Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Dustin Group AB (DUST) presented its third-quarter results for fiscal year 2024/25 on July 2, 2025, highlighting a challenging business environment but showcasing efforts to strengthen its financial position. The IT solutions provider, currently trading at 2.38, has seen its stock under pressure with a 52-week range of 1.87-11.81, reflecting the broader challenges in the IT sector and the company’s ongoing transformation efforts.

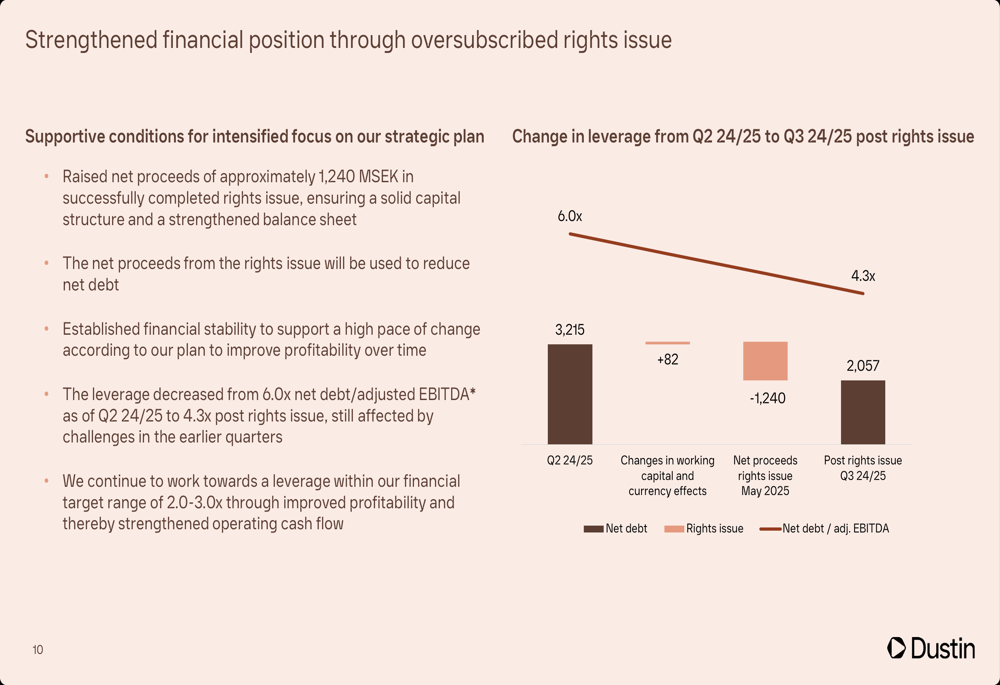

The quarter was marked by declining sales and profitability metrics, particularly in the Benelux region, though the company noted some signs of stabilization in its Nordic markets. A successful rights issue has significantly improved Dustin’s leverage position, providing breathing room as the company implements efficiency measures and strategic adjustments.

Quarterly Performance Highlights

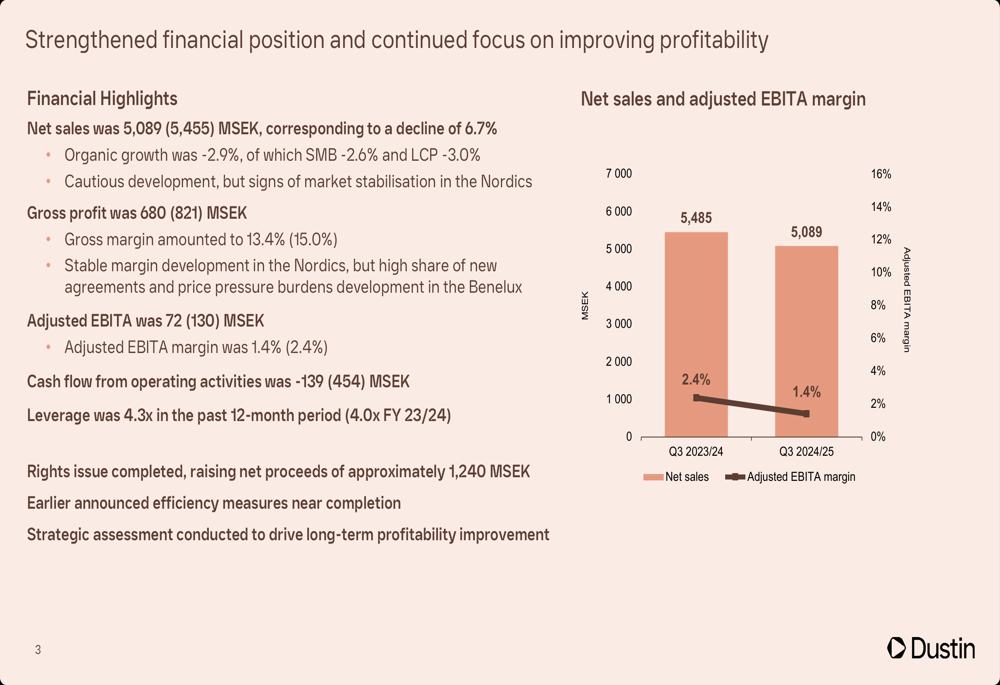

Dustin reported net sales of 5,089 MSEK for Q3 2024/25, representing a 6.7% decline from 5,455 MSEK in the same period last year. Organic growth was negative at -2.9%. The company’s adjusted EBITA fell to 72 MSEK from 130 MSEK, with the margin contracting to 1.4% from 2.4% in the prior-year quarter.

As shown in the following financial highlights chart, both sales and profitability metrics declined year-over-year:

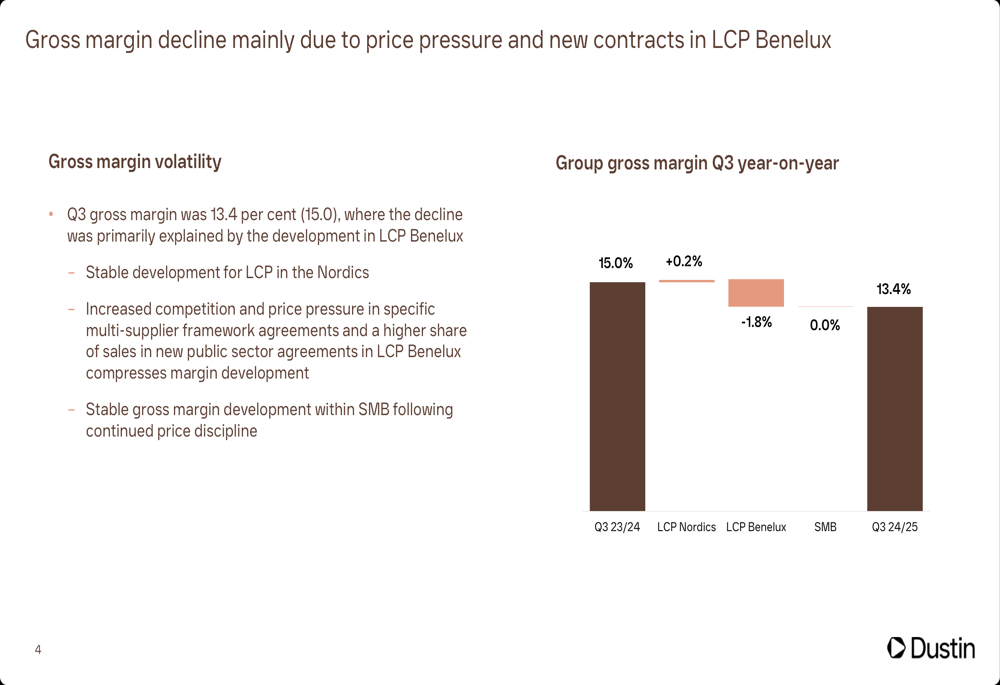

Gross margin contracted to 13.4% from 15.0% in the comparable quarter, with the decline primarily attributed to price pressure and new contracts in the Large Corporate and Public (LCP) segment in the Benelux region. The following chart breaks down the gross margin changes by business segment:

Detailed Financial Analysis

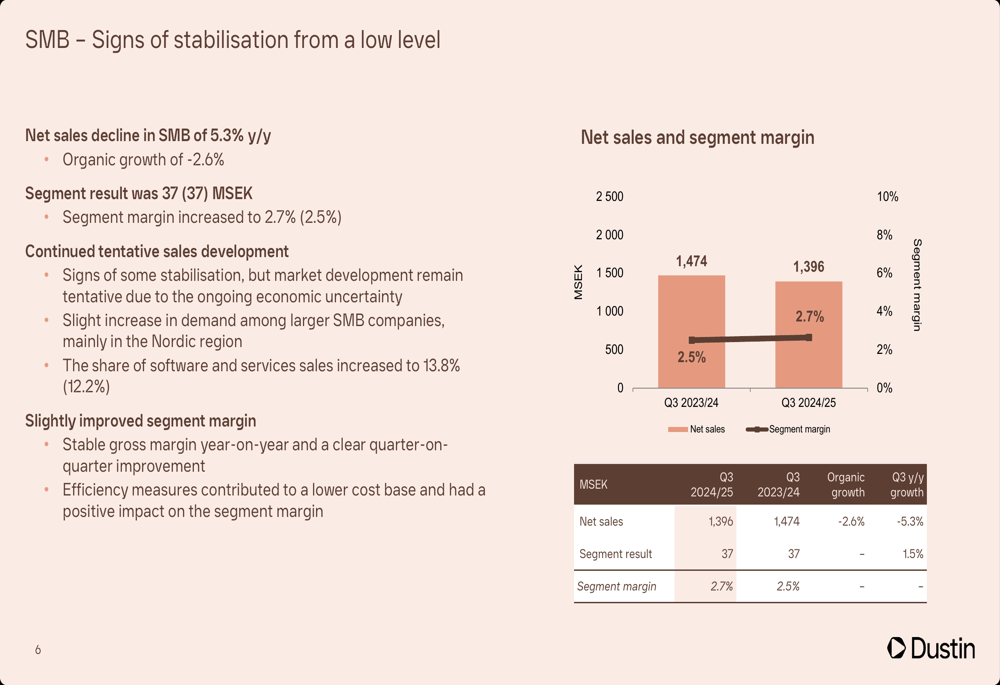

Dustin’s business segments showed divergent performance. The Small and Medium Business (SMB) segment saw net sales decline by 5.3% year-over-year, with organic growth at -2.6%. Despite the sales decline, the segment result held steady at 37 MSEK, with the segment margin actually improving to 2.7% from 2.5%, supported by a stable gross margin and efficiency measures. The company also noted an increased share of software and services sales, which rose to 13.8% from 12.2%.

The following chart illustrates the SMB segment’s performance metrics:

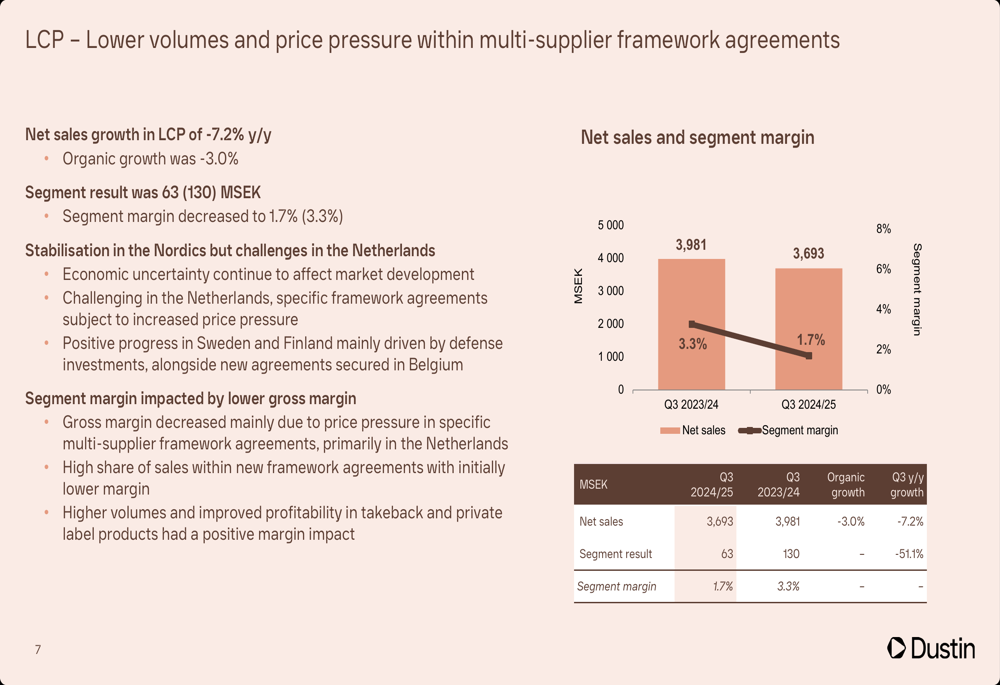

The Large Corporate and Public (LCP) segment faced more significant challenges, with net sales declining 7.2% year-over-year and organic growth at -3.0%. The segment result fell sharply to 63 MSEK from 130 MSEK, with the segment margin decreasing to 1.7% from 3.3%. The company cited economic uncertainty and price pressure in the Netherlands as key factors, while noting some stabilization in the Nordic markets.

The LCP segment’s performance is illustrated in the following chart:

Cash flow from operating activities deteriorated significantly to -139 MSEK from 454 MSEK in the prior-year period, primarily due to lower EBIT and changes in working capital. Net working capital increased to 261 MSEK from -205 MSEK, driven by higher inventory levels and delayed payment flows.

The company’s strengthened financial position through the rights issue is clearly visible in the following leverage reduction chart:

Strategic Initiatives

Dustin is implementing several strategic initiatives to address the profitability challenges. The company has nearly completed efficiency measures expected to yield annual savings of 150-200 MSEK. These measures include a reduction in full-time equivalent employees (FTEs), with a 7% reduction over the past year and a 12% reduction over the past two years.

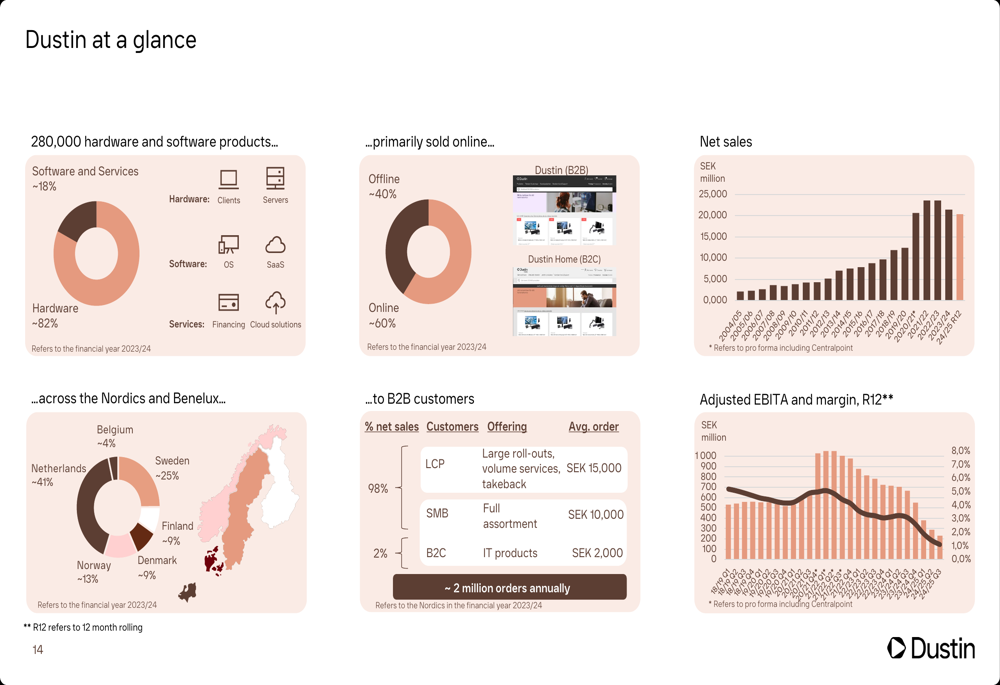

The company’s strategic focus includes implementing a new organization, transforming towards business customers, strengthening the B2B customer offering, and implementing long-term process improvements. Dustin positions itself as an aggregator in the IT ecosystem, connecting hardware, software, and service providers with various customer segments through both online (60%) and offline (40%) channels.

The following slide provides a comprehensive overview of Dustin’s business model and market position:

Forward-Looking Statements

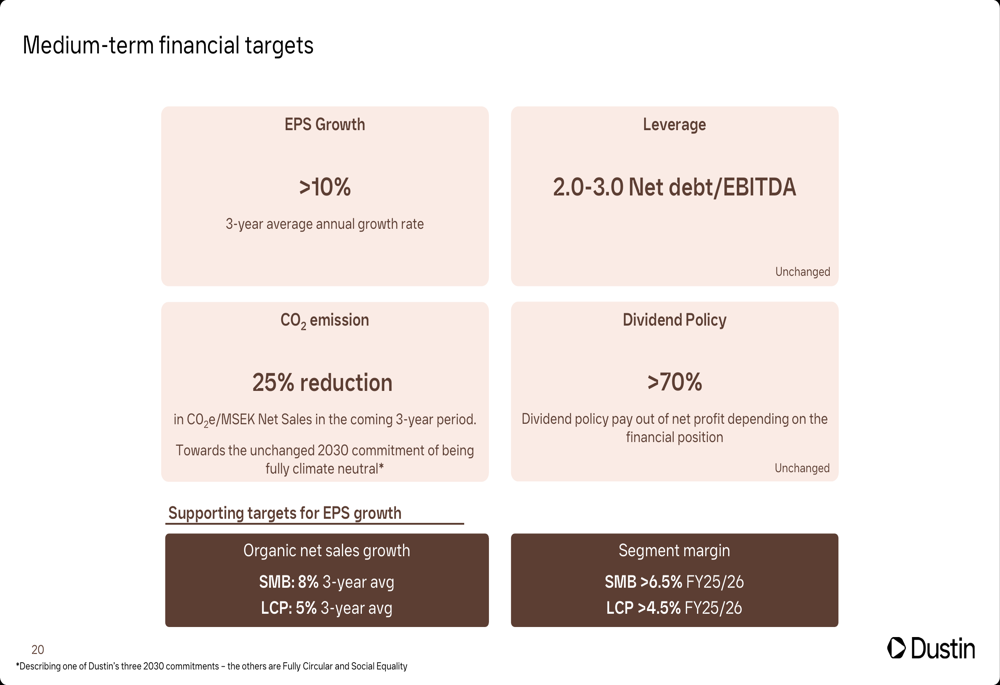

Dustin has established medium-term financial targets that include earnings per share growth exceeding 10%, a leverage ratio of 2.0-3.0x net debt to EBITDA, a CO2 emission reduction of 25%, and a dividend policy of over 70%. For specific segments, the company targets margins of over 6.5% for SMB and over 4.5% for LCP by fiscal year 2025/26.

The company’s financial targets are outlined in the following slide:

Dustin also emphasized its commitment to sustainability, with targets to reduce CO2 emissions by 25% by 2025/26. Key levers for this reduction include expanding services such as managed services and takeback, promoting solutions with lower environmental impact, and cooperating with committed vendors to reduce CO2 emissions.

While the current quarter presented challenges, the successful rights issue has provided Dustin with improved financial flexibility to navigate the uncertain market environment and implement its strategic initiatives aimed at returning to profitable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.