Gold prices dip as hawkish Fed minutes weigh ahead of Jackson Hole

Introduction & Market Context

D.R. Horton, Inc. (NYSE:DHI), America’s largest homebuilder, presented its Q2 fiscal 2025 results on April 17, 2025, highlighting solid performance despite ongoing challenges in the housing market. The company reported earnings per share of $2.58 on net income of $810.4 million, with consolidated pre-tax income of $1.1 billion on $7.7 billion of revenues. While maintaining its position as the market leader, D.R. Horton is navigating a complex environment characterized by elevated mortgage rates and affordability concerns, focusing on operational efficiency and capital returns to shareholders.

The stock has shown resilience, trading at $119.64, up 1.79% following the presentation, though still well below its 52-week high of $199.85.

Quarterly Performance Highlights

For the second quarter of fiscal 2025, D.R. Horton delivered 19,276 homes with home sales revenues of $7.2 billion. While this represents a decline from the 22,548 homes closed in Q2 FY2024, the company reported strong net sales orders of 22,437 homes valued at $8.4 billion, positioning it well for future quarters.

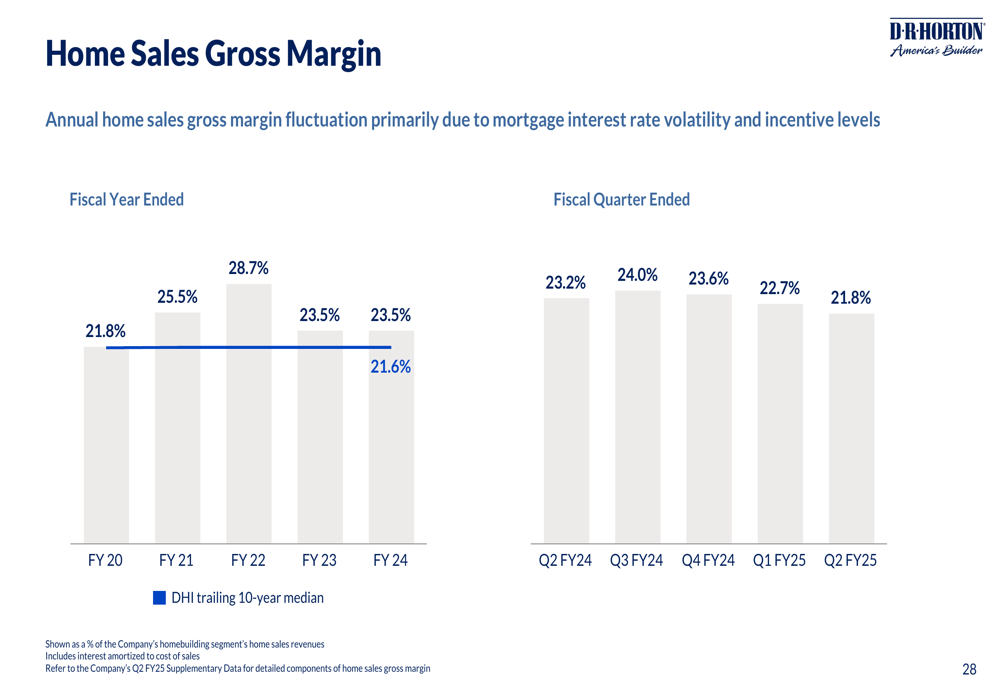

The company’s consolidated pre-tax profit margin was 13.8%, down from 16.8% in the same quarter last year, reflecting increased incentive costs and operational expenses. Home sales gross margin decreased to 21.8% from 23.2% in Q2 FY2024, primarily due to higher incentives to address affordability concerns in a higher interest rate environment.

As shown in the following chart, D.R. Horton’s home sales gross margin has fluctuated in recent quarters due to mortgage interest rate volatility and incentive levels:

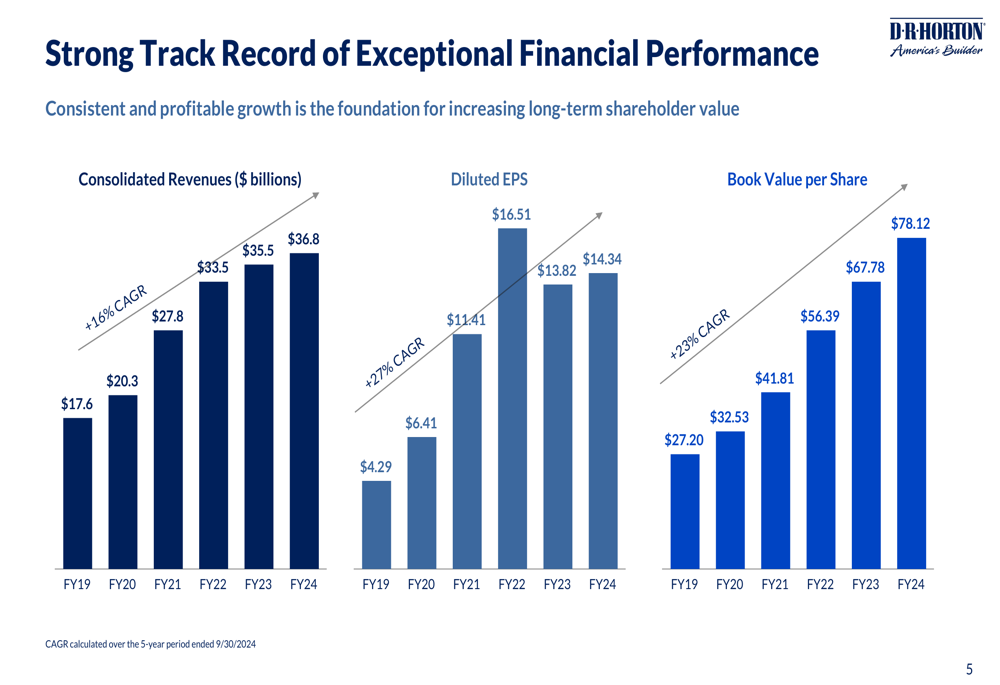

Despite margin pressure, D.R. Horton continues to demonstrate strong financial performance over the long term. The company has achieved impressive 5-year compound annual growth rates through September 30, 2024, with revenue growing at 16%, diluted EPS at 27%, and book value per share at 23%.

The following chart illustrates this exceptional financial trajectory:

Strategic Focus on Affordability

A key element of D.R. Horton’s strategy is addressing affordability challenges in the current market. The company has been proactively reducing square footage, with average home size decreasing by 8% from 2,119 to 1,950 square feet. This approach has helped maintain D.R. Horton’s average sales price approximately 25% below the national average for the quarter ended March 31, 2025.

The company’s product mix is strategically positioned to serve various market segments, with a particular emphasis on affordable housing. As illustrated in the following breakdown, 69% of homes closed were priced under $400,000, with an average sales price of $377,200:

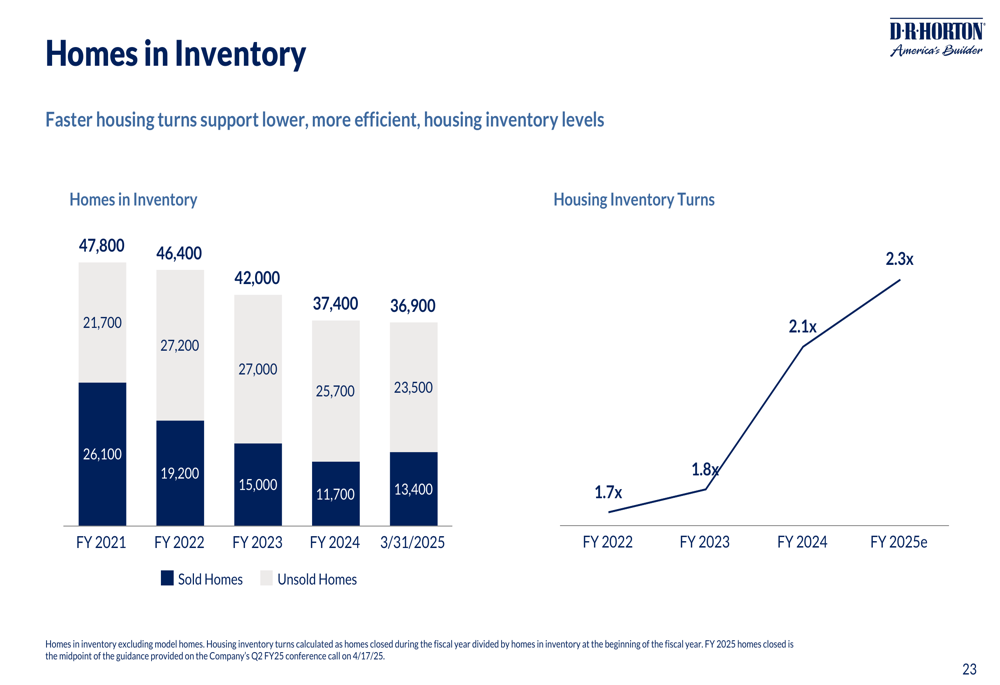

This focus on affordability is complemented by D.R. Horton’s operational efficiency. The company has improved its construction cycle times, which has allowed it to turn inventory faster and maintain a flexible approach to market conditions. The following chart shows the company’s inventory management strategy:

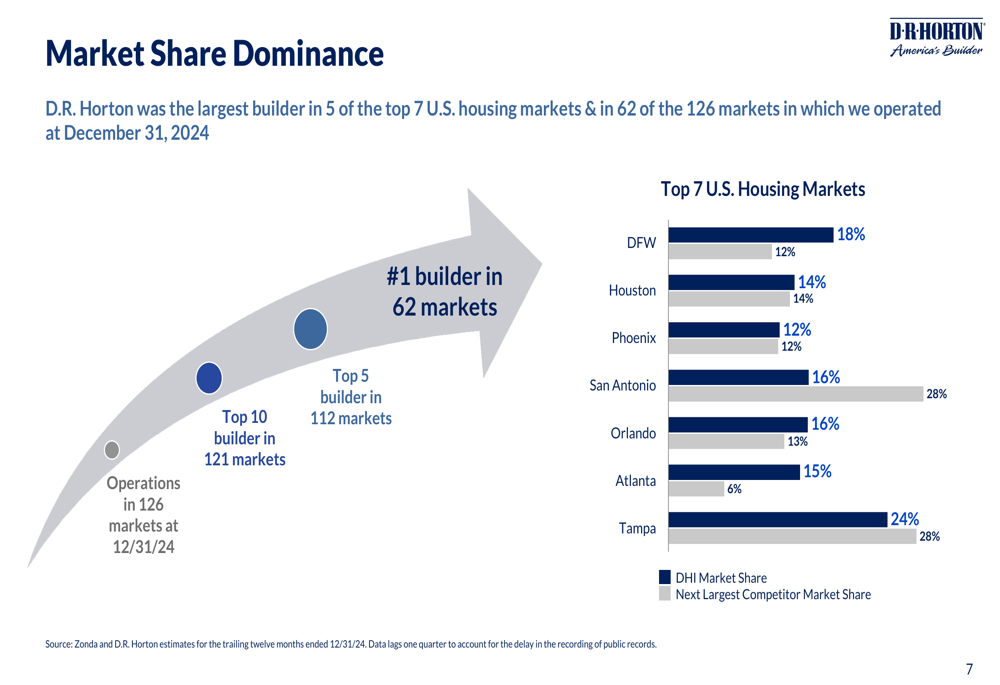

Market Leadership Position

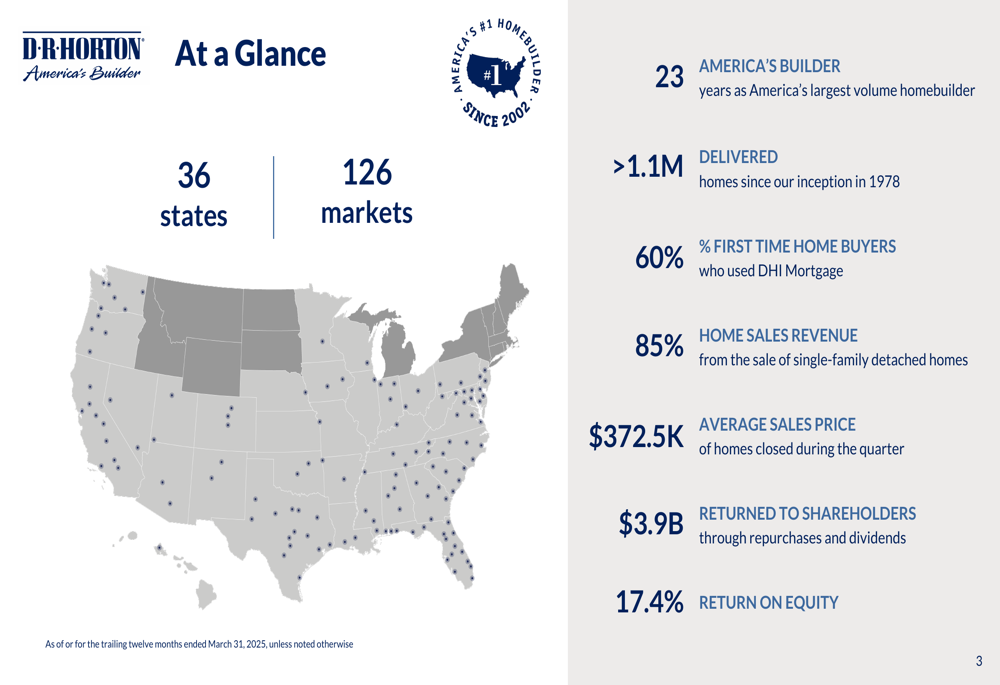

D.R. Horton continues to strengthen its position as America’s largest homebuilder, a title it has held for 23 years. The company operates in 36 states across 126 markets, with a particularly strong presence in the nation’s largest housing markets.

The following snapshot provides an overview of D.R. Horton’s market position and key metrics:

The company’s market dominance is particularly evident in its competitive positioning within top U.S. housing markets. D.R. Horton is the largest builder in 5 of the top 7 U.S. housing markets and in 62 of the 126 markets in which it operates. This scale provides significant advantages in purchasing power, brand recognition, and operational efficiency.

As illustrated in the following chart, D.R. Horton holds substantial market share advantages over competitors in key markets:

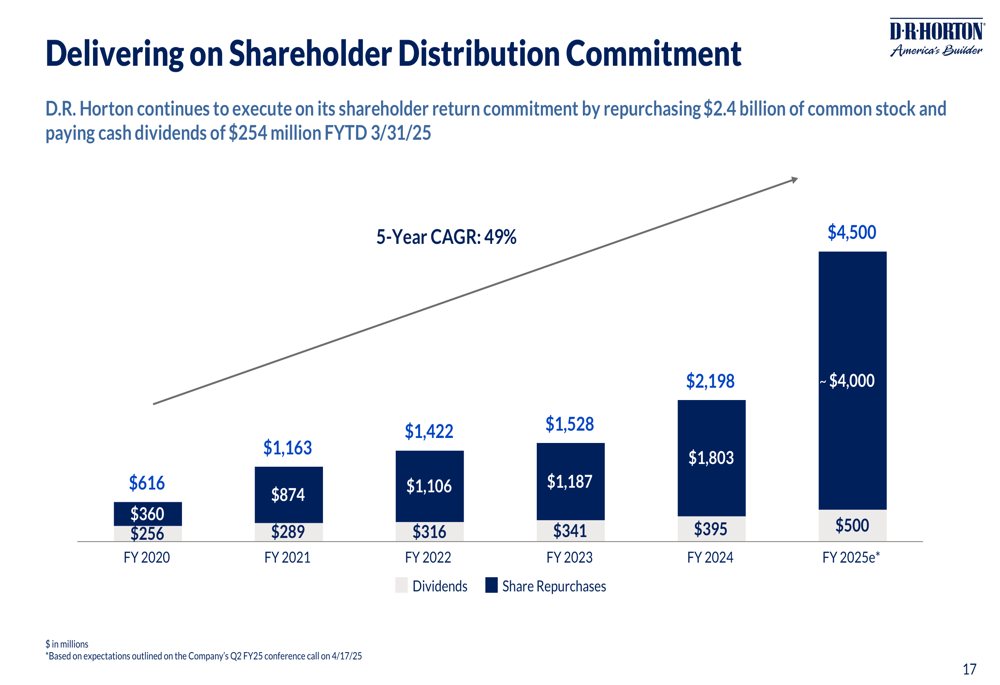

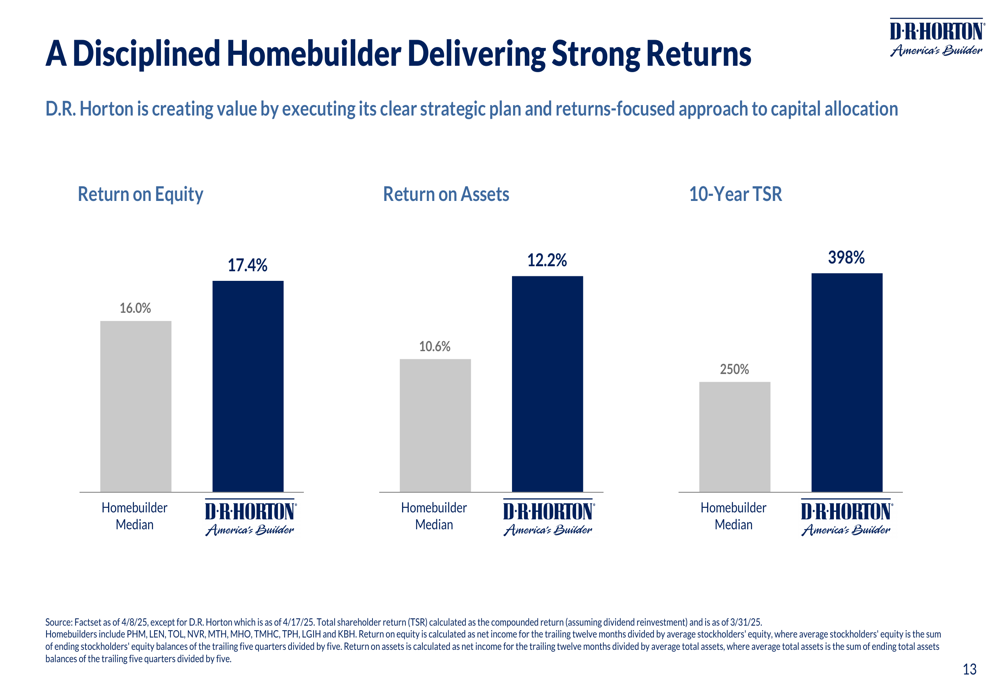

Capital Allocation & Shareholder Returns

D.R. Horton has significantly increased its commitment to shareholder returns. During Q2 FY2025, the company returned $1.4 billion to shareholders, including $1.3 billion in stock repurchases (9.7 million shares) and $125.5 million in cash dividends ($0.40 per common share).

Notably, the company has increased its fiscal 2025 share repurchase expectation from a range of $2.6-2.8 billion to approximately $4.0 billion, reflecting confidence in its financial position and future cash flow generation.

The following chart demonstrates D.R. Horton’s consistent and growing commitment to shareholder distributions:

This focus on shareholder returns has translated into superior performance compared to both industry peers and the broader market. D.R. Horton’s returns outpace the homebuilder median across key metrics, including return on equity (17.4% vs. 16.0%), return on assets (12.2% vs. 10.6%), and 10-year total shareholder return (398% vs. 250%).

The following comparison illustrates this outperformance:

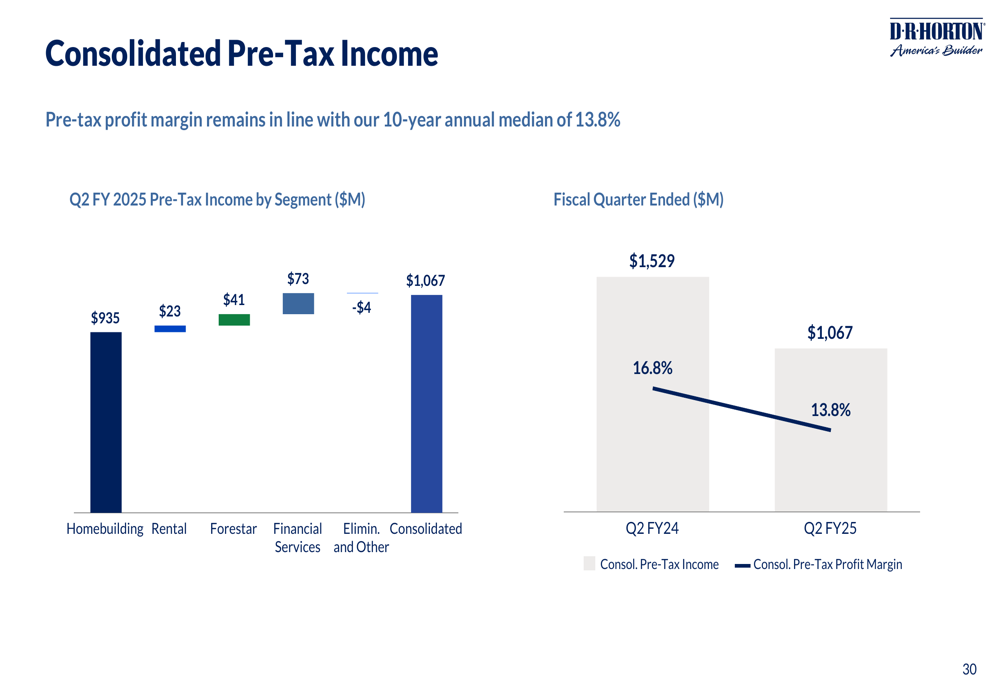

Segment Performance

D.R. Horton’s business model extends beyond traditional homebuilding to include rental operations, land development through its Forestar subsidiary, and financial services. This diversified approach provides multiple revenue streams and operational synergies.

For Q2 FY2025, the consolidated pre-tax income breakdown by segment shows the relative contribution of each business line:

The company’s homebuilding operations remain the primary driver of revenue and profit, accounting for 89% of total revenue. The geographic diversification of home closings provides resilience against regional market fluctuations, with balanced distribution across the Northwest (26%), Southwest (26%), Southeast (20%), South Central (11%), North (11%), and East (6%) regions.

Forward Outlook

Looking ahead, D.R. Horton is well-positioned to navigate market challenges while maintaining its leadership position. The company’s focus on affordable housing, operational efficiency, and strong capital allocation strategy provides a solid foundation for continued success.

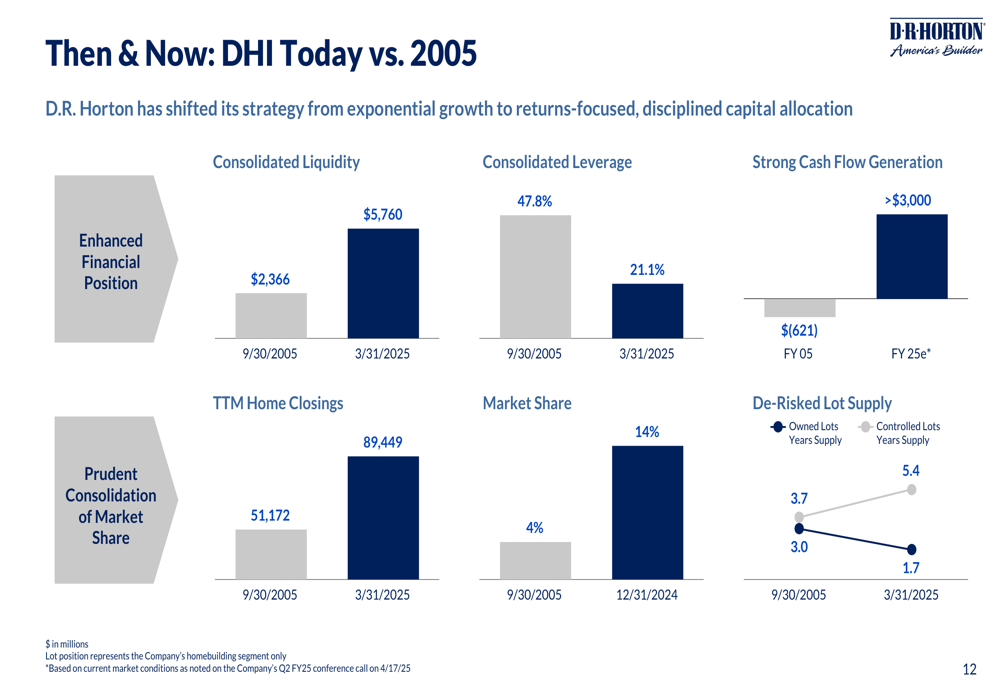

D.R. Horton has demonstrated its ability to adapt to changing market conditions, as evidenced by the strategic evolution of its business model since 2005. The company has significantly improved its financial flexibility, increasing consolidated liquidity from $2,366 million in 2005 to $5,760 million in 2025, while reducing leverage from 47.8% to 21.1% over the same period.

The following comparison highlights this transformation:

Despite near-term margin pressures, D.R. Horton’s Q2 2025 results reflect a company with strong fundamentals, market leadership, and a clear strategy focused on delivering value to shareholders. The increased share repurchase commitment signals management’s confidence in the company’s financial strength and future prospects, even as it navigates a challenging housing market environment.

With its focus on affordability, operational efficiency, and disciplined capital allocation, D.R. Horton appears well-equipped to maintain its position as America’s largest homebuilder while delivering strong returns to shareholders in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.