ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

DOF Group ASA (OB:DOFG) presented its Q1 2025 results on May 16, 2025, showcasing strong financial performance amid favorable market conditions in the offshore services sector. The company’s stock closed at 87 NOK on May 15, down 1.58% ahead of the results announcement, with the share price trading within its 52-week range of 71.85 to 115 NOK.

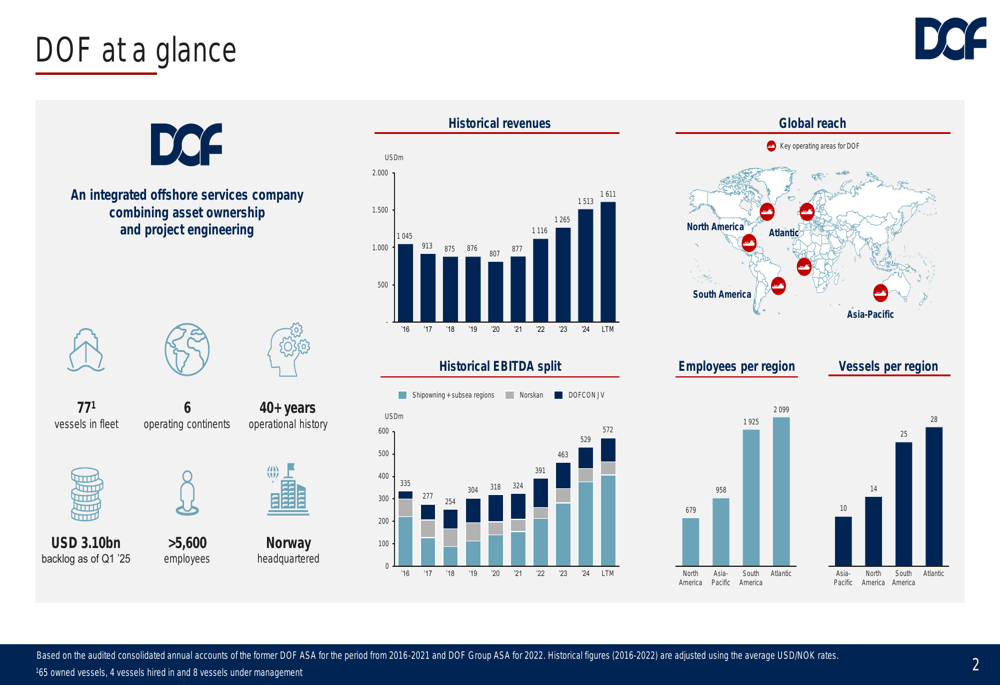

As an integrated offshore services company combining asset ownership and project engineering capabilities, DOF Group operates a fleet of 77 vessels across six continents with over 5,600 employees. The company’s global presence and diverse service offerings have positioned it well to capitalize on the continued strength in offshore energy markets.

As shown in the following overview of DOF Group’s global operations and financial performance:

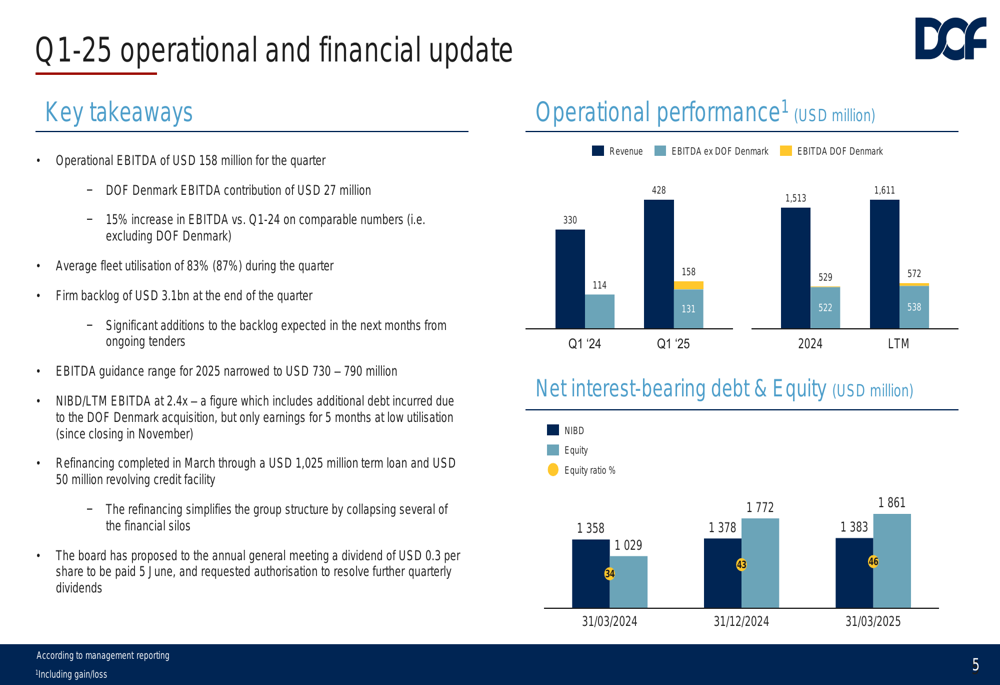

Quarterly Performance Highlights

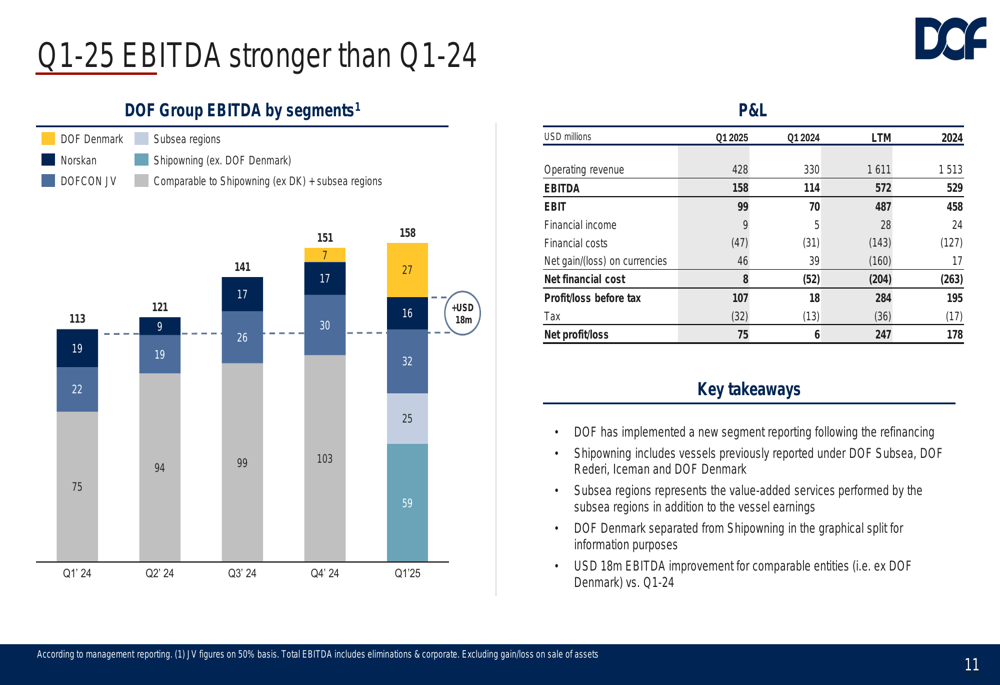

DOF Group reported impressive financial results for Q1 2025, with revenue reaching $428 million, a substantial 29.7% increase from $330 million in Q1 2024. Operational EBITDA surged to $158 million, representing a 38.6% year-over-year improvement compared to $114 million in the same period last year. On a comparable basis, excluding the contribution from DOF Denmark, EBITDA increased by 15% versus Q1 2024.

Net profit for the quarter reached $75 million, a dramatic improvement from just $6 million in Q1 2024, demonstrating the company’s enhanced profitability and operational efficiency. The average fleet utilization stood at 83%, slightly below the 87% reported in the previous period.

The following slide details DOF Group’s Q1 2025 financial performance compared to previous periods:

A more detailed breakdown of EBITDA by segment shows the contribution from different business units, with DOF Denmark adding $27 million to the quarterly results:

Financial Position and Debt Restructuring

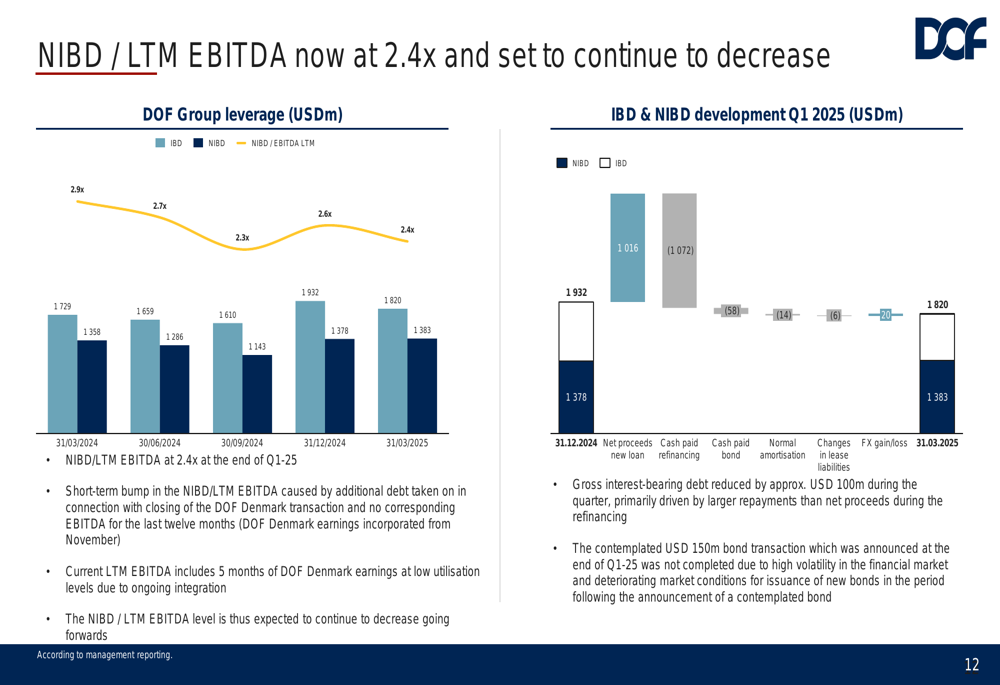

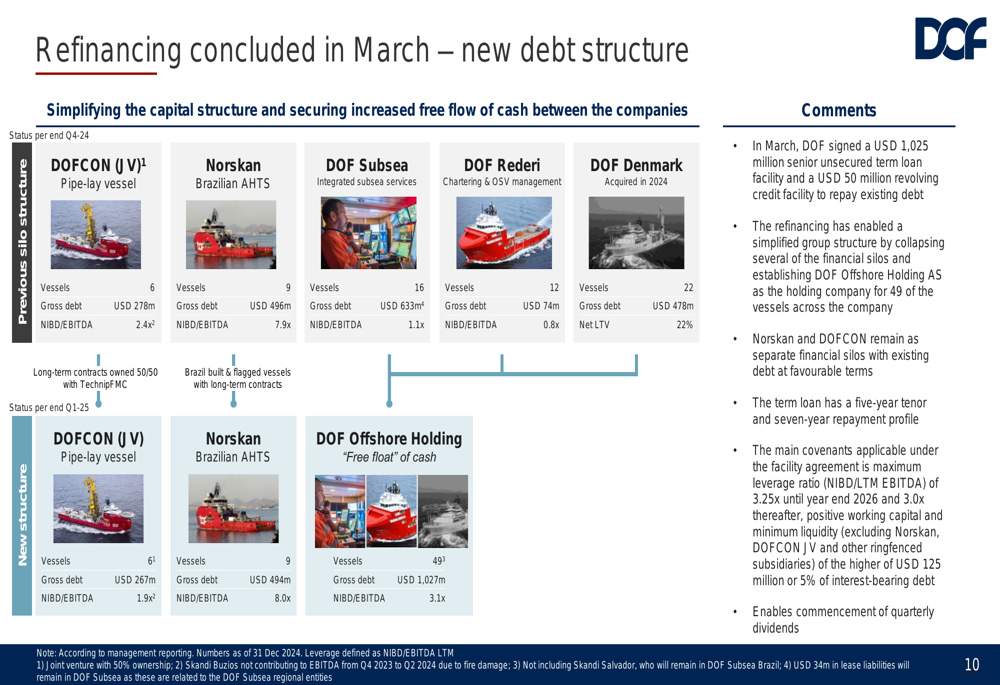

A significant development during the quarter was the completion of DOF Group’s refinancing in March 2025, which included a $1,025 million senior unsecured term loan facility and a $50 million revolving credit facility. This refinancing has enabled a simplified group structure by consolidating several financial silos and establishing DOF Offshore Holding AS as the holding company.

The company’s Net Interest-Bearing Debt (NIBD) to Last Twelve Months (LTM) EBITDA ratio stood at 2.4x at the end of Q1 2025. This ratio includes additional debt taken on for the DOF Denmark acquisition, with only five months of corresponding EBITDA contribution at low utilization levels due to ongoing integration. Management expects this leverage ratio to decrease further in coming quarters.

The following chart illustrates the company’s leverage position and its development:

The refinancing has significantly transformed DOF Group’s debt structure, as shown in this comparison of pre- and post-refinancing arrangements:

Backlog and New Contracts

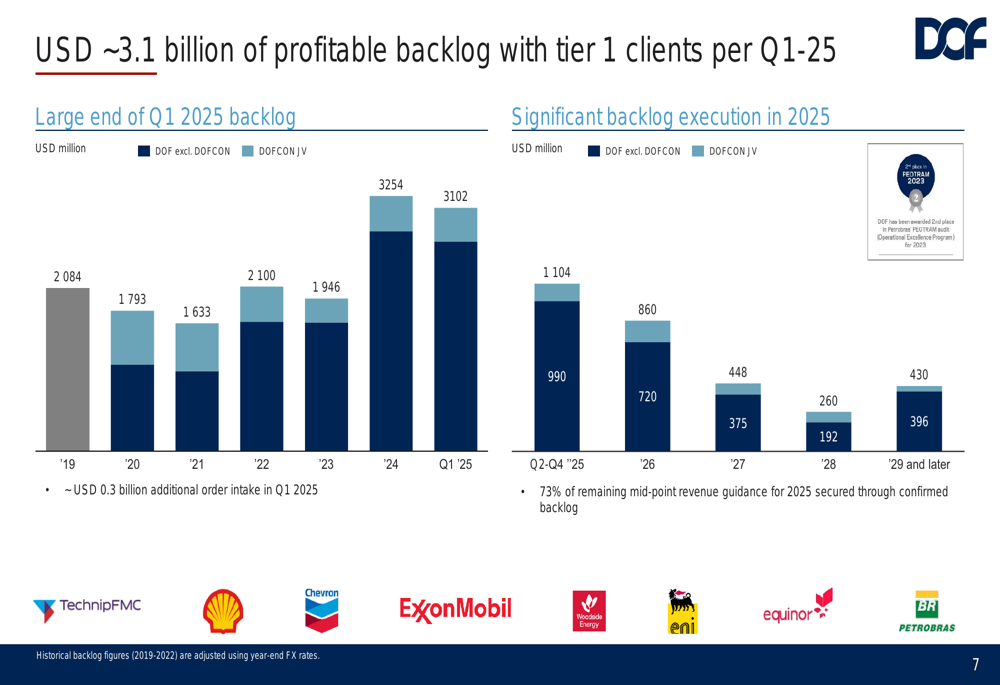

DOF Group reported a firm backlog of $3.1 billion at the end of Q1 2025, providing strong revenue visibility for the coming years. The company secured approximately $0.3 billion in additional order intake during the quarter and expects significant additions to the backlog in the coming months from ongoing tenders.

The backlog execution schedule indicates that 73% of the remaining mid-point revenue guidance for 2025 is already secured. The company maintains relationships with tier 1 clients including TechnipFMC (NYSE:FTI), Shell, Chevron (NYSE:CVX), ExxonMobil (NYSE:XOM), Woodside (OTC:WOPEY) Energy, Equinor, Eni, and Petrobras.

As illustrated in the following backlog analysis:

During Q1 and early Q2 2025, DOF Group secured several new contracts across multiple regions:

- Two projects in the Gulf of Mexico with international oil companies

- A SURF project in Africa valued at $100-200 million with over 450 vessel days

- Multiple subsea service contracts in the Asia-Pacific region worth over $30 million

- An FPSO installation project in Africa with a 3-year extension valued at $15-25 million

- Contract extensions for vessels operating in Brazil

The company also highlighted its strong position in ongoing AHTS and RSV tenders in Brazil, noting that it came second in preliminary results on a strategically important long-term RSV newbuild tender.

Updated Guidance and Outlook

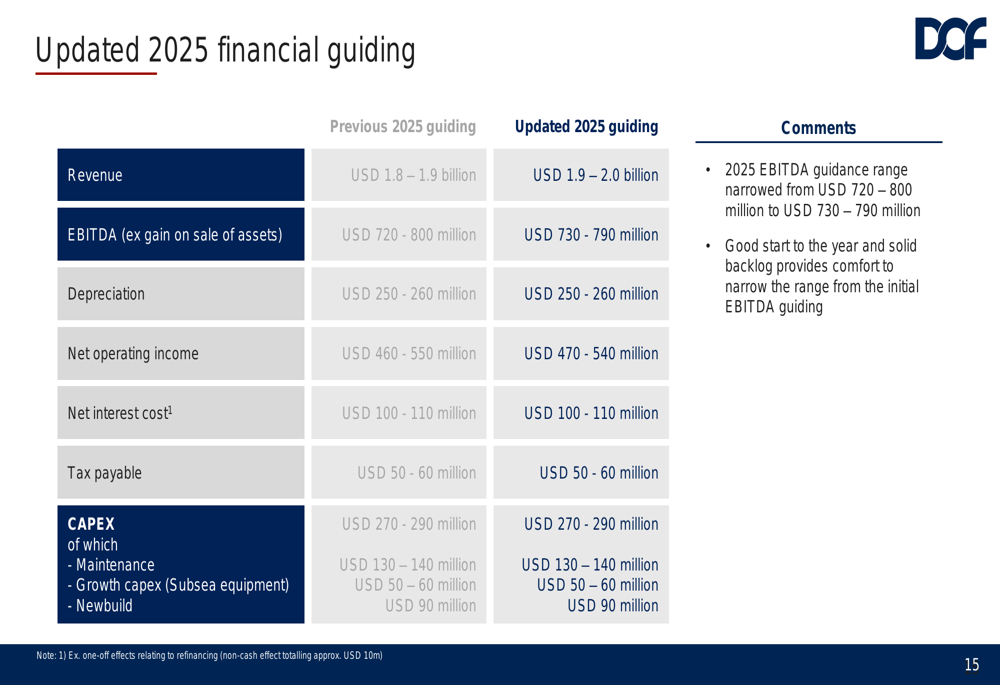

DOF Group has narrowed its 2025 EBITDA guidance range to $730-790 million from the previous $720-800 million, reflecting increased confidence in its financial projections. The company also raised its revenue guidance to $1.9-2.0 billion from the previous $1.8-1.9 billion.

The following slide details the updated financial guidance for 2025:

In a significant milestone for shareholder returns, the board has proposed a dividend of $0.30 per share to be paid on June 5, 2025, subject to approval at the annual general meeting on May 20, 2025. This marks the beginning of a quarterly dividend policy, signaling management’s confidence in the company’s financial strength and future prospects.

Looking ahead, DOF Group expects continued strong performance driven by high tendering activity, particularly in Brazil. The company’s strategic focus on fleet optimization and its strong backlog provide a solid foundation for sustained growth throughout 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.