Bitcoin price today: dips below $112k, near 6-wk low despite Fed cut bets

Introduction & Market Context

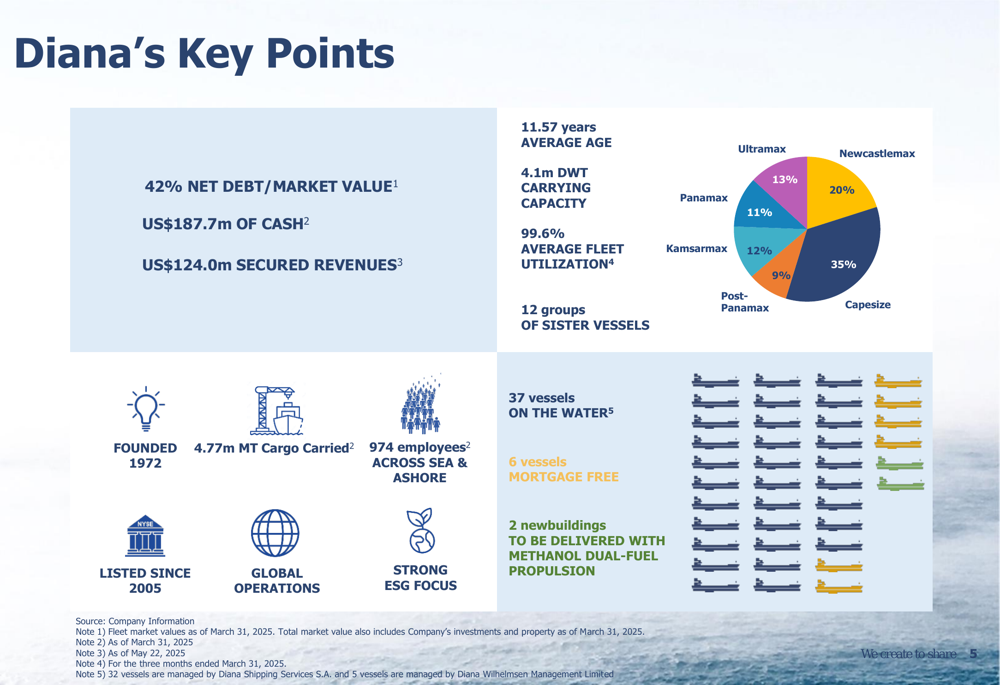

Diana Shipping Inc . (NYSE:DSX) presented its first-quarter 2025 financial results on May 29, 2025, revealing improved profitability despite a revenue decline. The dry bulk shipping company, currently valued at approximately $160 million in market capitalization, reported a 43% increase in net income year-over-year while time charter revenues fell by 5%. Following the announcement, Diana Shipping’s stock price showed a modest gain of 2.52%, trading at $1.22 per share.

The company’s presentation highlighted its strategic positioning in a challenging market environment, emphasizing its conservative chartering approach and strong cash reserves. Diana Shipping, which celebrated its 20-year anniversary of listing on the New York Stock Exchange during the quarter, continues to focus on medium to long-term time charters to provide earnings visibility and strengthen resilience against market fluctuations.

Quarterly Performance Highlights

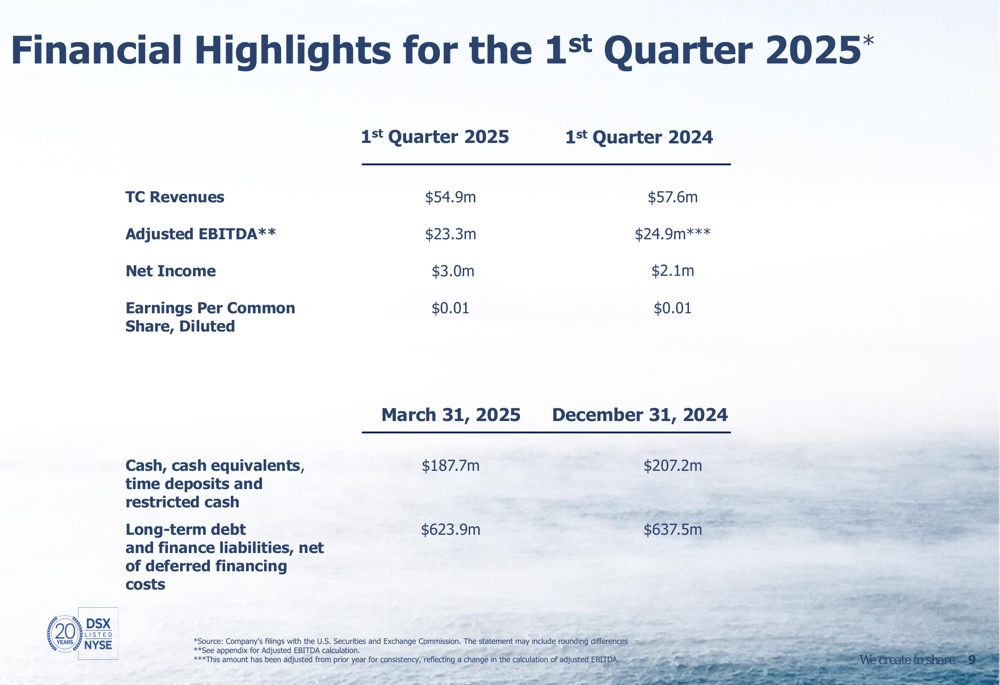

Diana Shipping reported net income of $3.0 million for Q1 2025, up from $2.1 million in the same period last year, while time charter revenues decreased to $54.9 million from $57.6 million. Adjusted EBITDA declined slightly to $23.3 million compared to $24.9 million in Q1 2024. The company maintained its earnings per share at $0.01, unchanged from the previous year.

As shown in the following financial highlights chart:

Fleet utilization improved to 99.6% in Q1 2025 from 99.1% in Q1 2024, while the time charter equivalent (TCE) rate increased to $15,739 from $15,051 year-over-year. The company operated an average of 37.8 vessels during the quarter, down from 39.7 vessels in Q1 2024, reflecting its strategic fleet optimization efforts.

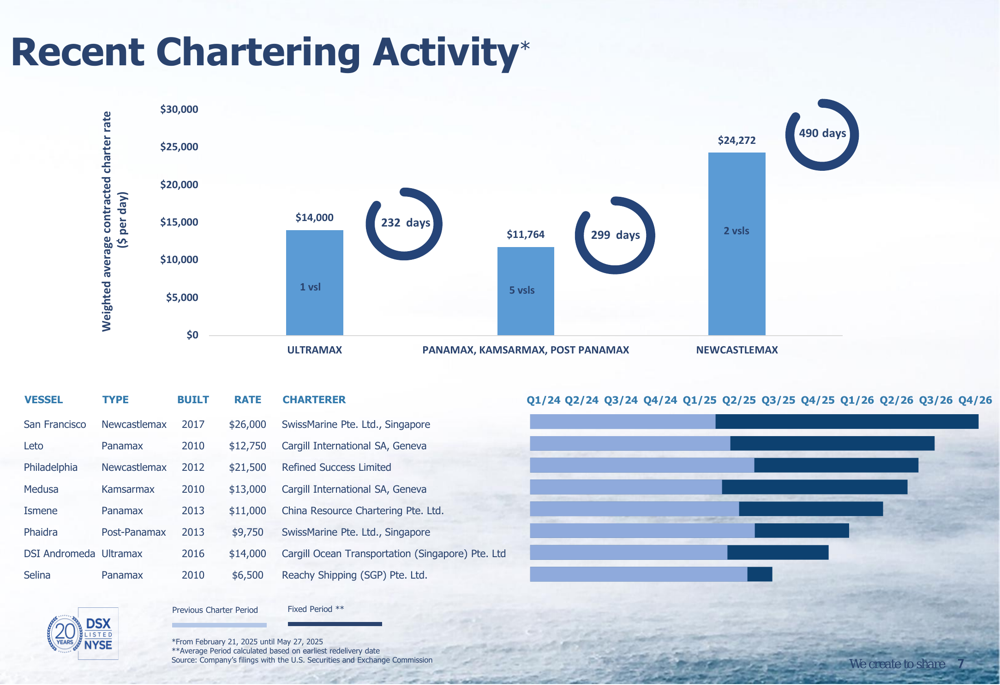

Diana Shipping’s chartering activity remains focused on securing stable income streams. The company has secured $86.8 million in contracted revenues for 66% of its remaining ownership days in 2025 and $36.5 million for 13% of ownership days in 2026. The weighted average contracted charter rates vary significantly by vessel type, with Newcastlemax vessels commanding the highest rates at $24,272 per day.

The following chart illustrates the company’s recent chartering activity by vessel type:

Detailed Financial Analysis

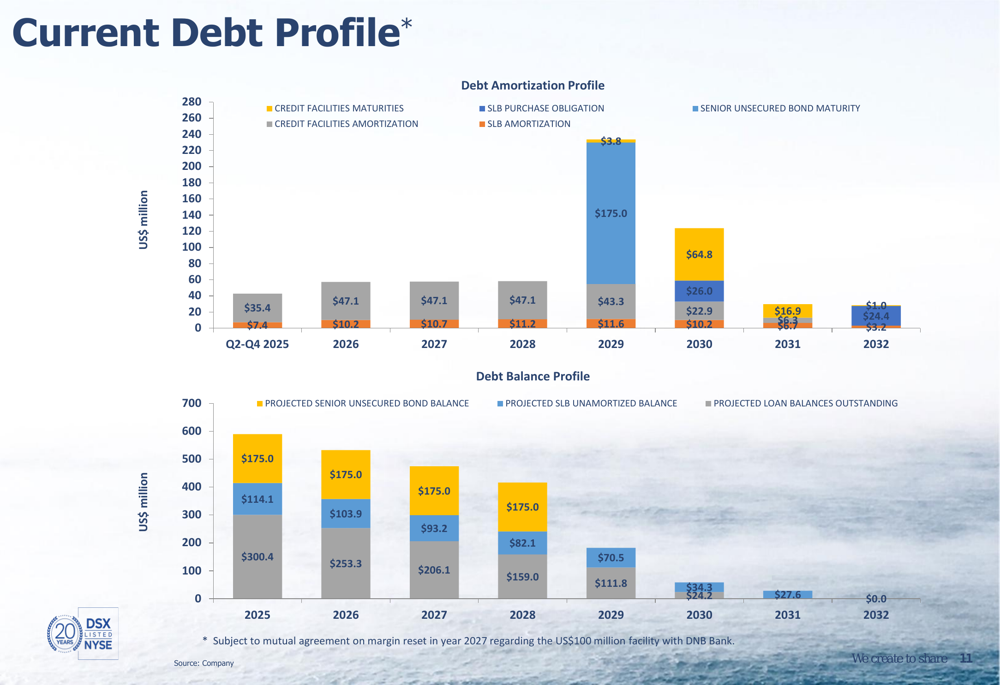

Diana Shipping maintained a strong financial position with $187.7 million in cash, cash equivalents, time deposits, and restricted cash as of March 31, 2025, though this represents a decrease from $207.2 million at the end of 2024. The company’s long-term debt and finance liabilities stood at $623.9 million, down from $637.5 million at year-end 2024.

The company’s debt profile shows a well-structured amortization schedule extending through 2032, with manageable maturities in the coming years. This provides financial flexibility as the company navigates market uncertainties.

The following chart details Diana Shipping’s current debt profile:

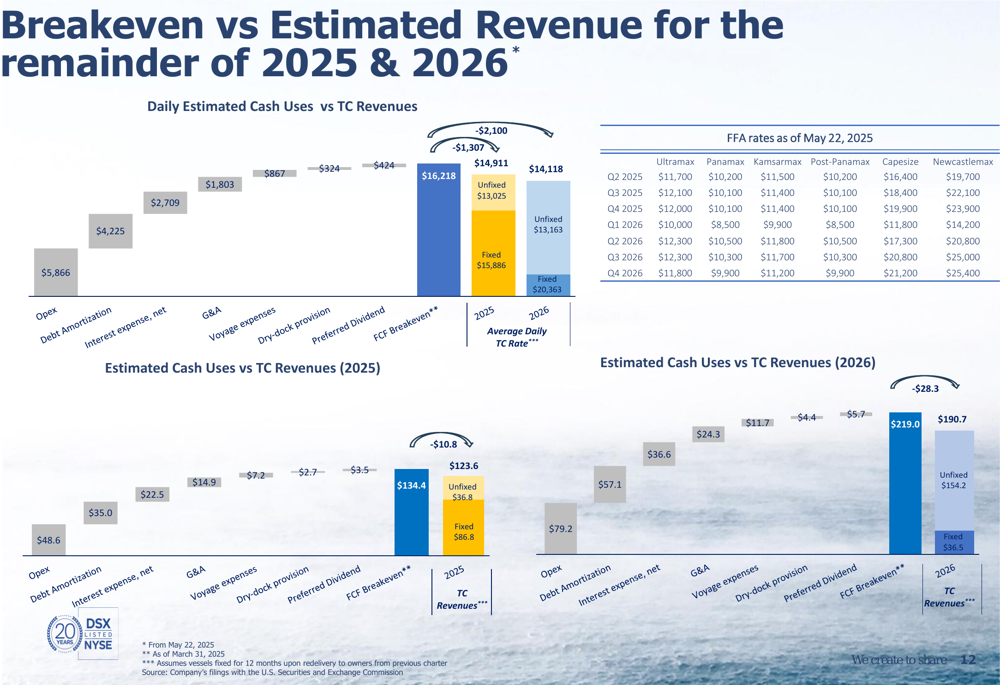

Diana Shipping’s breakeven analysis reveals a daily cash requirement of approximately $16,218 for the remainder of 2025, covered by fixed time charter revenues of $15,886 per day for 66% of remaining ownership days. For 2026, the company has secured higher fixed rates of $20,363 per day for 13% of ownership days, providing some visibility into future earnings.

The company’s breakeven versus estimated revenue is illustrated in this chart:

Diana Shipping declared a cash dividend of $0.01 per common share for Q1 2025, continuing its consistent dividend policy. Since 2021, the company has paid cumulative dividends of $2.670 per common share, including both cash dividends and dividends in kind.

Strategic Initiatives

Diana Shipping continues to implement its fleet renewal strategy, selling the m/v Alcmene for approximately $11.9 million during the quarter. The company currently operates 37 vessels on the water, of which six are mortgage-free, with an average fleet age of 11.57 years.

In a strategic diversification move, Diana Shipping has become a partner in two 7,500 cbm semi-refrigerated LPG newbuildings, with an option for two additional vessels. The company has also ordered two newbuildings with methanol dual-fuel propulsion, reflecting its commitment to reducing its environmental footprint.

The company’s key metrics are summarized in the following overview:

Diana Shipping successfully raised $25.6 million from the exercise of warrants during the period, with potential to raise an additional $64.9 million. This capital strengthens the company’s position for future investments and fleet modernization efforts.

The company maintains relationships with reputable charterers in the industry, enhancing its market position and stability:

Forward-Looking Statements

Diana Shipping’s presentation outlined both positive and negative factors affecting the dry bulk shipping industry. Positive factors include a strong Brazilian soybean crop, commencement of iron ore shipments from Simandou, and potential resolution of conflicts affecting shipping routes. Negative factors include worldwide lower steel production, protectionist measures with high tariffs, and bulk carrier fleet growth outpacing demand growth.

The dry bulk market faces challenges from weaker global GDP growth, with expected 2025 rates of 4.0% for China, 0.8% for the United States, and 1.8% for the world economy. The company noted that most major dry bulk commodity shipments are expected to either remain steady or decline somewhat in the near term.

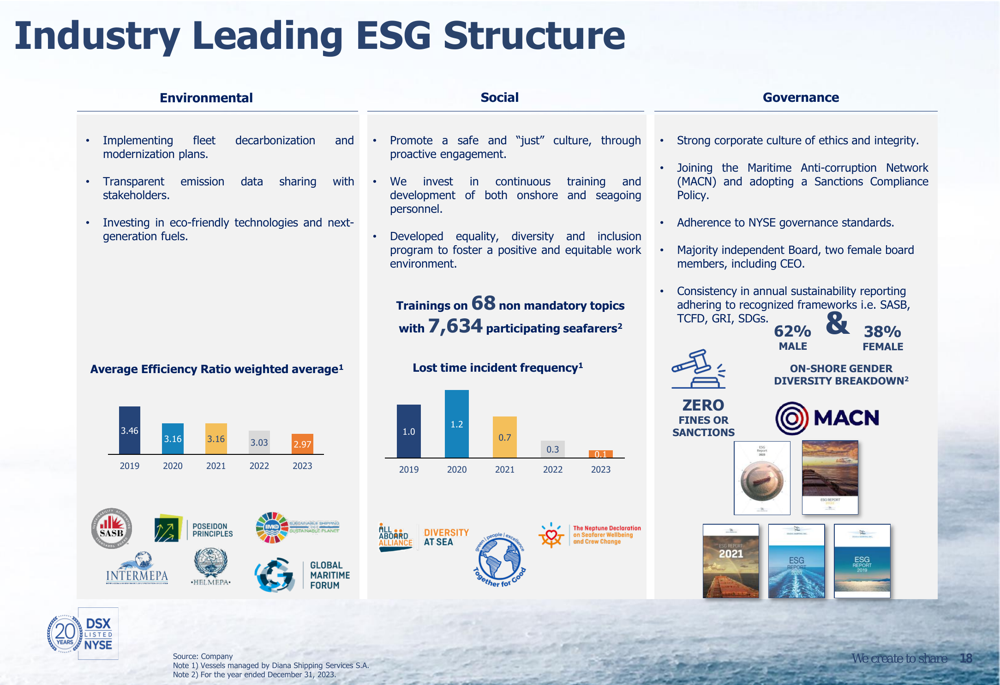

Diana Shipping continues to emphasize its ESG initiatives, implementing fleet decarbonization plans and investing in eco-friendly technologies. The company has improved its Average Efficiency Ratio from 3.46 in 2019 to 2.97 in 2023, while reducing its Lost Time Incident Frequency from 1.2 to 0.1 over the same period.

The company’s ESG performance is highlighted in this summary:

Competitive Industry Position

Diana Shipping positions itself as a leading pure-play dry bulk carrier company with a legacy dating back to 1972. The company’s fleet consists of diverse vessel types, including Ultramax (13%), Newcastlemax (20%), Panamax (11%), Kamsarmax (12%), Capesize (35%), and Post Panamax (9%).

The company’s disciplined and non-speculative chartering strategy, focusing on medium to long-term time charters, provides earnings visibility and strengthens resilience to market downturns. This approach has secured $124.0 million in revenues as of May 22, 2025.

Diana Shipping summarizes its competitive advantages in this overview:

The dry bulk orderbook currently stands at 10.3% of the existing fleet, suggesting moderate fleet growth in the coming years. This relatively contained orderbook, combined with Diana Shipping’s strategic positioning and strong cash reserves, may provide opportunities for the company to capitalize on potential market improvements despite current challenges.

In conclusion, Diana Shipping’s Q1 2025 results reflect a company effectively navigating a complex market landscape while making strategic investments for future growth. Despite revenue challenges, the company’s improved profitability, high fleet utilization, and secured future revenues position it to weather market uncertainties while maintaining shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.