US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

Douglas Emmett , Inc. (NYSE:DEI) recently shared its investor overview presentation dated March 31, 2025, highlighting the company’s strategic positioning in high-barrier markets amid challenging financial results. The presentation comes after DEI reported disappointing Q4 2024 earnings with an EPS of -$1, significantly below the forecasted -$0.05, though revenue slightly exceeded projections at $245 million.

The real estate investment trust, which focuses primarily on office and multifamily properties in Los Angeles and Honolulu, is trading at $14.02 as of May 6, 2025, down 0.85% in the latest session. The stock has experienced volatility but remains within its 52-week range of $12.39 to $20.50.

Portfolio Overview

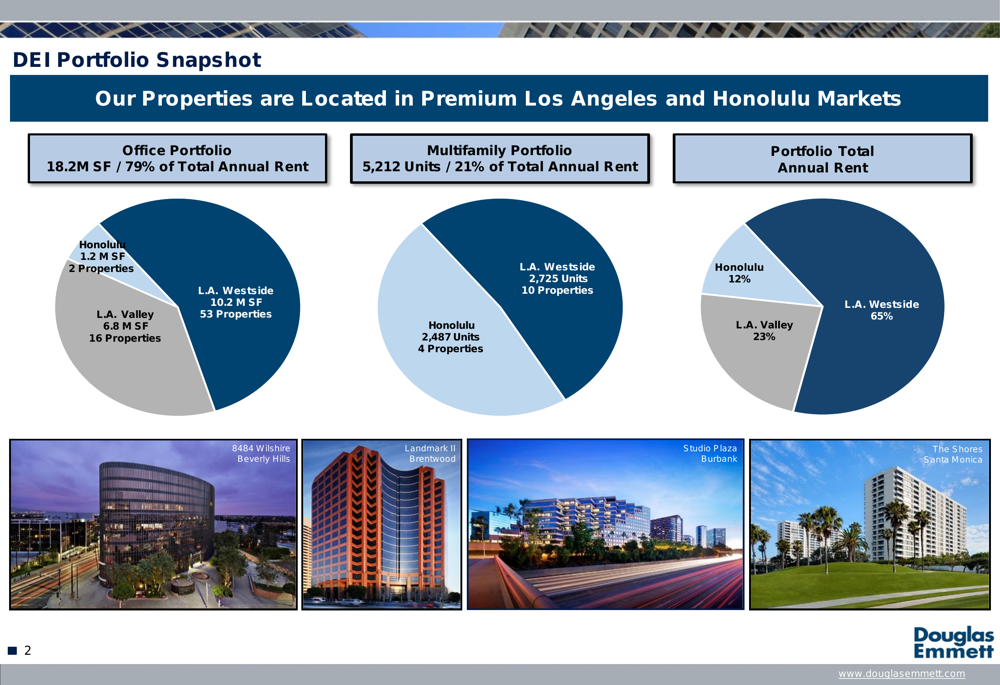

Douglas Emmett’s portfolio consists of 18.2 million square feet of office space contributing 79% of total annual rent, and 5,212 multifamily units generating the remaining 21%. The company maintains a concentrated geographic focus with 65% of annual rent coming from Los Angeles Westside, 23% from Los Angeles Valley, and 12% from Honolulu.

As shown in the following portfolio breakdown:

The company’s office properties are distributed across key submarkets with 53 properties (10.2M SF) in L.A. Westside, 16 properties (6.8M SF) in L.A. Valley, and 2 properties (1.2M SF) in Honolulu. Its multifamily portfolio includes 10 properties (2,725 units) in L.A. Westside and 4 properties (2,487 units) in Honolulu.

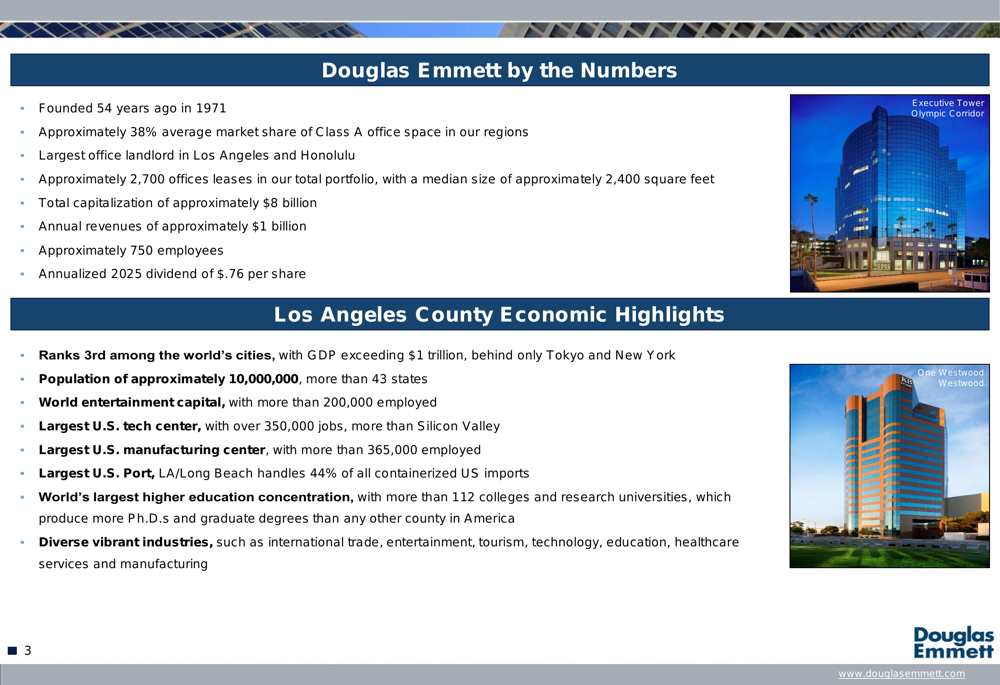

Founded 54 years ago in 1971, Douglas Emmett has established itself as the largest office landlord in Los Angeles and Honolulu, with approximately 38% average market share of Class A office space in its markets. The company reports a total capitalization of approximately $8 billion, annual revenues of approximately $1 billion, and an annualized 2025 dividend of $0.76 per share.

Strategic Advantages

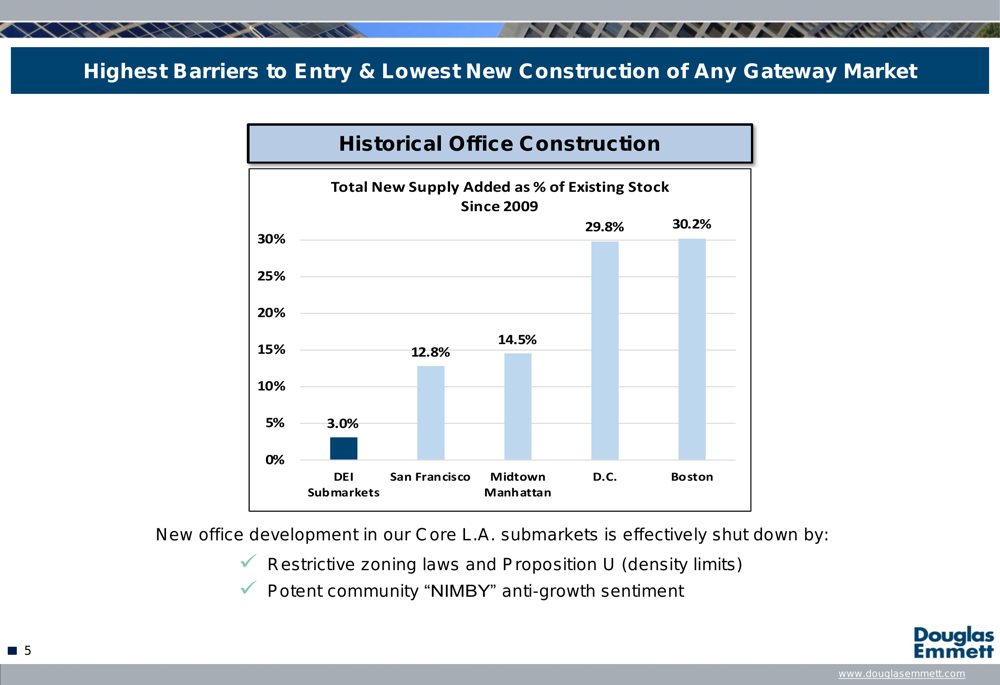

A cornerstone of DEI’s investment thesis is the limited new construction in its core markets. The presentation highlights that since 2009, DEI’s submarkets have seen only 3.0% new supply added as a percentage of existing stock, compared to significantly higher rates in other major markets: San Francisco (12.8%), Midtown Manhattan (14.5%), Washington D.C. (29.8%), and Boston (30.2%).

This limited supply is attributed to restrictive zoning laws, density limits under Proposition U, and strong community anti-growth sentiment, as illustrated in the following chart:

The company also benefits from Los Angeles’ notorious traffic congestion, which effectively creates distinct submarkets with limited competition. Commute times from Westside residential neighborhoods to DEI’s closest submarkets average just 21 minutes, compared to 71 minutes to Hollywood and 80 minutes to Downtown Los Angeles, creating a natural barrier to competition.

Financial Performance & Operational Efficiencies

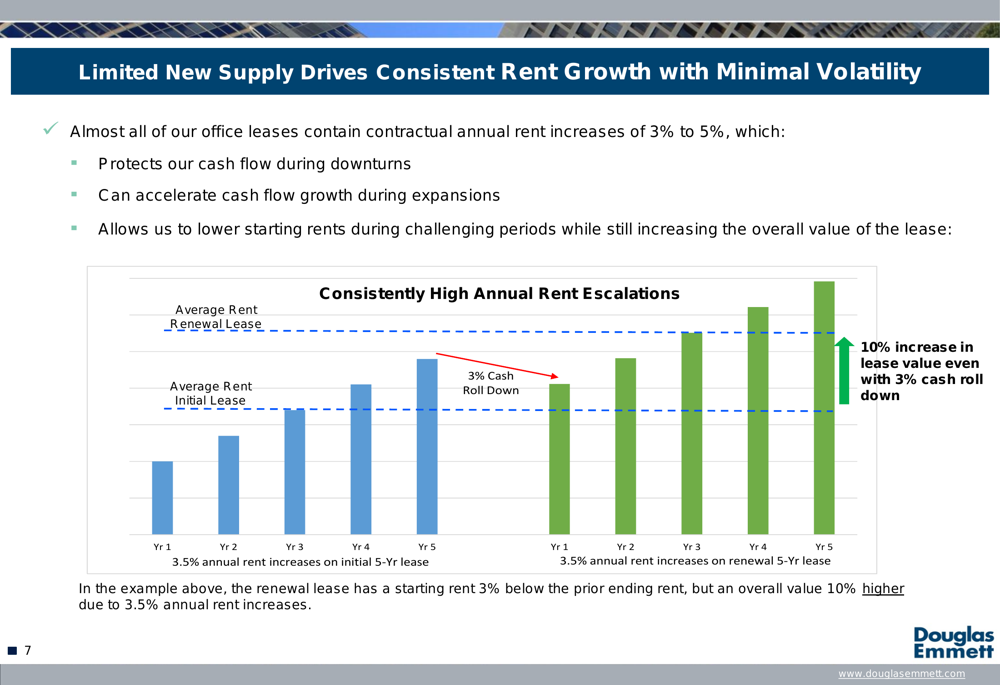

Douglas Emmett emphasizes its consistent rent growth model, with office leases containing contractual annual rent increases of 3% to 5%. This structure is designed to protect cash flow and accelerate growth during expansions, as illustrated in the following chart showing how even with a 3% initial cash roll-down, a renewal lease can achieve a 10% increase in overall lease value:

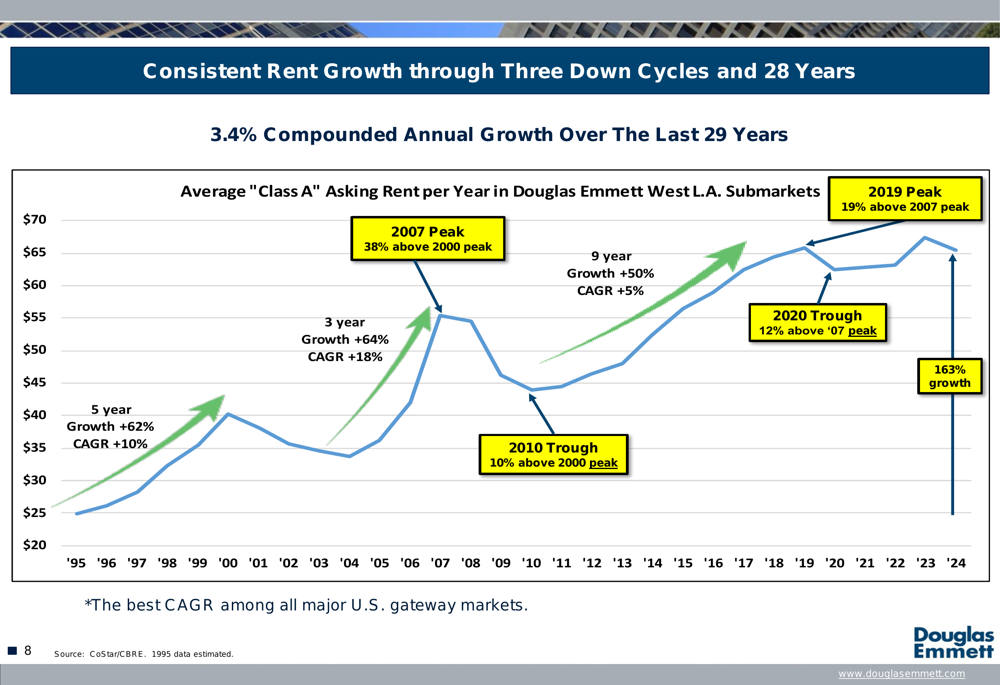

The company touts its long-term rent growth through multiple market cycles, claiming a 3.4% Compounded Annual Growth Rate over 28 years. According to DEI’s data, West Los Angeles has outperformed other major markets with 122% cumulative rent growth since 1998, compared to 87% in D.C., 58% in Midtown Manhattan, 38% in Boston, and 15% in San Francisco.

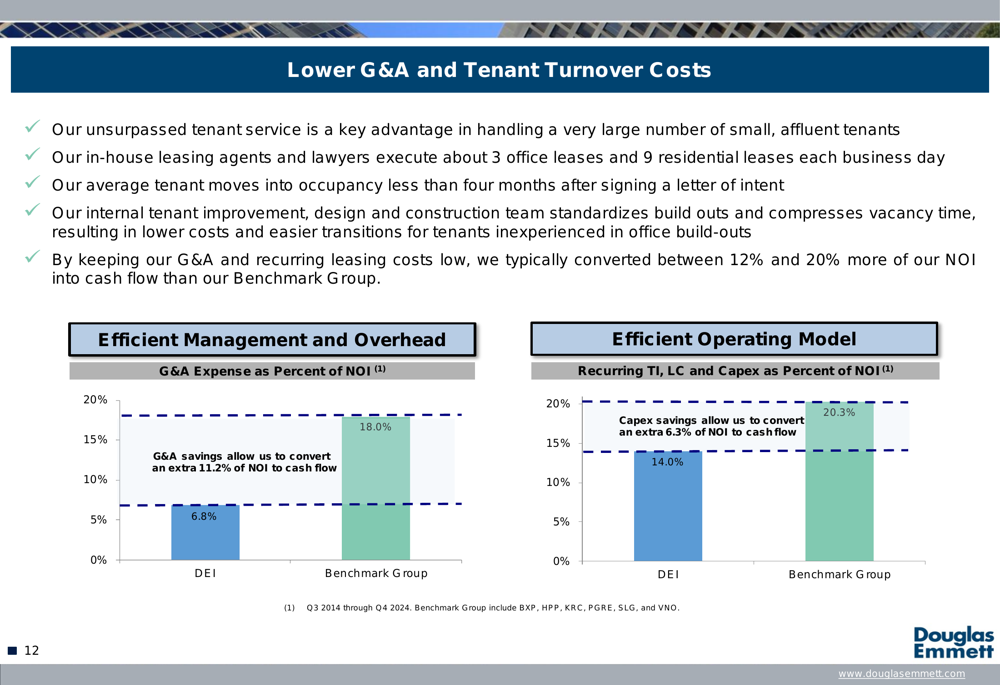

A key operational advantage highlighted is DEI’s lower expense structure compared to industry benchmarks. The company reports G&A expenses at 6.8% of NOI versus 18.0% for its benchmark group, and lower recurring tenant improvements, leasing commissions, and capital expenditures at 14.0% of NOI versus 20.3% for the benchmark group.

However, these operational strengths contrast with recent financial challenges. According to the Q4 2024 earnings report, DEI experienced a 5.5% year-over-year revenue decline and a 4.5% decrease in same property cash NOI. The company’s guidance for 2025 projects net income per share between -$0.17 and -$0.11, indicating continued pressure on profitability.

Tenant Diversity & Multifamily Strength

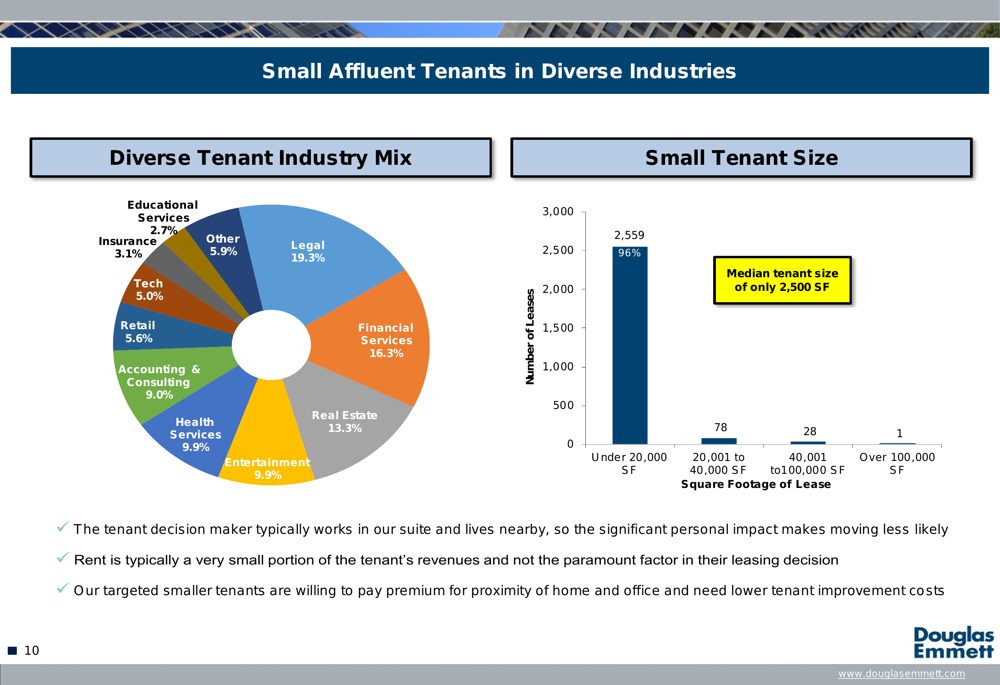

Douglas Emmett’s tenant base is characterized by diversity across industries and a focus on smaller tenants. The company’s office portfolio includes approximately 2,700 leases with a median tenant size of only 2,500 square feet. The tenant industry mix spans legal (19.3%), financial services (16.3%), real estate (13.3%), health services (9.9%), entertainment (9.9%), and other sectors.

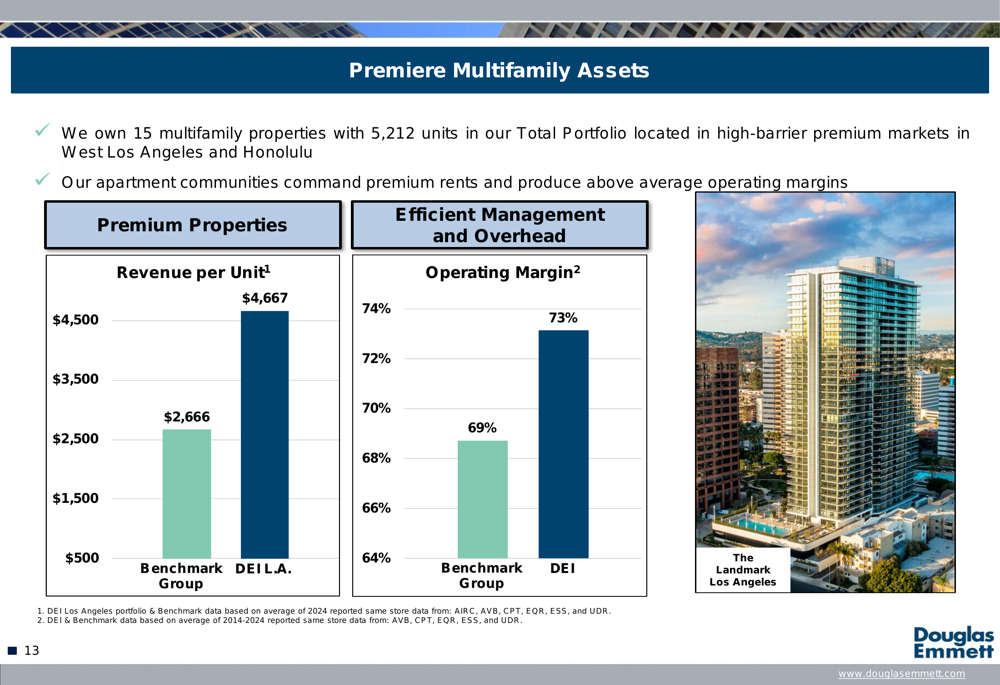

The company’s multifamily portfolio also demonstrates strong performance metrics relative to benchmarks. DEI reports revenue per unit of $4,667 for its Los Angeles properties compared to $2,666 for its benchmark group, and a higher operating margin of 73% versus 69% for the benchmark group.

Forward-Looking Statements & Challenges

A significant near-term challenge for Douglas Emmett is its debt maturity schedule, with substantial maturities coming due in the next few years: $1.38 billion in 2026, $951 million in 2027, $638 million in 2028, and $808 million in 2029. During the recent earnings call, management indicated they are focusing on refinancing the 2026 maturities.

The company is also emphasizing its sustainability initiatives, reporting that more than 84% of eligible office space qualified for "ENERGY STAR Certification" as of December 2024, and a 13% reduction in greenhouse gas emissions by December 31, 2024, compared to 2019 levels.

During the Q4 2024 earnings call, CEO Jordan Kaplan expressed optimism about market dynamics, noting increased showings in January 2025 and highlighting "thousands of units of potential development opportunities." However, investors will need to balance this optimism against the company’s recent financial performance and the challenges of a changing office market landscape.

As Douglas Emmett navigates these challenges, its concentrated portfolio in high-barrier markets with limited new supply may provide some insulation, but execution on debt refinancing and adapting to evolving tenant demands will be critical to improving its financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.