IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

Denny’s Corporation (NASDAQ:DENN) released its Q1 2025 investor presentation on May 5, 2025, revealing divergent performance between its two restaurant brands. The presentation comes after Denny’s reported disappointing Q4 2024 results that missed analyst expectations, contributing to the stock’s continued decline. Currently trading at $3.70 in after-hours trading, down 2.37% from its close of $3.79, Denny’s shares have fallen significantly from their 52-week high of $8.30.

The company’s Q1 2025 results highlight the contrasting trajectories of its flagship Denny’s brand, which experienced negative same-restaurant sales, and its growing Keke’s Breakfast Cafe concept, which showed positive momentum. This performance disparity underscores the company’s strategic focus on expanding the Keke’s brand while working to stabilize its core Denny’s business.

Quarterly Performance Highlights

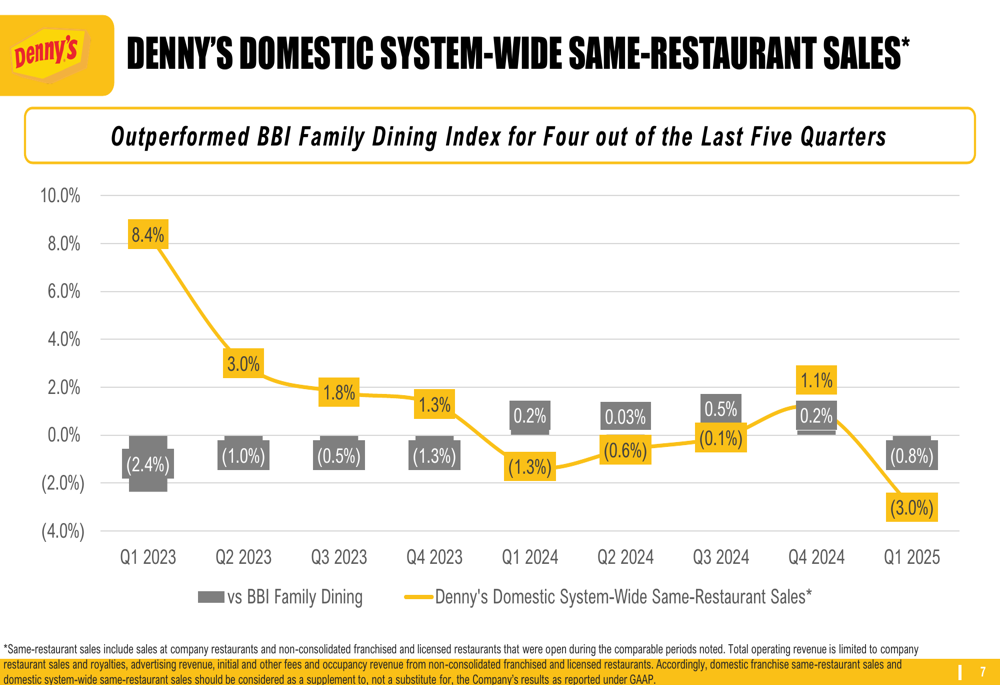

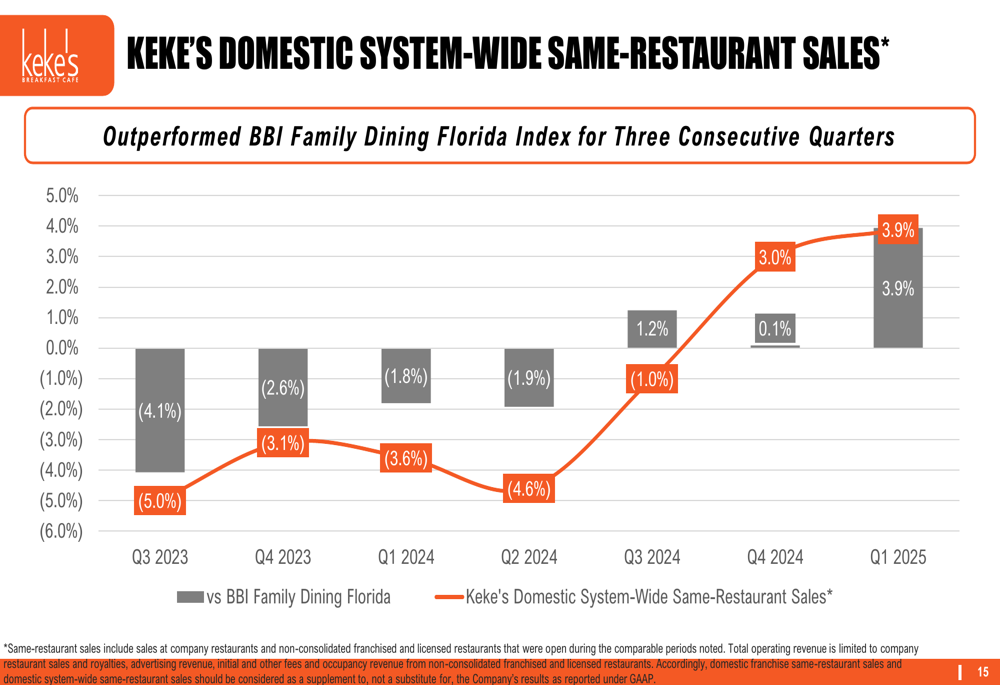

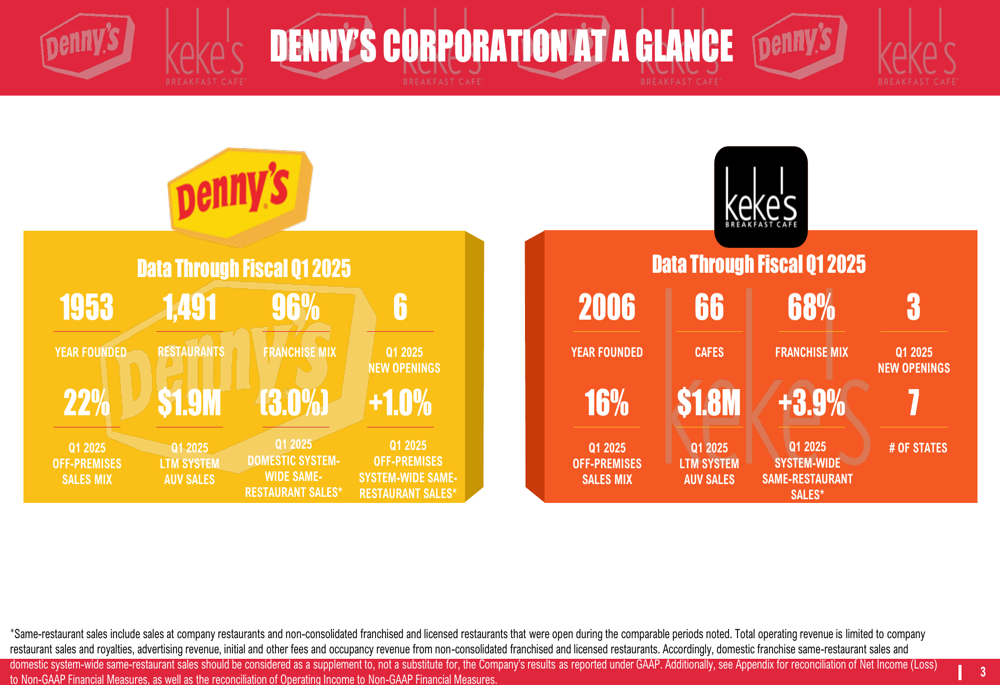

Denny’s reported domestic system-wide same-restaurant sales of -3.0% for its flagship brand in Q1 2025, while Keke’s Breakfast Cafe delivered positive same-restaurant sales of +3.9%. This stark contrast illustrates the different growth trajectories of the two concepts, with Keke’s outperforming the BBI Family Dining Florida Index by nearly 400 basis points.

As shown in the following chart comparing Denny’s performance to industry benchmarks, the brand has outperformed the BBI Family Dining Index for four out of the last five quarters, though it slipped in Q1 2025:

For Keke’s, the positive momentum is even more pronounced, with the brand outperforming the BBI Family Dining Florida Index for three consecutive quarters:

Off-premises sales continue to be a significant component of the business model for both brands, accounting for 22% of Denny’s sales and 16% of Keke’s sales in Q1 2025. For Denny’s, off-premises sales actually benefited same-restaurant sales by +1.0%, partially offsetting declines in dine-in traffic.

The company’s financial position remains stable but challenging, with Q1 2025 operating income of $5.2 million and net income of just $0.3 million, resulting in earnings per share of $0.01. This represents a significant decline from historical performance, as operating income has trended downward from $73.6 million in 2018 to $45.3 million in 2024.

Strategic Initiatives

Both brands are focusing heavily on remodel programs to drive growth. Denny’s Diner 2.0 Remodel Program has shown promising results during testing, with a sales lift of +6.4% and traffic lift of +6.5%. Over 50% of company-owned restaurants and more than 10% of franchised locations have been remodeled to the new image.

As illustrated in the following image, the remodel program represents a significant investment with clear performance targets:

Similarly, Keke’s is implementing its own remodel program with ambitious targets, including a sales lift of +6-8% and an internal rate of return of +30%. The company currently has three company remodels in test phase:

Denny’s is also leveraging value offerings to drive traffic, with the relaunched $2-$4-$6-$8 menu continuing to be a staple for consumers. The company introduced a new BOGO $1 offer at the end of Q1 to drive incremental dine-in traffic. Meanwhile, Keke’s has expanded its alcohol program to approximately 80% of its system and launched new menu items including a kids cheeseburger meal and stuffed French toast with bananas and Nutella®.

Digital enhancements remain a priority, with Denny’s reporting that improvements to the digital guest experience increased conversion rates by over 16% in Q1.

Competitive Industry Position

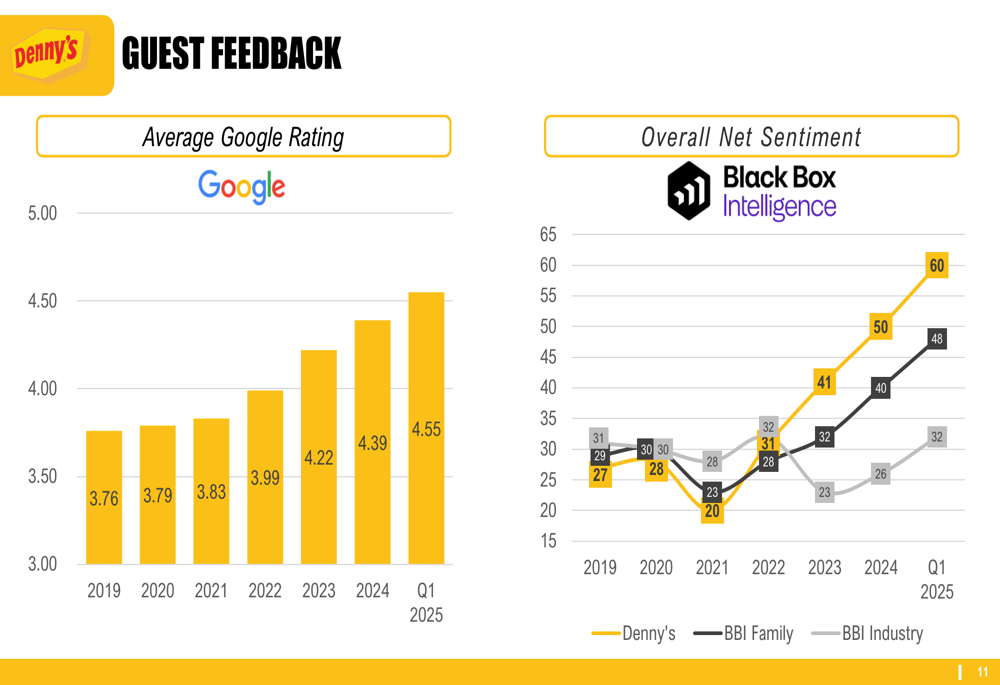

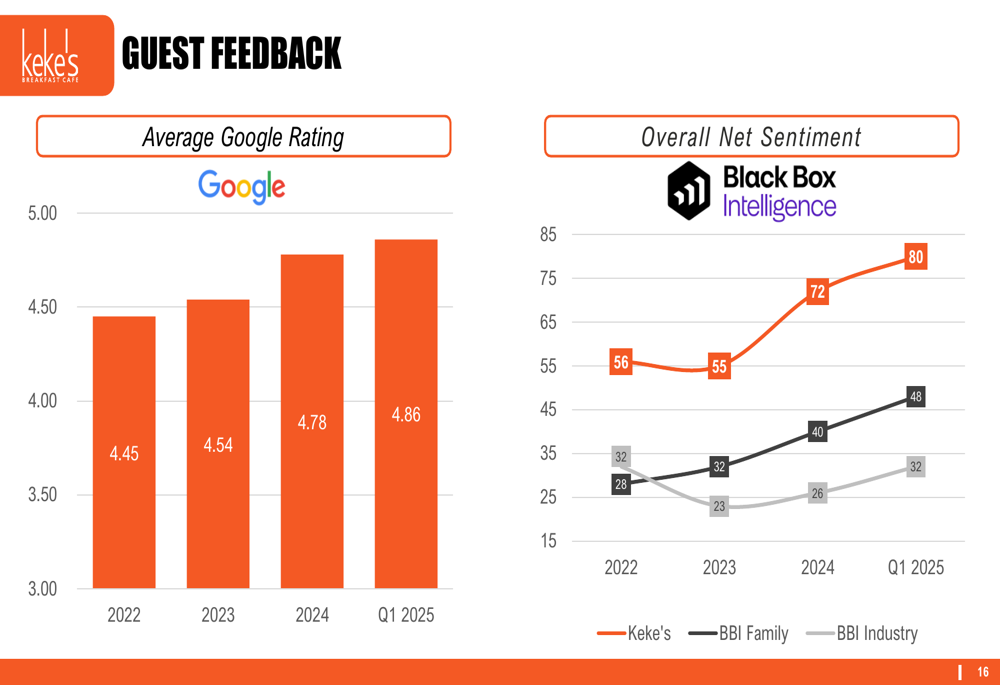

Both brands have shown improvement in guest satisfaction metrics, with Denny’s average Google (NASDAQ:GOOGL) rating increasing from 3.76 in 2019 to 4.55 in Q1 2025, and Keke’s rating rising from 4.45 in 2022 to 4.86 in Q1 2025.

The following chart illustrates Denny’s improving guest feedback metrics compared to industry benchmarks:

Keke’s has shown even stronger guest satisfaction results, significantly outperforming industry benchmarks:

Denny’s maintains a strong presence with 1,491 restaurants globally (96% franchised), while Keke’s has 66 cafes across 7 states (68% franchised). The company provided a comprehensive overview of both brands in its presentation:

Forward-Looking Statements

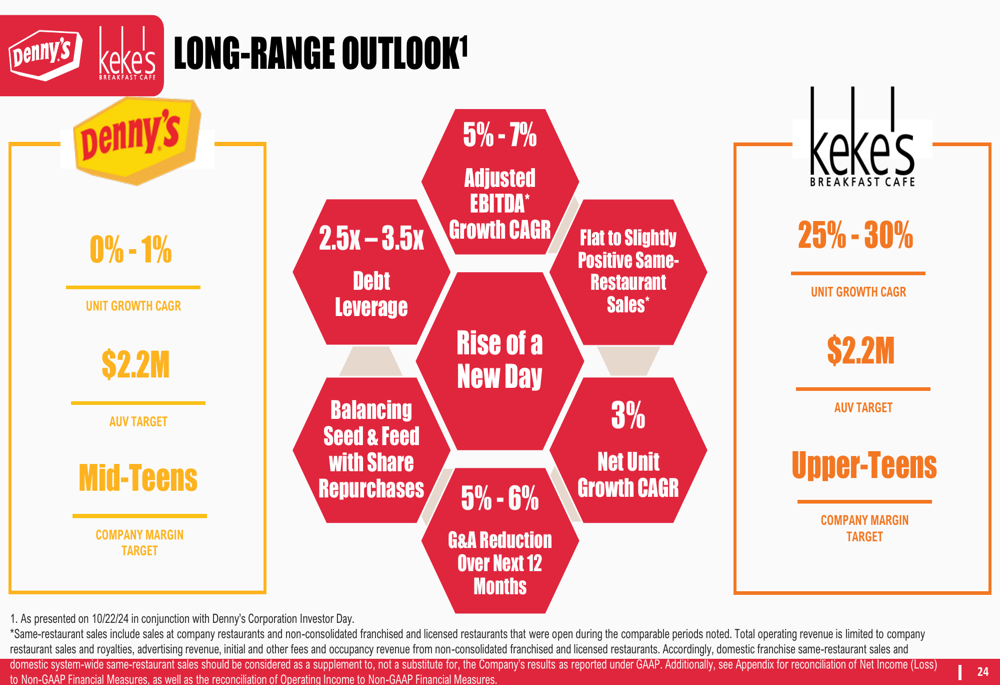

Despite current challenges, Denny’s provided an optimistic long-range outlook for both brands. The company expects Denny’s unit growth CAGR of 0-1% and adjusted EBITDA growth CAGR of 5-7%, while projecting much stronger unit growth for Keke’s at 25-30% CAGR.

The following slide details the company’s long-range targets for both brands:

Denny’s aims to reduce its debt leverage, which stood at 3.9x at the end of Q1 2025, to a long-term target of 2.5x-3.5x. The company expects to refinance its existing credit facility prior to August 2025 and anticipates that debt leverage will moderate throughout the year.

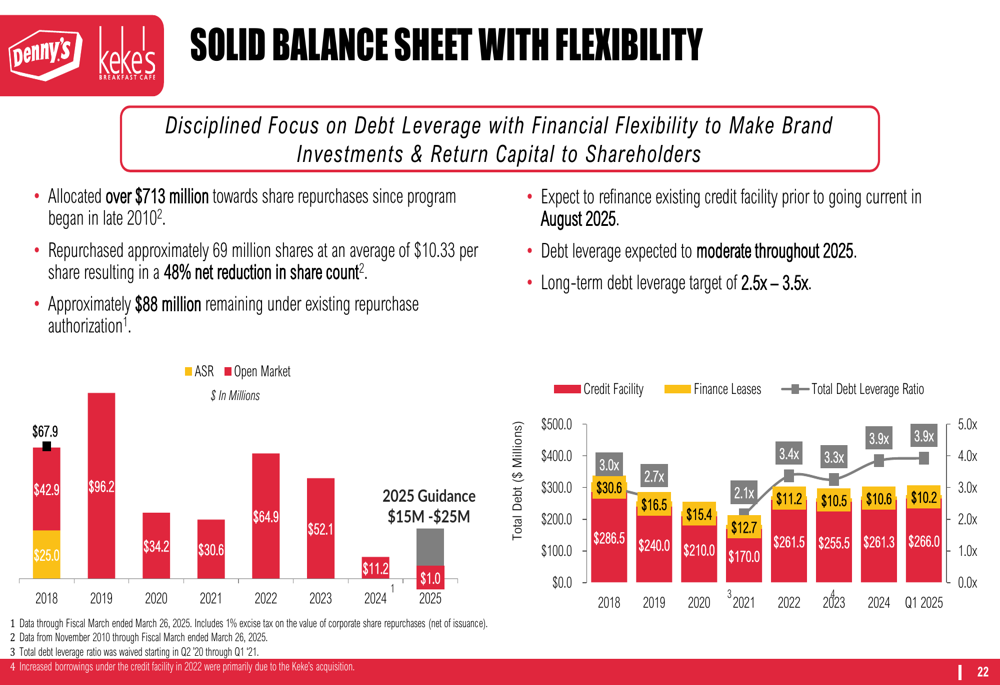

As shown in the following chart, the company has maintained a solid balance sheet despite recent challenges:

For 2025, Denny’s projects domestic system-wide same-restaurant sales to range from a 2% decline to a 1% increase, aligning with the Q1 performance. The company plans to open 25-40 new restaurants while closing 70-90 others, expecting consolidated adjusted EBITDA between $80-85 million.

Keke’s expansion remains a bright spot, with over 135 development commitments in the pipeline across 10 different states, representing a significant growth opportunity as the brand expands beyond its core Florida market.

The contrasting performance between Denny’s and Keke’s highlights the company’s dual-brand strategy, with Keke’s providing growth potential while the company works to stabilize and revitalize its flagship Denny’s brand amid challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.