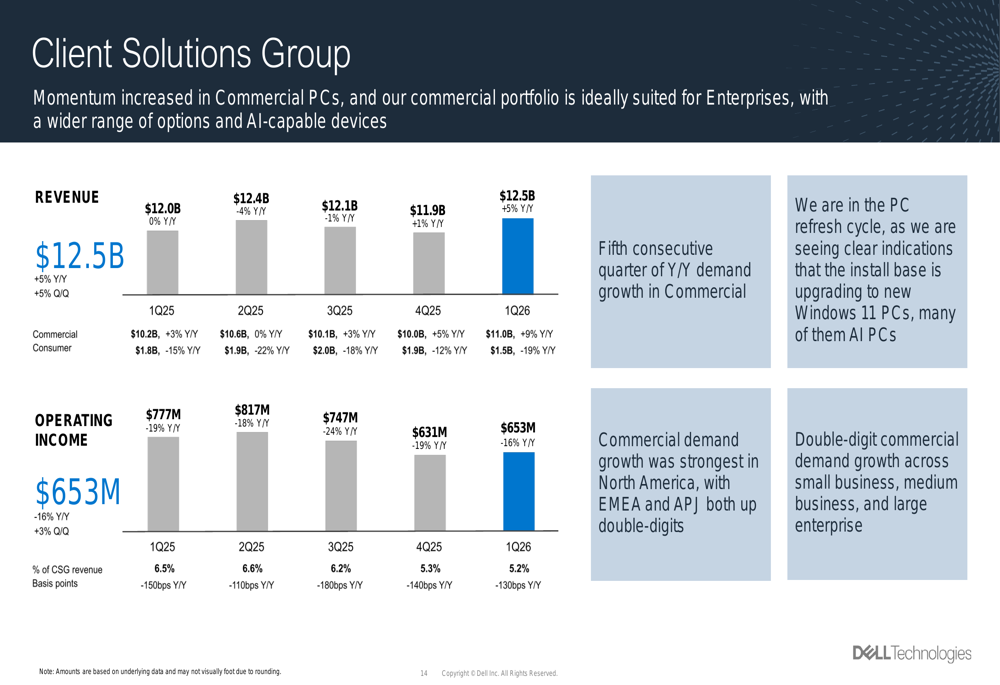

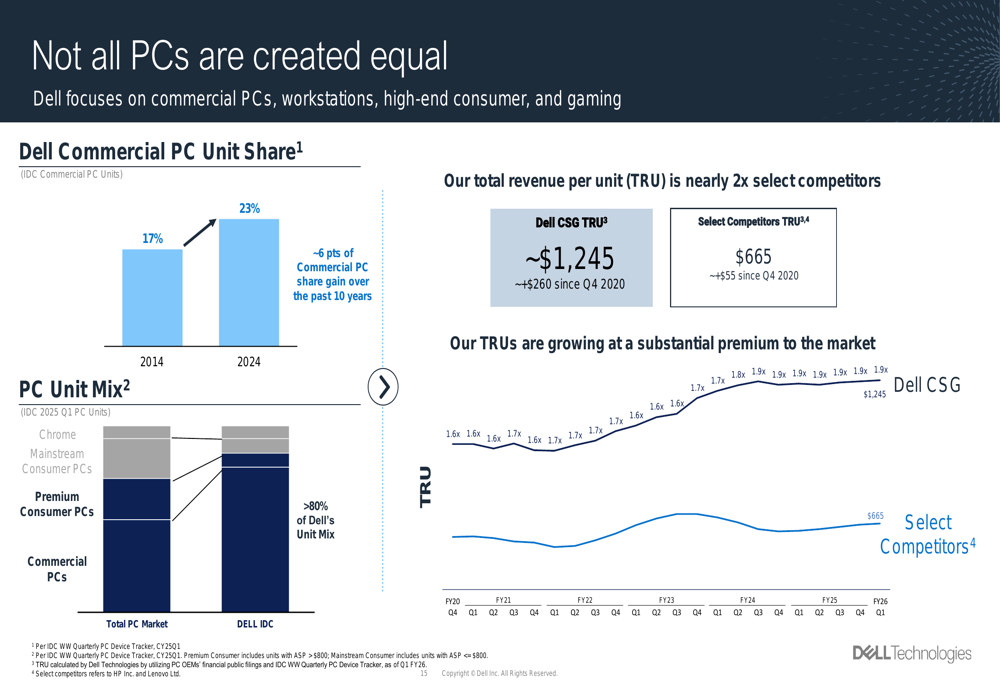

Client Solutions Group Performance

Dell’s Client Solutions Group maintained positive momentum, particularly in the commercial segment. The following chart illustrates CSG’s performance over the past five quarters:

Commercial PC demand grew for the fifth consecutive quarter, with particularly strong performance in North America and double-digit growth across small business, medium business, and large enterprise segments. While consumer revenue declined 19% year-over-year, Dell’s strategic focus on higher-value commercial PCs, workstations, and premium consumer devices has yielded benefits.

The company highlighted that its total revenue per unit (TRU) is nearly twice that of select competitors at approximately $1,245 versus $665. Dell also noted its #1 position in commercial AI PCs for the last 12 months and its simplified product lineup with Dell, Dell Pro, and Dell Pro Max offerings.

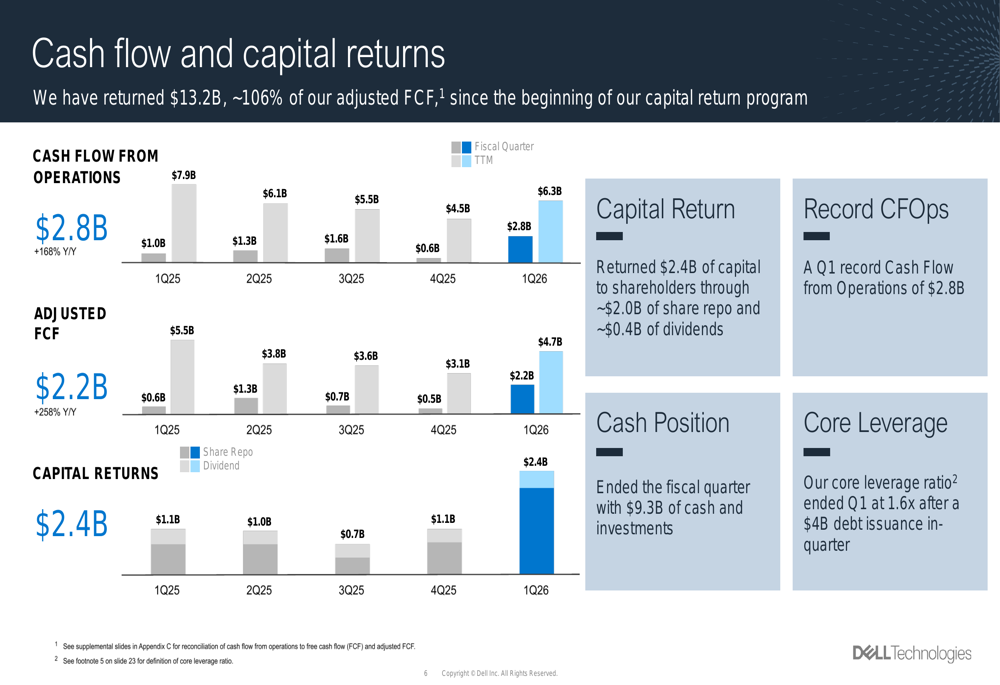

Cash Flow and Capital Allocation

Dell generated record Q1 cash flow from operations of $2.8 billion, up 168% year-over-year. The company returned $2.4 billion to shareholders during the quarter, including $2.0 billion in share repurchases and $396 million in dividends. Since the beginning of its capital return program, Dell has returned $13.2 billion to shareholders, representing approximately 106% of adjusted free cash flow.

The following chart illustrates Dell’s strong cash flow performance over the past five quarters:

The company ended Q1 with $9.3 billion in cash and investments. Its core leverage ratio stood at 1.6x after a $4 billion debt issuance during the quarter.

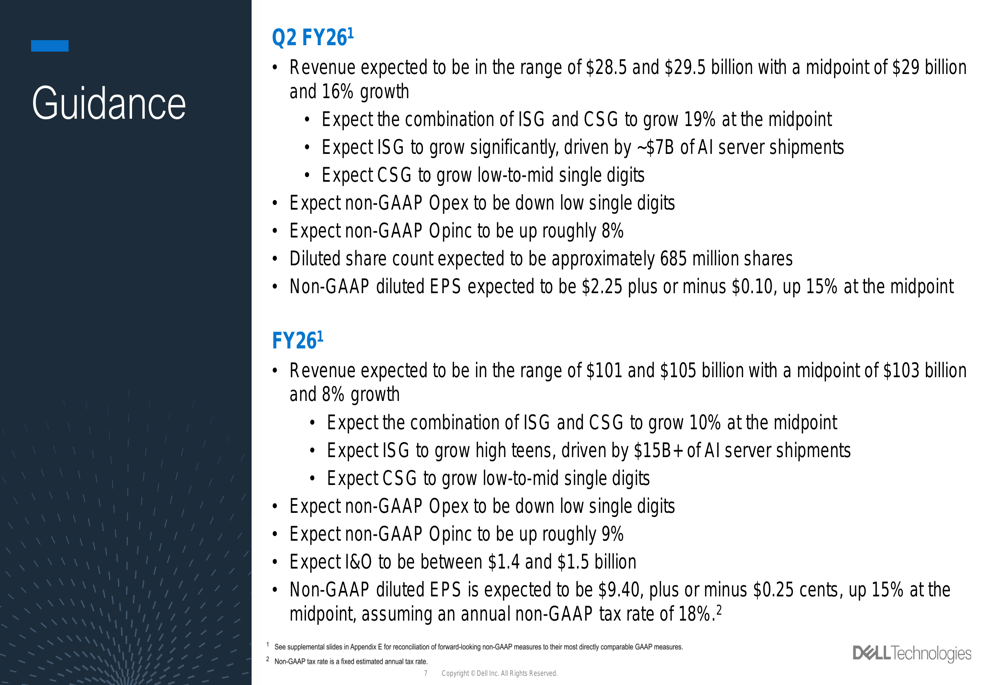

Forward Guidance and Outlook

Dell provided an optimistic outlook for both Q2 FY26 and the full fiscal year. For Q2, the company expects revenue between $28.5 billion and $29.5 billion (midpoint $29 billion), representing 16% growth year-over-year. This growth will be driven by approximately $7 billion in AI server shipments. Non-GAAP diluted EPS is expected to be $2.25 (±$0.10), up 15% at the midpoint.

For the full fiscal year 2026, Dell projects revenue between $101 billion and $105 billion (midpoint $103 billion), representing 8% growth. The company expects to ship more than $15 billion in AI servers during the year. Non-GAAP diluted EPS is forecast at $9.40 (±$0.25), up 15% at the midpoint.

The following guidance slide details these projections:

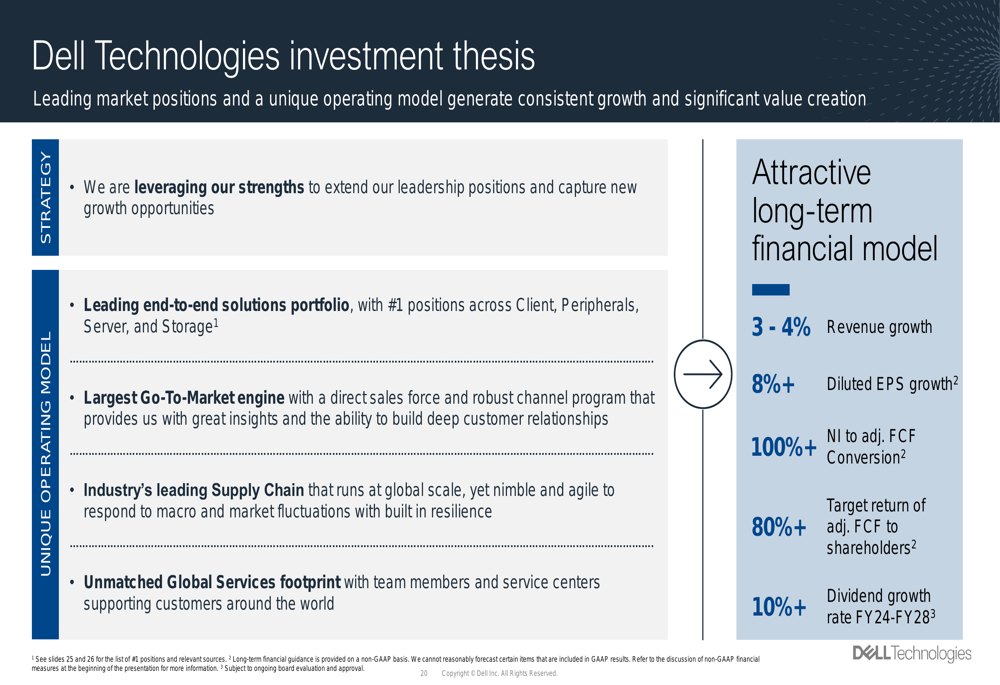

Dell’s long-term investment thesis remains focused on leveraging its strengths to extend leadership positions and capture new growth opportunities. The company targets 3-4% revenue growth, 8%+ diluted EPS growth, and 100%+ net income to adjusted free cash flow conversion, with a commitment to returning 80%+ of adjusted free cash flow to shareholders.

As AI adoption continues to accelerate, Dell expects the total addressable market for AI hardware and services to reach $295 billion by 2027, positioning the company for sustained growth in this rapidly expanding segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.