WATCH LIVE: Investing.com reveals the top 10 stock picks for 2026

Introduction & Market Context

DOF Group ASA (OB:DOFG) delivered a strong second quarter performance, according to its Q2 2025 presentation released on August 20, 2025. The offshore services provider reported significant growth in key financial metrics while continuing to secure substantial contracts across its global operations. The company's stock has shown positive momentum, with shares up 2.47% to 97.8 NOK at the time of the presentation, approaching its 52-week high of 103.6 NOK.

The offshore services market continues to show robust demand across DOF's operating regions, with particularly strong activity in Brazil, where the company has secured multiple long-term contracts with Petrobras. DOF's integrated business model, combining vessel ownership with subsea engineering capabilities, has positioned it well to capitalize on the current favorable market conditions.

Quarterly Performance Highlights

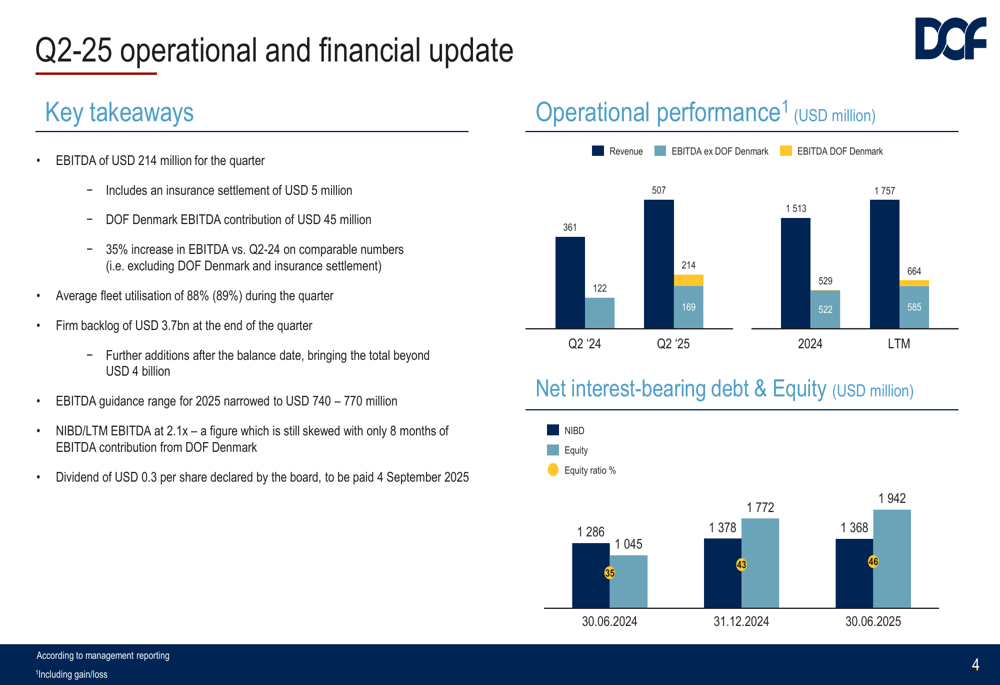

DOF Group reported Q2 2025 EBITDA of USD 214 million, representing a 35% increase compared to Q2 2024 on comparable numbers. This figure includes a USD 5 million insurance settlement and a USD 45 million contribution from DOF Denmark. The company maintained strong fleet utilization at 88% during the quarter.

As shown in the following operational and financial update chart, DOF has demonstrated consistent improvement in key metrics:

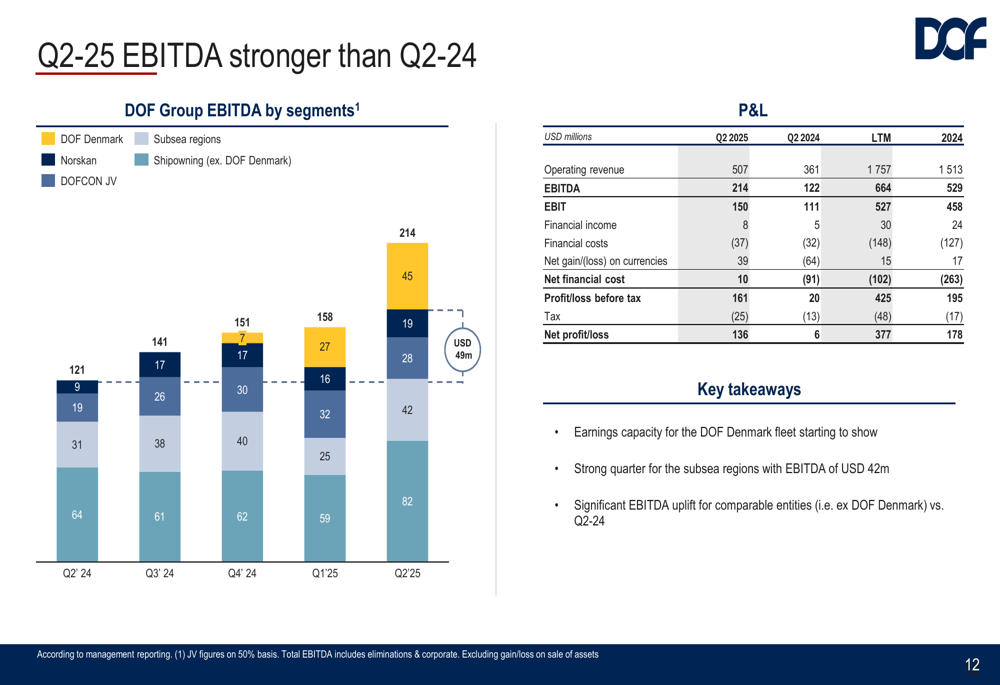

Revenue for the quarter reached USD 507 million, compared to USD 361 million in Q2 2024. The company's P&L breakdown reveals a net profit of USD 136 million, showcasing the company's improved profitability.

"The subsea regions continue to contribute with solid earnings and projects to secure utilisation for the project fleet," noted the company in its presentation, highlighting that a third-party vessel was utilized on a short-term charter for a North Sea project when no DOF vessels were available.

Strategic Initiatives

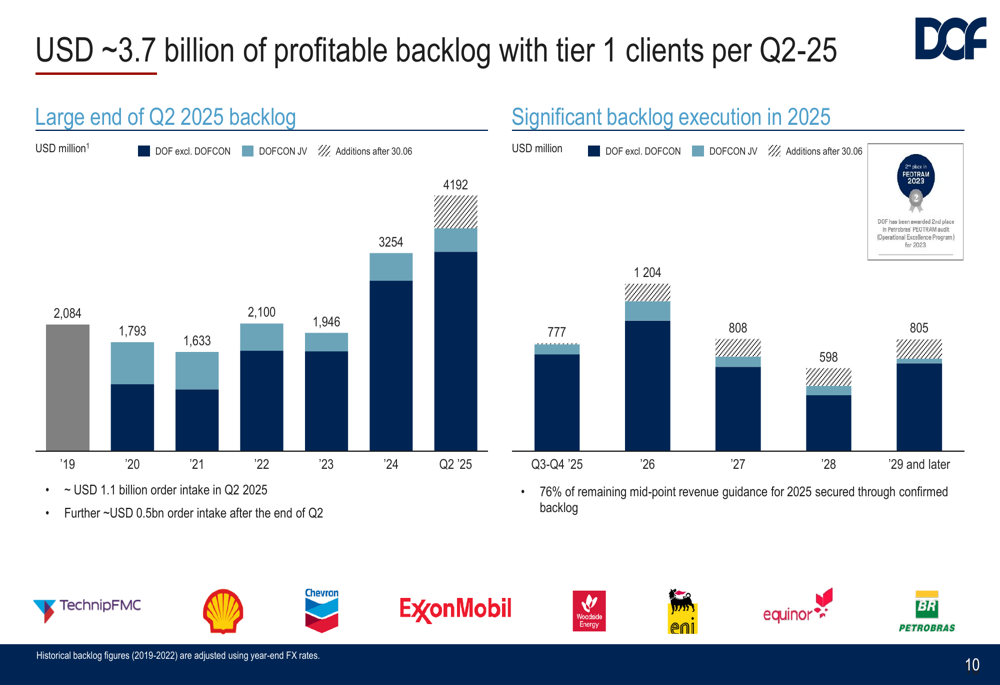

DOF Group has significantly strengthened its contract backlog, which now stands at USD 3.7 billion. The company reported USD 1.1 billion in new order intake during Q2 2025, with an additional USD 0.5 billion secured after the quarter's end. This robust backlog provides substantial revenue visibility, with 76% of the remaining mid-point revenue guidance for 2025 already secured.

The company's backlog development and client quality are illustrated in the following chart:

A major strategic achievement has been the securing of ten 4-year contracts with Petrobras in Brazil, with a total value exceeding USD 1.25 billion. These contracts, announced from the AHTS and RSV tender processes, are expected to commence between December 2025 and February 2026. The vessels assigned to these contracts will undergo various degrees of upgrading to meet contract specifications.

DOF has also made significant progress in securing long-term contracts for its DOF Denmark AHTS fleet, which was acquired in late 2024. Several vessels have been secured on multi-year contracts, including:

- Skandi Mover and Skandi Mariner contracted with Cenovus for 5.5 and 2 years respectively

- Skandi Lifter and Skandi Logger contracted with Petrobras on 4-year agreements

- Skandi Cutter's existing engagement extended for an additional 3 years

- Skandi Tender and Skandi Trader agreed to be sold to an international buyer

Detailed Financial Analysis

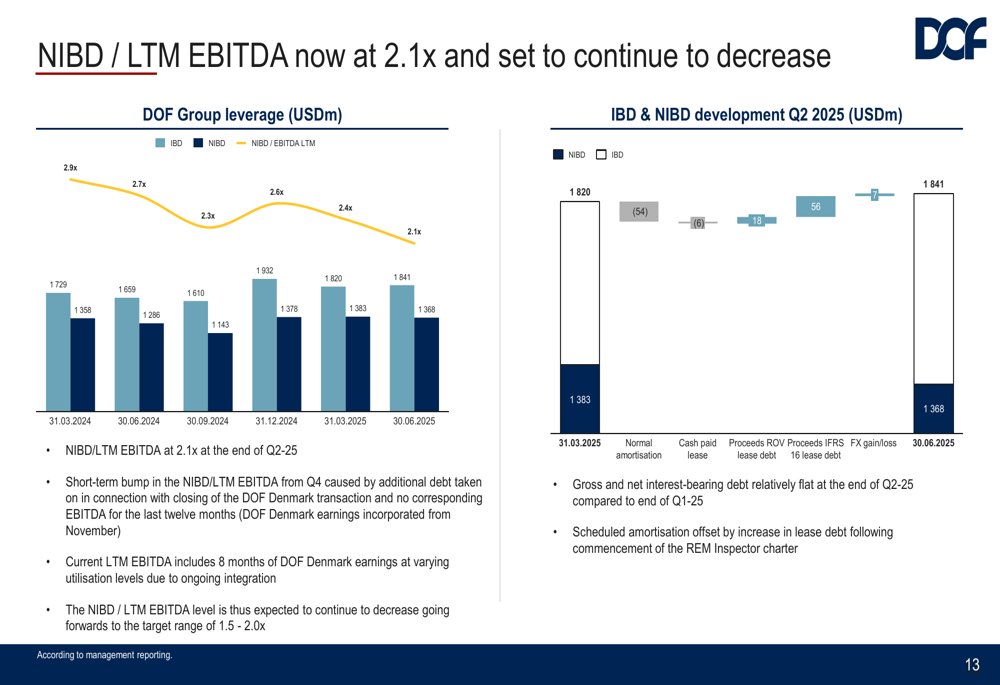

DOF Group's financial position continues to strengthen, with the company making steady progress in reducing its leverage. The NIBD/LTM EBITDA ratio has improved to 2.1x, down from 2.9x in early 2024, as illustrated in the following debt development chart:

The company maintained a healthy cash balance of USD 396 million at the end of Q2 2025. Operating cash flow remained strong at USD 157 million for the quarter, while investing activities used USD 55 million and financing activities used USD 142 million.

DOF's equity ratio has improved from 35% to 46% over the past year, reflecting the company's strengthened balance sheet. The board has declared a dividend of USD 0.3 per share (approximately USD 74 million total), to be paid on September 4, 2025. This brings the total dividends paid and declared year-to-date to USD 148 million, demonstrating the company's commitment to shareholder returns.

The company's EBITDA performance by segment shows strong contributions across the business:

The subsea regions delivered particularly strong results, with EBITDA of USD 42 million in Q2 2025. The DOF Denmark acquisition has significantly contributed to the company's earnings capacity, while the core business continues to perform well.

Forward-Looking Statements

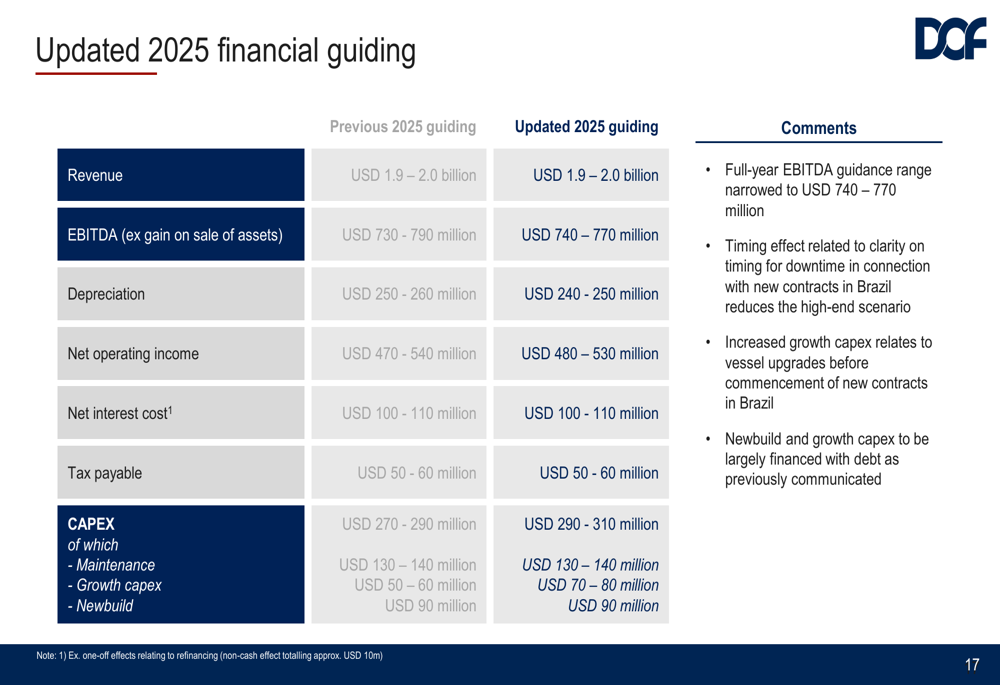

DOF Group has narrowed its 2025 EBITDA guidance to USD 740-770 million, reflecting increased confidence in its outlook. Revenue guidance for the full year is set at USD 1.9-2.0 billion, an upward revision from the USD 1.8-1.9 billion projected in the Q4 2024 earnings call.

The updated financial guidance for 2025 is presented in the following table:

The company expects continued strong market conditions globally, with high activity levels across all regions. The robust backlog provides revenue visibility, while continued high tendering activity points to a solid pipeline of future opportunities.

DOF's strategic focus remains on further reducing debt and leverage, optimizing its fleet, and capitalizing on its global presence to capture business opportunities in regions with the highest demand. The successful integration of DOF Denmark and the significant contract wins in Brazil position the company well for continued growth in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.