IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

DFDS A/S (CPH:DFDS) presented its Q2 2025 results on August 20, 2025, revealing significant challenges in its Mediterranean operations despite achieving modest overall revenue growth. The stock traded at 104.5 DKK, up 1.36% on the day of the presentation, as investors assessed the company’s strategic initiatives to address underperformance in key segments.

The presentation highlighted a complex operating environment characterized by subdued European growth, challenges in Turkish exports due to FX parity issues, and increasing oil price spreads. Competitive pressures have intensified, particularly in the Mediterranean region, where increased ferry capacity has put downward pressure on pricing.

Quarterly Performance Highlights

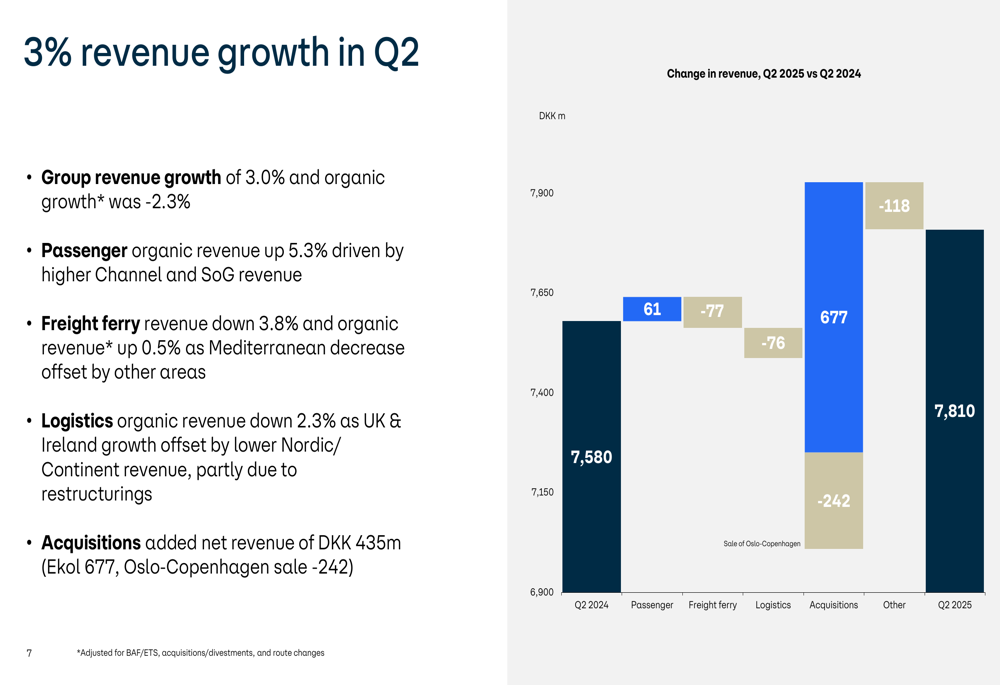

DFDS reported a 3.0% increase in revenue for Q2 2025, reaching 7,810 million DKK, though organic growth was negative at -2.3%. The acquisition of Ekol contributed significantly with 677 million DKK in revenue, offsetting the impact of the Oslo-Copenhagen route sale.

As shown in the following chart of revenue changes by segment:

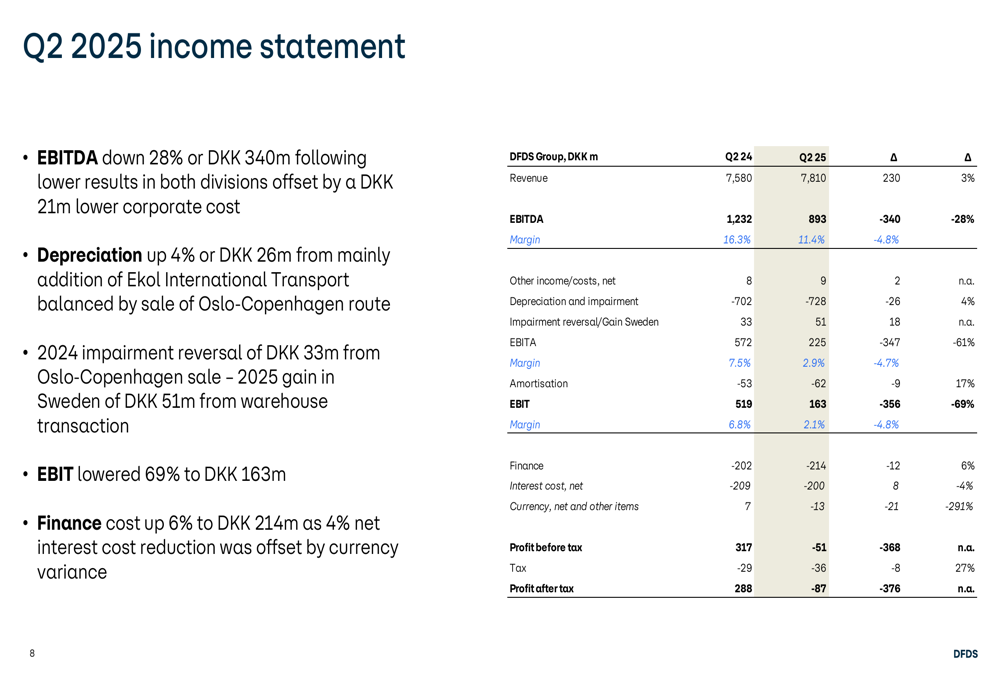

However, profitability metrics showed substantial deterioration. EBITDA decreased by 28% to 893 million DKK, while EBIT fell by 69% to 163 million DKK. The EBITDA margin contracted to 11.4%, and the company reported a loss after tax of 87 million DKK.

The comprehensive income statement reveals the extent of the financial impact:

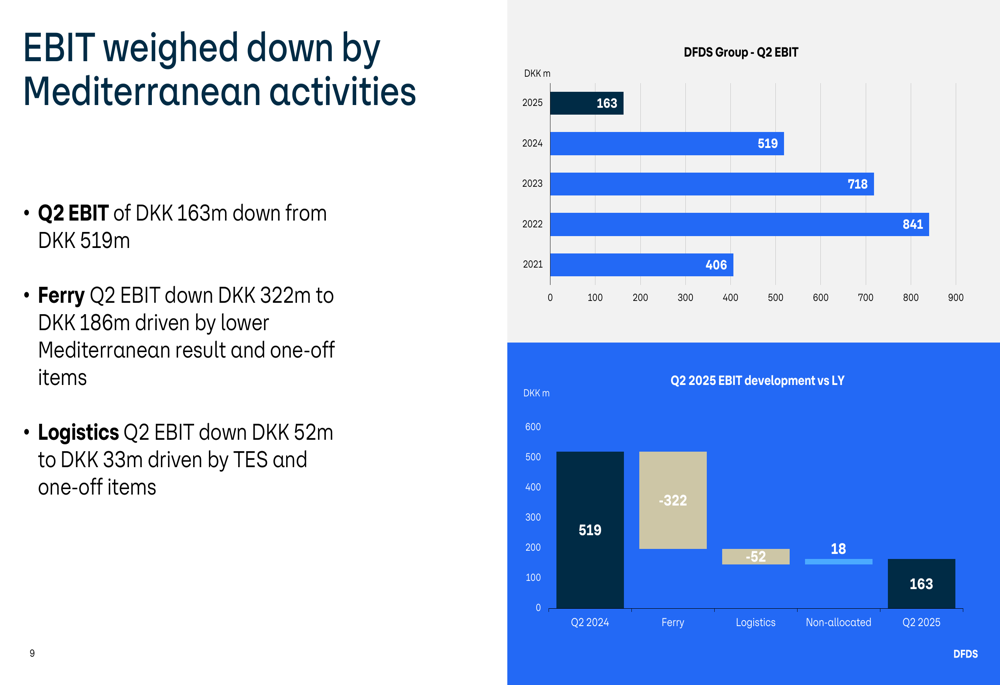

The company’s EBIT was particularly affected by underperformance in Mediterranean operations, as illustrated in this breakdown:

Mediterranean Challenges

The Mediterranean region emerged as the primary source of DFDS’s financial challenges. Ferry Division EBIT decreased by DKK 322 million to DKK 186 million, with Mediterranean results alone accounting for a DKK 181 million decline. This deterioration was attributed to lower pricing amid intensified competition, as three new RoRo ferries entered the Istanbul-Trieste corridor.

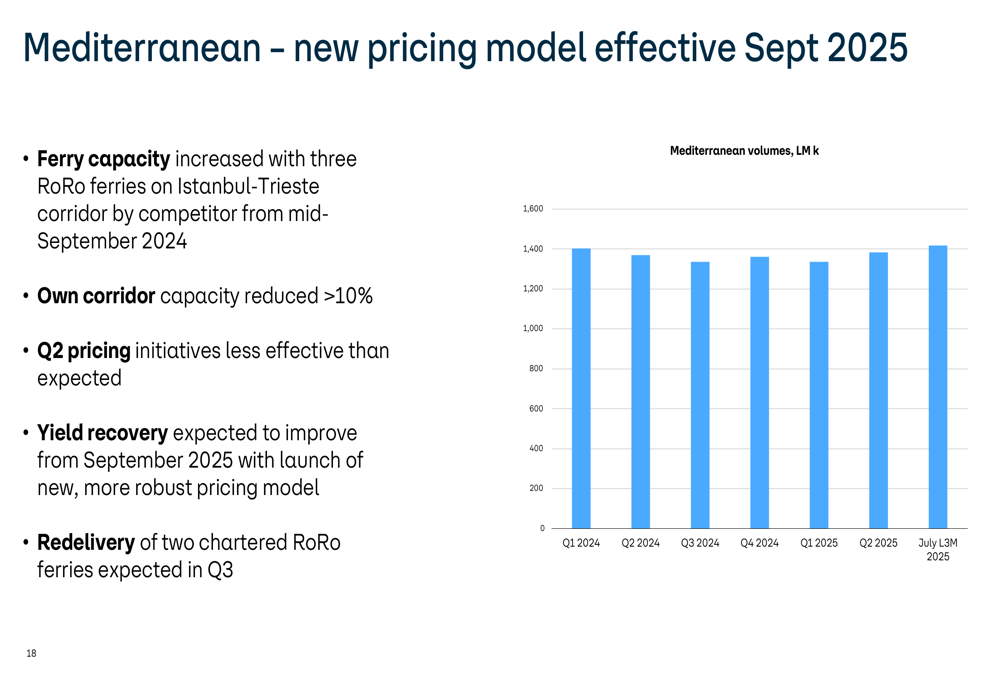

In response, DFDS has reduced its own corridor capacity by more than 10% and plans to redeliver two chartered RoRo ferries in Q3. The company acknowledged that Q2 pricing initiatives were less effective than expected, prompting the development of a new pricing model to be implemented in September 2025.

The following chart illustrates Mediterranean volume trends:

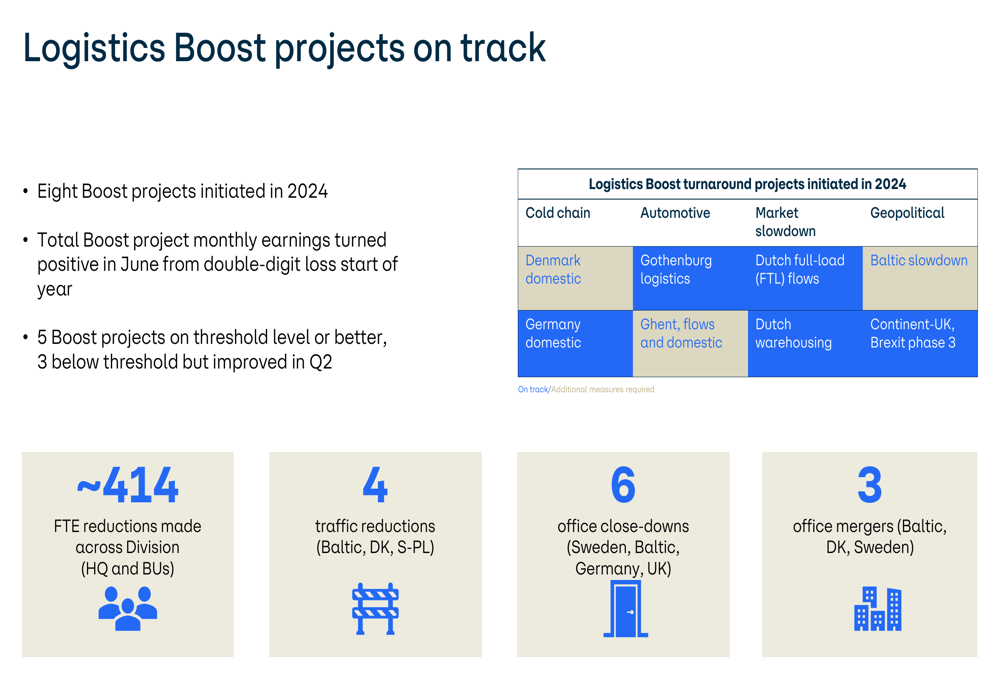

Similarly, the Türkiye & Europe South segment of the Logistics Division faced significant headwinds. The company is implementing a turnaround plan that includes rightsizing equipment, reviewing the customer portfolio, optimizing road/ferry/rail interactions, and restructuring the network. Staff reductions from 3,700 to 2,750 are underway, and three country organizations are scheduled for closure during Q3.

Strategic Initiatives

DFDS outlined three key focus areas for 2025: Logistics Boost projects, adapting Mediterranean operations, and turning around the Türkiye & Europe South segment. The Logistics Boost projects, initiated in 2024, have shown promising results, with five of eight projects meeting or exceeding threshold performance levels.

The company has implemented significant operational changes as part of these initiatives:

For the Mediterranean region, DFDS is developing a new pricing model to improve yield recovery, scheduled for implementation in September 2025. In the Türkiye & Europe South segment, the company is replicating its proven RoRo model from Northern Europe while restructuring operations to address profitability challenges.

Sustainability Progress

Despite financial challenges, DFDS continued to advance its sustainability agenda. Ferry CO2 emission intensity was reduced by 4.1% for the company’s own fleet, primarily through increased biofuel usage on certain routes. The company now operates 145 e-trucks, up from previous quarters.

Safety metrics also improved, with the Lost Time Injury Frequency (LTIF) improving to 5.2 for Q2 2025. Additionally, the percentage of women in management positions increased by 1 percentage point to 21%, reflecting progress on diversity initiatives.

Forward-Looking Statements

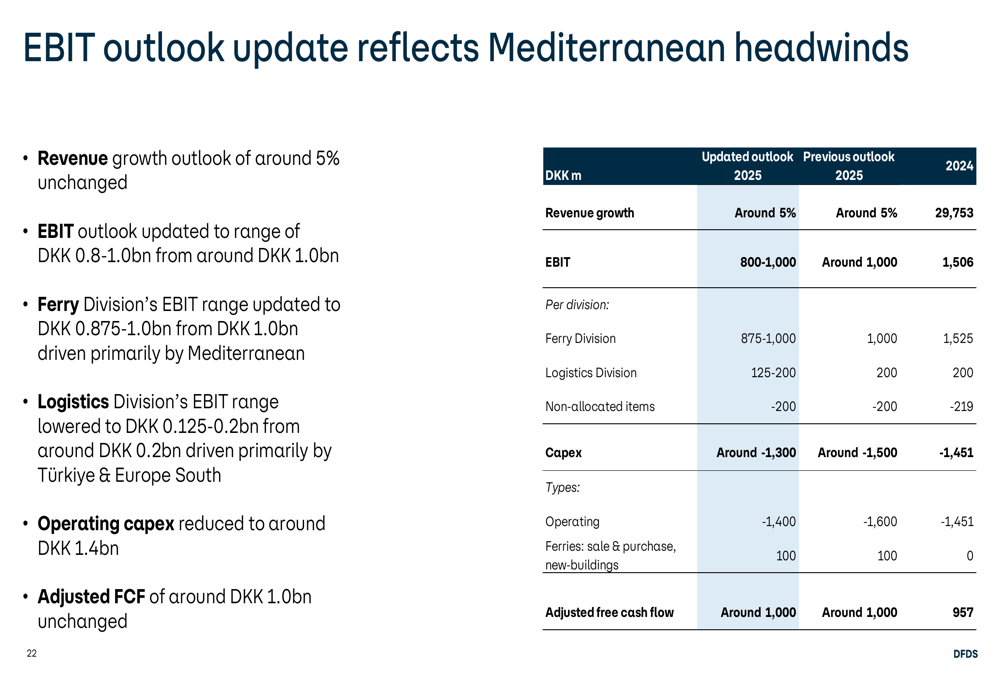

In light of the Mediterranean headwinds, DFDS has revised its financial outlook for 2025. While revenue growth is still expected to be around 5%, the EBIT guidance has been lowered to a range of DKK 800-1,000 million, down from the previous target of around DKK 1,000 million.

The updated guidance reflects the company’s assessment of ongoing challenges and recovery initiatives:

DFDS maintains its focus on organic growth, delivering on the three specific turnaround areas, cost management, cash flow optimization, green transition, and diversity, equity, and inclusion (DEI) initiatives. The company expects its adjusted free cash flow to be around DKK 1,000 million for the year, and anticipates that operations in Türkiye & Europe South will break even by 2026.

Despite near-term challenges, DFDS remains committed to its long-term strategy of unlocking network value, advancing the green transition, and maintaining disciplined cash flow management as it works toward its 2030 goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.