September looms as a risk month for stocks, Yardeni says

Dundee Precious Metals Inc . (TSX:DPM) presented its second-quarter 2025 results on August 1, showing record financial performance despite rising production costs. The company reported significant year-over-year growth in revenue and earnings while maintaining its full-year guidance with expectations for higher production in the second half of the year.

Quarterly Performance Highlights

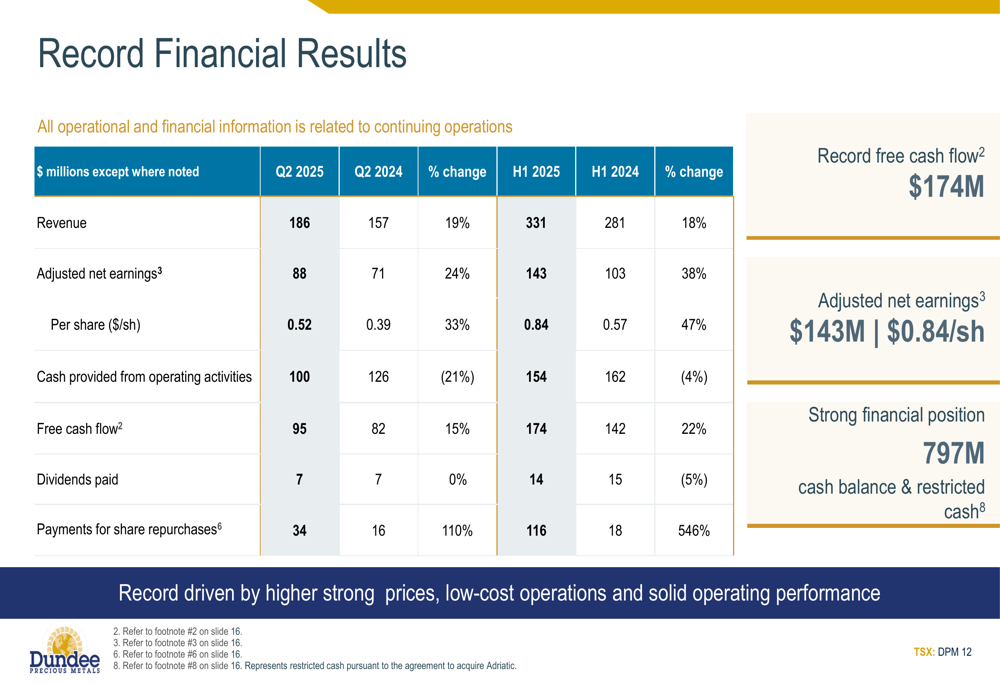

Dundee Precious Metals delivered strong financial results in Q2 2025, with revenue reaching $186 million, a 19% increase compared to Q2 2024. Adjusted net earnings rose to $88 million ($0.52 per share), representing a 24% increase from the previous year.

"Record driven by higher strong prices, low-cost operations and solid operating performance," the company stated in its presentation.

This performance marks a significant improvement from Q1 2025, when the company missed analyst expectations with EPS of $0.32 versus a forecast of $0.3779.

As shown in the following chart of quarterly financial metrics:

The company generated $95 million in free cash flow during Q2, a 15% increase year-over-year. For the first half of 2025, free cash flow reached a record $174 million, up 22% compared to H1 2024.

Detailed Financial Analysis

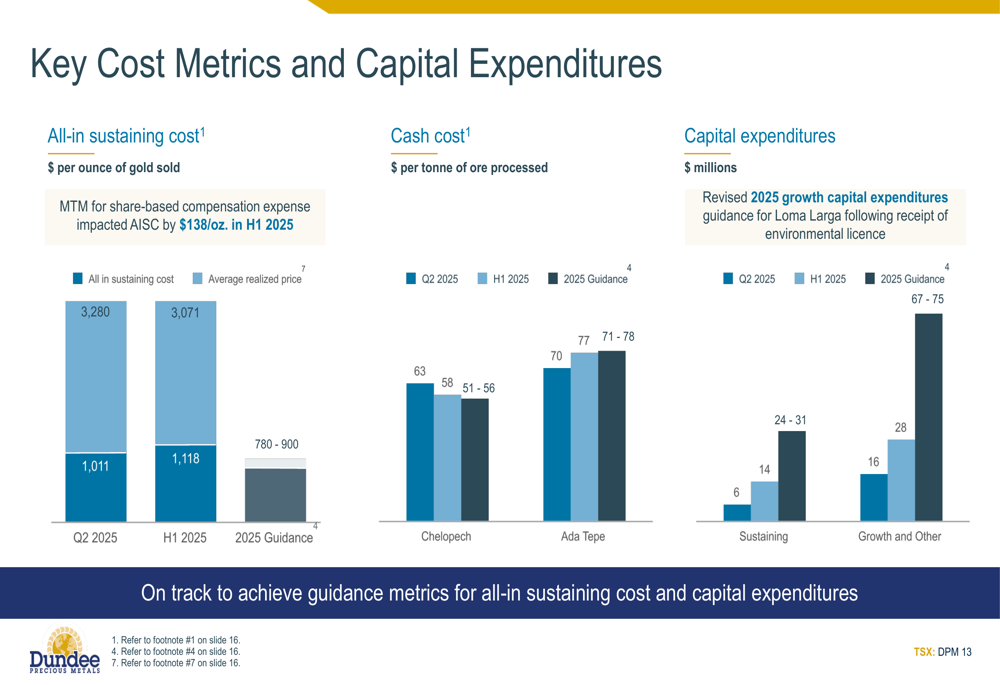

While financial results were strong, production costs have increased significantly. The all-in sustaining cost (AISC) for Q2 2025 was $1,011 per ounce of gold sold, with H1 2025 at $1,118 per ounce. These figures are notably higher than the 2025 guidance range of $780-900 per ounce.

The cost metrics and capital expenditures are illustrated in the following chart:

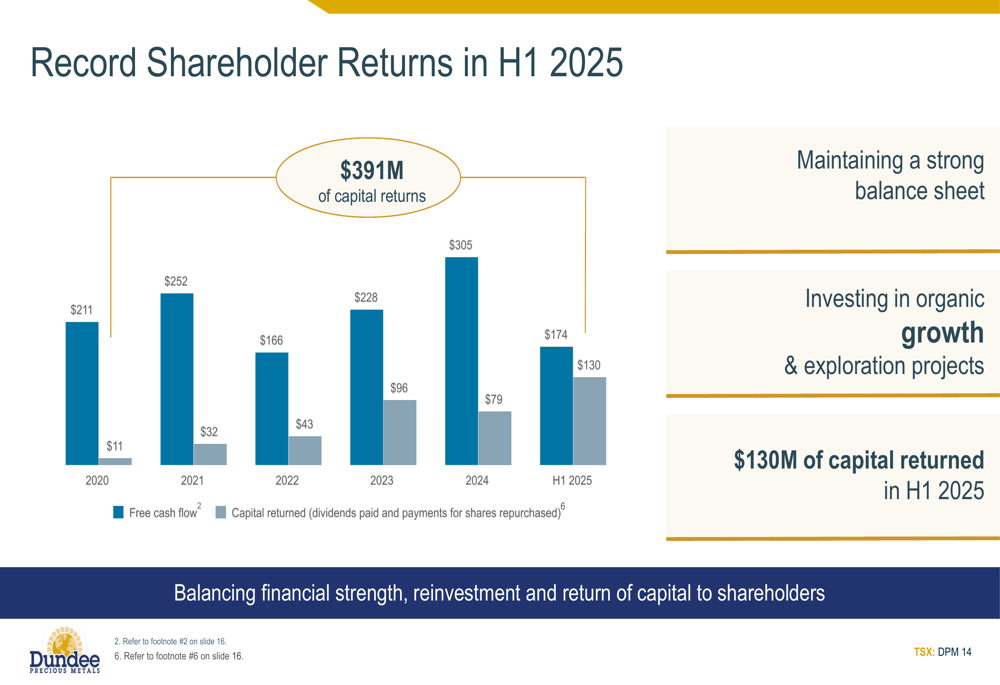

Despite rising costs, Dundee Precious Metals maintained a robust balance sheet with a cash position of $797 million, up from $763 million reported at the end of Q1 2025. The company has continued its shareholder return program, paying $7 million in dividends during Q2 and significantly increasing share repurchases to $34 million, a 110% increase compared to Q2 2024.

The company’s capital return strategy is highlighted in this chart showing the progression of shareholder returns:

" Total (EPA:TTEF) of $391M of capital returns," the company noted, with $130 million returned to shareholders in just the first half of 2025, representing a substantial increase from previous periods.

Operating Performance

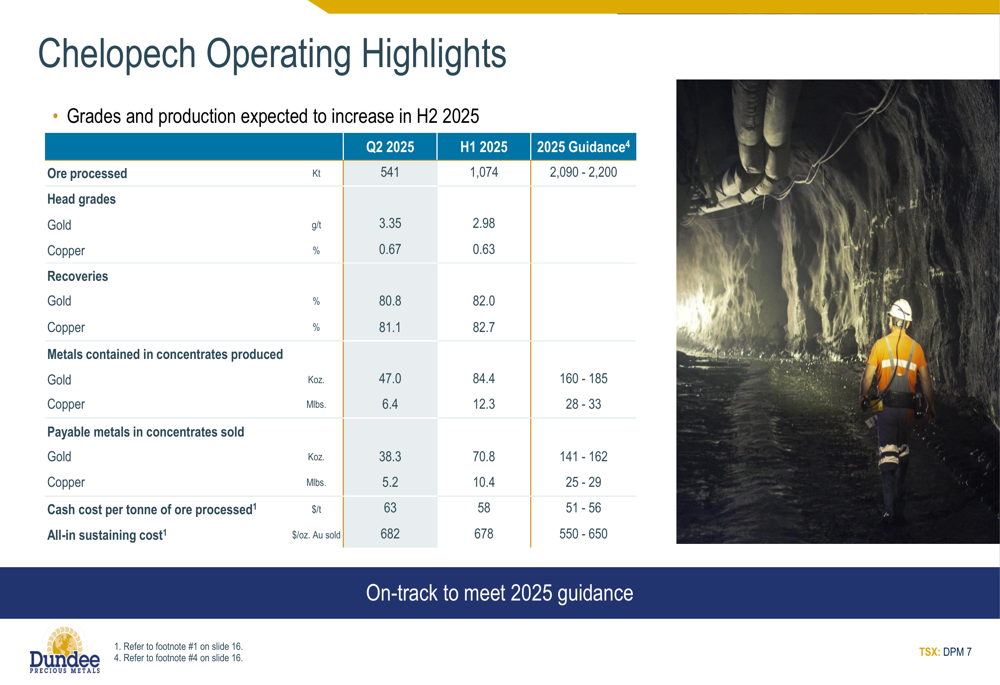

Production at both the Chelopech and Ada Tepe mines was lower than anticipated in the first half of the year, but the company expects a significant increase in the second half to meet full-year guidance.

At Chelopech, gold production reached 47.0 thousand ounces in Q2 2025, bringing the first-half total to 84.4 thousand ounces against full-year guidance of 160-185 thousand ounces. Copper production was similarly positioned to increase in H2, with 6.4 million pounds produced in Q2 and 12.3 million pounds in H1 against guidance of 28-33 million pounds for the year.

The following chart details Chelopech’s operating metrics:

Ada Tepe’s production is expected to nearly double in the second half of 2025 compared to H1. The mine produced 14.2 thousand ounces of gold in Q2 and 26.6 thousand ounces in H1, with full-year guidance of 65-80 thousand ounces.

The Ada Tepe operating highlights are shown in this chart:

Strategic Growth Initiatives

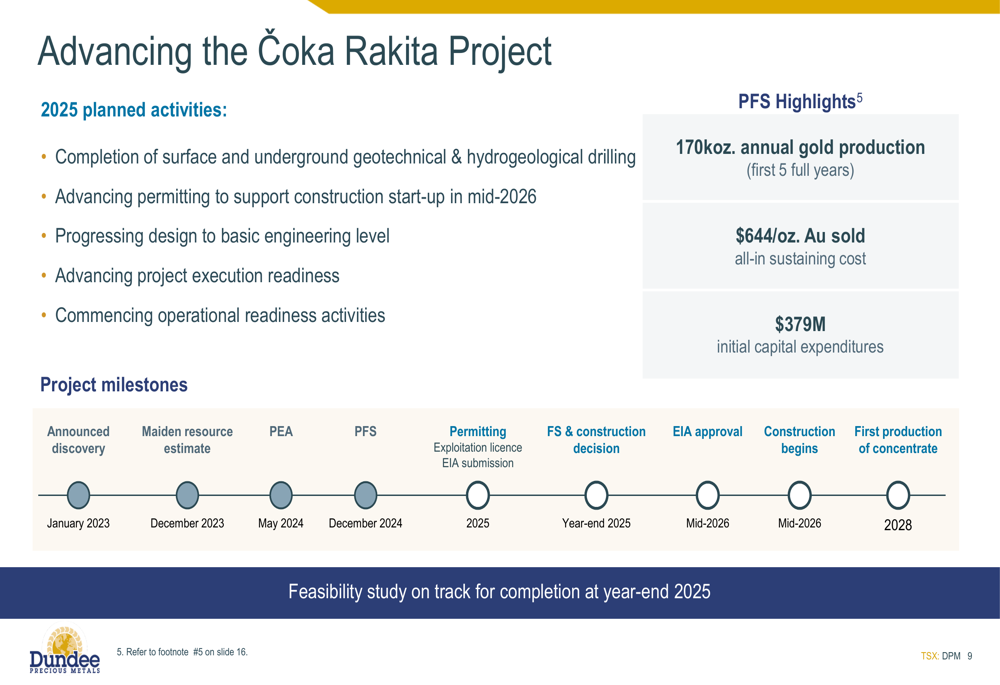

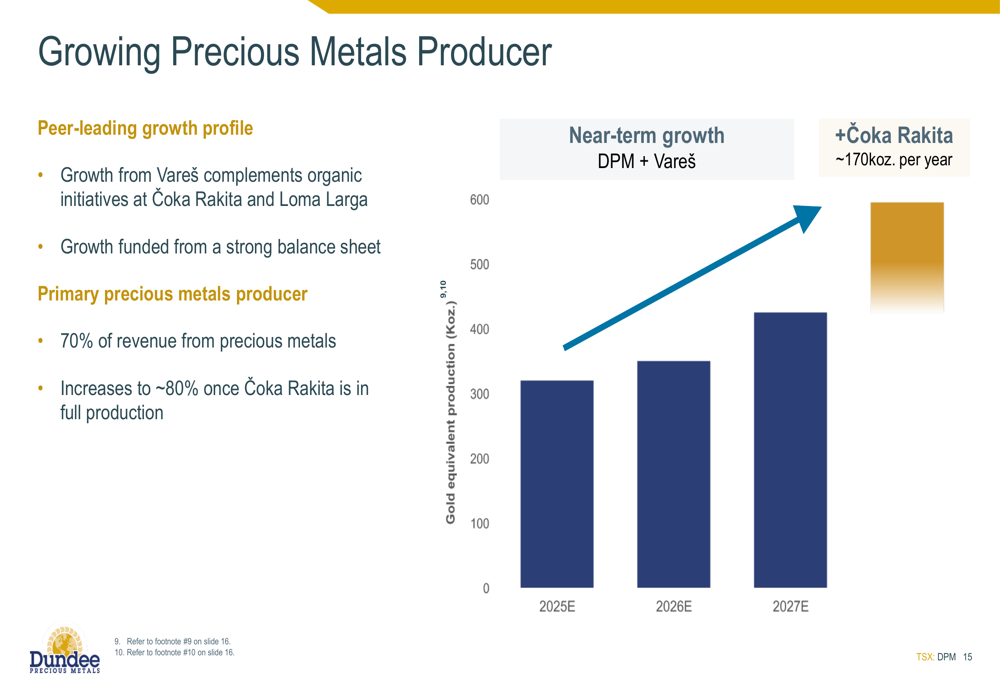

Dundee Precious Metals continues to advance its growth pipeline, with significant progress on the Čoka Rakita project. The company expects to complete a feasibility study by the end of 2025, with first production targeted for 2028. The project is anticipated to produce approximately 170,000 ounces of gold annually during its first five years of operation, with an all-in sustaining cost of $644 per ounce.

The timeline and key metrics for the Čoka Rakita project are illustrated in this chart:

The company also reported progress on the Loma Larga project, having received an environmental license in Q2 2025. The Ministry of Energy and Mines has completed the free, prior, and informed consultation process, and the company received notice of a 25-year extension of the Cristal concession.

Additionally, Dundee Precious Metals is positioning itself as a growing precious metals producer, with plans to increase its gold production significantly in the coming years.

The company is also pursuing an acquisition strategy, with the proposed Adriatic acquisition intended to create what it calls a "Premier Mining Business" with a "peer-leading growth profile."

Forward-Looking Statements

Looking ahead, Dundee Precious Metals remains confident in meeting its 2025 production and cost guidance, despite the lower production in the first half of the year. The company’s strong cash position provides flexibility to continue investing in growth projects while maintaining its shareholder return program.

The rising costs remain a concern, as noted in the Q1 2025 earnings report, which highlighted a 41% year-over-year increase in all-in sustaining costs. However, the company’s ability to generate record free cash flow despite these challenges suggests operational resilience.

Dundee Precious Metals stock closed at $22.40 on July 31, 2025, down 0.44% for the day. The stock has traded between $11.22 and $23.74 over the past 52 weeks, indicating strong performance despite recent market volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.