US stock futures dip as Trump’s firing of Cook sparks Fed independence fears

Diebold Nixdorf Inc (NYSE:DBD) presented its first quarter 2025 earnings results on May 7, showing a mixed performance with declining revenue but improving margins and a growing order backlog. The company’s stock was down 2.32% in premarket trading to $44.20, reflecting investor concerns despite management’s positive outlook.

Quarterly Performance Highlights

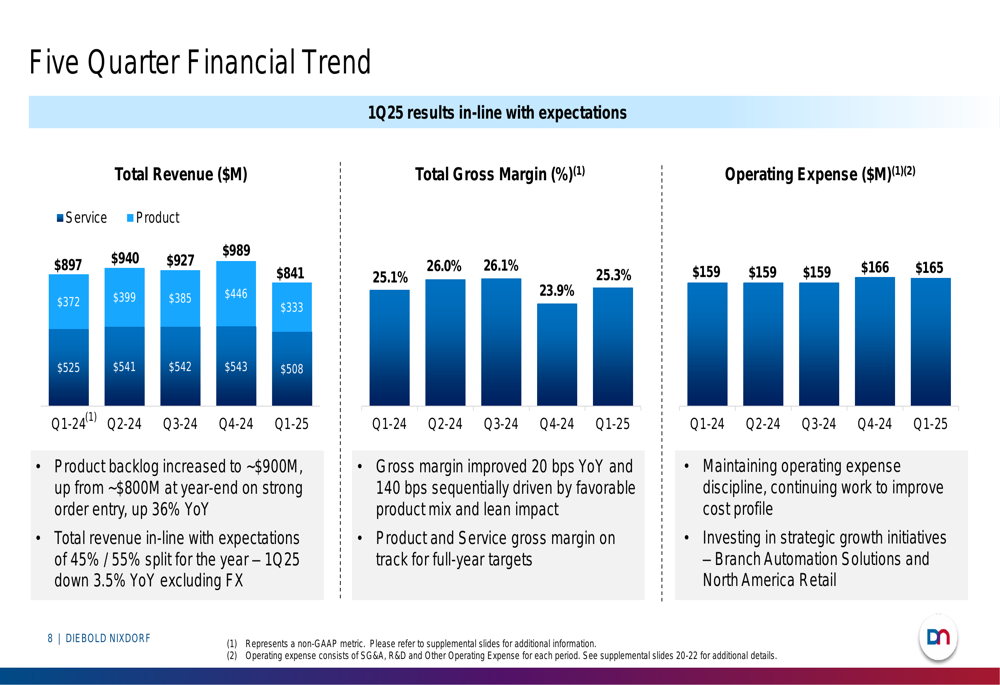

Diebold Nixdorf (OTC:DBDQQ) reported Q1 2025 revenue of $841 million, down 3.5% year-over-year excluding foreign exchange effects. Despite the revenue decline, the company highlighted several positive developments, including gross margin improvement of 20 basis points year-over-year and 140 basis points sequentially to 25.3%, driven by favorable product mix and the impact of lean initiatives.

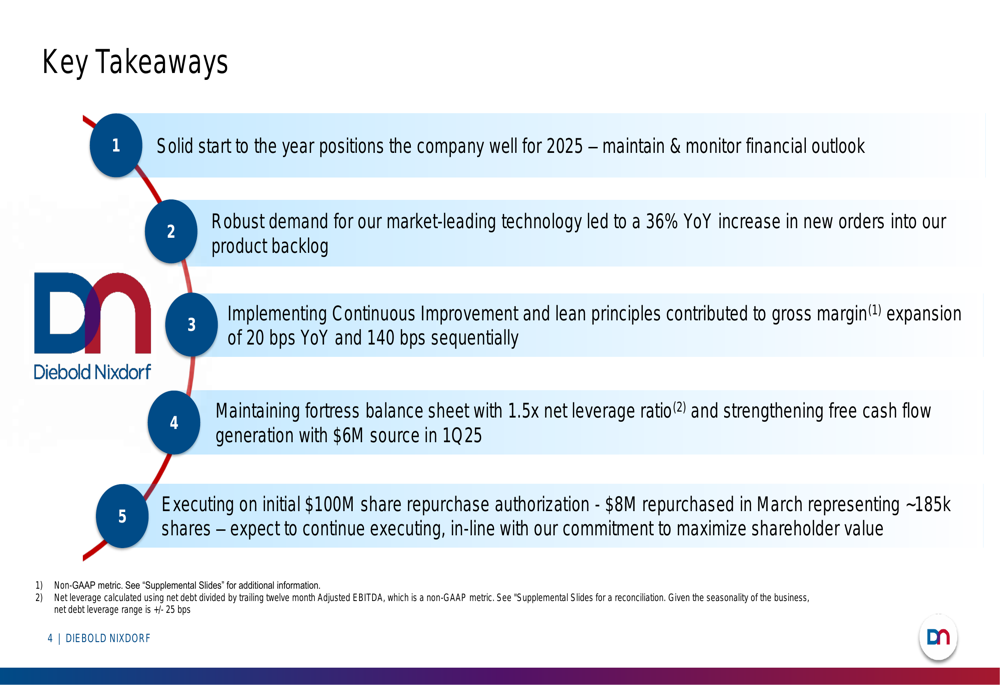

As shown in the following key takeaways slide, the company saw robust demand for its technology, with new orders into product backlog increasing 36% year-over-year:

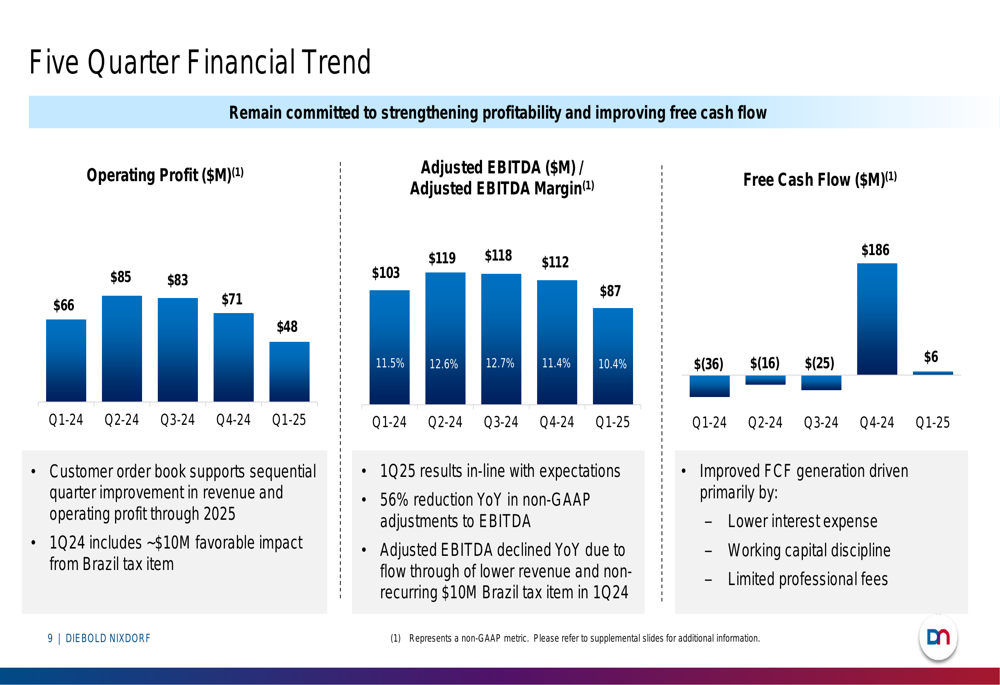

The company’s product backlog increased to approximately $900 million, up from $800 million at year-end, providing visibility for future revenue. Adjusted EBITDA for the quarter was $87 million with a 10.4% margin, down from $103 million and 11.5% in Q1 2024, primarily due to lower revenue and a non-recurring $10 million Brazil tax item that benefited the prior-year period.

The following chart illustrates the five-quarter financial trend for revenue, gross margin, and operating expenses:

Segment Performance Analysis

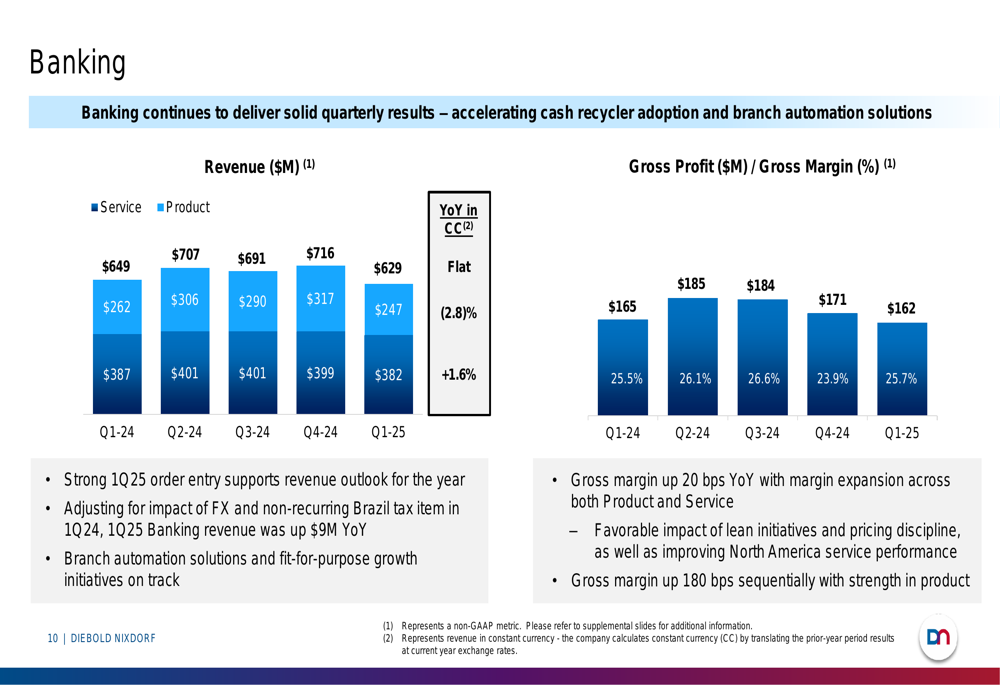

The Banking segment, which represents approximately 75% of total revenue, reported Q1 2025 revenue of $629 million, flat year-over-year in constant currency. Service revenue within Banking grew 1.6% while Product revenue declined 2.8%. Gross profit for the segment was $162 million with a margin of 25.7%, up 20 basis points year-over-year and 180 basis points sequentially.

The following slide details the Banking segment’s performance over the past five quarters:

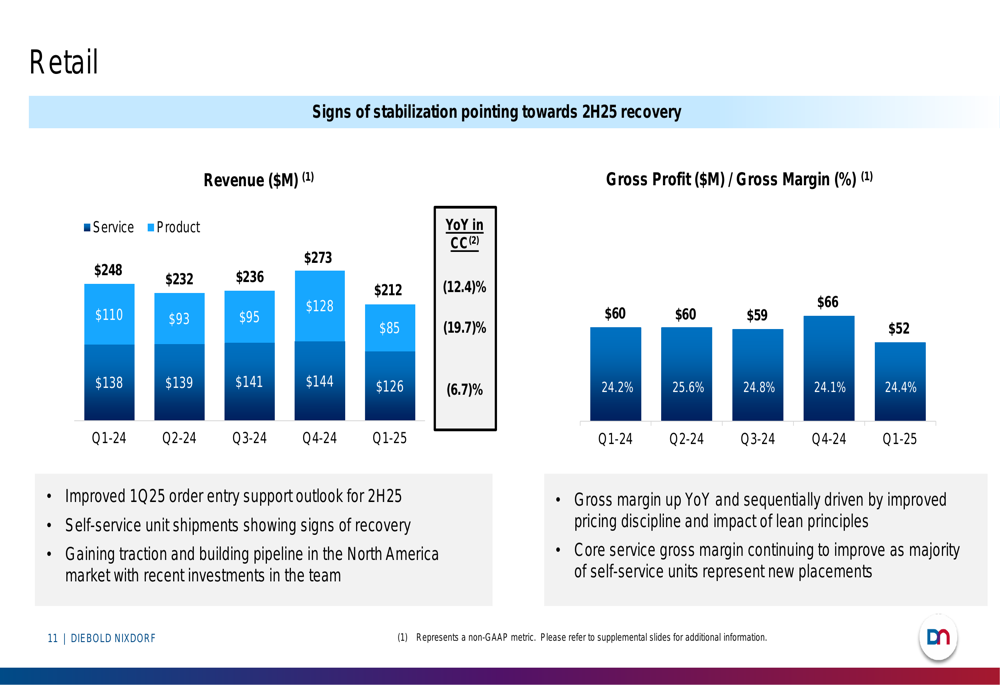

The Retail segment faced more significant challenges, with Q1 2025 revenue of $212 million, down 12.4% year-over-year in constant currency. Service revenue declined 6.7% and Product revenue fell 19.7%. Despite these challenges, gross margin improved to 24.4%, up from 24.2% in Q1 2024, driven by improved pricing discipline and lean principles implementation.

The Retail segment’s five-quarter performance is illustrated in this chart:

Balance Sheet and Cash Flow

One of the most notable improvements in Q1 2025 was the company’s free cash flow, which turned positive at $6 million compared to a use of $36 million in Q1 2024. This improvement was driven by lower interest expense, working capital discipline, and reduced professional fees.

The following chart shows the five-quarter trend in profitability and cash flow metrics:

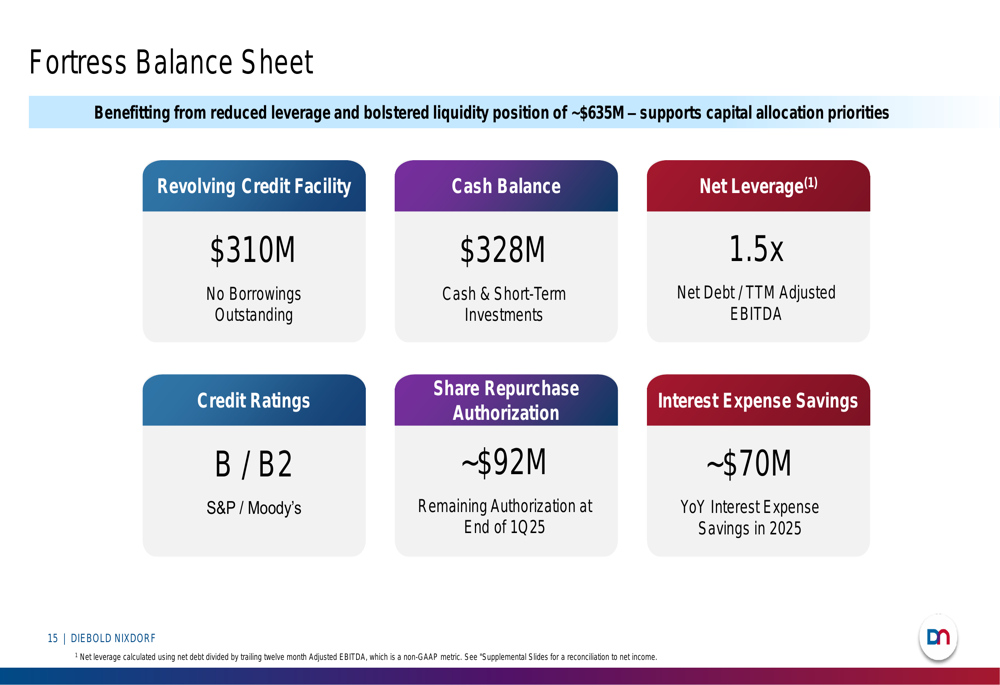

Diebold Nixdorf emphasized its "fortress balance sheet" with a net leverage ratio of 1.5x, cash and short-term investments of $328 million, and no borrowings outstanding on its $310 million revolving credit facility. The company also highlighted its ongoing share repurchase program, with $8 million repurchased in March representing approximately 185,000 shares, and approximately $92 million remaining in the authorization at the end of Q1.

The key balance sheet metrics are summarized in this slide:

2025 Outlook and Guidance

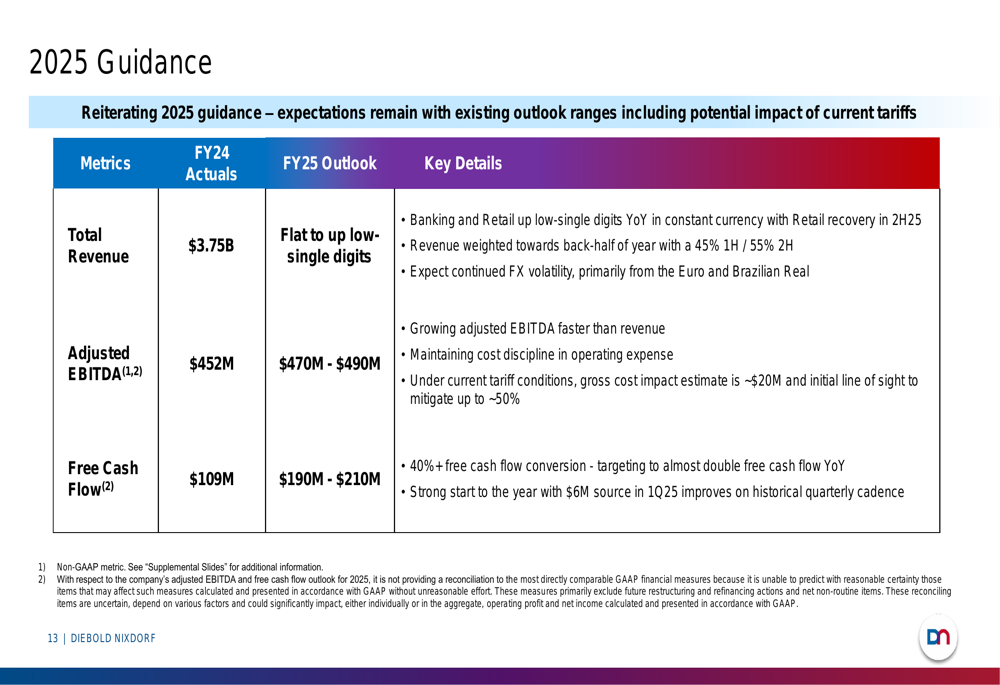

Diebold Nixdorf reiterated its 2025 guidance, projecting flat to low-single-digit revenue growth, with adjusted EBITDA of $470-490 million and free cash flow of $190-210 million. The company expects revenue to be weighted toward the second half of the year, with a 45%/55% split between the first and second halves.

A significant concern highlighted in the presentation is the potential impact of tariff policies, with an estimated gross cost impact of approximately $20 million under current conditions. Management outlined mitigation strategies that could offset up to 50% of this impact, including accelerated productivity efforts, sourcing alternative parts, supplier renegotiation, and price adjustments.

The following slide details the company’s 2025 guidance:

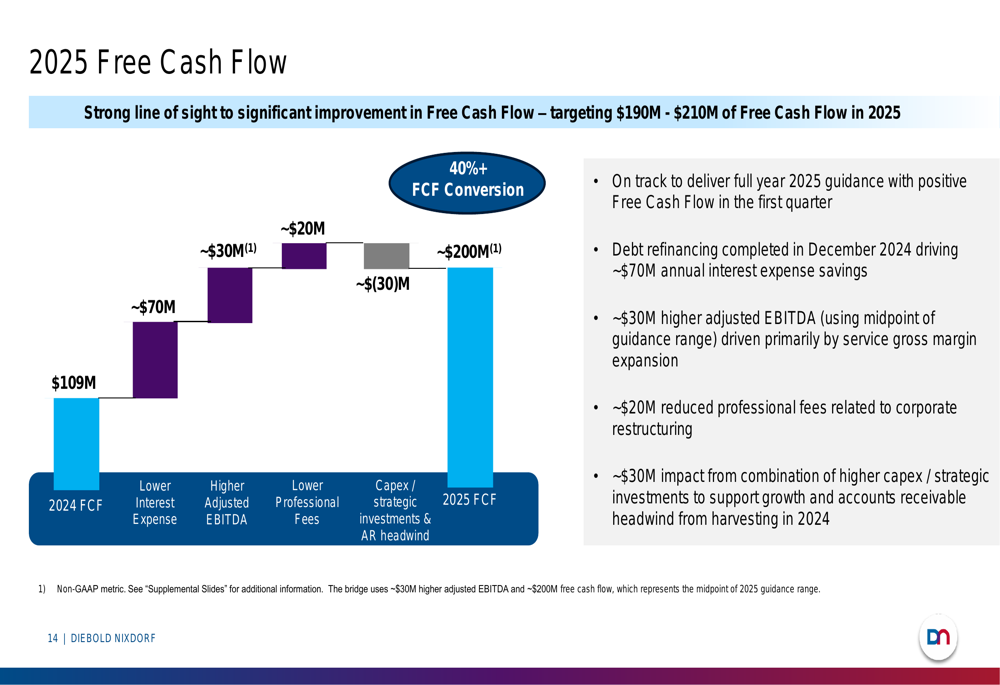

The company expects to nearly double its free cash flow in 2025 compared to 2024, with the improvement primarily driven by lower interest expense (+$70 million) from debt refinancing completed in December 2024, higher adjusted EBITDA (+$30 million), and reduced professional fees (+$20 million). These positive factors are partially offset by higher capex/strategic investments and accounts receivable headwinds (-$30 million).

This waterfall chart illustrates the drivers of free cash flow improvement expected in 2025:

Strategic Initiatives and Challenges

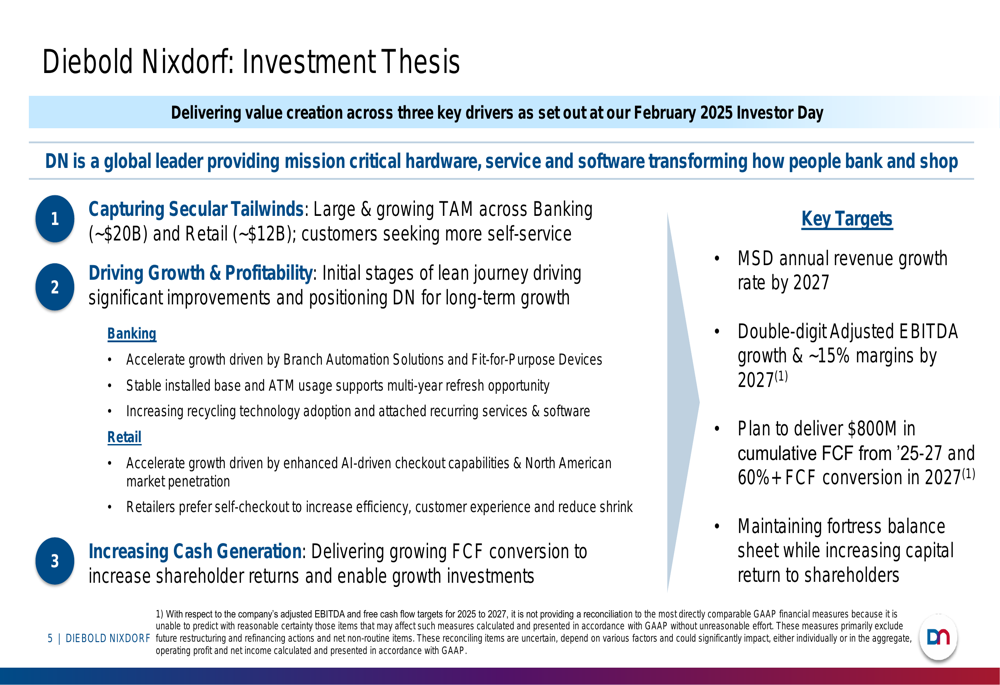

Diebold Nixdorf outlined its investment thesis centered on three key drivers: capturing secular tailwinds in large addressable markets (Banking ~$20 billion, Retail ~$12 billion), driving growth and profitability through lean initiatives, and increasing cash generation to enhance shareholder returns and enable growth investments.

The company’s long-term targets include mid-single-digit annual revenue growth by 2027, double-digit adjusted EBITDA growth with margins reaching approximately 15% by 2027, and delivering $800 million in cumulative free cash flow from 2025-2027.

The following slide summarizes the company’s investment thesis and long-term targets:

Management highlighted progress on its growth strategy, including developing a strong customer pipeline for teller cash recycling in Banking, conducting live pilots and proof-of-concept deployments for Vynamic Smart Vision in Retail, and implementing lean principles across manufacturing and service operations to drive margin expansion.

While the company faces challenges, particularly in the Retail segment and with potential tariff impacts, management expressed confidence in its ability to execute its strategy and deliver on its financial targets for 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.