CAC 40 falls after French Prime Minister resigns

Introduction & Market Context

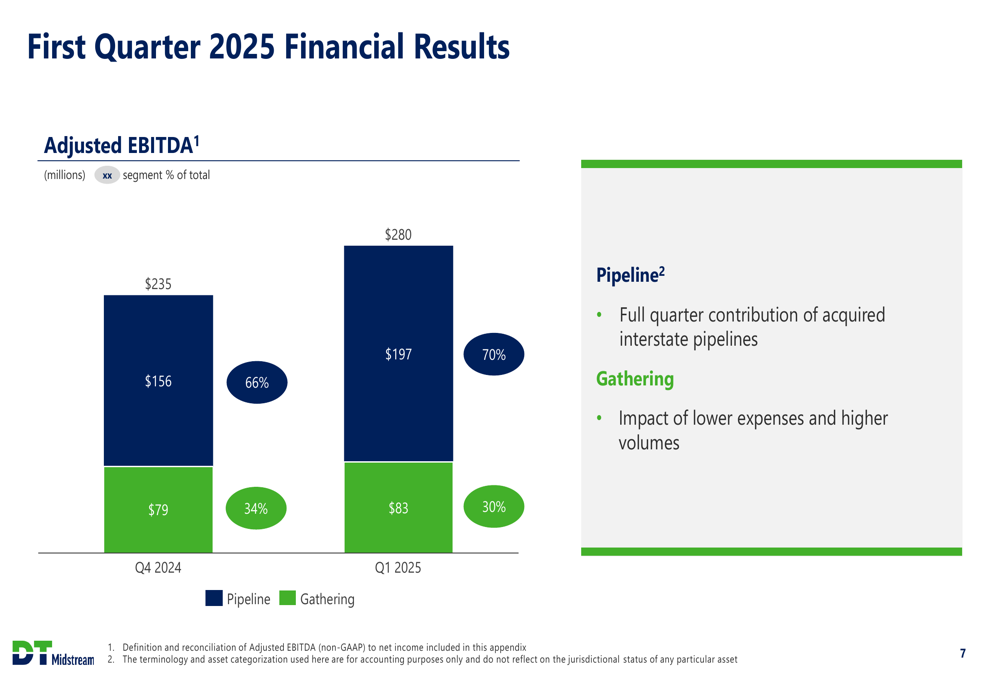

DT Midstream Inc (NYSE:DTM) reported strong first-quarter 2025 results on April 30, with net income of $108 million and Adjusted EBITDA of $280 million, representing a 19% increase from the previous quarter. The company’s stock has shown resilience, trading near $98.11 in pre-market activity, slightly down 0.43% from its previous close of $98.53.

The natural gas infrastructure company continues to benefit from its strategic acquisition of Midwest pipeline assets, with the pipeline segment now contributing 70% of total Adjusted EBITDA, up from 66% in the previous quarter. This shift aligns with the company’s long-term strategy to increase its pipeline segment contribution to approximately 70% of its business mix.

Quarterly Performance Highlights

DT Midstream reported Q1 2025 Operating EPS of $1.06, up from $0.94 in Q4 2024, reflecting strong operational performance across its business segments. The company’s Adjusted EBITDA reached $280 million, with the pipeline segment contributing $197 million (70%) and the gathering segment adding $83 million (30%).

As shown in the following chart of quarterly financial results, the company saw significant improvement across key metrics:

Distributable Cash Flow increased substantially to $250 million in Q1 2025 from $133 million in Q4 2024, providing ample financial flexibility for the company’s growth initiatives and shareholder returns. Growth capital expenditures were $63 million during the quarter, significantly lower than the $1,277 million in Q4 2024, which included the major Midwest pipeline acquisition.

The company highlighted three key accomplishments for the quarter:

Strategic Initiatives

The integration of acquired Midwest pipeline assets is progressing according to plan, with the company reporting high pipeline utilization during the winter season. DT Midstream has already completed the financial system integration within 90 days of acquisition, and remaining integration milestones are on track for completion by year-end.

"We’ve onboarded all key employees and fully integrated the assets into our financial system within 90 days," the company noted in its presentation. DT Midstream has also commenced construction activities on the Midwestern Gas Transmission lateral to serve AES (NYSE:AES) Indiana’s Petersburg Generating Station, demonstrating its ability to leverage the expanded footprint for new commercial opportunities.

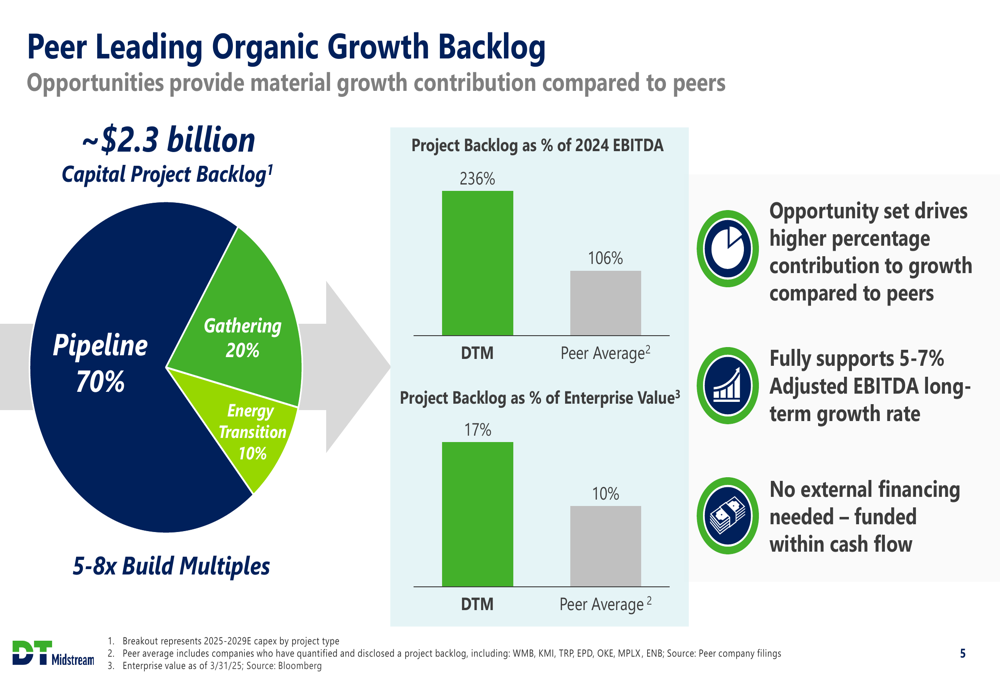

The company continues to execute on its approximately $2.3 billion organic project backlog, with several key projects progressing on schedule and on budget. These projects include the Haynesville LEAP expansion, Stonewall to Mountain Valley Pipeline expansion, and various gathering system expansions in Appalachia and Haynesville.

The company’s project backlog as a percentage of 2024 EBITDA stands at an impressive 236%, significantly outpacing the peer average of 106%, highlighting DT Midstream’s strong growth trajectory.

Competitive Industry Position

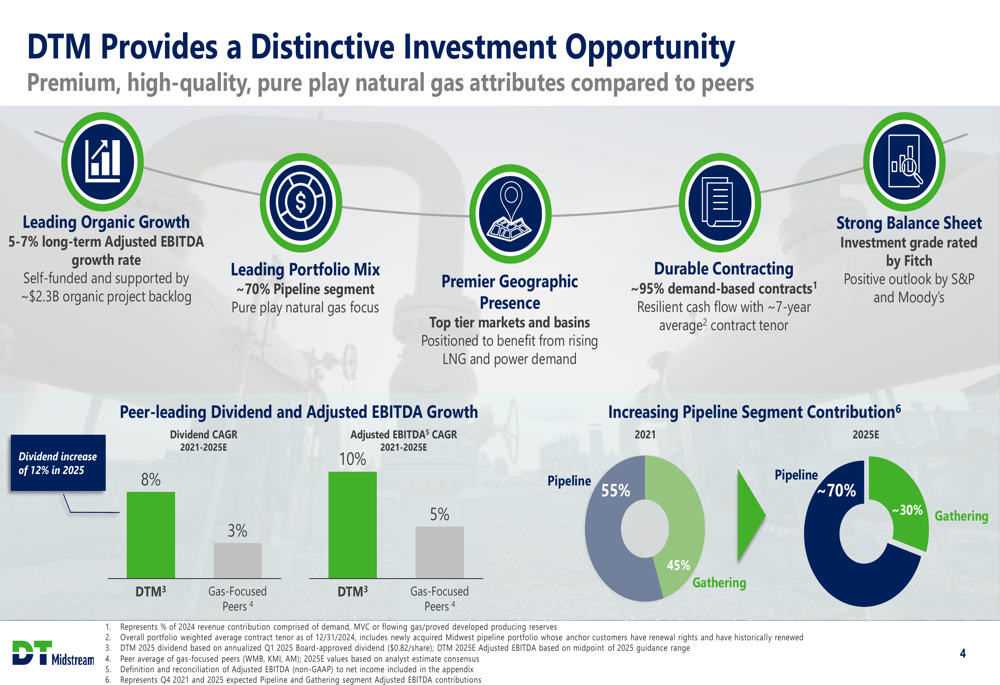

DT Midstream emphasized its distinctive investment opportunity compared to peers, highlighting its leading organic growth, premier portfolio mix, and strong geographic presence in top-tier markets and basins. The company is well-positioned to benefit from rising LNG and power demand, with approximately 95% of contracts being demand-based with an average tenor of about 7 years.

The following slide illustrates the company’s competitive positioning:

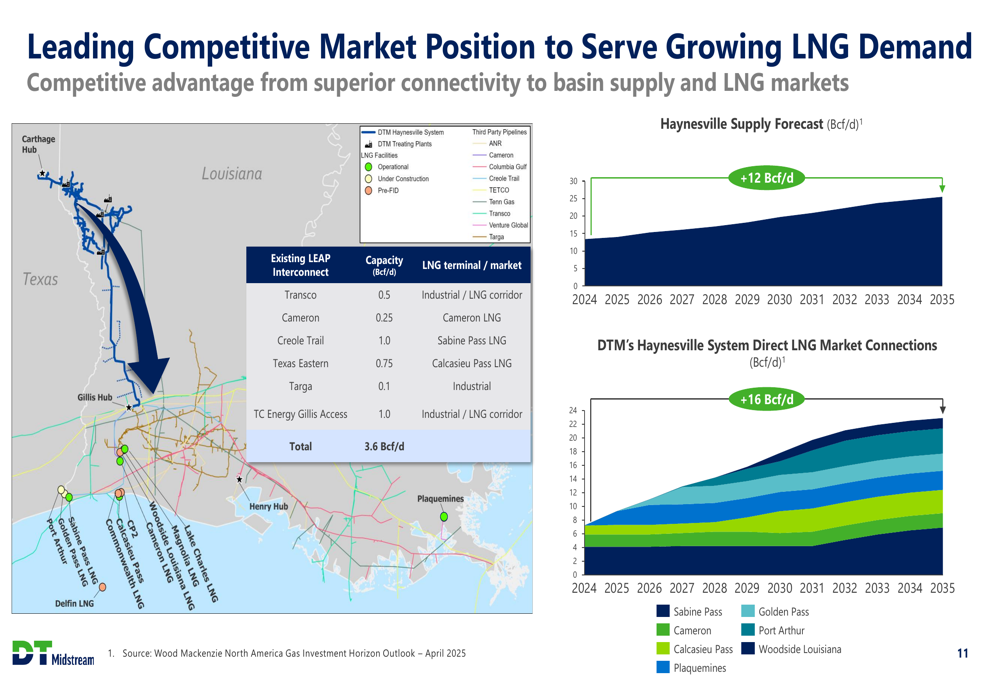

The company’s Haynesville system is strategically positioned to serve growing LNG demand, with direct connections to multiple LNG export facilities totaling over 16 Bcf/d of capacity. This positioning is crucial as U.S. natural gas demand is forecast to grow from 113 Bcf/d in 2025 to 132 Bcf/d by 2030, driven primarily by LNG exports and power generation.

DT Midstream’s competitive market position to serve this growing demand is illustrated in the following chart:

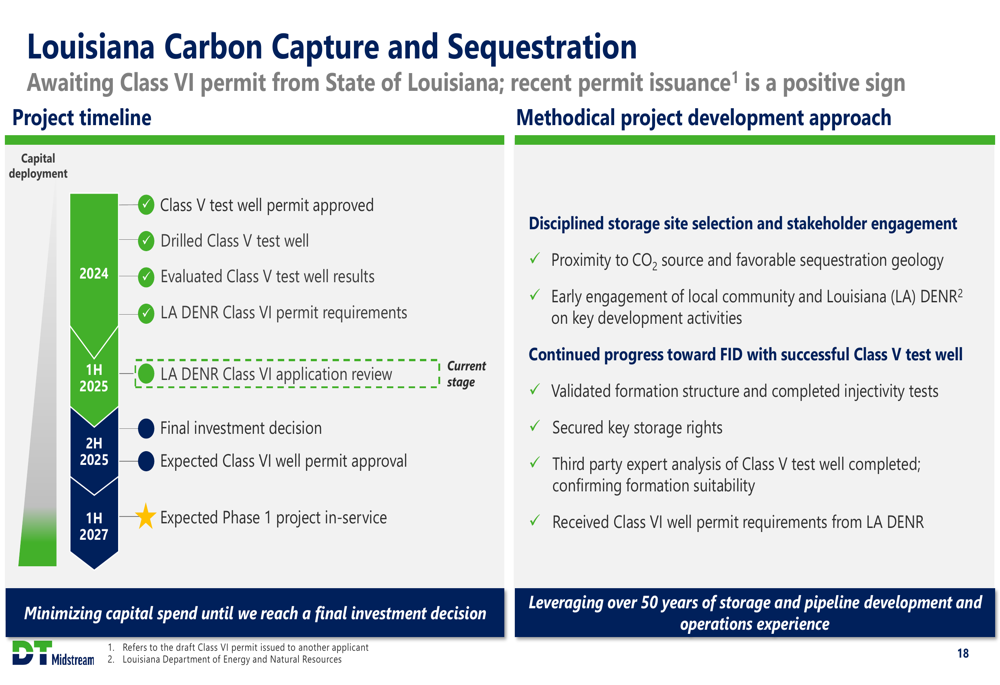

The company is also advancing its Louisiana Carbon Capture and Sequestration project, having completed drilling of a Class V test well and evaluated the results. This initiative aligns with the industry’s increasing focus on reducing carbon emissions and demonstrates DT Midstream’s commitment to sustainable operations.

Forward-Looking Statements

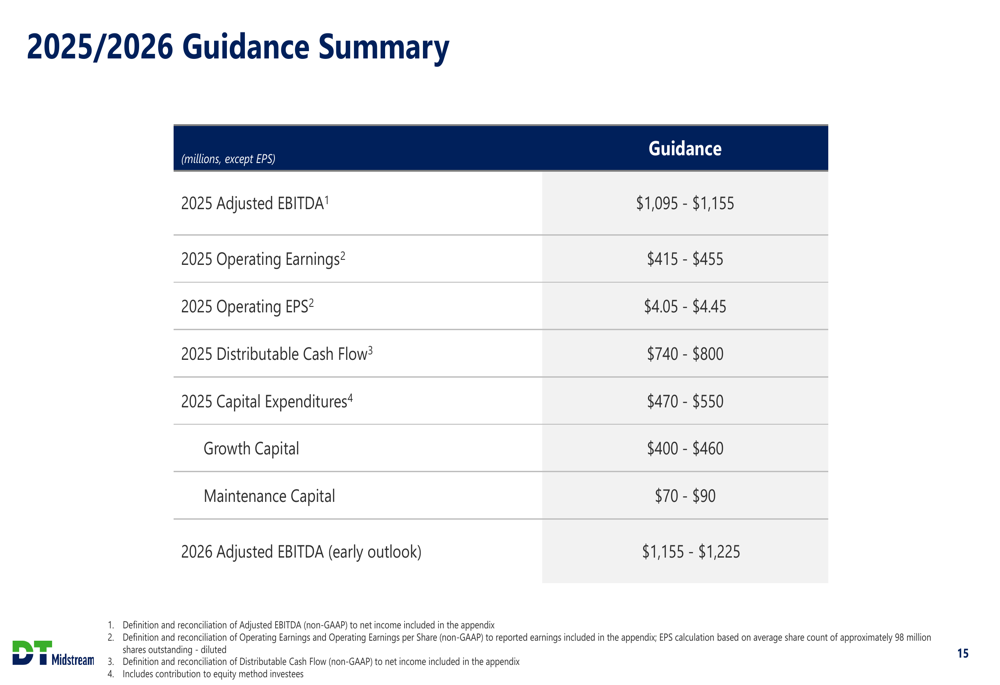

DT Midstream reaffirmed its 2025 Adjusted EBITDA guidance range of $1,095-$1,155 million and its early outlook for 2026 of $1,155-$1,225 million. The company expects to maintain its 5-7% long-term Adjusted EBITDA growth rate, supported by its robust project backlog.

The 2025/2026 guidance summary provides a comprehensive view of the company’s financial expectations:

The company’s capital plan for 2025 and 2026 is largely committed, with total investments of approximately $465 million over the two-year period. DT Midstream emphasized that it is self-funding its organic growth projects from the $2.3 billion capital backlog, with no need for external financing.

"We’re advancing projects towards final investment decisions to utilize 2026 free cash flow," the company stated, indicating a disciplined approach to capital allocation while maintaining growth momentum.

The LEAP Phase 4 expansion represents a significant growth opportunity, increasing capacity from 1.9 Bcf/d to 2.1 Bcf/d. This project, expected to be in service in the first half of 2026, is underpinned by new long-term, demand-based contracts with two new customers.

With strong U.S. demand and production fundamentals, particularly in its core Haynesville and Appalachia basins, DT Midstream appears well-positioned to continue its growth trajectory and deliver value to shareholders through both capital appreciation and its recently increased dividend.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.