Gold prices hold gains amid Fed rate cut hopes, tariff jitters

Introduction & Market Context

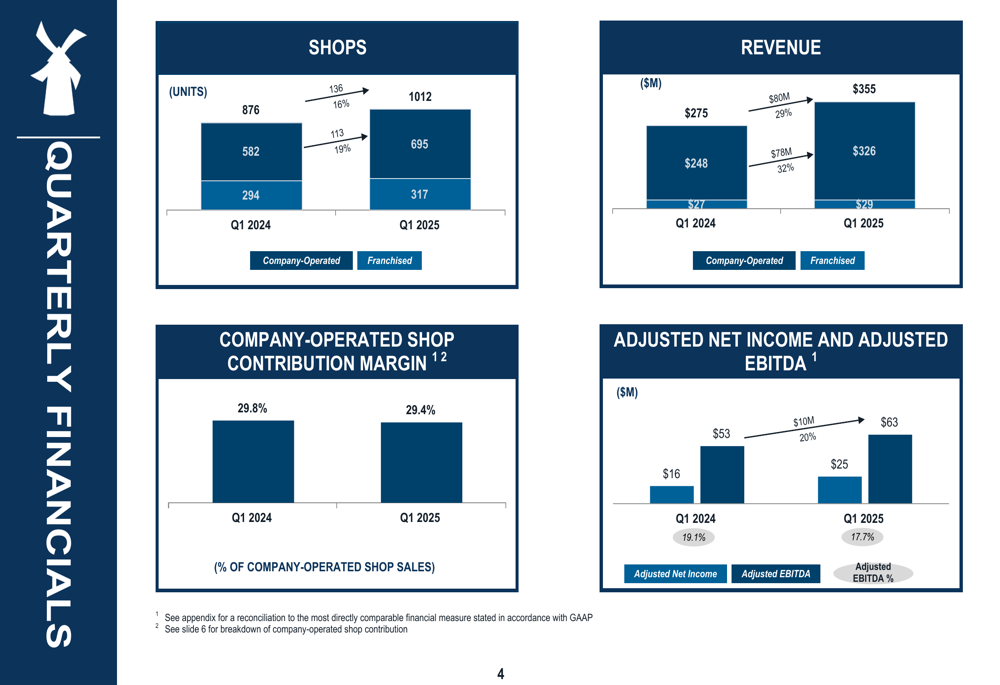

Dutch Bros Inc (NYSE:BROS) released its first quarter 2025 earnings presentation on May 7, revealing continued strong revenue growth as the coffee chain’s aggressive expansion strategy pushed its total shop count past the 1,000 mark. The company’s stock traded up 4.37% in after-hours trading at $61.81, reflecting positive investor sentiment despite some margin compression.

The coffee chain reported a 29% increase in revenue to $355 million, while adjusted net income jumped 56% to $25 million compared to the same period last year. These results build on Dutch Bros’ strong performance in Q4 2024, when the company significantly exceeded analyst expectations with adjusted EPS of $0.07 versus a forecasted $0.02.

Quarterly Performance Highlights

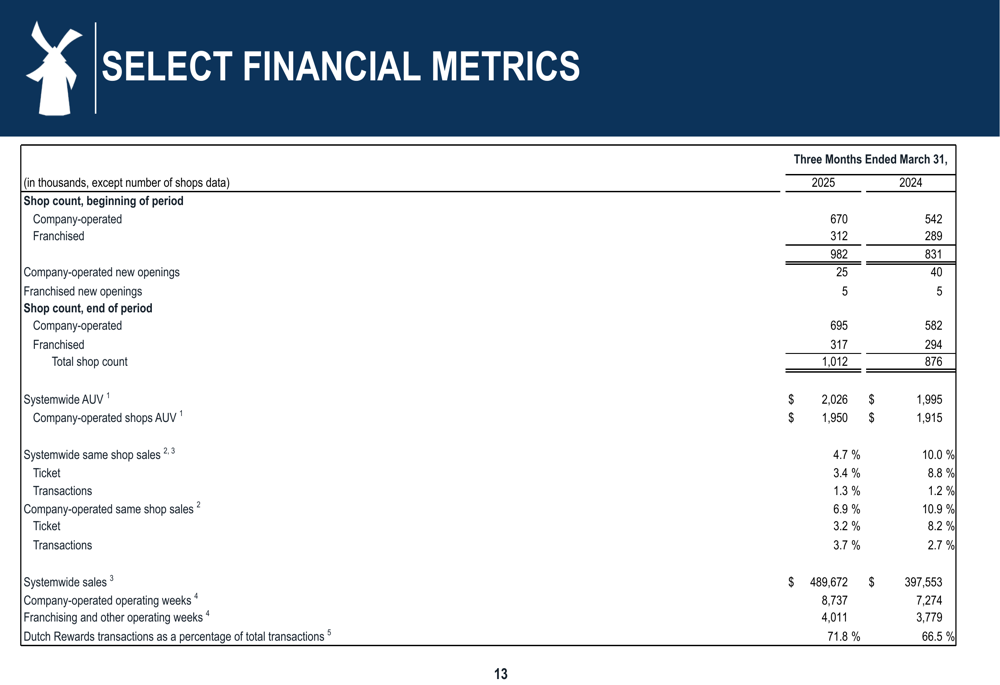

Dutch Bros’ total shop count reached 1,012 locations at the end of Q1 2025, representing a 15.5% increase from 876 shops in the prior-year period. This growth included 695 company-operated shops (up from 582) and 317 franchised locations (up from 294).

As shown in the following quarterly financials chart, the company delivered substantial top-line and bottom-line growth:

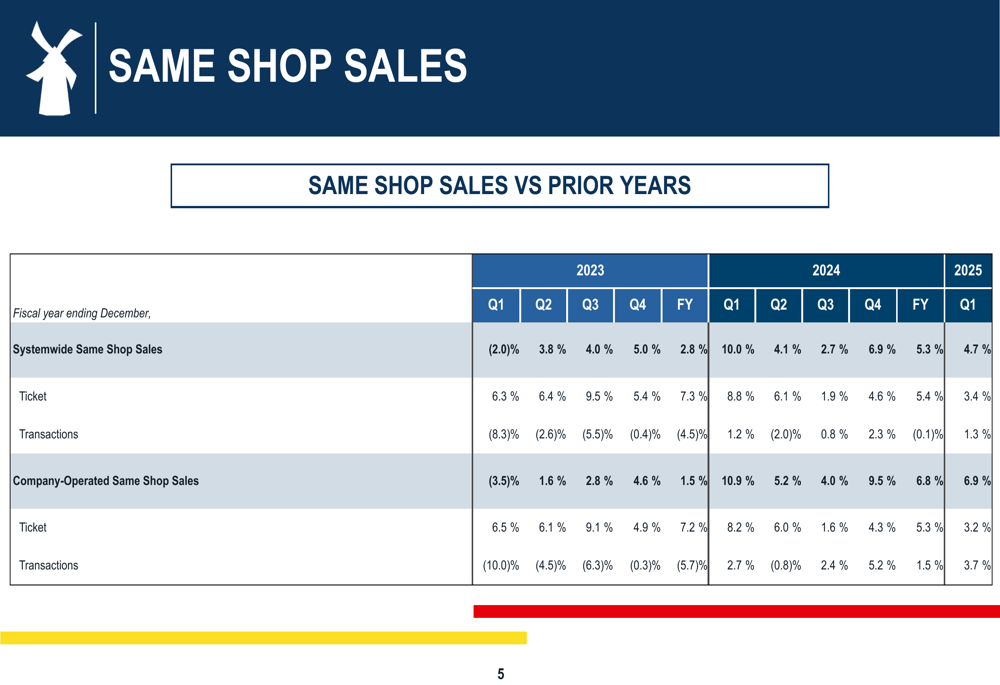

Same shop sales showed healthy growth, with systemwide comparable sales increasing 4.7% and company-operated shops posting an even stronger 6.9% gain. This growth was driven by both higher average tickets and increased transaction volumes, with company-operated shops seeing transaction growth of 3.7%.

The following chart details the same shop sales performance across recent quarters:

Dutch Bros’ loyalty program continues to gain traction, with Dutch Rewards transactions increasing to 71.8% of total transactions, up from 66.5% in Q1 2024. This metric suggests growing customer engagement and potential for increased frequency among repeat customers.

Detailed Financial Analysis

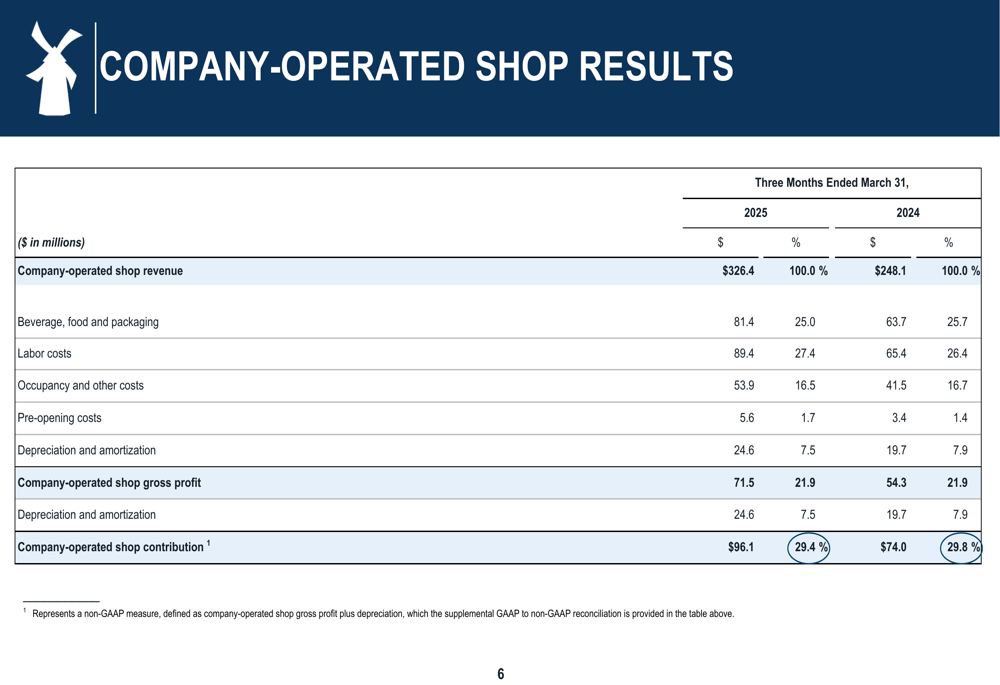

While revenue growth remained robust, Dutch Bros experienced some margin pressure during the quarter. The company-operated shop contribution margin decreased slightly from 29.8% to 29.4%, primarily due to increased labor costs, which rose from 26.4% to 27.4% of revenue.

The detailed breakdown of company-operated shop results reveals the specific cost pressures:

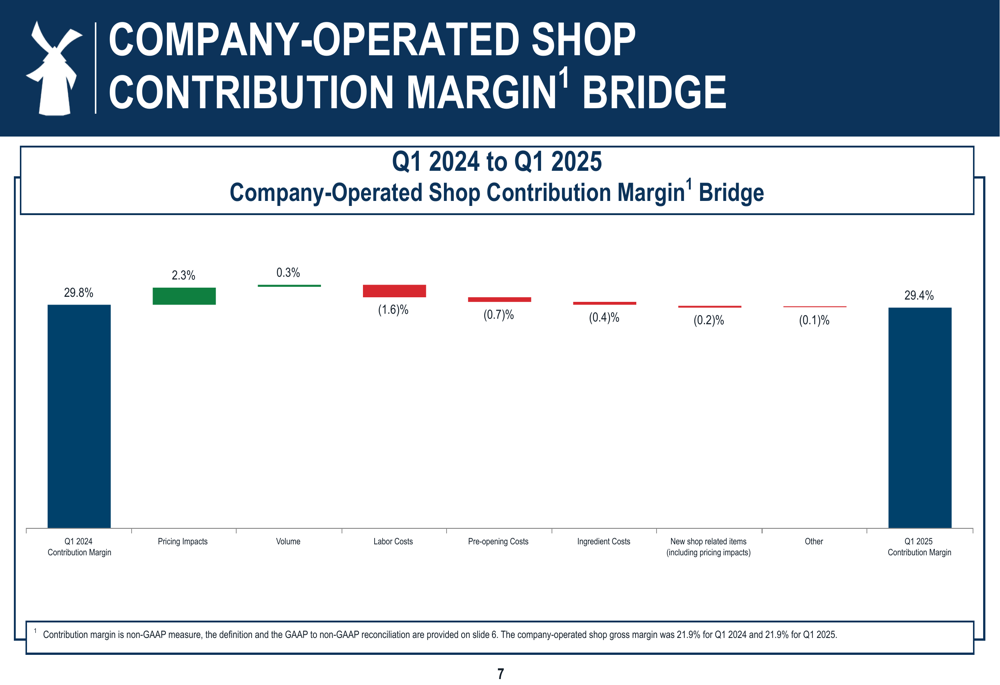

A closer examination of the margin changes shows that pricing and volume gains were offset by several factors, particularly labor costs. The company-operated shop contribution margin bridge illustrates these dynamics:

Despite these margin pressures at the shop level, Dutch Bros has made significant progress in leveraging its selling, general, and administrative expenses. SG&A as a percentage of total revenue has improved dramatically from 23.3% in Q1 2023 to just 16.6% in Q1 2025, demonstrating the company’s ability to scale its corporate infrastructure efficiently as it grows.

Adjusted EBITDA increased 19% to $63 million, though the adjusted EBITDA margin decreased from 19.1% to 17.7%. This slight margin compression reflects the challenges of maintaining profitability while pursuing aggressive expansion in an inflationary environment.

Strategic Initiatives

Dutch Bros continues to prioritize expansion as its primary growth driver, with significant capital investment planned for 2025. The company’s strategic focus remains on building its footprint in both existing and new markets, with particular emphasis on Texas and Florida as highlighted in previous earnings calls.

The company’s key performance indicators show improvements in several strategic areas:

Systemwide average unit volume (AUV) increased to $2.026 million from $1.995 million, indicating that new shops are performing well and existing locations are maintaining their sales momentum. The company’s ability to maintain strong AUVs while rapidly expanding suggests its site selection and operational execution remain effective.

Forward-Looking Statements

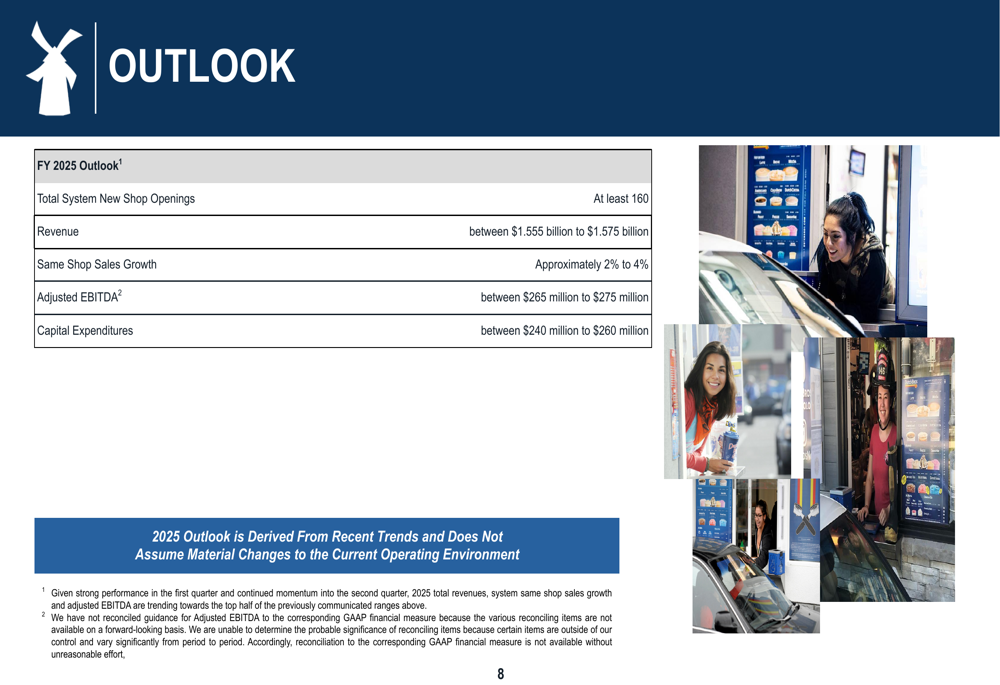

Dutch Bros provided a detailed outlook for fiscal year 2025, maintaining its aggressive growth targets while acknowledging the potential for continued margin pressures:

The company expects to open at least 160 new shops in 2025, projecting revenue between $1.555 billion and $1.575 billion. This represents approximately 21-23% growth compared to the $1.28 billion reported for fiscal 2024. Same shop sales are expected to grow between 2% and 4%, a more modest pace than the 4.7% reported in Q1.

Adjusted EBITDA is projected to reach between $265 million and $275 million, up from $230 million in 2024, representing growth of approximately 15-20%. Capital expenditures are expected to remain substantial at $240-260 million, reflecting the company’s continued investment in expansion.

Competitive Industry Position

Dutch Bros continues to carve out its position in the competitive specialty coffee market, differentiating itself with drive-thru focused locations and a high-energy customer experience. The company’s ability to maintain transaction growth in company-operated shops (3.7% in Q1) suggests it is successfully competing for customer visits despite inflationary pressures on consumer spending.

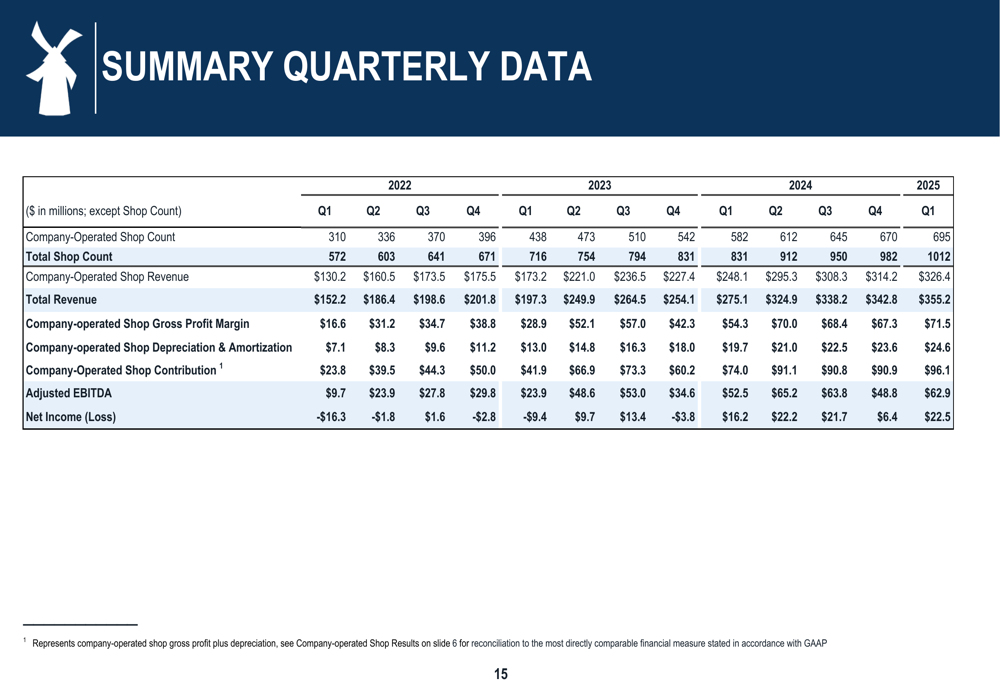

The company’s historical quarterly performance shows consistent growth in both shop count and financial metrics:

While facing competition from established players like Starbucks (NASDAQ:SBUX) and emerging regional chains, Dutch Bros’ expansion strategy and strong same-shop sales growth indicate it continues to resonate with consumers. The company’s focus on building its rewards program, which now accounts for over 70% of transactions, should help strengthen customer loyalty in an increasingly competitive market.

As Dutch Bros approaches the midpoint of fiscal 2025, the company appears well-positioned to continue its growth trajectory, though investors will likely monitor margin trends closely as the business scales beyond 1,000 locations and navigates ongoing labor and ingredient cost pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.