Gold prices edge lower; heading for weekly losses ahead of U.S.-Russia talks

Introduction & Market Context

Dentalcorp Holdings Ltd (TSX:DNTL) presented its Q2 2025 investor slides on August 8, 2025, highlighting the company’s continued expansion as Canada’s largest dental practice network. The presentation showcased Dentalcorp’s strong financial performance, consolidation strategy, and technological initiatives within the $22 billion Canadian dental market.

The company’s stock closed at $8.21 following the presentation, up 0.49% for the day, continuing its positive momentum after gaining 45.84% over the past year according to recent data. This performance comes as Dentalcorp maintains its position in a highly fragmented market where 93% of Canada’s approximately 16,000 dental practices remain independently operated.

Quarterly Performance Highlights

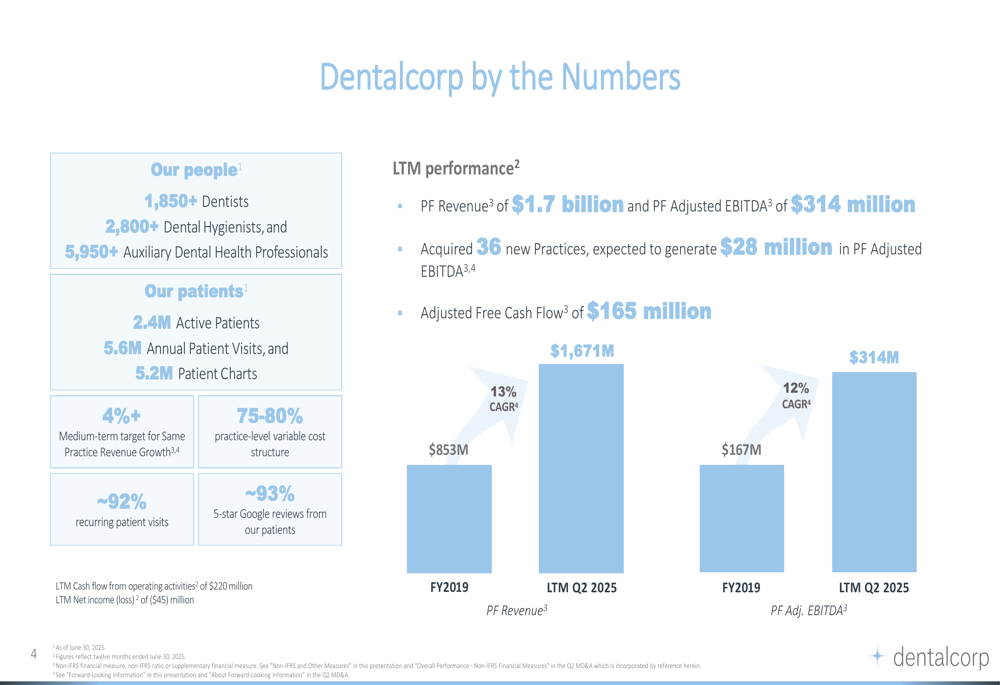

Dentalcorp reported impressive financial metrics for the trailing twelve months ending Q2 2025, including $1.7 billion in pro forma revenue and $314 million in pro forma adjusted EBITDA. The company has maintained strong growth trajectories across key metrics since its IPO.

As shown in the following chart of financial performance:

The company highlighted its consistent revenue growth with a 13% CAGR from FY2019 to Q2 2025 LTM, while adjusted EBITDA grew at a 12% CAGR over the same period. This performance builds on Q1 2025 results, where the company reported a 10% year-over-year revenue increase to $409.4 million and an 11.5% growth in adjusted EBITDA to $75.9 million.

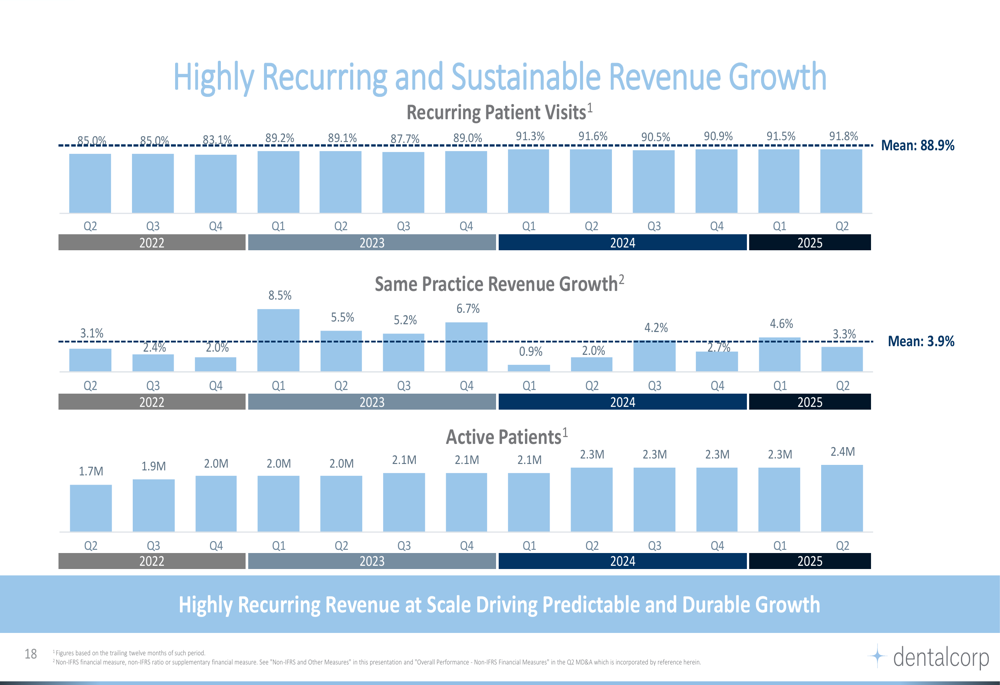

Dentalcorp’s recurring revenue model is evidenced by approximately 92% recurring patient visits and a steady increase in active patients, providing stability to its business model.

The following chart illustrates the company’s recurring revenue trends:

Strategic Growth Initiatives

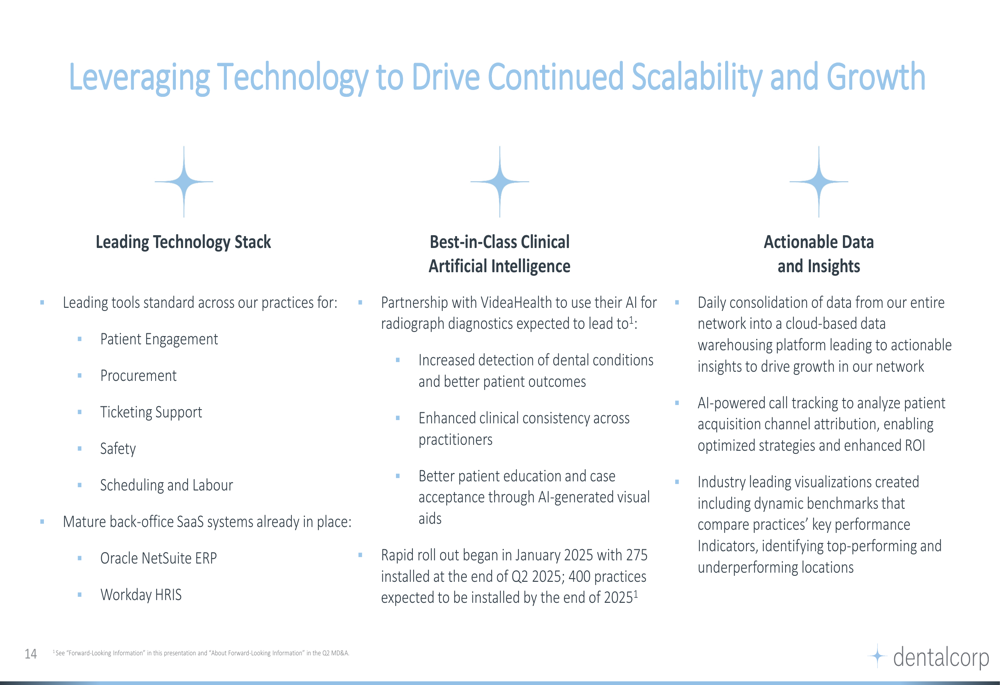

Dentalcorp’s growth strategy rests on three pillars: organic growth, operating productivity, and acquisitive growth. The company has set a medium-term target of 4%+ for same-practice revenue growth, driven by expanded specialty services and technology implementation.

The company’s presentation detailed its AI-driven diagnostic tools, with 275 practices equipped with VideaHealth’s AI radiograph diagnostics by the end of Q2 2025. Dentalcorp expects to expand this technology to 400 practices by year-end, enhancing diagnostic capabilities and practice efficiency.

The company’s strategic technology implementation is illustrated in this slide:

Dentalcorp continues to execute its acquisition strategy, having completed acquisitions of 36 practices expected to generate $28 million in pro forma adjusted EBITDA. The company’s presentation highlighted its ability to improve practice-level EBITDA margins by 10-15%+ following acquisition through labor optimization, procurement efficiencies, and technology integration.

Competitive Industry Position

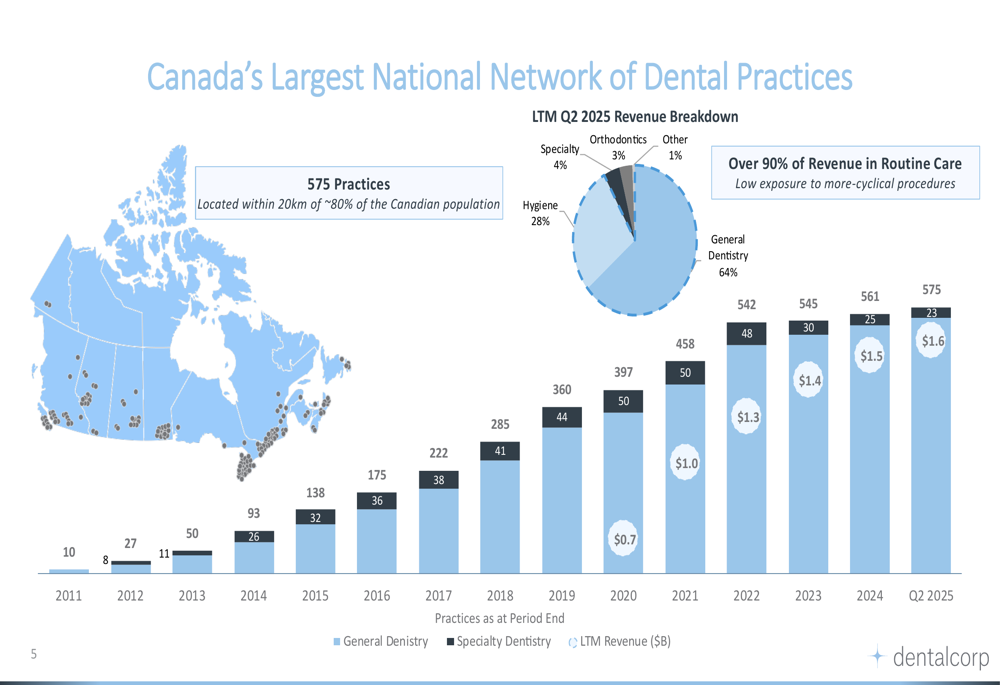

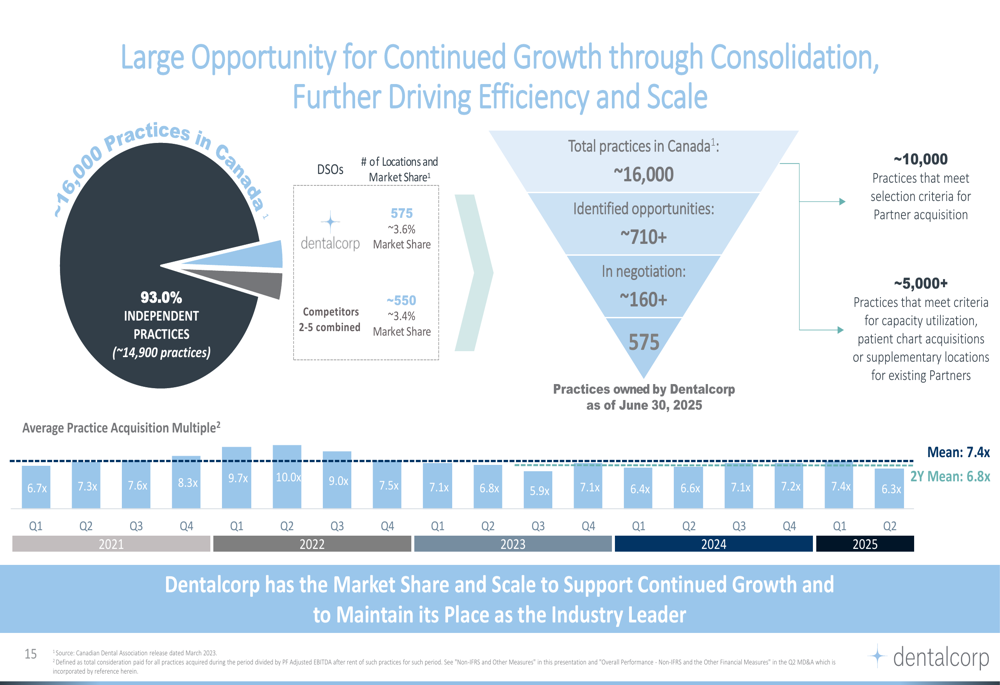

Dentalcorp has established itself as the dominant player in Canada’s dental market, with 575 practices representing approximately 3.6% market share. The company’s national footprint reaches approximately 80% of the Canadian population within 20km of its locations.

The following map illustrates Dentalcorp’s extensive network across Canada:

The company’s presentation emphasized the significant consolidation opportunity that remains, with over 710 potential acquisition targets identified and more than 160 in active negotiation. This represents a substantial runway for continued growth in a highly fragmented market.

The consolidation opportunity is visualized in this comprehensive market overview:

Financial Outlook and Guidance

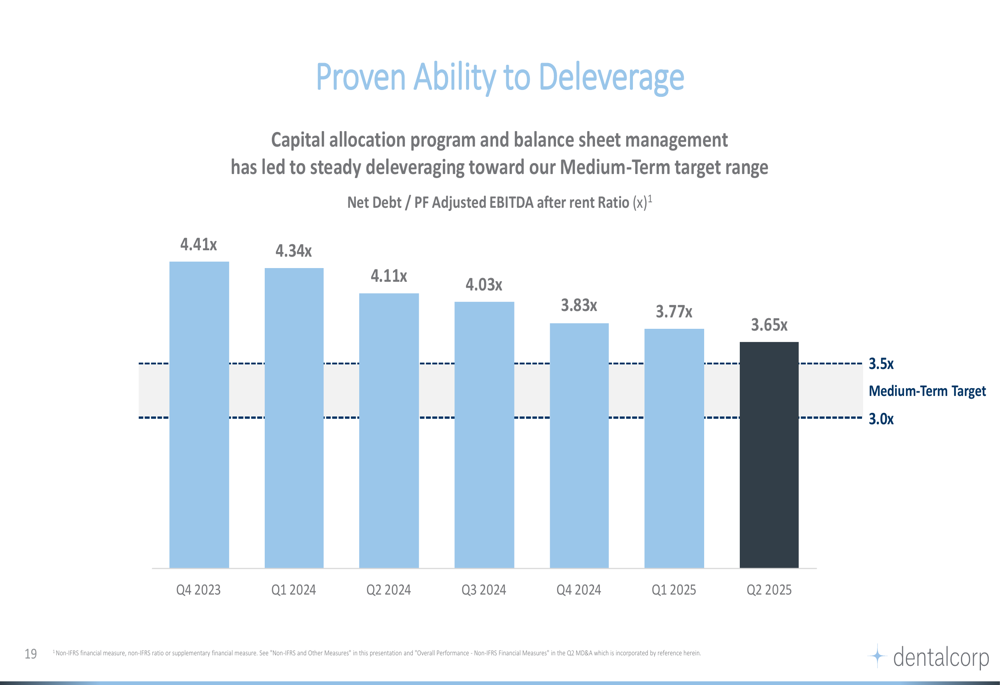

Dentalcorp highlighted its deleveraging progress, reducing its Net Debt to Pro Forma Adjusted EBITDA ratio from 4.41x in Q4 2023 to 3.65x in Q2 2025, approaching its medium-term target range of 3.0x to 3.5x.

The company’s deleveraging trajectory is shown in the following chart:

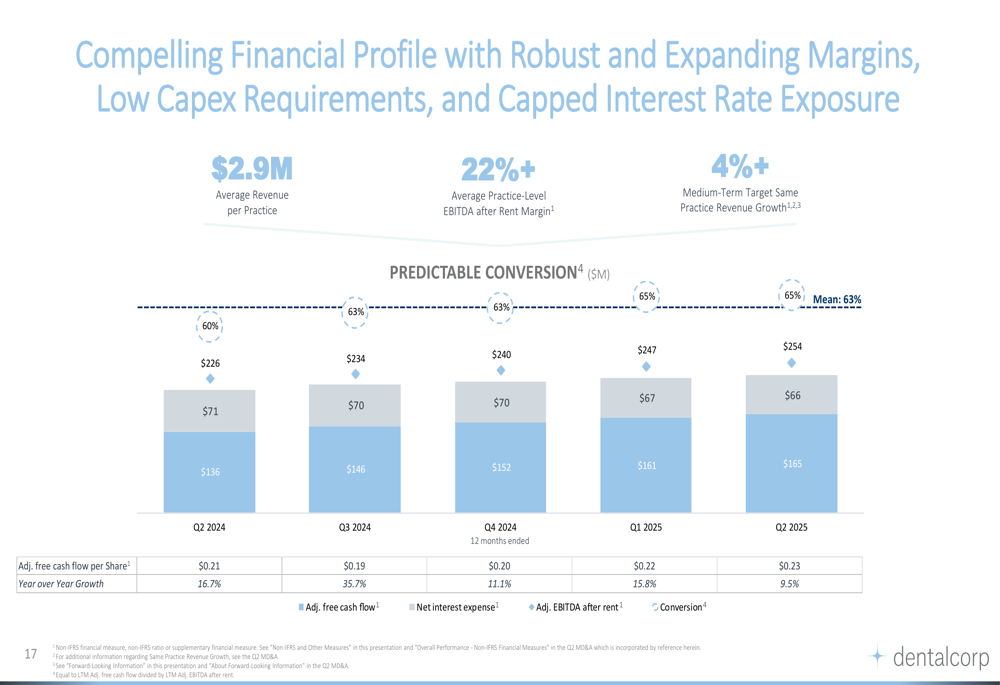

Free cash flow conversion improved from 60% to 63%, with adjusted free cash flow per share increasing from $0.21 in Q2 2024 to $0.23 in Q2 2025. This aligns with the company’s Q1 earnings report, which noted free cash flow conversion of 65%, up from 59% in the prior year period.

Dentalcorp’s financial profile includes robust margins and strong cash flow generation:

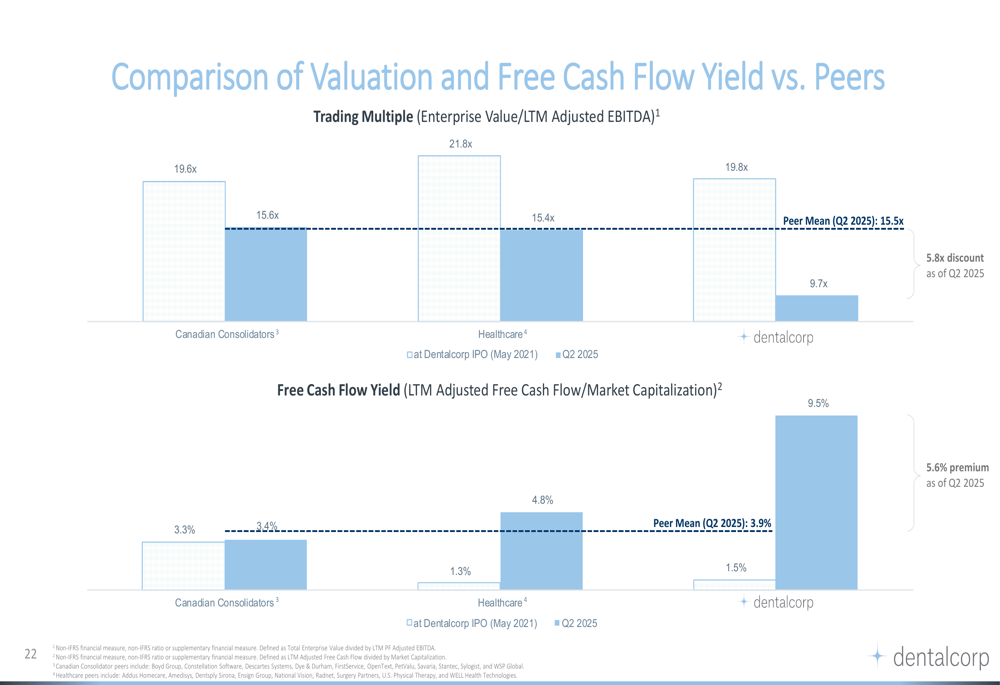

The company’s valuation metrics show a favorable free cash flow yield compared to peers, despite trading at a discount on an EV/EBITDA basis. According to the presentation, Dentalcorp’s free cash flow yield of 9.5% represents a 5.6% premium to its peer group average of 3.9%.

The comparative valuation metrics are illustrated in this chart:

For the full year 2025, Dentalcorp projects revenue growth of 10-11% and same-practice revenue growth of 3-5%, consistent with the guidance provided in its Q1 earnings report. The company also anticipates $25+ million in pro forma adjusted EBITDA from acquisitions and continued margin expansion.

With its combination of organic growth initiatives, operational efficiencies, and strategic acquisitions, Dentalcorp appears well-positioned to maintain its leadership in the Canadian dental market while delivering continued financial improvement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.