IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

DFDS A/S (CPH:DFDS) presented its Q1 2025 investor call on May 6, highlighting the company’s performance during what management described as a transition year. The Danish shipping and logistics company reported revenue growth amid a challenging competitive environment, particularly in its Mediterranean operations.

Trading at DKK 94.8 as of May 6, DFDS shares are closer to their 52-week low of DKK 77.3 than their high of DKK 230, reflecting investor caution about the company’s near-term prospects despite management’s confidence in the underlying strength of its network.

The company is navigating several external challenges, including European recession risks, changing US trade policies, and continued geopolitical tensions in Ukraine and Türkiye. Management noted that while European growth remains muted, they continue to see growth potential in Mediterranean and North African markets.

Quarterly Performance Highlights

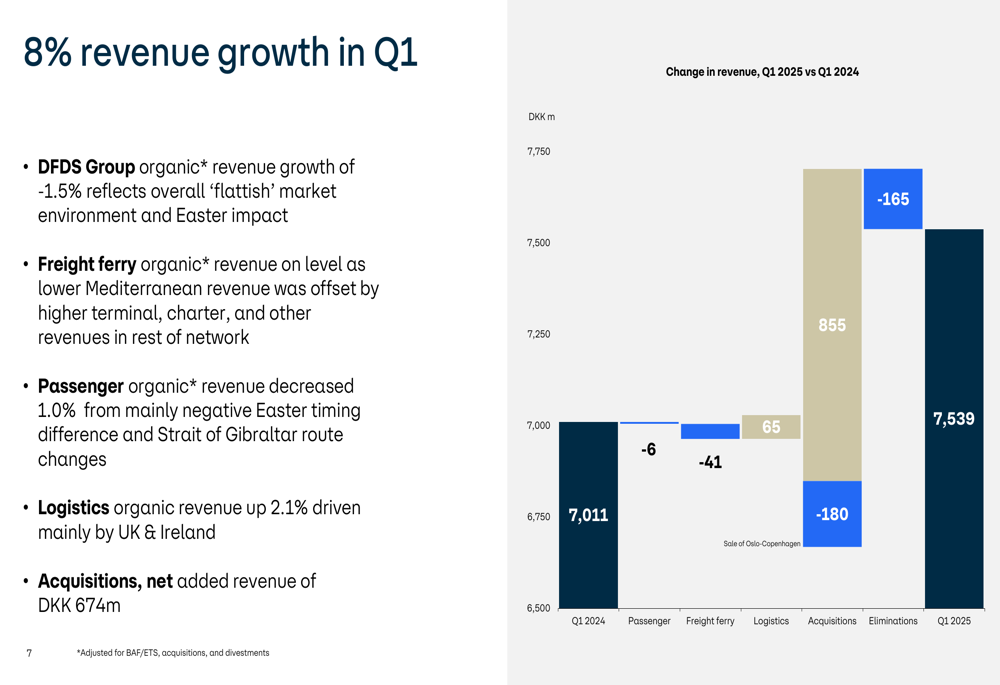

DFDS reported 8% revenue growth in Q1 2025, reaching DKK 7.54 billion compared to DKK 7.01 billion in Q1 2024. However, as shown in the following revenue breakdown, this growth was primarily driven by acquisitions, which added DKK 674 million, while organic growth was negative at -1.5%.

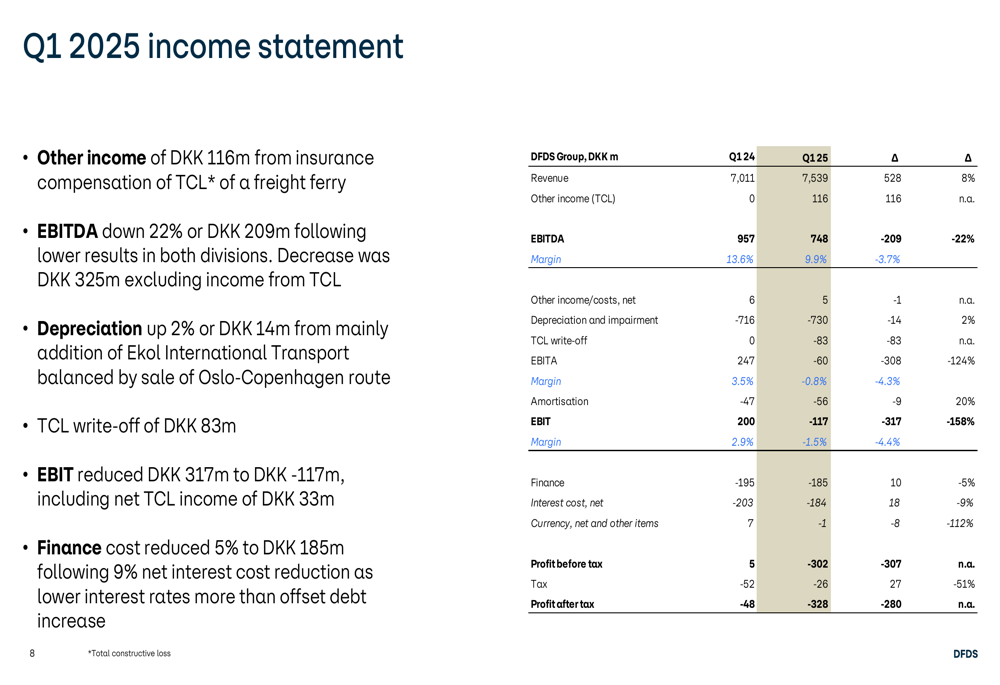

The company’s profitability metrics showed significant pressure during the quarter. EBITDA decreased by 22% to DKK 748 million, with margins contracting from 13.6% to 9.9%. EBIT turned negative at DKK -117 million, down from DKK 200 million in the same period last year, as illustrated in the comprehensive income statement:

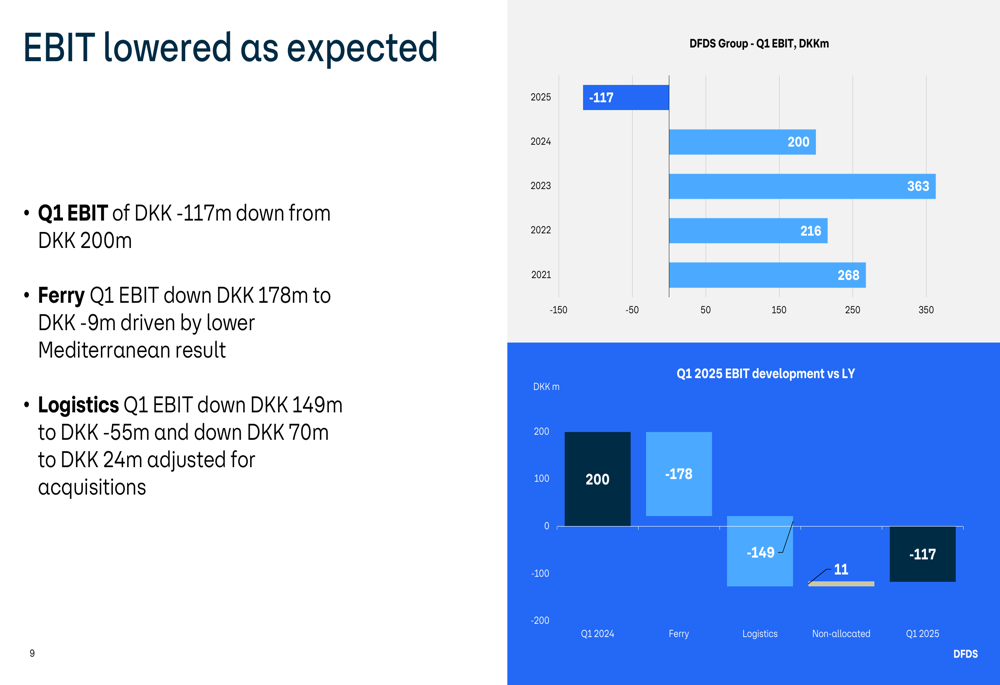

The EBIT decline was particularly notable when compared to previous years’ first quarters, highlighting the severity of the current challenges:

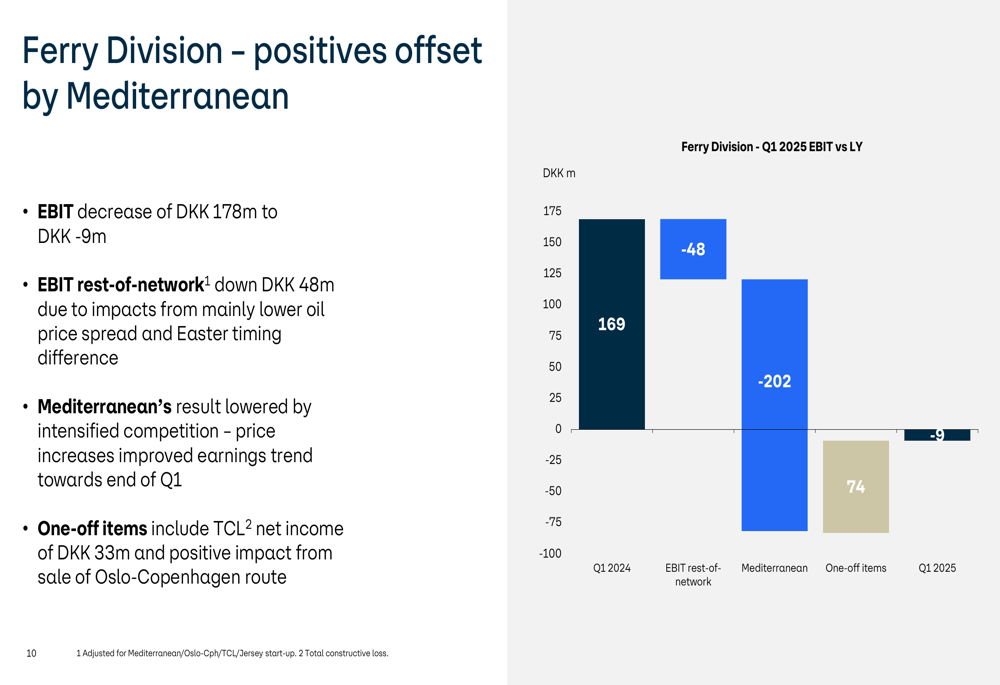

The Ferry Division, traditionally DFDS’s strongest performer, saw its EBIT decline by DKK 178 million to DKK -9 million. This was primarily driven by intensified competition in the Mediterranean region, which offset positive performance in other network areas:

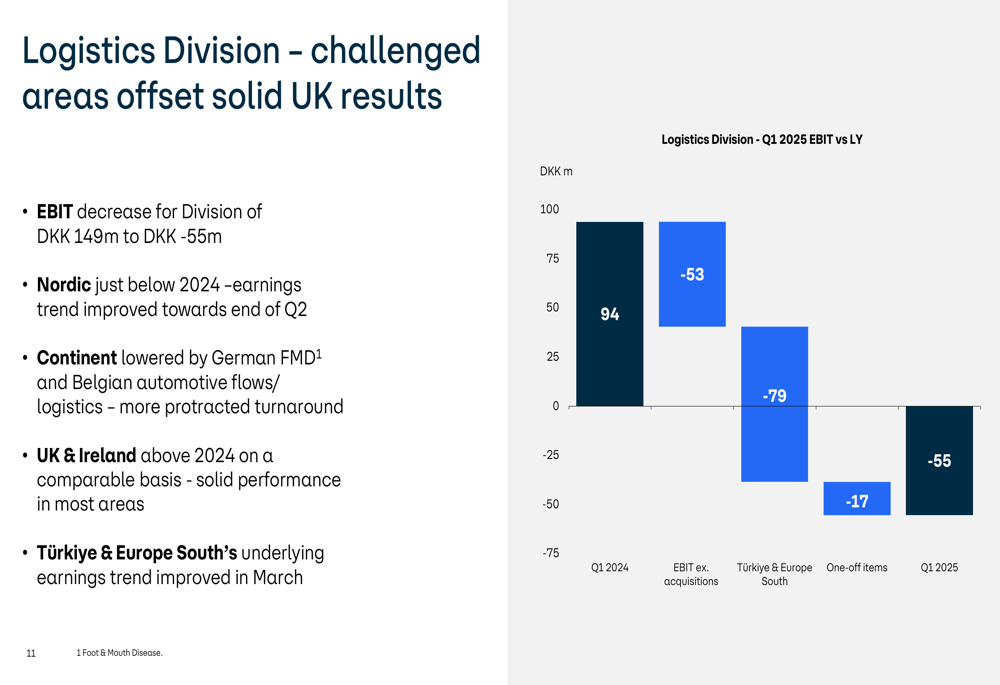

Similarly, the Logistics Division reported an EBIT decrease of DKK 149 million to DKK -55 million. While the UK & Ireland business performed above 2024 levels, this was more than offset by challenges in the Continent region and significant losses in Türkiye & Europe South:

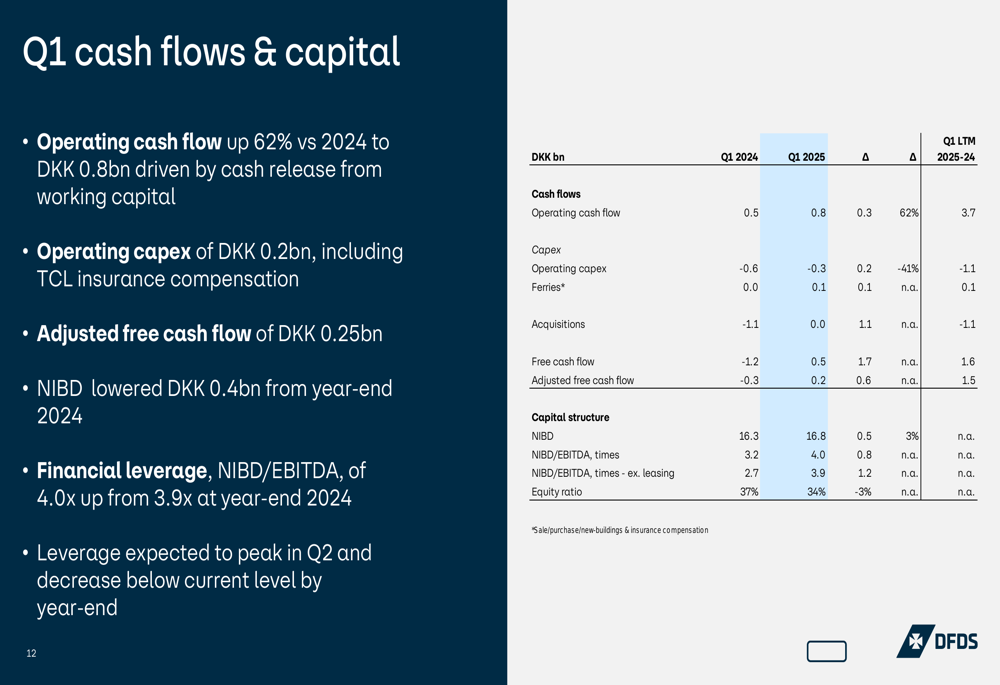

Despite these operational challenges, DFDS demonstrated strong cash flow management. Operating cash flow increased by 62% compared to Q1 2024, reaching DKK 0.8 billion, and the company reduced its net interest-bearing debt by DKK 0.4 billion from year-end 2024:

Strategic Initiatives

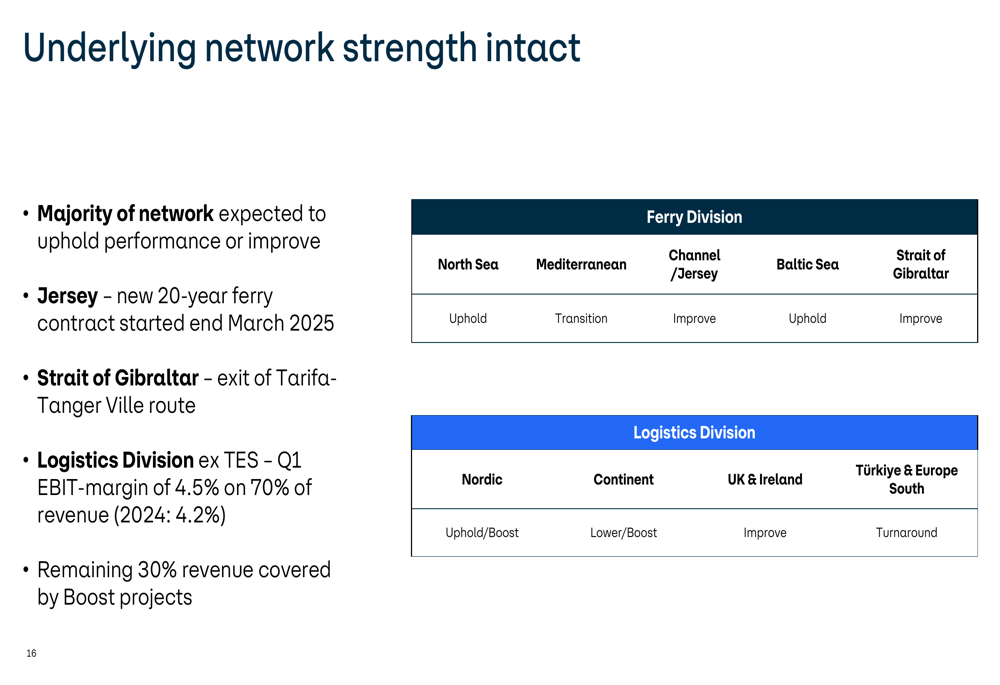

DFDS outlined three key focus areas for 2025 to address current challenges while maintaining the underlying strength of its network. The company categorized its various business segments according to their strategic priorities, ranging from "Uphold" for strong performers to "Turnaround" for struggling operations:

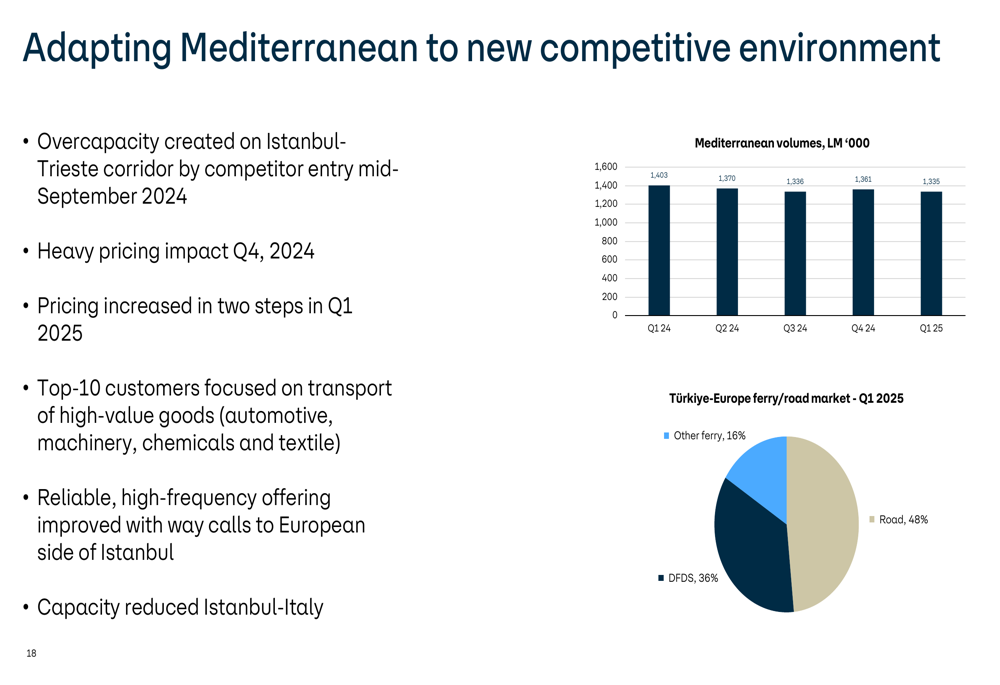

The Mediterranean business faces significant competitive pressure, particularly on the Istanbul-Trieste corridor where overcapacity has led to pricing challenges. Management has implemented a two-step pricing increase in Q1 2025 and reduced capacity on Istanbul-Italy routes to adapt to the new competitive environment:

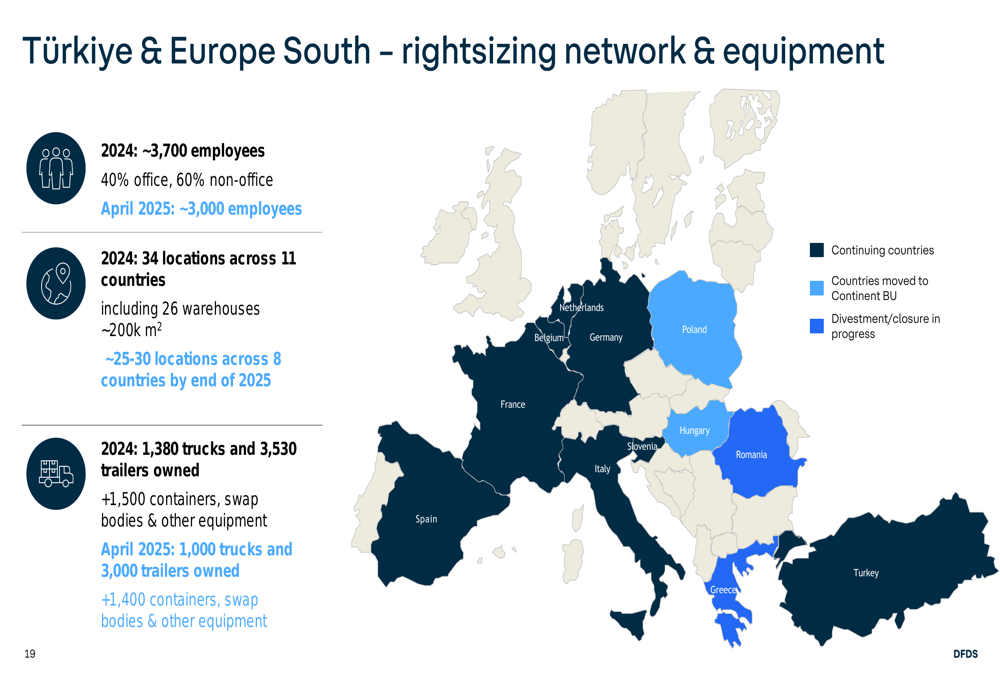

For the underperforming Türkiye & Europe South division, DFDS is implementing a comprehensive restructuring program. This includes reducing headcount from approximately 3,700 to 3,000 employees, consolidating locations from 34 across 11 countries to 25-30 across 8 countries, and downsizing the fleet:

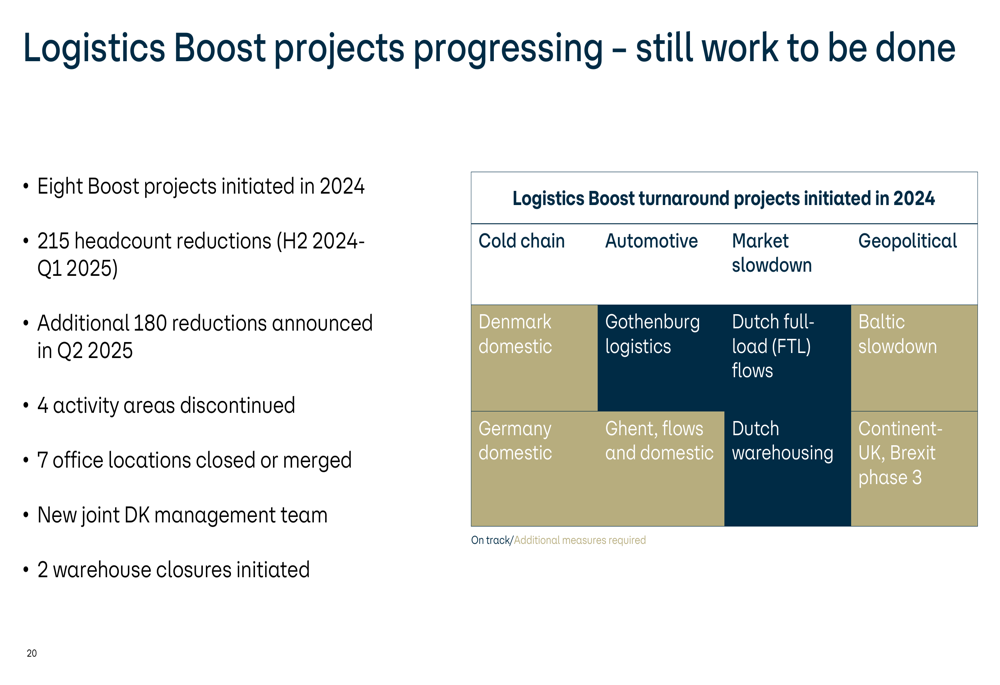

The company is also addressing challenges in its Logistics Division through targeted boost projects, though progress varies across different business areas:

On the sustainability front, DFDS reported a 5.9% reduction in ferry CO2 emission intensity and now operates 136 e-trucks, an increase of 5 from the previous period. The company also improved its safety metrics, with the Lost Time Injury Frequency (LTIF) improving to 4.3, and increased women in management positions by 1 percentage point to 21%.

Forward-Looking Statements

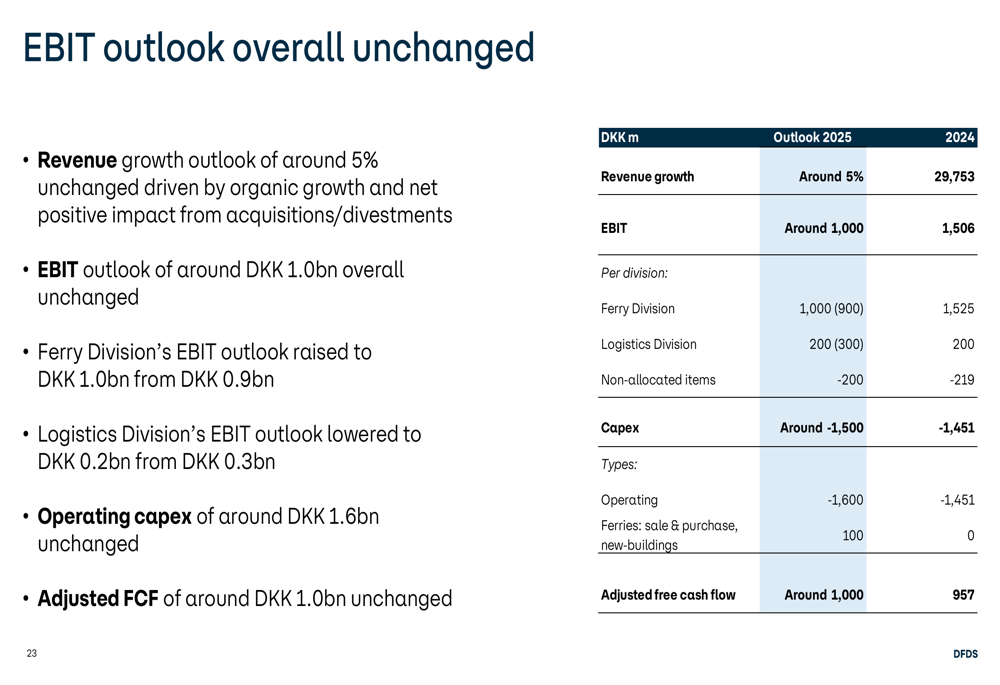

Despite the challenging start to 2025, DFDS maintained its overall outlook for the year. The company expects revenue growth of around 5% and an EBIT of approximately DKK 1.0 billion. Notably, the Ferry Division’s EBIT outlook was raised to DKK 1.0 billion from DKK 0.9 billion, while the Logistics Division’s outlook was lowered to DKK 0.2 billion from DKK 0.3 billion:

CEO Torben Karlsen emphasized that 2025 is "a year where we lay the groundwork for improving financial performance" and expressed confidence in the company’s ability to overcome challenges in the Mediterranean region. Management expects Q2 and Q3 2025 results to remain below 2024 levels, with recovery beginning in Q4 2025.

The company’s key priorities for 2025 include protecting and growing its underlying network strength, focusing on organic growth, executing turnarounds in the three focus areas, reversing cost increase trends, maintaining cash flow discipline, and continuing to deliver on green transition and diversity targets.

With a maintained operating capex target of DKK 1.6 billion and an adjusted free cash flow target of around DKK 1.0 billion, DFDS is balancing investment in future growth with near-term financial stability as it navigates through this transition year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.