US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

D.R. Horton (NYSE:DHI), America’s largest homebuilder, delivered strong third-quarter results for fiscal year 2025, with shares surging over 10% in response to the positive earnings report. The company’s stock traded at $144.98 as of mid-day on July 22, 2025, reflecting investor enthusiasm for the homebuilder’s performance amid challenging market conditions.

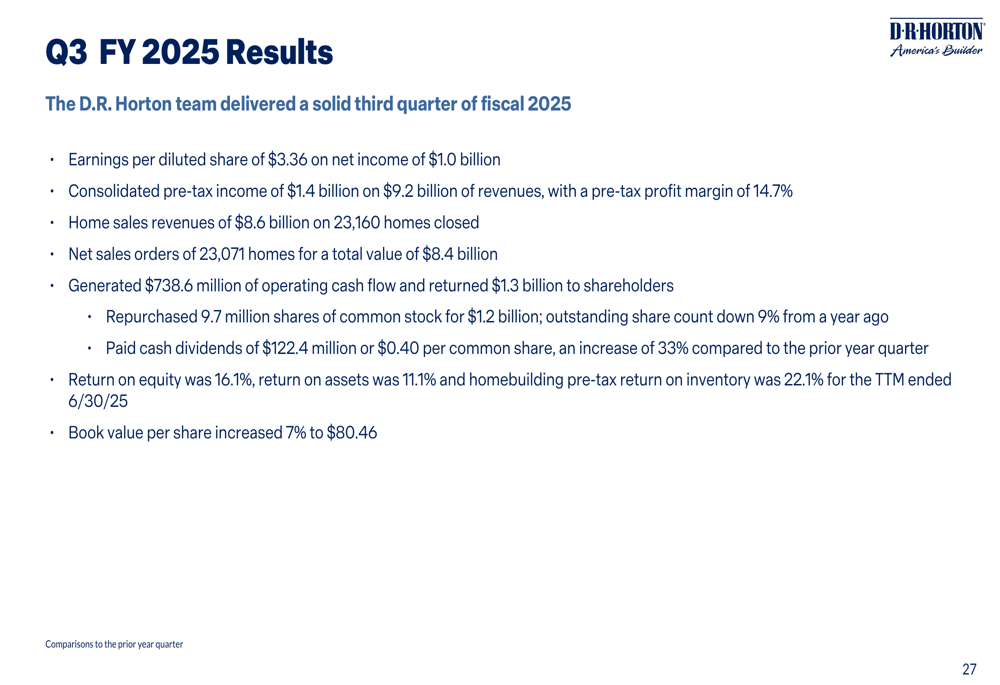

The company reported diluted earnings per share of $3.36 on net income of $1.0 billion, a significant improvement from the $2.58 EPS reported in Q2 2025, when the company missed analyst expectations. This quarter’s performance demonstrates D.R. Horton’s ability to navigate affordability constraints while maintaining strong profitability.

Quarterly Performance Highlights

D.R. Horton reported consolidated revenues of $9.2 billion for Q3 FY 2025, with a pre-tax profit margin of 14.7%. The company closed 23,160 homes during the quarter, generating home sales revenues of $8.6 billion. Net sales orders remained strong at 23,071 homes, representing a total value of $8.4 billion.

As shown in the following summary of Q3 FY 2025 results:

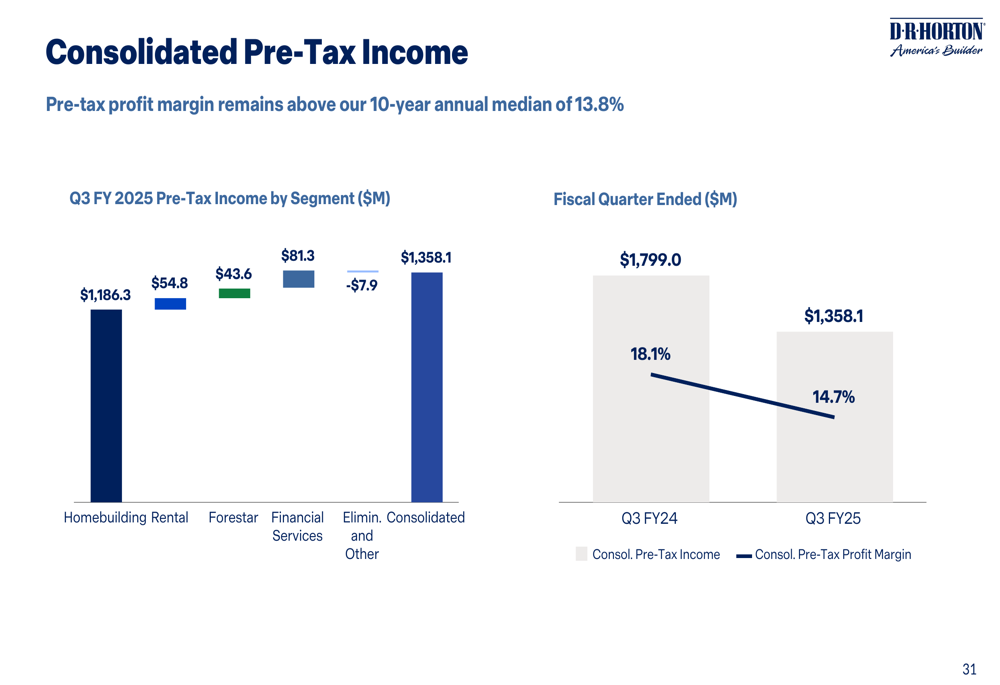

The company’s pre-tax income breakdown reveals the continued dominance of the homebuilding segment, which remains the primary driver of profitability. However, the company’s diversification into rental operations, financial services, and lot development through its Forestar subsidiary provides additional revenue streams.

The following chart illustrates the pre-tax income by segment for Q3 FY 2025:

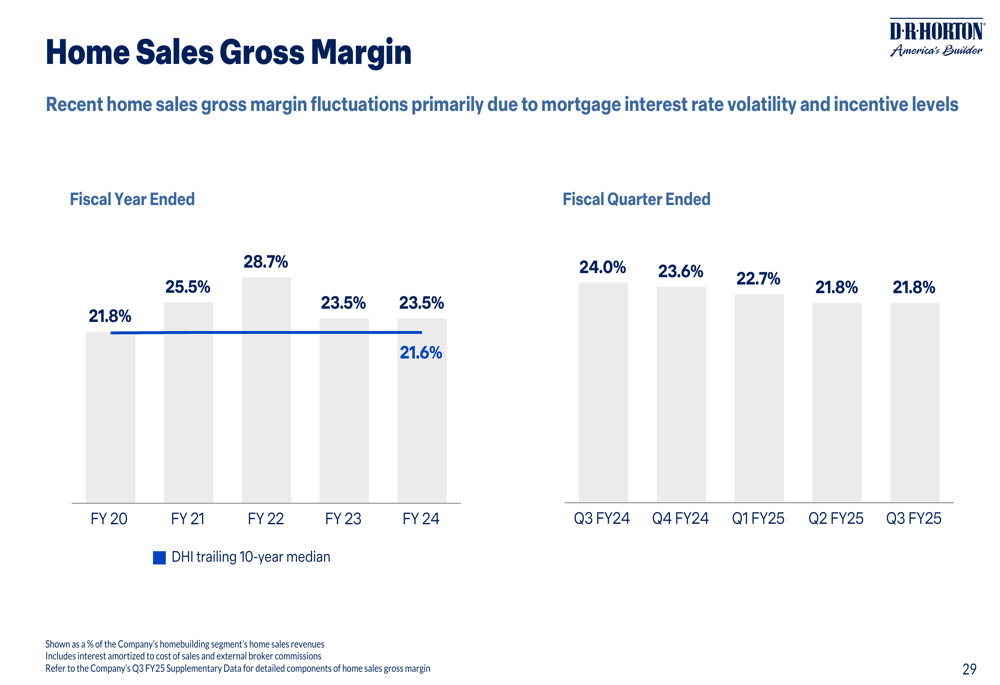

Home sales gross margin has been affected by mortgage interest rate volatility and incentive levels, as shown in the following chart tracking margin performance over time:

Strategic Initiatives

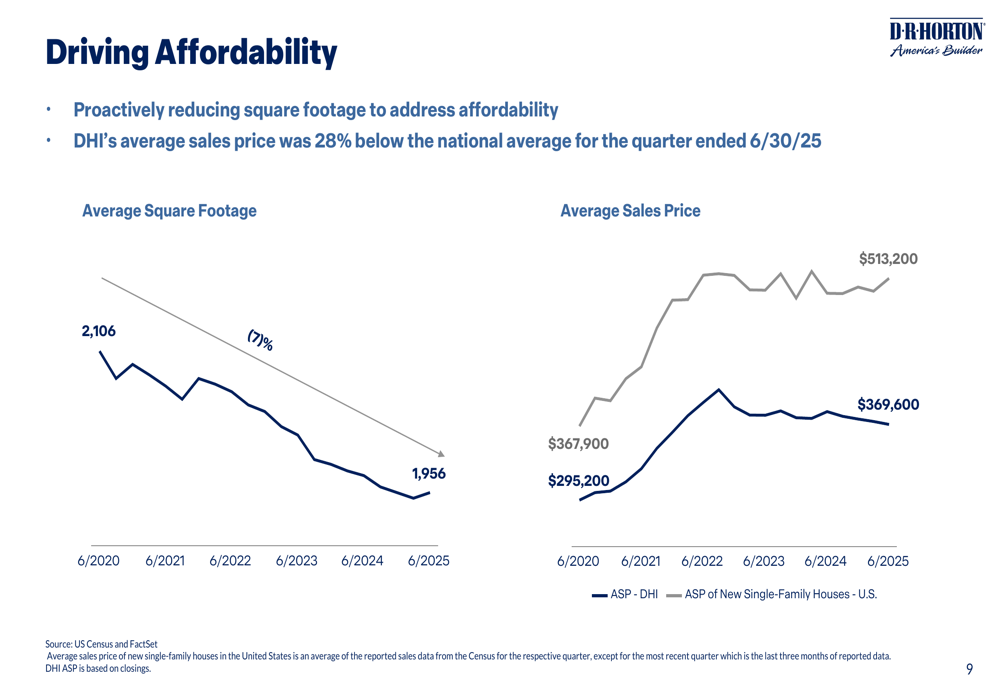

D.R. Horton’s strategy continues to focus on affordability, with the company actively reducing the average square footage of its homes to address market demands. The company’s average sales price of $369,600 during Q3 2025 was 28% below the national average of $513,200, positioning D.R. Horton favorably in a market where affordability remains a key concern.

The following chart illustrates the company’s focus on driving affordability through reduced square footage and competitive pricing:

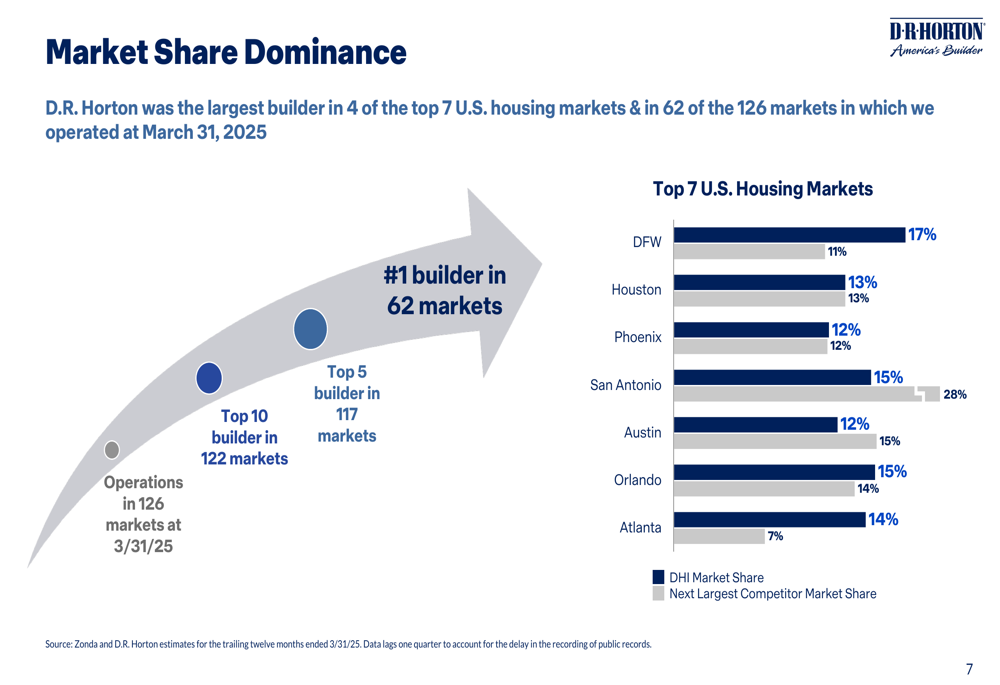

The company’s market dominance remains a key strength, with D.R. Horton ranking as the #1 builder in 62 of the 126 markets in which it operates. The company is particularly dominant in several of the nation’s largest housing markets, including Dallas-Fort Worth, Houston, and Phoenix.

As shown in the following market share comparison:

Detailed Financial Analysis

D.R. Horton has demonstrated exceptional financial performance over the past five years, with a 16% CAGR in consolidated revenues, 27% CAGR in diluted EPS, and 23% CAGR in book value per share from FY 2019 to FY 2024.

The following chart highlights this strong financial trajectory:

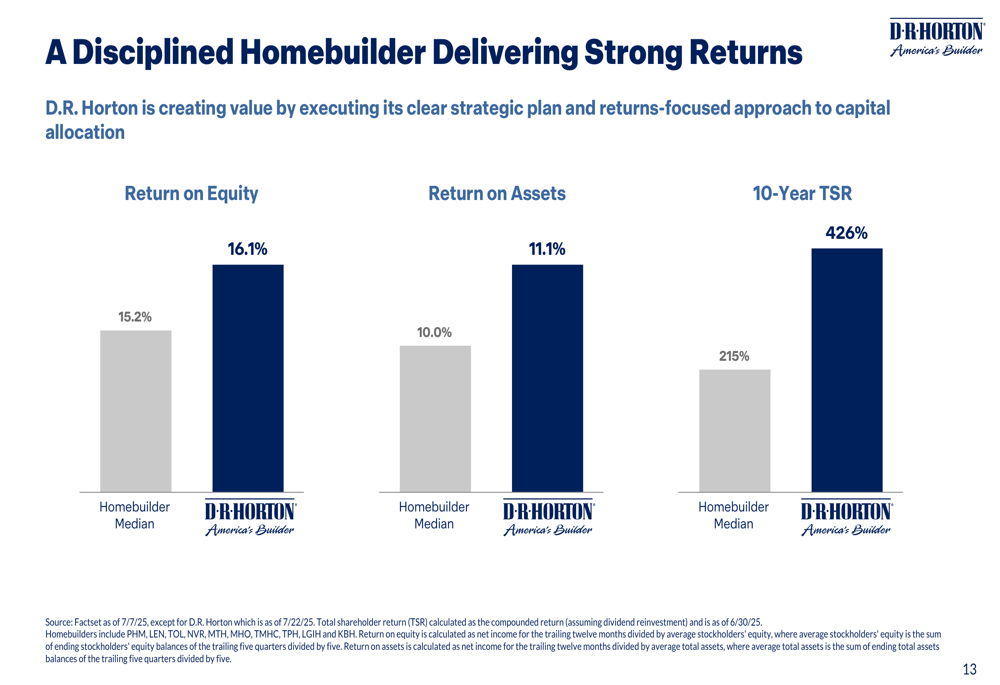

The company’s return metrics continue to outperform industry peers, with a return on equity of 16.1% compared to the homebuilder median of 15.2%, and a return on assets of 11.1% versus the industry median of 10.0%.

As illustrated in this comparison of returns versus homebuilder medians:

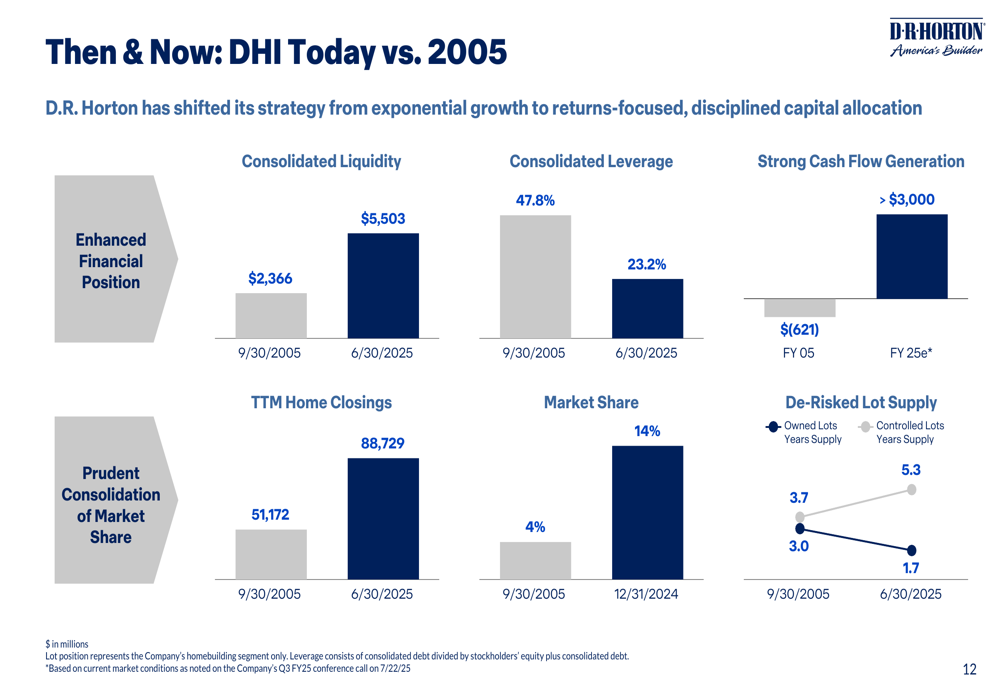

D.R. Horton has significantly transformed its business model since 2005, shifting from an exponential growth approach to a returns-focused, disciplined capital allocation strategy. This transformation has resulted in stronger liquidity, lower leverage, and improved cash flow generation.

The following comparison highlights the company’s evolution:

Capital Allocation & Shareholder Returns

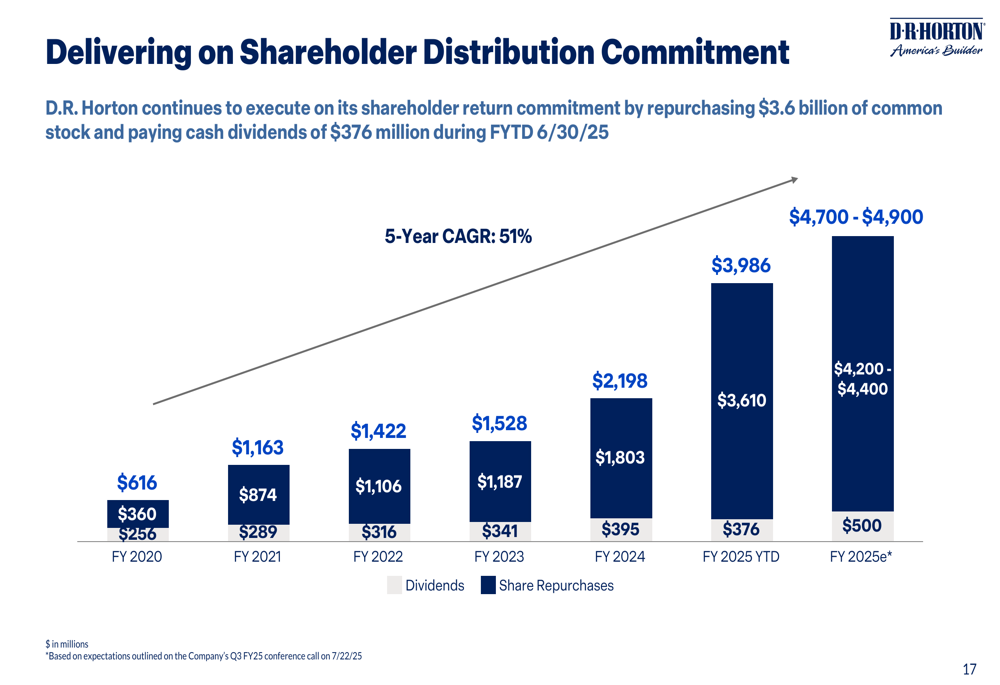

D.R. Horton continues to prioritize shareholder returns through substantial share repurchases and dividend payments. During the first nine months of FY 2025, the company has repurchased $3.6 billion of common stock and paid $376 million in dividends, with expectations to reach $4.2-$4.4 billion in share repurchases and approximately $500 million in dividends for the full fiscal year.

The following chart demonstrates the company’s commitment to shareholder returns:

The company maintains a strong financial position with a focus on conservative leverage, which has declined from 26.6% in FY 2020 to 23.2% in Q3 FY 2025. This financial discipline provides flexibility for both operational investments and shareholder returns.

Forward-Looking Statements

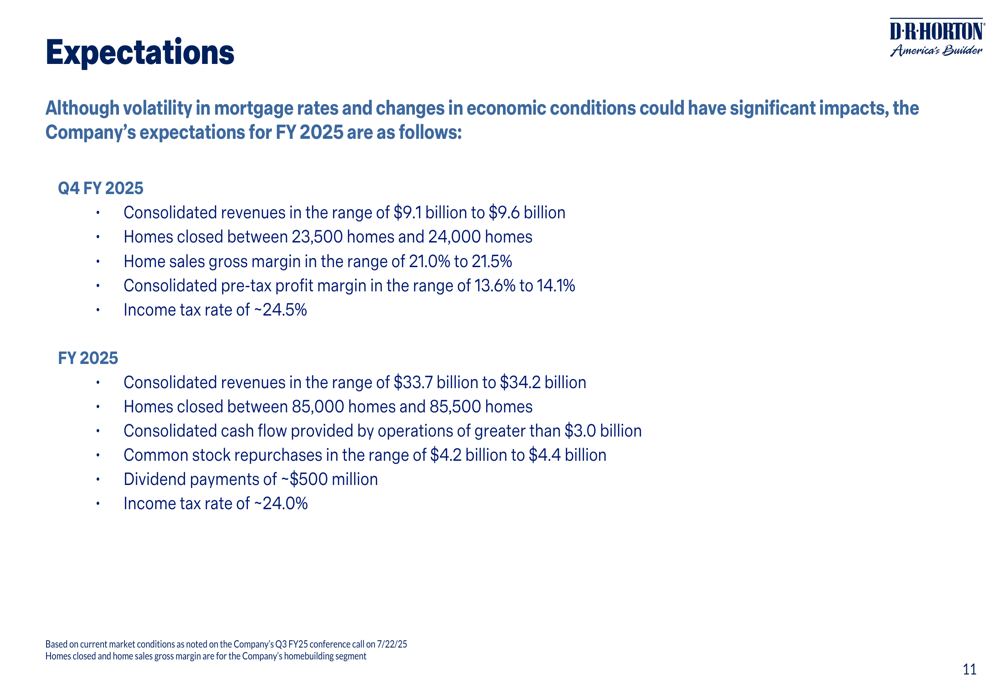

For the fourth quarter of fiscal 2025, D.R. Horton expects consolidated revenues between $9.1 billion and $9.6 billion, with homes closed ranging from 23,500 to 24,000. The company anticipates a home sales gross margin between 21.0% and 21.5%, with a consolidated pre-tax profit margin between 13.6% and 14.1%.

For the full fiscal year 2025, D.R. Horton projects consolidated revenues between $33.7 billion and $34.2 billion, with homes closed between 85,000 and 85,500. The company expects consolidated cash flow from operations to exceed $3.0 billion.

As outlined in the company’s expectations slide:

Conclusion

D.R. Horton’s Q3 2025 results demonstrate the company’s ability to navigate a challenging housing market while maintaining strong profitability and market leadership. The company’s focus on affordability, geographic diversification, and disciplined capital allocation continues to drive performance, with significant returns to shareholders through share repurchases and dividends.

The positive market reaction to these results suggests investor confidence in D.R. Horton’s strategy and execution, particularly following the EPS miss in the previous quarter. As the largest homebuilder in America, D.R. Horton remains well-positioned to capitalize on housing demand while managing affordability constraints through its diverse product offerings and price points.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.