Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Densan System Holdings Co., Ltd. (TSE:4072) presented its second quarter fiscal year 2025 results on August 12, 2025, revealing continued growth across its business segments despite facing some operational challenges. The company, which specializes in information services and payment agency solutions, maintained its full-year forecast despite recent market volatility, with its stock price declining 5.26% to ¥3,515 in recent trading.

Quarterly Performance Highlights

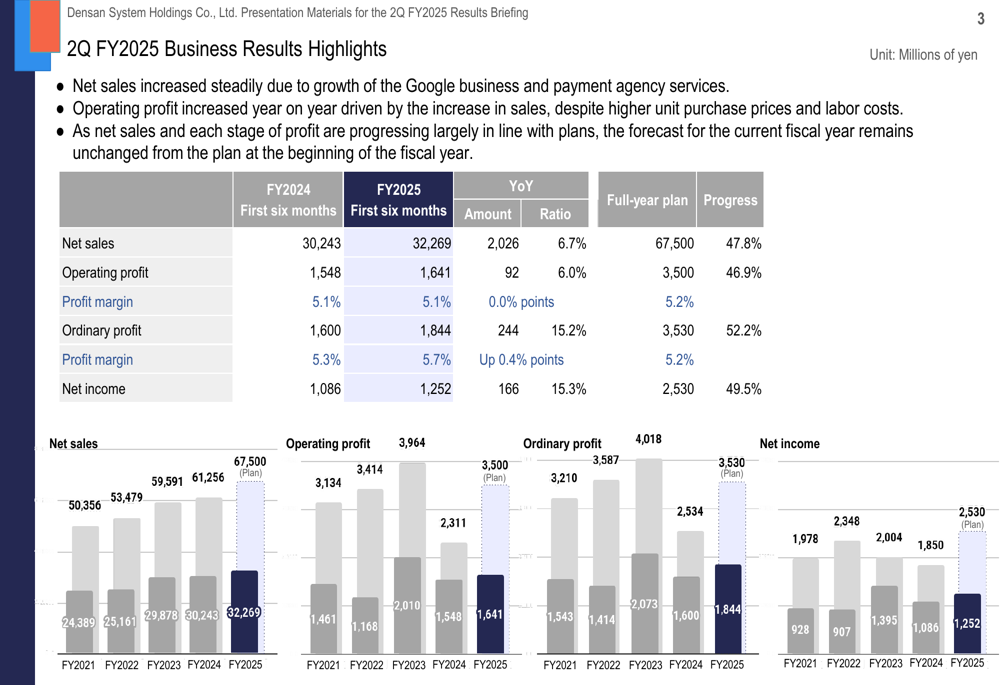

Densan System reported net sales of ¥32,269 million for the first six months of FY2025, representing a 6.7% year-over-year increase. Operating profit grew 6.0% to ¥1,641 million, while ordinary profit and net income showed more substantial gains of 15.2% and 15.3%, respectively. The company has achieved approximately 48% of its full-year sales target and 47% of its operating profit goal.

As shown in the following financial highlights chart, the company has maintained steady growth across all key metrics:

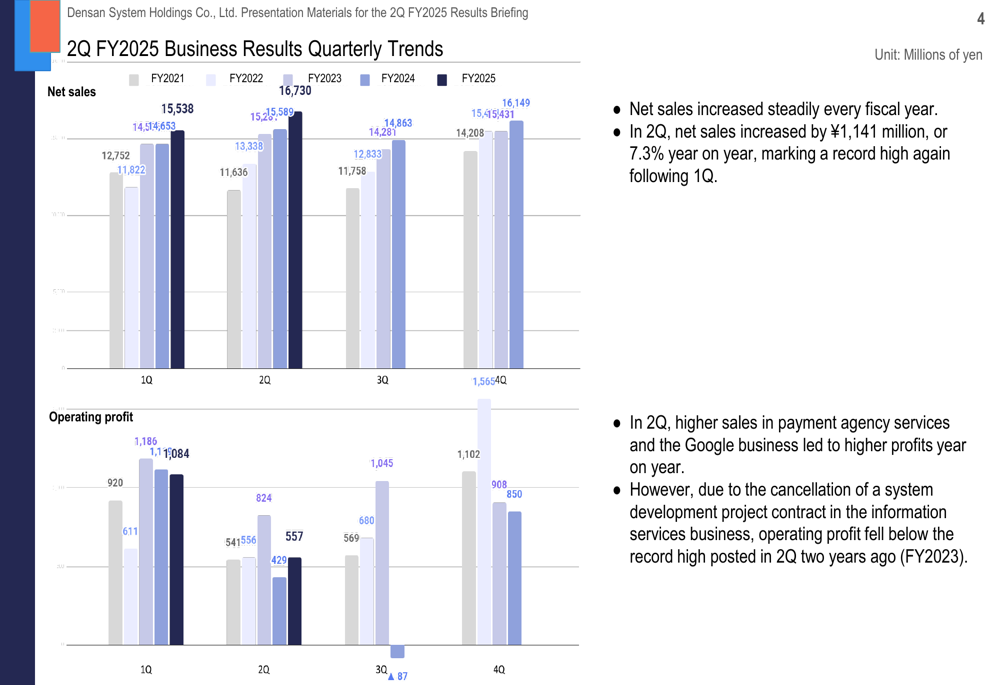

Quarterly performance analysis shows that Q2 net sales increased by ¥1,141 million or 7.3% year-on-year, marking a record high for the second consecutive quarter. The company noted that higher sales in payment agency services and the Google business were the primary drivers of profit growth, though results were tempered by the cancellation of a system development project in the information services business.

Segment Analysis

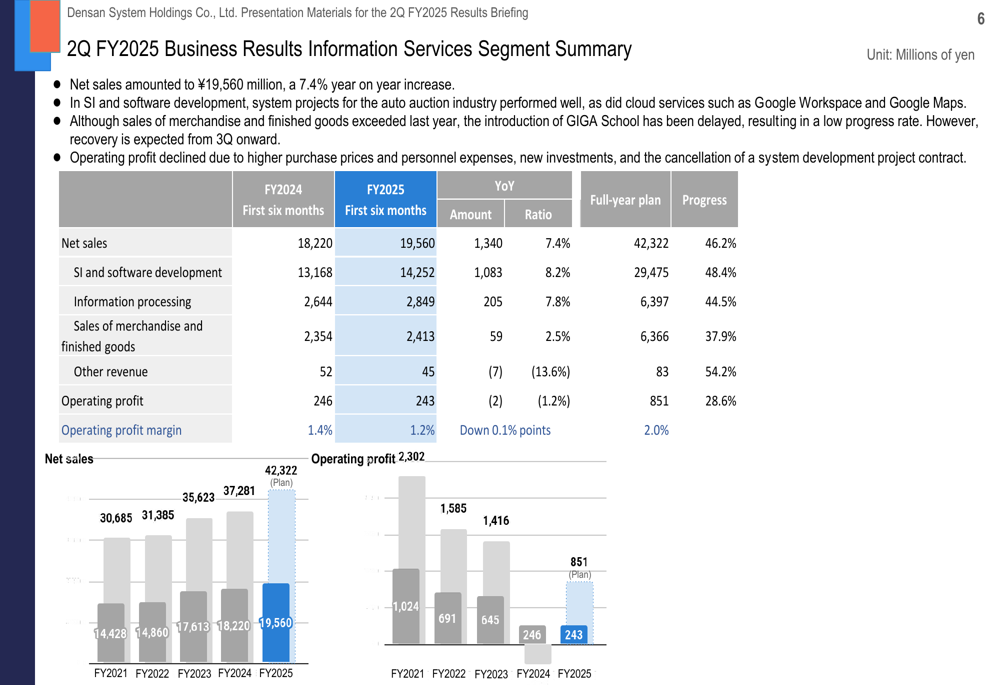

The Information Services segment, which accounts for approximately 61% of total revenue, posted sales of ¥19,560 million, up 7.4% year-on-year. However, operating profit in this segment declined slightly by 1.2% to ¥243 million, with profit margins contracting from 1.4% to 1.2%. Management attributed this decline to higher purchase prices, increased personnel expenses, new investments, and the aforementioned project cancellation.

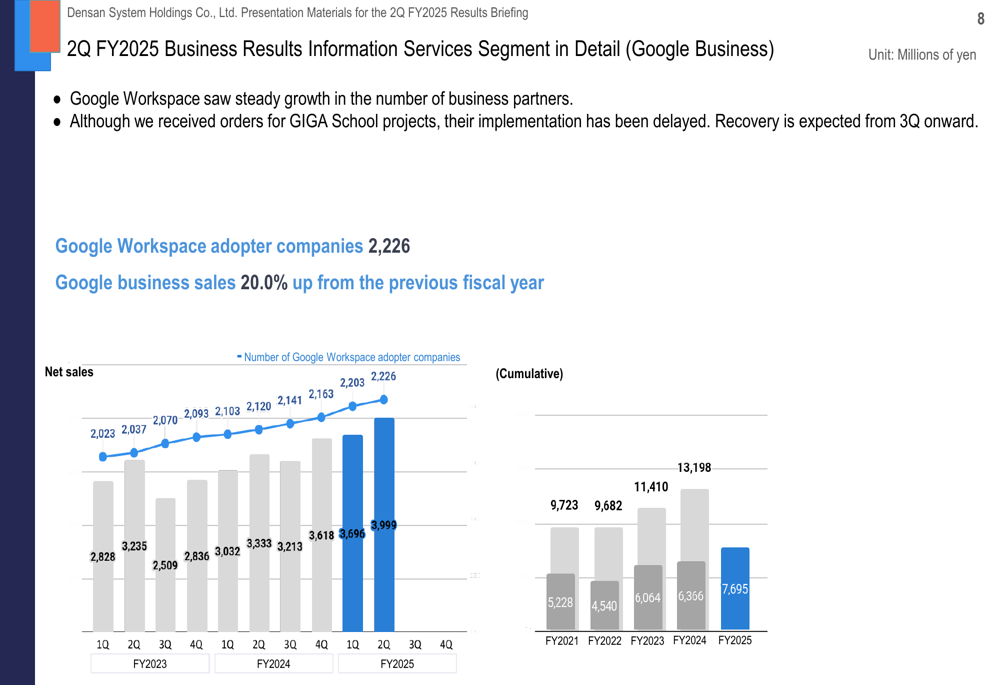

Within the Information Services segment, the Google business showed particularly strong performance with a 20.0% year-over-year increase in sales. The company reported steady growth in Google Workspace adopter companies, reaching 2,226 by the end of Q2 FY2025. However, the presentation noted that GIGA School project implementation delays impacted merchandise sales, though recovery is expected in the second half of the fiscal year.

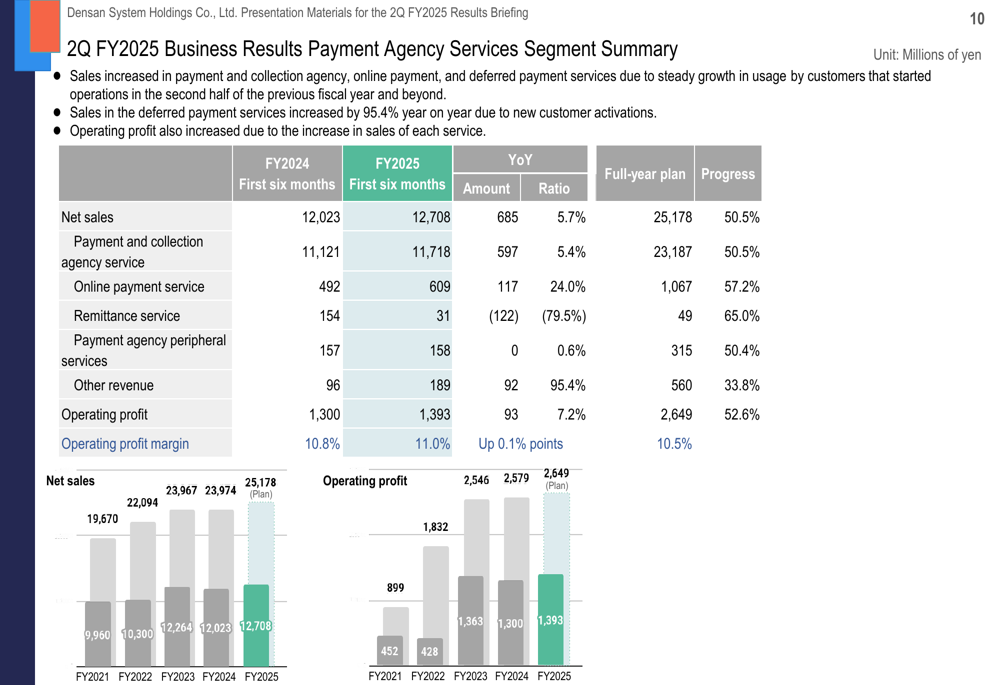

The Payment Agency Services segment delivered robust results with net sales increasing 5.7% year-on-year to ¥12,708 million and operating profit rising 7.2% to ¥1,393 million. This segment maintained a healthy operating profit margin of 11.0%, up slightly from 10.8% in the previous year. The company highlighted particularly strong growth in online payment services, which increased 24.0% year-on-year.

Financial Condition

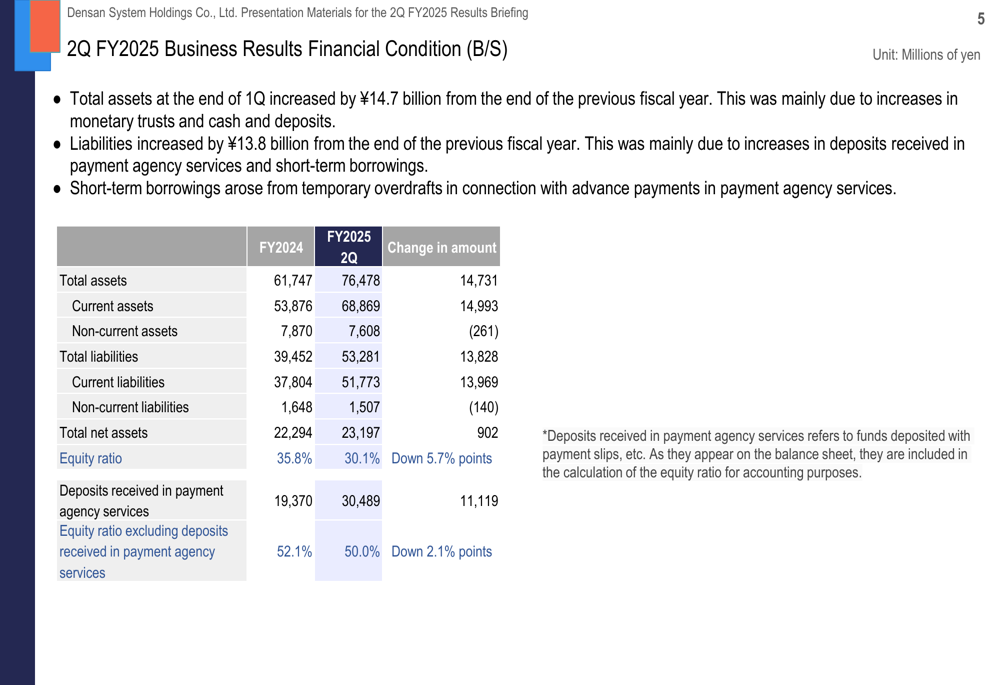

Densan System’s balance sheet showed significant changes during the quarter, with total assets increasing by ¥14.7 billion from the end of the previous fiscal year to ¥76,478 million. This was matched by a ¥13.8 billion increase in liabilities, primarily due to growth in deposits received in payment agency services, which rose by ¥11.1 billion. As a result, the equity ratio declined from 35.8% to 30.1%.

Strategic Initiatives

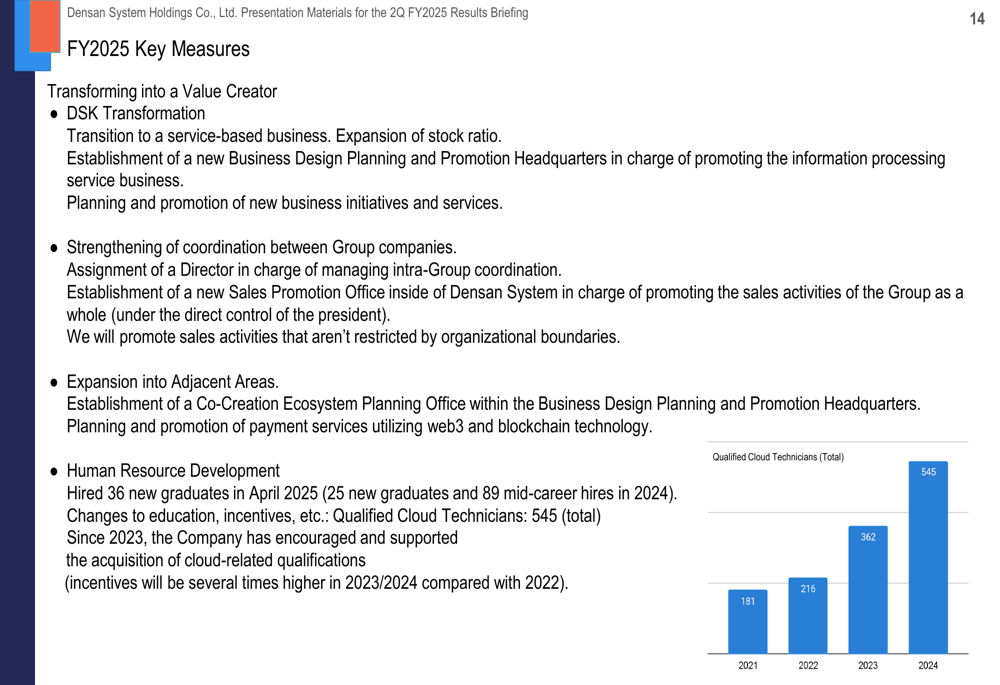

Looking ahead, Densan System outlined several key strategic initiatives for FY2025, centered around transforming into a "value creator." The company is focusing on transitioning to a more service-based business model, strengthening coordination between group companies, and expanding into adjacent areas including new payment services and blockchain technology.

Human resource development remains a priority, with particular emphasis on cloud technology expertise. The presentation highlighted significant growth in qualified cloud technicians, which have increased from 362 in 2023 to 545 in 2024.

Forward-Looking Statements

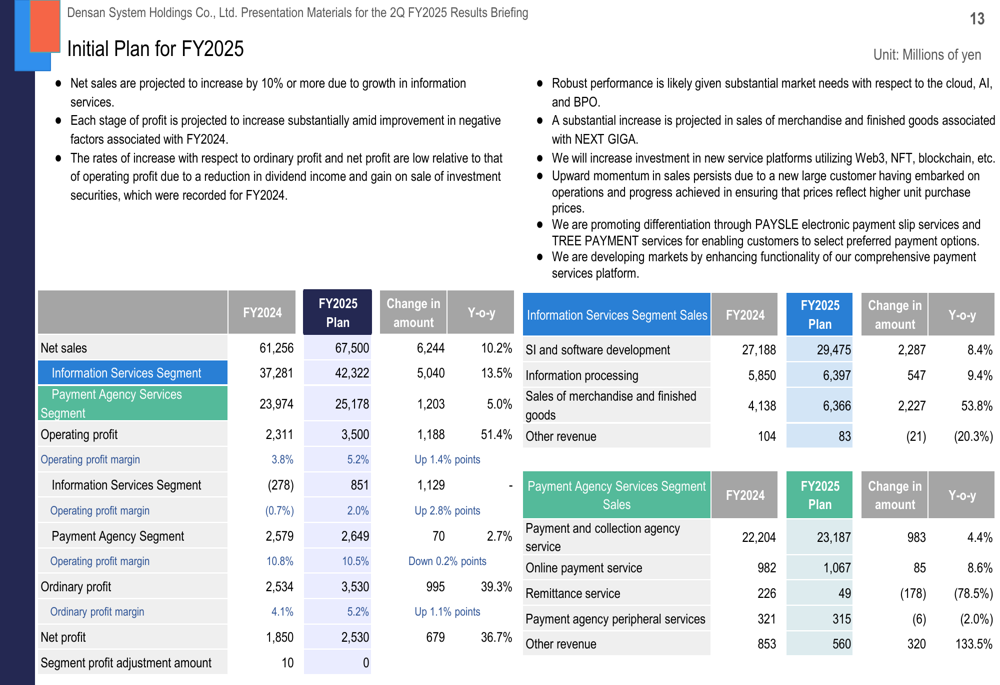

Densan System maintained its initial FY2025 forecast, projecting net sales to increase by 10.2% to ¥67,500 million and operating profit to surge by 51.4% to ¥3,500 million. The Information Services segment is expected to grow by 13.5%, while the Payment Agency Services segment is forecast to increase by 5.0%.

The company’s projections by business line show particularly strong growth expectations for merchandise sales (53.8% increase) within the Information Services segment, while the Payment Agency Services segment is expected to see more modest growth across its various service offerings.

Despite facing some operational challenges in Q2, including project cancellations and margin pressure in the Information Services segment, management expressed confidence in achieving its full-year targets through continued expansion of its Google business, growth in payment and online payment services, and recovery in delayed GIGA School projects in the second half of the fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.