Gold futures surpass $4,000 for the first time amid global political uncertainty

Introduction & Market Context

De’Longhi SpA (BIT:DLG) presented its H1 and Q2 2025 financial results on July 31, 2025, showcasing continued strong performance across its business segments. The Italian household appliance manufacturer reported an 11.3% increase in revenue for the first half of 2025, building on its positive momentum from 2024. Despite the solid results, De’Longhi’s stock was down 2.89% to €27.58 during the trading session following the presentation.

The company’s performance comes amid a dynamic consumer environment and follows a strong 2024, when De’Longhi reported a 14% increase in total revenue. The latest results demonstrate the company’s ability to maintain growth momentum while navigating challenges such as U.S. tariffs and working capital absorption.

Quarterly Performance Highlights

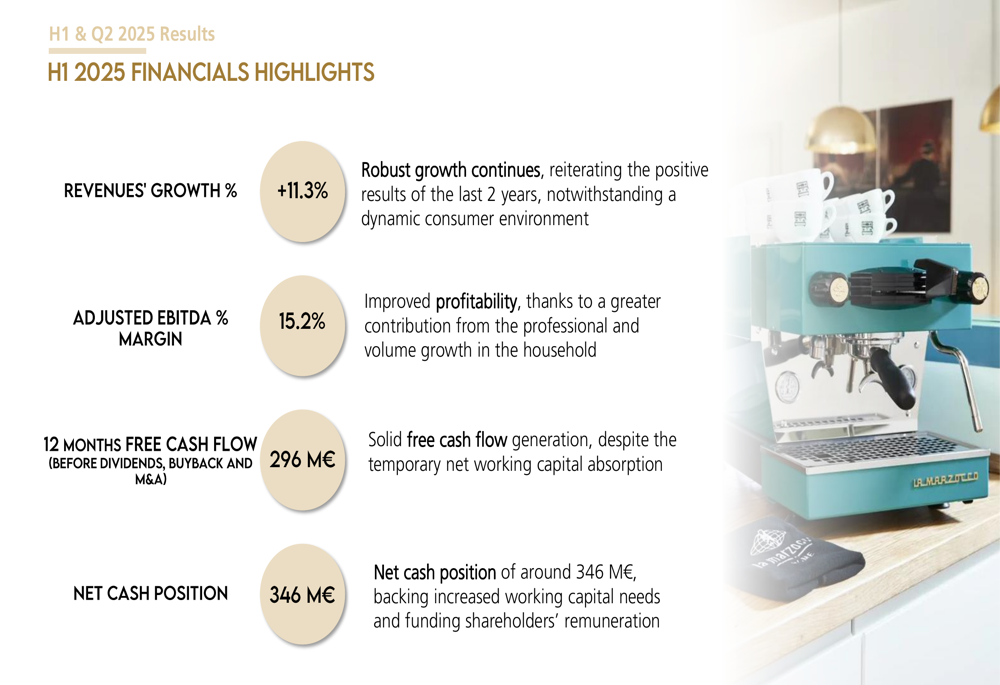

De’Longhi reported H1 2025 revenues of €1,584.2 million, representing an 11.3% increase compared to the same period last year. For Q2 specifically, revenues reached €829.0 million, up 8.4% year-over-year. The company’s profitability also improved, with adjusted EBITDA margin expanding to 15.2% in H1 2025 from 14.4% in H1 2024.

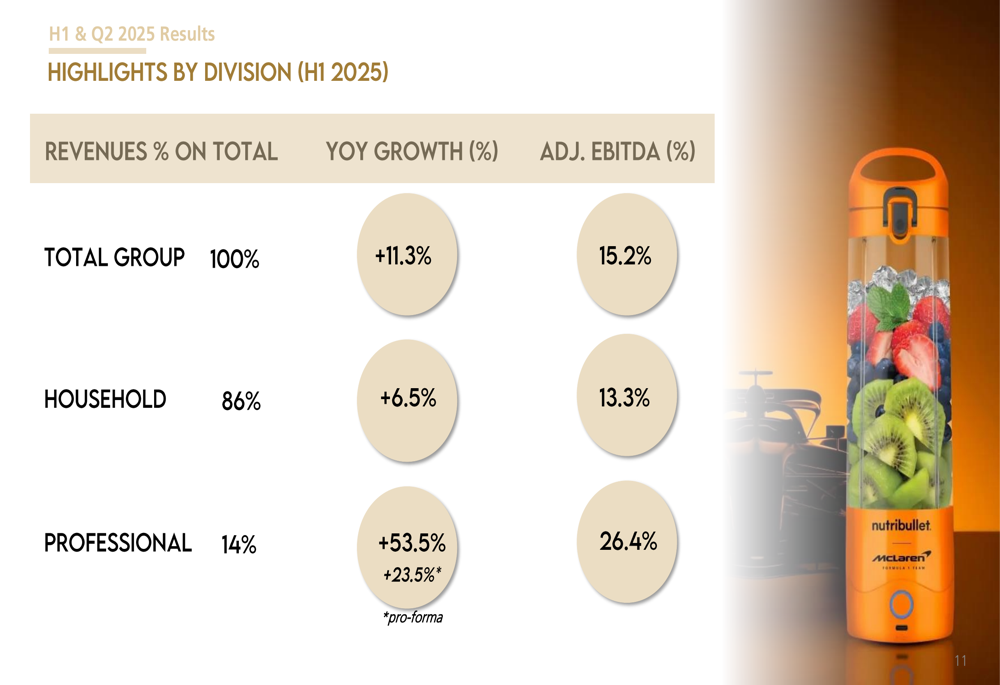

The company’s performance was particularly strong in its Professional division, which includes La Marzocco and Eversys brands. This segment grew by an impressive 53.5% year-over-year (23.5% on a pro-forma basis), accounting for 14% of total revenues with a robust 26.4% adjusted EBITDA margin. The Household division, representing 86% of revenues, grew by 6.5% with a 13.3% adjusted EBITDA margin.

As shown in the following breakdown of performance by division:

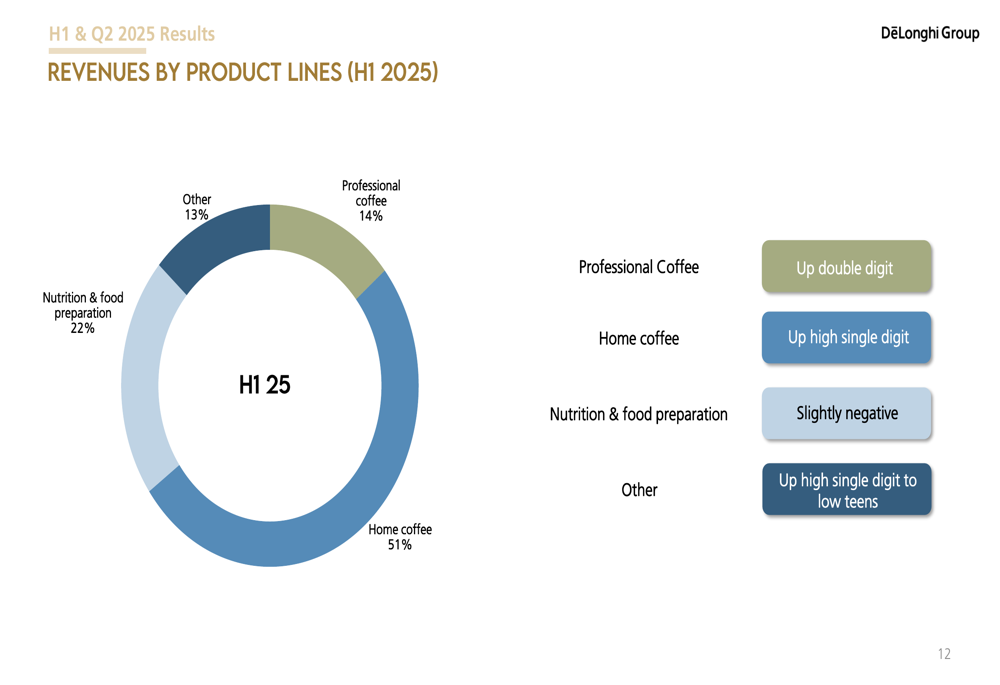

The company’s product portfolio continues to be dominated by coffee-related products, which account for 65% of total revenues (51% home coffee and 14% professional coffee). Both segments showed strong growth, with professional coffee up by double digits and home coffee increasing by high single digits.

The following chart illustrates the revenue distribution by product line:

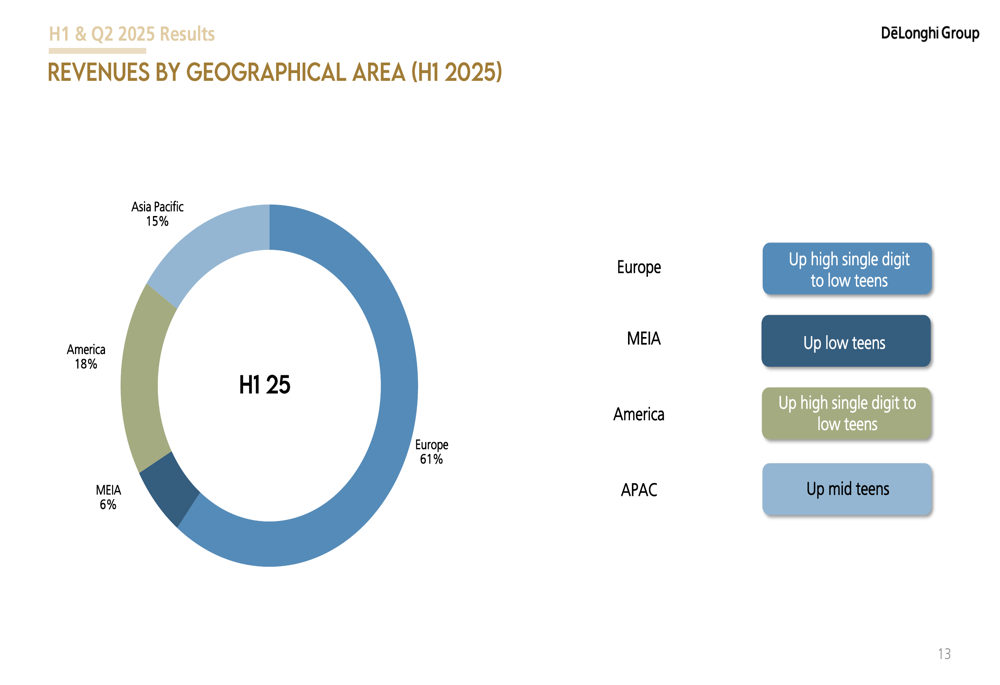

From a geographical perspective, Europe remains De’Longhi’s largest market, accounting for 61% of revenues and showing growth in the high single digit to low teens range. The Asia Pacific region demonstrated the strongest growth at mid-teens, representing 15% of total revenues. The Americas (18% of revenues) and MEIA (6%) both grew in the high single digit to low teens range.

The geographic revenue distribution is illustrated in this breakdown:

Detailed Financial Analysis

De’Longhi’s P&L statement shows solid performance across key metrics. Net income for H1 2025 reached €116.6 million, representing a 9.8% increase compared to H1 2024. For Q2 2025, net income was €59.3 million, up 8.1% year-over-year. The company maintained a healthy net income margin of 7.4% for the half-year period.

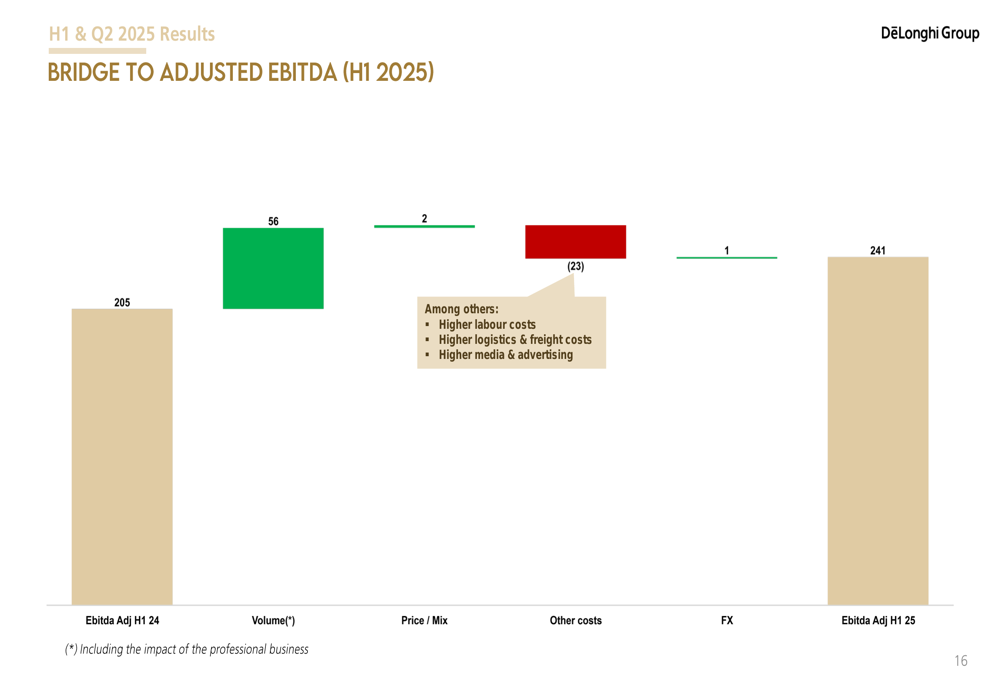

The company’s adjusted EBITDA for H1 2025 increased by 17.6% to €240.7 million, driven primarily by volume growth (+€56 million contribution) which offset increases in other costs (-€23 million impact). For Q2 specifically, adjusted EBITDA grew by 12.2% to €124.4 million.

The following bridge analysis illustrates the factors contributing to the H1 2025 EBITDA growth:

De’Longhi maintained a strong balance sheet with a net cash position of €345.8 million as of June 30, 2025, compared to €305.3 million a year earlier. However, this represents a decrease from €643.2 million at the end of December 2024, primarily due to working capital absorption and shareholder remuneration.

The company’s net working capital increased to 1.6% of revenues as of June 2025, compared to 0.0% in June 2024 and -2.8% in December 2024. This temporary absorption of working capital was highlighted in the company’s financial summary:

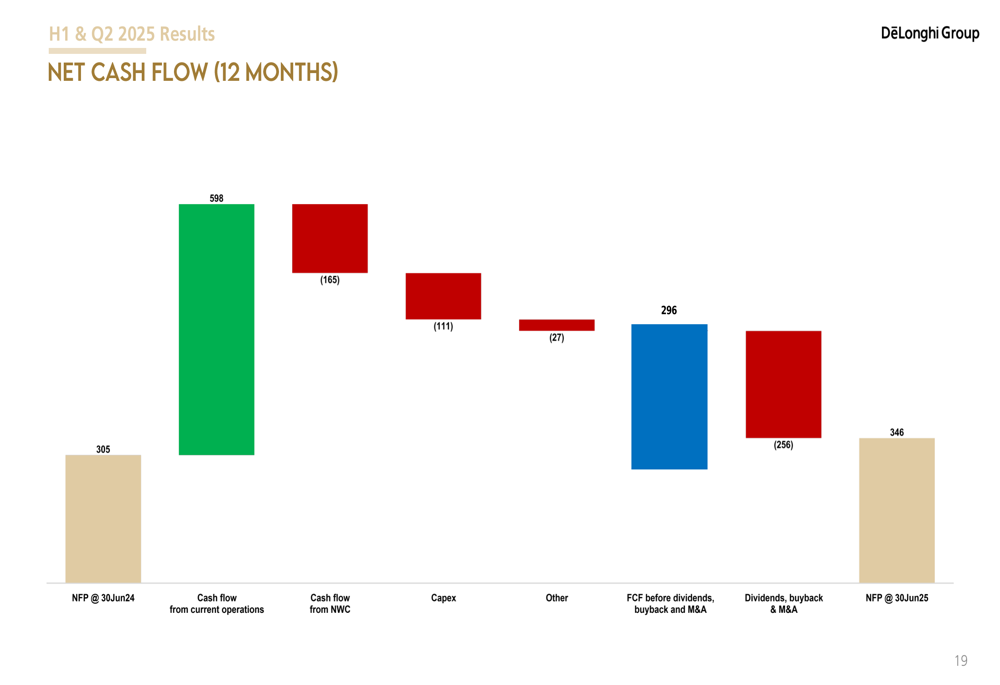

De’Longhi generated solid free cash flow of €296 million over the trailing 12 months before dividends, buyback, and M&A activities. The 12-month cash flow breakdown shows €598 million from operations, partially offset by €165 million in working capital changes and €111 million in capital expenditures.

The following waterfall chart illustrates the 12-month net cash flow:

Strategic Initiatives

De’Longhi continues to focus on enhancing global brand visibility through high-impact activations at premier events. The presentation highlighted the company’s presence at several key industry events, including the Milan Design Week, London Coffee Festival, and World of Coffee Geneva.

The company emphasized its prompt reaction to tariffs through a flexible operational footprint and solid partnerships. Additionally, De’Longhi continues to invest in advertising and promotion, with plans for an upcoming global coffee campaign to further strengthen its market position.

The H1 2025 key takeaways summarize the company’s strategic focus:

Forward-Looking Statements

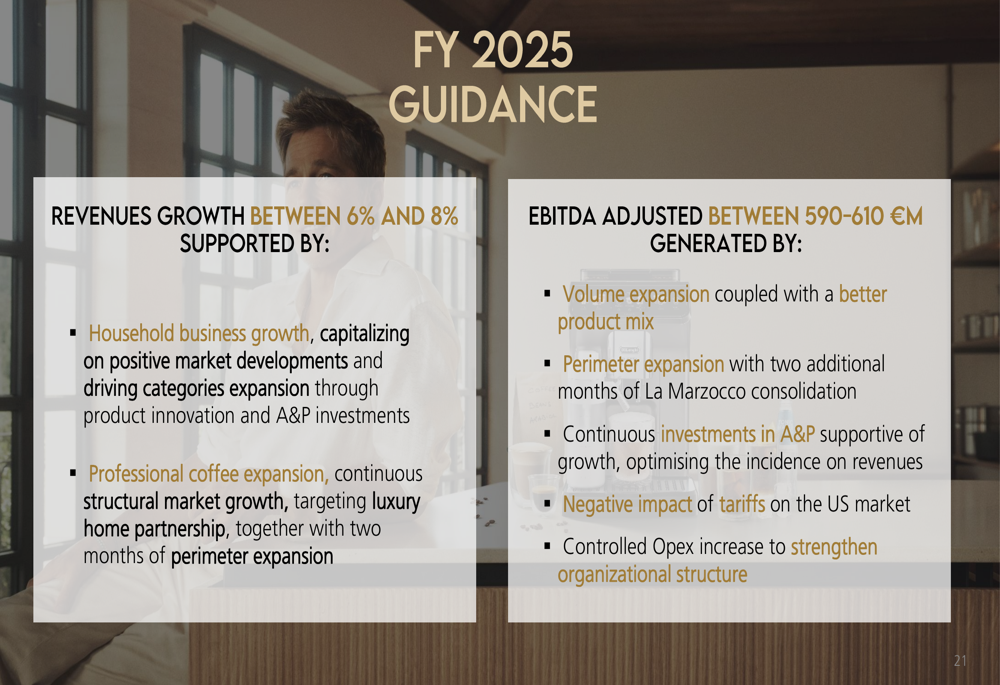

Looking ahead, De’Longhi provided guidance for fiscal year 2025, projecting revenue growth between 6% and 8%. This growth is expected to be supported by expansion in both the Household and Professional divisions, with a particular focus on product innovation and advertising investments.

The company forecasts adjusted EBITDA between €590-610 million for FY 2025, driven by volume expansion, improved product mix, and the consolidation of La Marzocco for an additional two months. However, De’Longhi acknowledged potential headwinds from U.S. tariffs, which it plans to mitigate through pricing strategies and cost management.

The detailed FY 2025 guidance is presented in the following slide:

This guidance represents a slight upward revision from the company’s previous outlook provided in its 2024 earnings report, which projected 2025 revenue growth of 5-7% and adjusted EBITDA of €550-600 million. The more optimistic outlook suggests management’s confidence in the company’s growth trajectory despite macroeconomic challenges.

De’Longhi’s continued focus on both organic growth and potential M&A opportunities, particularly in the coffee and kitchen appliances sectors, positions the company to maintain its growth momentum through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.