IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

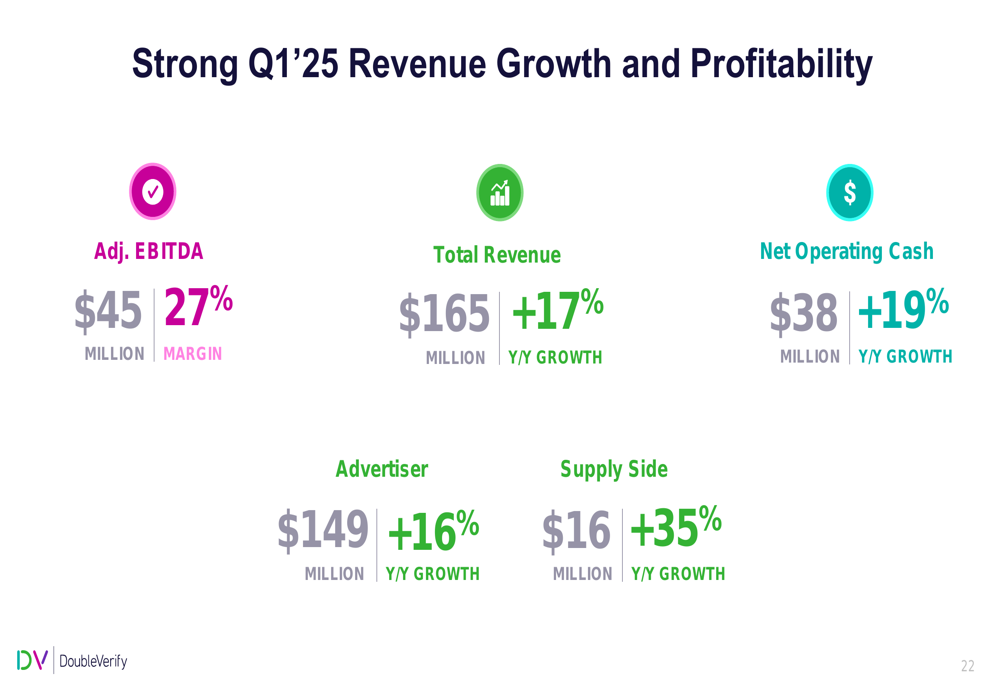

DoubleVerify Holdings Inc. (NYSE:DV) released its Q1 2025 investor presentation on May 8, 2025, showcasing strong financial performance with total revenue of $165 million, representing a 17% year-over-year increase. The digital advertising verification company reported adjusted EBITDA of $45 million with a 27% margin, demonstrating continued profitability despite market challenges.

The positive Q1 results come after a disappointing Q4 2024, where the company missed revenue expectations ($191 million versus $197 million forecast), which led to a significant stock price decline. Currently trading at $13.54, DV shares remain well below their 52-week high of $23.11, indicating ongoing investor concerns despite the solid Q1 performance.

DoubleVerify operates in a large and expanding digital advertising market, which the company projects will grow from $329 billion in 2024 to $477 billion by 2029, representing an 8% five-year CAGR. The company positions itself as an essential third-party verification solution addressing critical challenges in digital advertising.

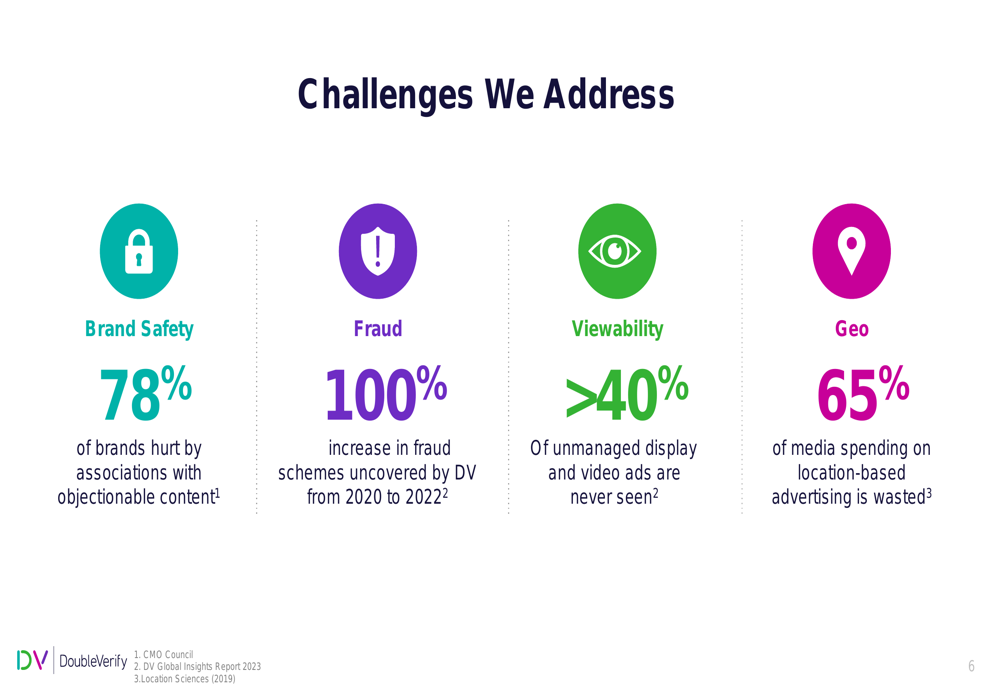

As shown in the following slide highlighting the challenges DoubleVerify addresses:

Quarterly Performance Highlights

DoubleVerify’s Q1 2025 financial results demonstrated strong growth across all business segments. Total (EPA:TTEF) revenue reached $165 million, up 17% year-over-year, with advertiser revenue growing 16% to $149 million and supply-side revenue surging 35% to $16 million.

The company’s financial performance for Q1 2025 is summarized in the following slide:

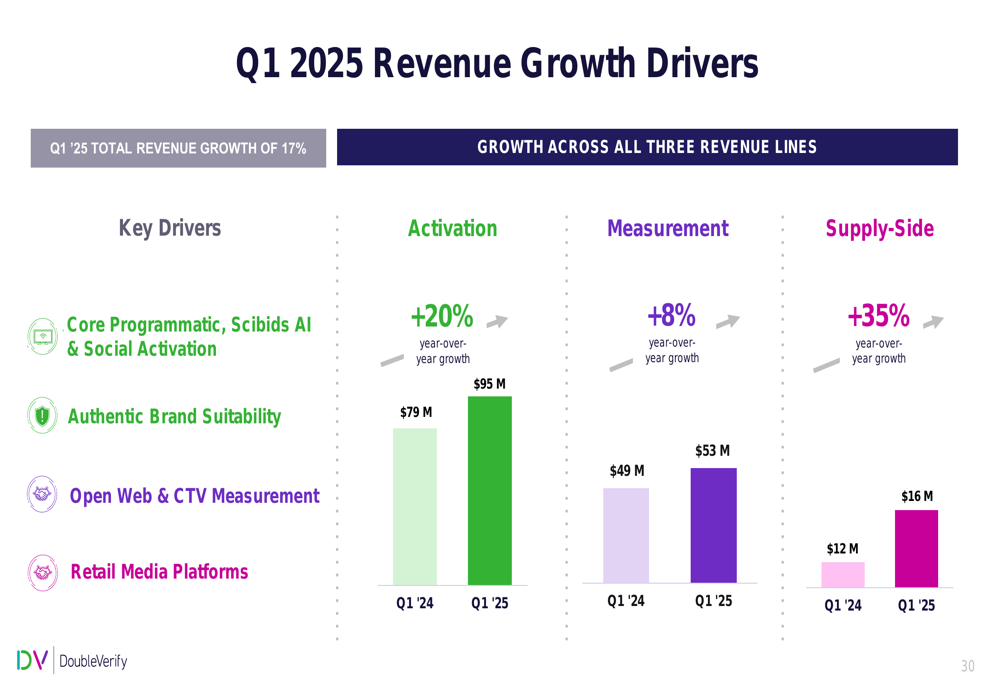

Breaking down the revenue growth drivers, activation revenue increased by 20% year-over-year to $95 million, while measurement revenue grew by 8% to $53 million. The company’s growth was primarily volume-driven, with transaction volume (MTM) increasing by 22%, partially offset by a 6% decline in pricing (MTF).

The following slide details the revenue growth drivers for Q1 2025:

DoubleVerify maintained strong customer relationships, reporting 112% net revenue retention and over 95% gross revenue retention. The company now has 337 customers generating over $200,000 in annual revenue, representing a 14% year-over-year increase. The average tenure for the top 25 customers stands at 8.9 years, demonstrating high customer loyalty.

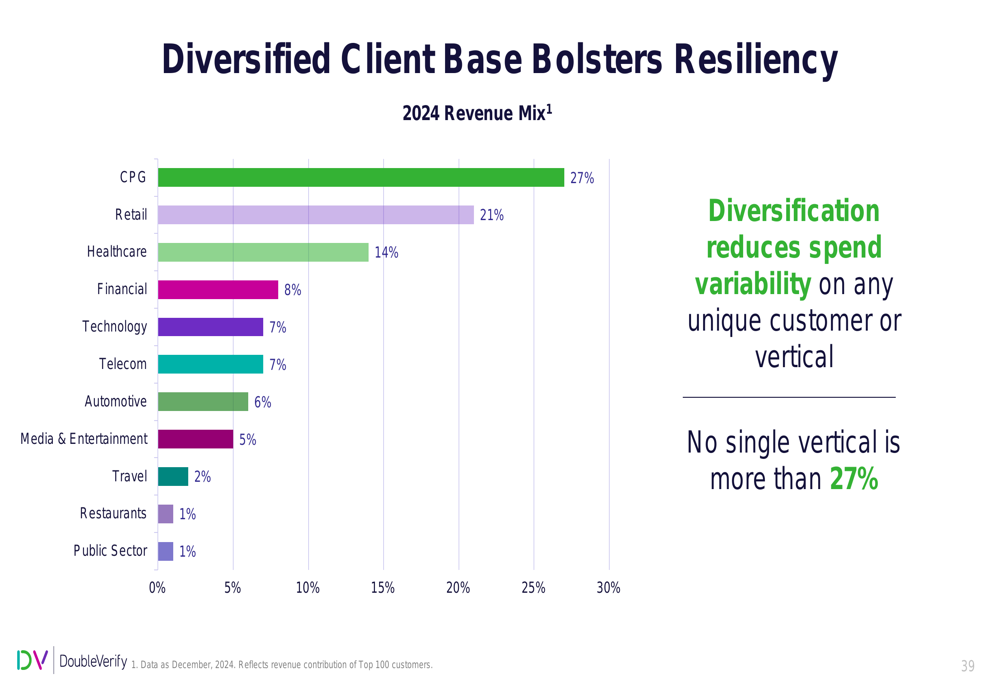

The company’s diversified client base, with no single vertical accounting for more than 27% of revenue, has helped maintain resilience against sector-specific advertising fluctuations, as illustrated in this breakdown:

Strategic Initiatives

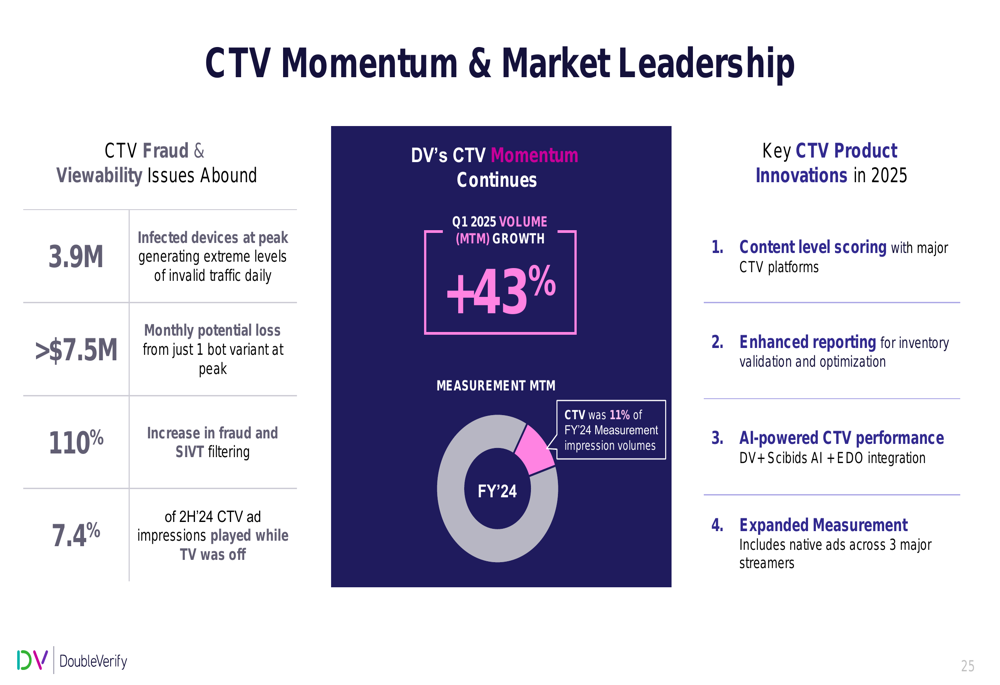

DoubleVerify is focusing on several strategic growth areas, particularly in connected TV (CTV), social media, and retail media networks. The company reported a 43% year-over-year increase in CTV volume for Q1 2025, highlighting its momentum in this rapidly growing segment.

The following slide outlines the company’s CTV momentum and market leadership:

In social media, which represents a $200+ billion market opportunity, DoubleVerify has expanded its pre-bid suitability controls on platforms like Facebook (NASDAQ:META), Instagram, and TikTok. Currently, social media accounts for only 16% of the company’s revenue, indicating significant room for expansion.

The company is also building a unified intelligence platform that combines media quality, optimization, and outcomes measurement. This strategy is supported by recent acquisitions, including Rockerbox for outcomes measurement and Scibids for AI-powered optimization.

DoubleVerify maintains a strong balance sheet with approximately $175 million in cash and zero long-term debt, providing flexibility for further strategic acquisitions and investments in core growth areas.

Forward-Looking Statements

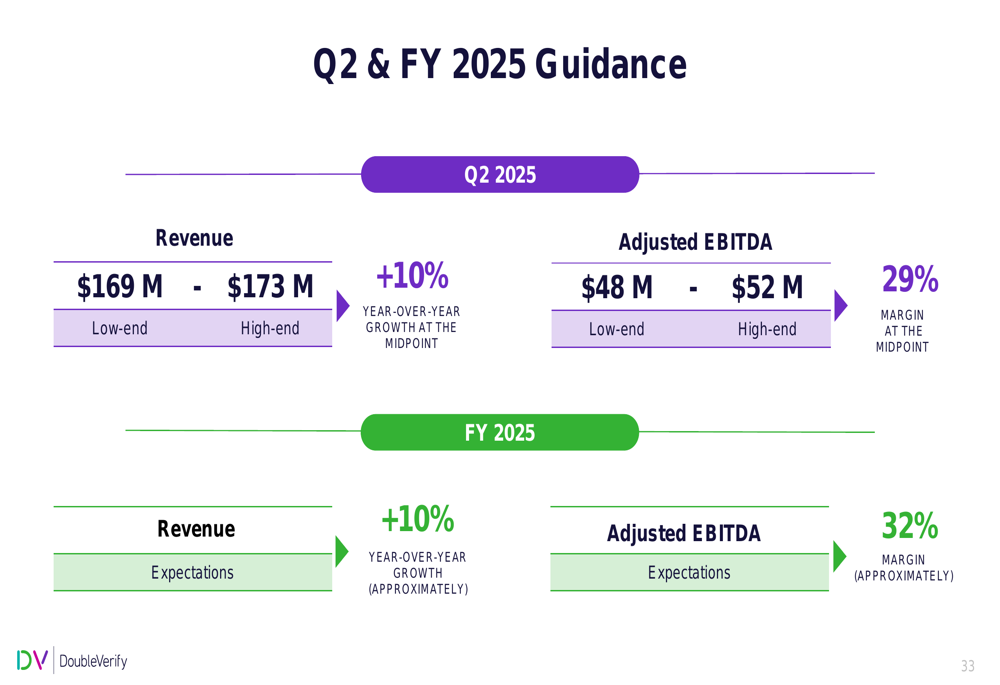

For Q2 2025, DoubleVerify projects revenue between $169 million and $173 million, representing approximately 10% year-over-year growth at the midpoint. Adjusted EBITDA is expected to be between $48 million and $52 million, with a 29% margin at the midpoint.

For the full year 2025, the company anticipates approximately 10% year-over-year revenue growth and an adjusted EBITDA margin of approximately 32%. This guidance suggests a slight deceleration from the 15% revenue growth achieved in 2024.

The company’s Q2 and FY 2025 guidance is presented in the following slide:

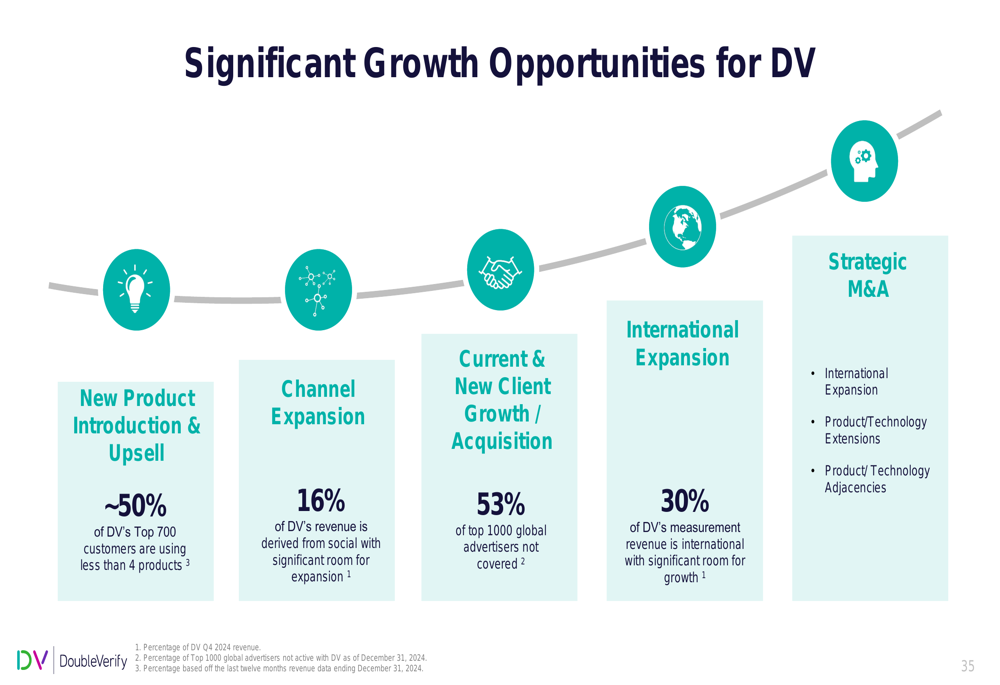

DoubleVerify identified several significant growth opportunities, including product cross-selling (approximately 50% of top 700 customers use less than 50% of DV products), international expansion (only 30% of measurement revenue is international), and new client acquisition (53% of top 1000 global advertisers not yet covered).

The following slide outlines these growth opportunities:

Competitive Industry Position

DoubleVerify positions itself as an essential solution for digital advertisers, focusing on three key differentiators: scale across platforms, innovation that is identifier-independent, and trust through accreditation and objectivity.

The company’s "verify everywhere" strategy makes it largely agnostic to shifts in ad spend across sectors, while its fixed-fee business model helps insulate revenue from CPM volatility. This approach has resulted in a diversified customer base that includes many of the world’s largest brands.

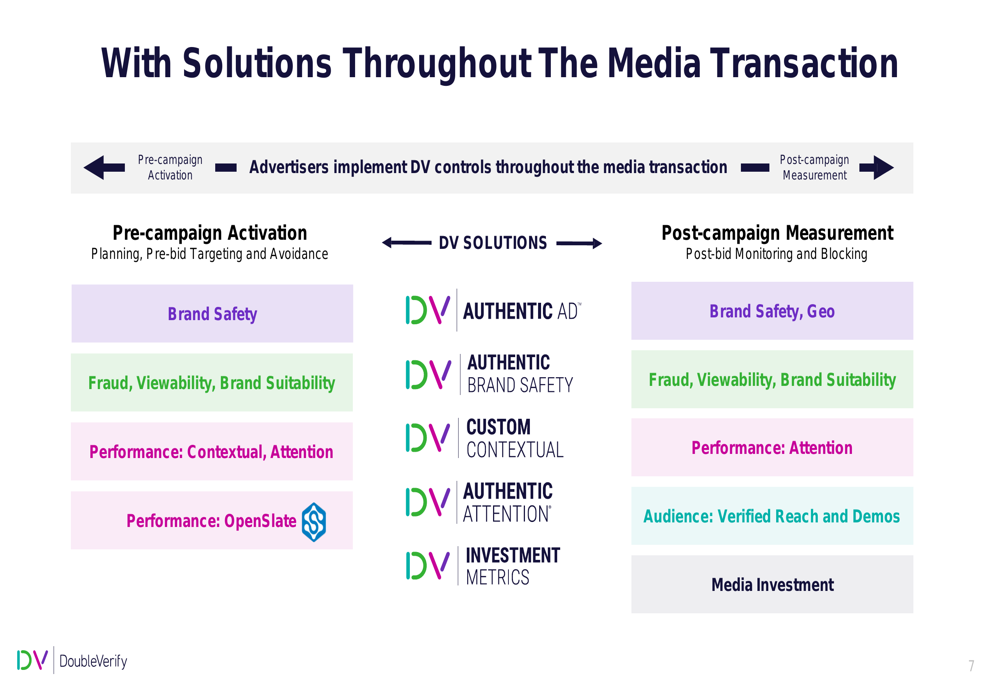

As shown in the following slide, DoubleVerify’s solutions address critical challenges throughout the media transaction lifecycle:

The company’s comprehensive Media Rating Council accreditations and other industry certifications provide competitive advantages and reinforce its position as an impartial third-party verification provider.

Despite the positive Q1 2025 results, investors should note the contrast with the previous quarter’s performance and the projected slowdown in revenue growth for 2025. The company’s ability to execute on its cross-selling opportunities and expansion into high-growth areas like CTV and social media will be crucial for maintaining investor confidence and supporting long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.