Trump signs order raising Canada tariffs to 35% from 25%

Introduction & Market Context

Dun & Bradstreet (NYSE:DNB) released its first quarter 2025 financial results on May 1, showing modest revenue growth and improved profitability metrics compared to the previous year. The results come after a disappointing fourth quarter 2024, when the company missed both earnings and revenue expectations, causing its stock to drop significantly.

Currently trading at $8.97, DNB shares remain near their 52-week low of $7.78, reflecting ongoing investor concerns about the company’s growth trajectory and high debt levels. The company continues to undergo a strategic review process that began in late 2024.

Quarterly Performance Highlights

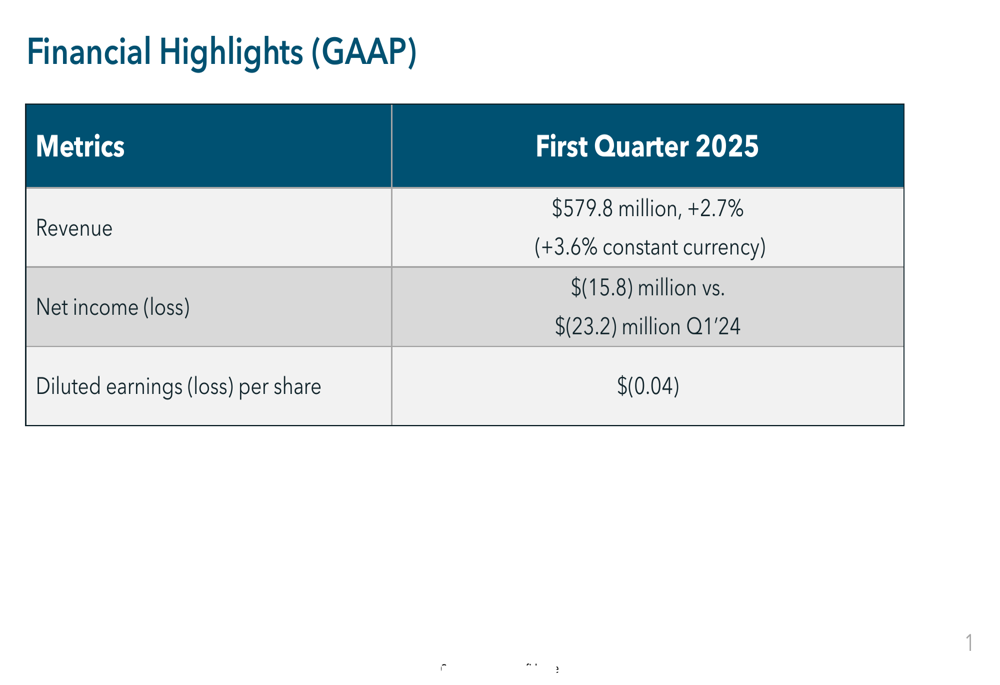

Dun & Bradstreet reported first-quarter revenue of $579.8 million, representing a 2.7% increase year-over-year, or 3.6% growth in constant currency. This marks a slight improvement from the less than 1% growth seen in Q4 2024.

The company reduced its GAAP net loss to $15.8 million, compared to a $23.2 million loss in the same quarter last year. Diluted loss per share was $0.04 for the quarter.

As shown in the following financial highlights table:

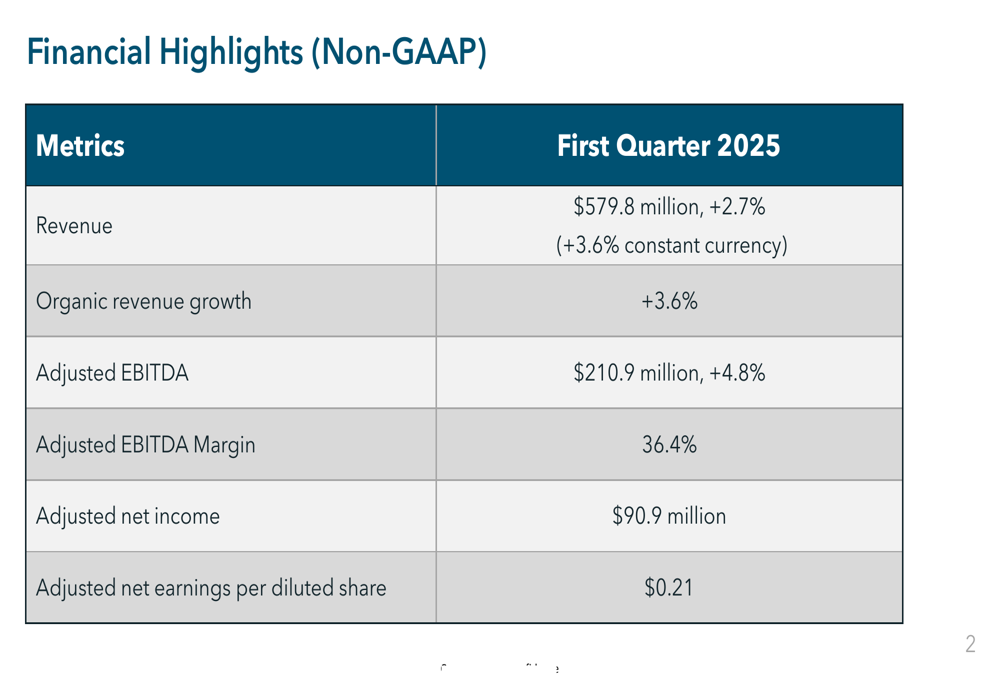

On a non-GAAP basis, the company’s results showed more positive momentum. Adjusted EBITDA increased 4.8% to $210.9 million, with an adjusted EBITDA margin of 36.4%. Adjusted net income reached $90.9 million, translating to adjusted earnings per diluted share of $0.21.

The following non-GAAP financial highlights provide additional context:

Regional Performance Analysis

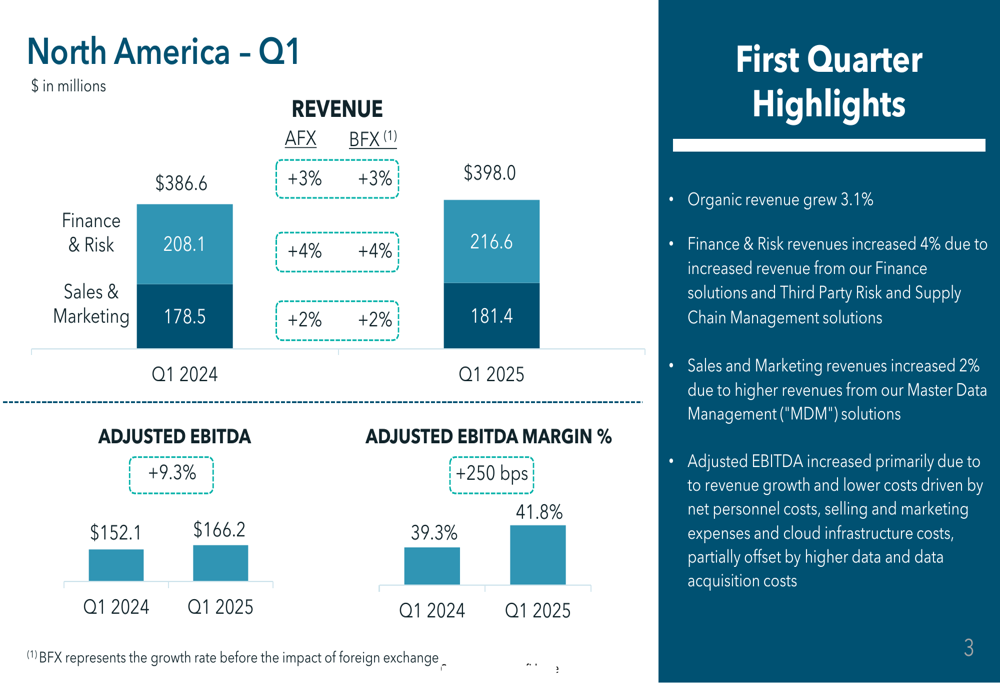

North America emerged as the primary growth driver for Dun & Bradstreet in Q1 2025, with total revenue reaching $398.0 million, a 3% increase from $386.6 million in Q1 2024. The region’s adjusted EBITDA showed even stronger improvement, growing 9.3% to $166.2 million, with margins expanding 250 basis points to 41.8%.

The company attributed North America’s performance to increased revenue from Finance solutions, Third Party Risk and Supply Chain Management solutions, and Master Data Management offerings. Cost reductions in personnel, marketing, and cloud infrastructure also contributed to the improved profitability.

The North America segment’s detailed performance is illustrated below:

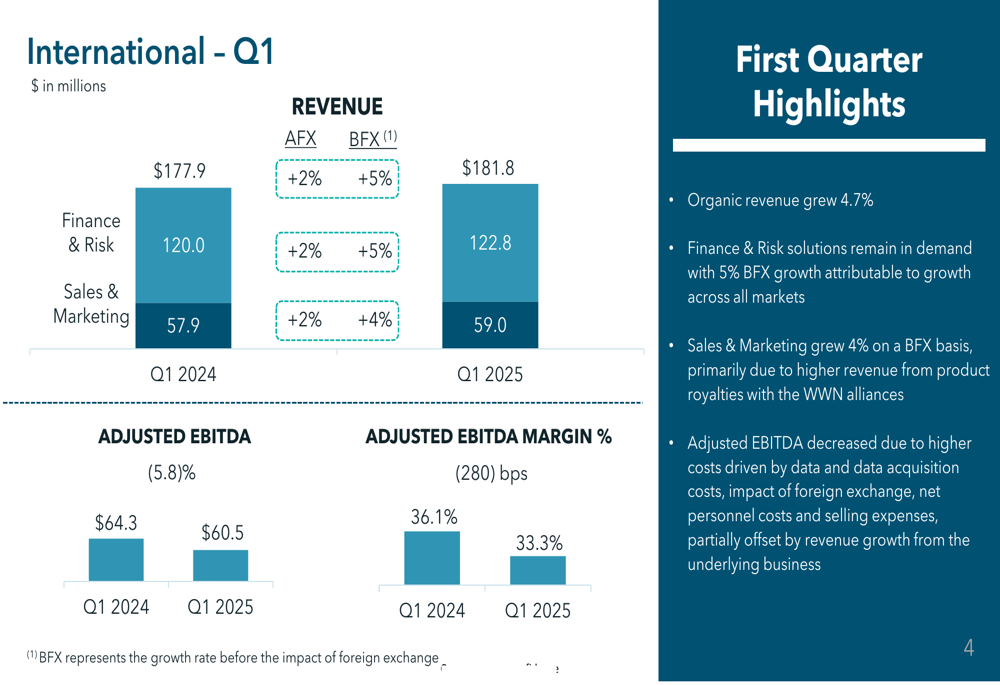

In contrast, the International segment faced more significant challenges despite posting revenue growth. International revenue increased to $181.8 million, up from $177.9 million in Q1 2024, representing 2% growth as reported and 4.7% organic growth.

However, International adjusted EBITDA declined 5.8% to $60.5 million, with margins contracting 280 basis points to 33.3%. The company cited higher data acquisition costs, foreign exchange impacts, and increased personnel and selling expenses as factors offsetting revenue growth.

The following chart details the International segment’s performance:

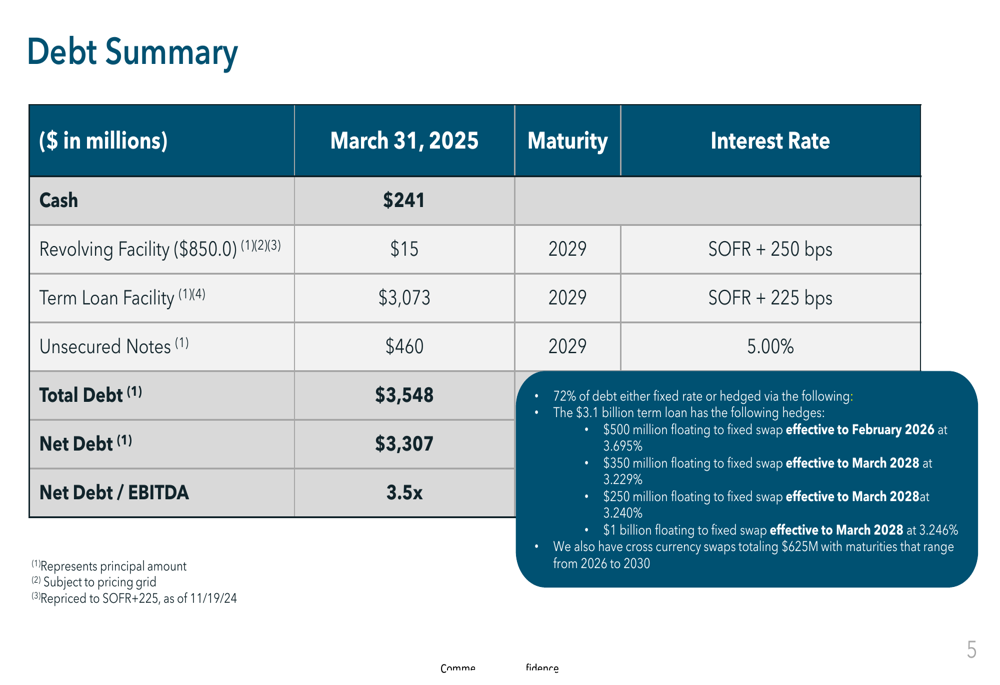

Debt Position and Financial Health

Dun & Bradstreet continues to manage a substantial debt load, with total debt of $3,548 million as of March 31, 2025. Net debt stood at $3,307 million, resulting in a net debt to EBITDA ratio of 3.5x.

This represents a slight improvement from the 3.6x leverage ratio reported at the end of 2024, but remains above the company’s target of 3.25x by the end of 2025. The company has taken steps to manage interest rate risk, with 72% of its debt either at fixed rates or hedged.

The company’s debt structure is detailed in the following summary:

Forward Outlook

While the Q1 2025 presentation did not include specific forward guidance, Dun & Bradstreet’s recent earnings call indicated revenue projections between $440 million and $500 million for 2025, representing growth of 2.5% to 5%. The company has also targeted adjusted EBITDA between $955 million and $985 million for the full year.

The modest revenue growth in Q1 2025 (3.6% organic) suggests the company is making progress toward its medium-term goal of 5-7% organic growth, though challenges remain, particularly in the International segment.

The ongoing strategic review process, expected to conclude in the first half of 2025, continues to create some uncertainty around the company’s future direction. Investors will be watching closely for any announcements regarding potential structural changes or strategic initiatives resulting from this review.

Dun & Bradstreet’s focus on AI-powered solutions and risk analytics, highlighted in previous communications, remains central to its growth strategy as the company works to leverage its extensive global data coverage in an increasingly competitive market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.