Evercore picks Astera and MACOM as top AI connectivity stocks

Introduction & Market Context

Discover Financial Services (NYSE:DFS) reported strong first-quarter 2025 financial results on April 23, with net income rising 30% year-over-year as the company prepares to finalize its merger with Capital One (NYSE:COF). The credit card issuer and financial services provider saw its stock rise 3.69% to close at $178.69 on the day of the announcement, though it retreated slightly in after-hours trading.

The company’s solid performance comes as it enters the final stages of its acquisition by Capital One, with the merger expected to close on May 18, 2025, after securing all necessary regulatory and shareholder approvals.

Quarterly Performance Highlights

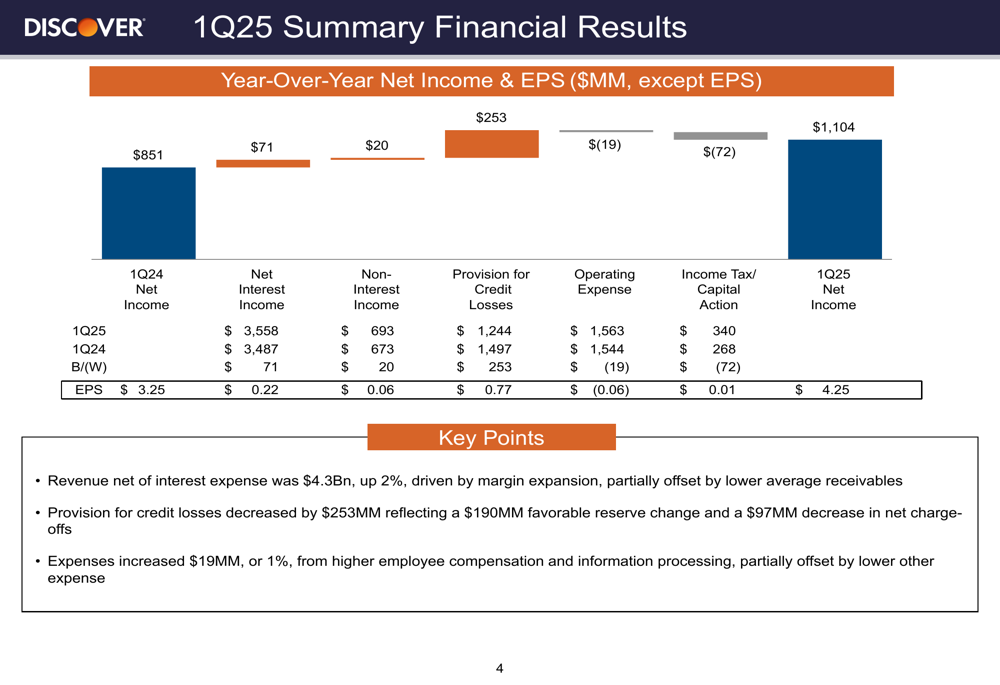

Discover reported net income of $1.1 billion for Q1 2025, up from $851 million in the same period last year. Diluted earnings per share reached $4.25, compared to $3.25 in Q1 2024, representing a 31% increase. Return on equity stood at an impressive 24%.

Total (EPA:TTEF) revenue net of interest expense increased 2% year-over-year to $4.3 billion, driven primarily by margin expansion rather than loan growth.

As shown in the following comprehensive financial comparison:

Net interest income rose to $3.56 billion, up from $3.49 billion in Q1 2024, while non-interest income increased slightly to $693 million from $673 million. The provision for credit losses decreased significantly by $253 million to $1.24 billion, reflecting improved credit performance. Operating expenses saw a modest 1% increase to $1.56 billion.

Detailed Financial Analysis

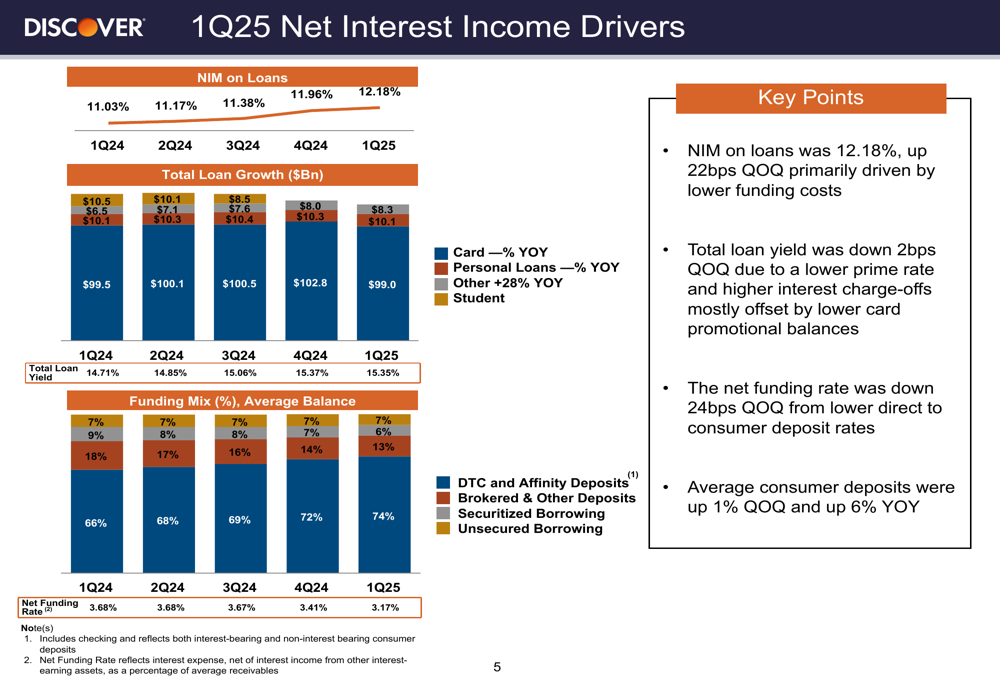

Discover’s net interest margin (NIM) on loans expanded substantially, reaching 12.18% in Q1 2025 compared to 11.03% in Q1 2024. This margin improvement helped offset relatively flat loan growth, with total loans slightly decreasing from $99.5 billion to $99.0 billion year-over-year.

The following chart illustrates the drivers behind Discover’s net interest income performance:

The company’s funding costs improved, with the net funding rate decreasing from 3.68% in Q1 2024 to 3.17% in Q1 2025. Average consumer deposits grew by 6% year-over-year and 1% quarter-over-quarter, providing stable funding for the company’s operations.

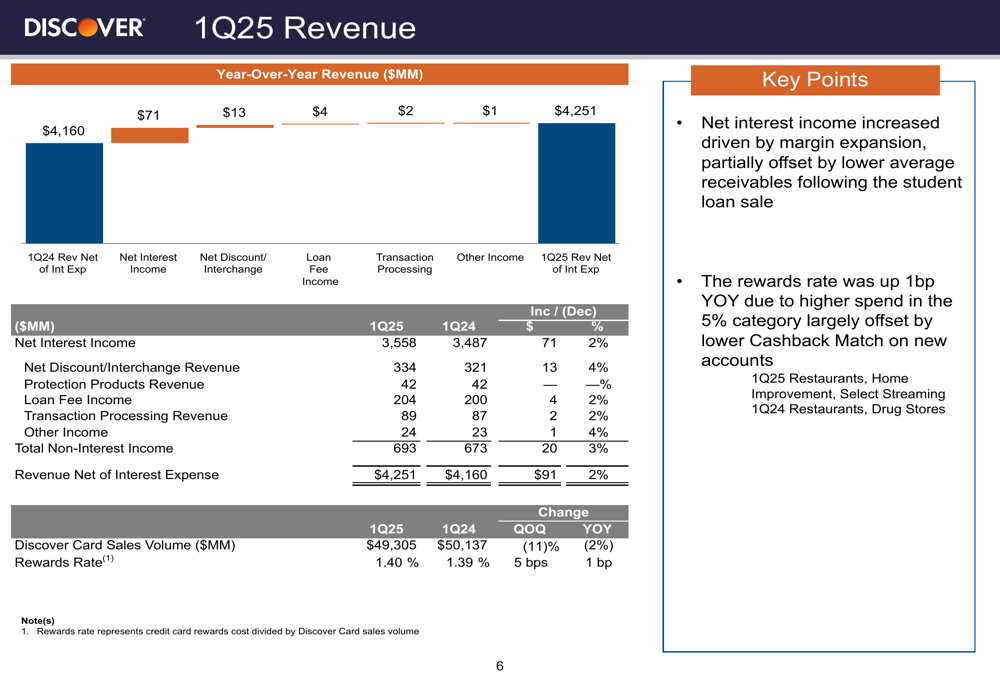

Revenue details show a slight decrease in Discover card sales volume, which fell from $50.1 billion in Q1 2024 to $49.3 billion in Q1 2025, while the rewards rate remained relatively stable at 1.40%:

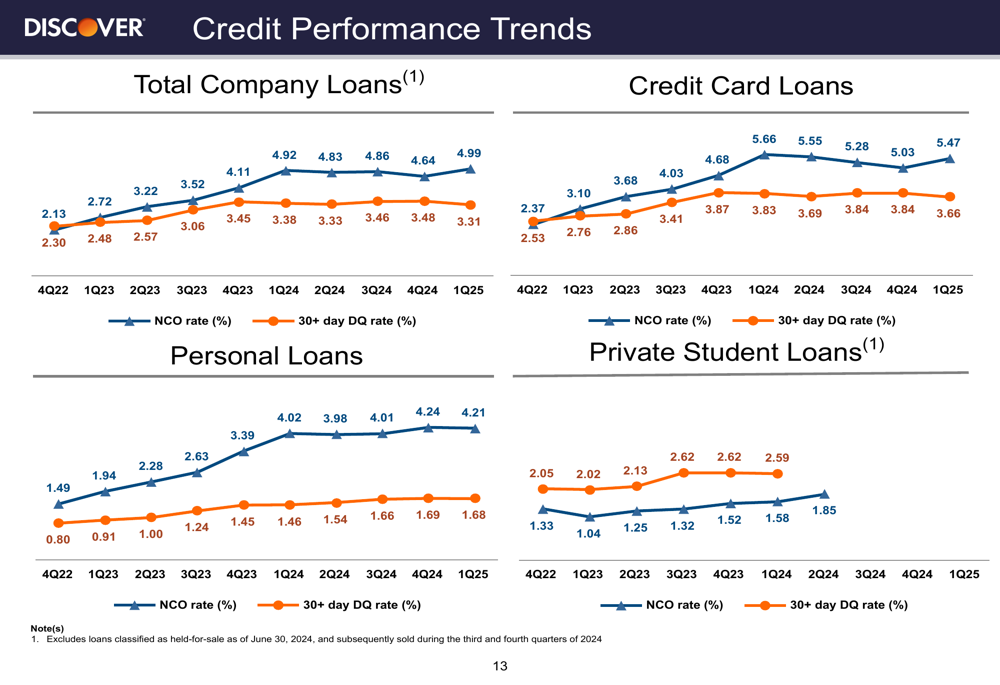

Credit Performance

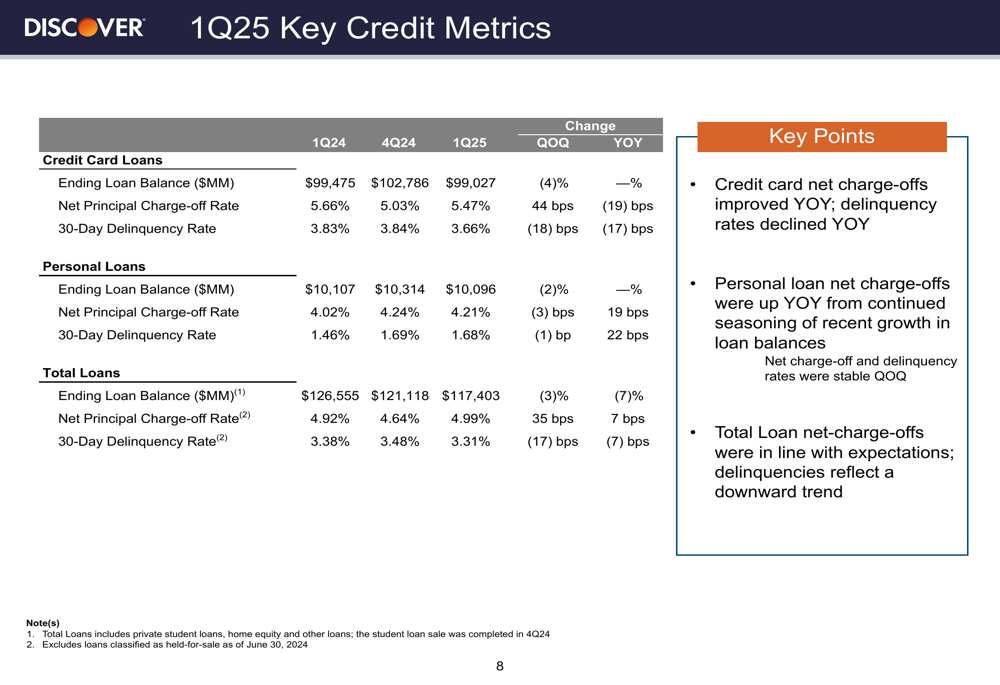

Discover reported improved credit metrics in the first quarter, with credit card net principal charge-offs decreasing to 5.47% and the 30-day delinquency rate at 3.66%. The total loan net principal charge-off rate stood at 4.99%, with a 30-day delinquency rate of 3.31%.

The following table provides a detailed breakdown of credit metrics across Discover’s loan portfolio:

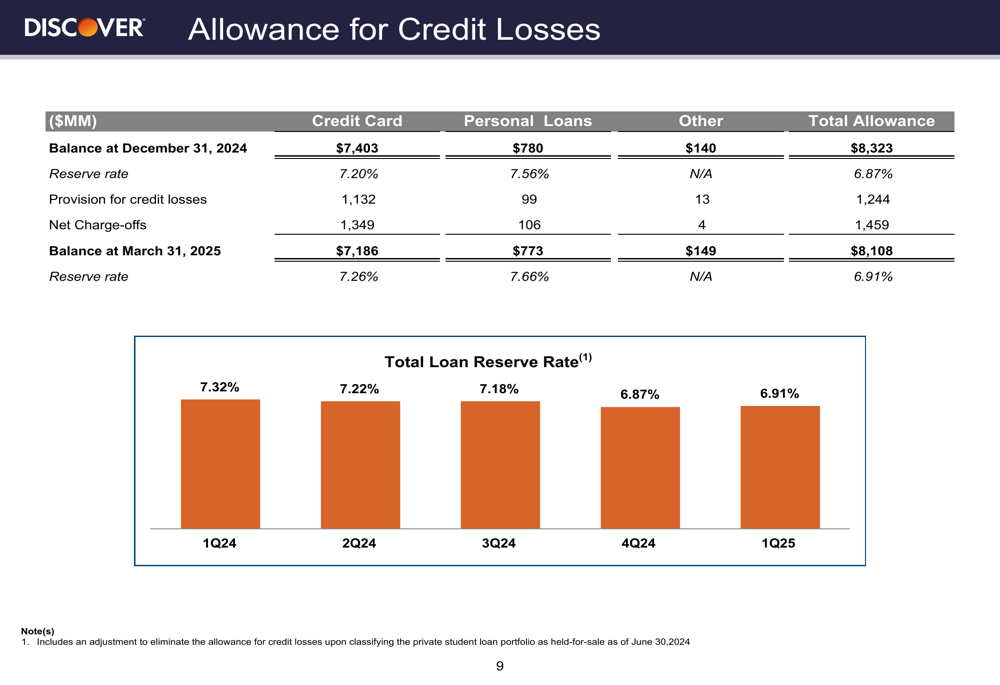

The company’s allowance for credit losses totaled $8.11 billion at the end of Q1 2025, with the total loan reserve rate decreasing to 6.91%. This reduction in reserves contributed positively to the company’s earnings for the quarter.

As illustrated in this chart showing the allowance for credit losses:

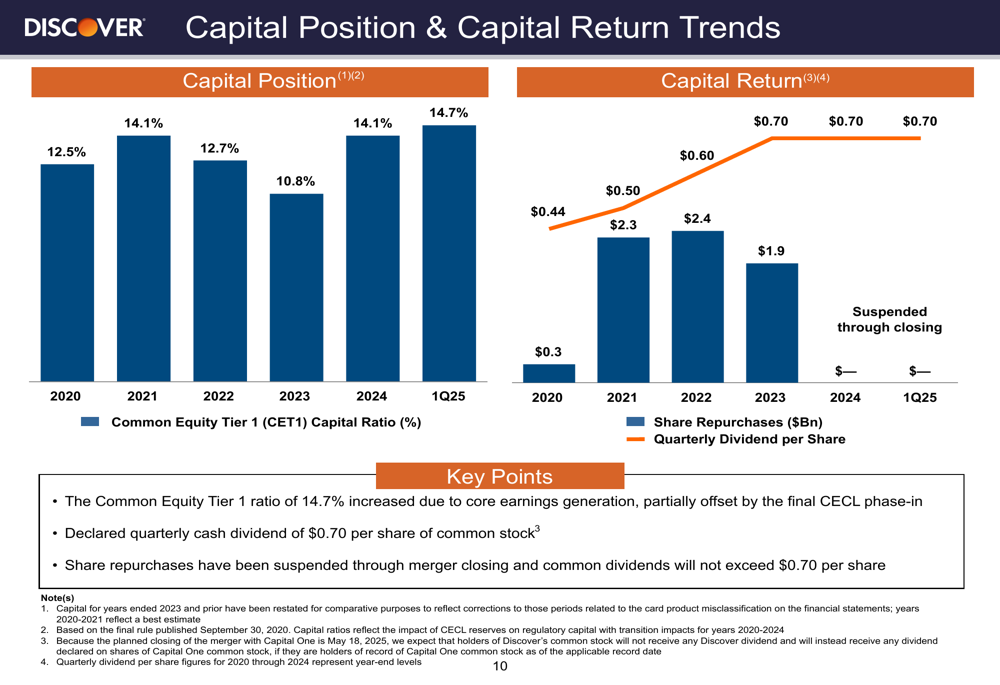

Capital Position & Dividend

Discover maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 14.7% in Q1 2025. The company declared a quarterly cash dividend of $0.70 per share of common stock but has suspended share repurchases in anticipation of the Capital One merger.

The following chart illustrates Discover’s capital position and capital return trends:

Capital One Merger Update

A significant highlight from the presentation was the progress of Discover’s pending merger with Capital One. The company secured all necessary approvals, including shareholder approval with 99.3% of votes in favor and regulatory approval from both the Federal Reserve and the Office of the Comptroller of the Currency (OCC).

The expected closing date for the merger is May 18, 2025, contingent on satisfying customary closing conditions. This timeline aligns with previous guidance and suggests the integration is proceeding as planned.

Forward-Looking Statements

While Discover’s presentation did not provide specific forward-looking guidance for the remainder of 2025, the company noted that business is being managed prudently with stable customer trends and active economic monitoring. Management emphasized the solid financial performance driven by revenue growth from margin expansion and good credit performance.

The imminent merger with Capital One will likely dominate Discover’s strategic direction in the coming quarters, with integration efforts and potential synergies becoming key focus areas for investors.

Credit performance trends, as shown in the following graphs, will remain an important indicator to watch as the company navigates the current economic environment:

Discover’s Q1 2025 results demonstrate the company’s ability to maintain profitability and manage credit effectively while preparing for a significant corporate transition. With the Capital One merger expected to close next month, investors will be closely watching how the combined entity positions itself in the competitive financial services landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.