China’s Xi speaks with Trump by phone, discusses Taiwan and bilateral ties

Introduction & Market Context

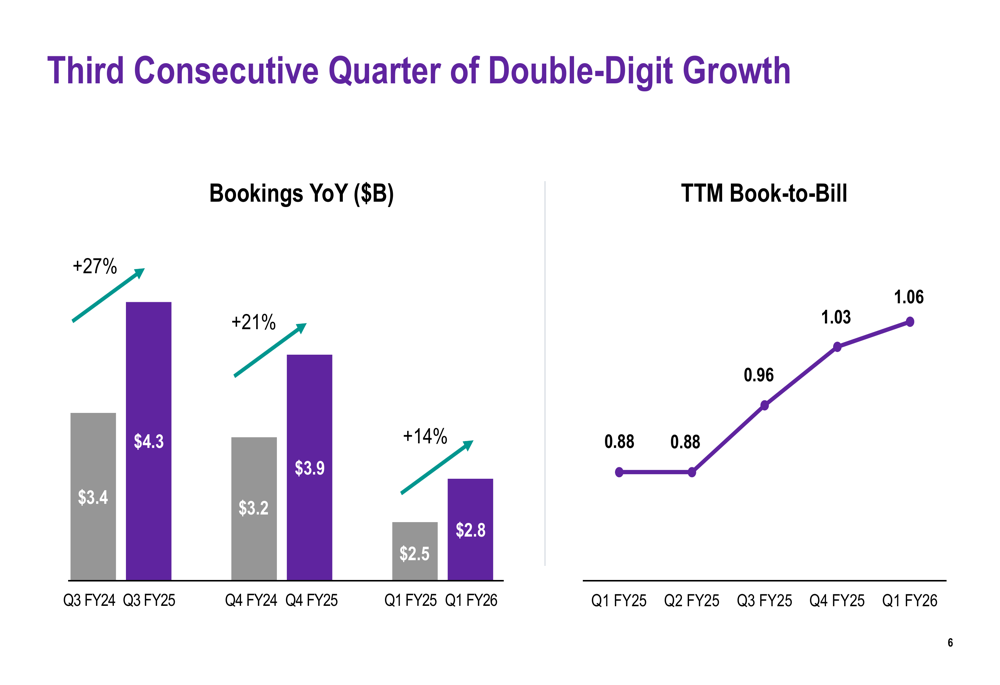

DXC Technology (NYSE:DXC) presented its first quarter fiscal year 2026 earnings results on July 31, 2025, highlighting continued bookings growth despite ongoing revenue challenges. The IT services provider reported its third consecutive quarter of double-digit bookings growth, with a 14% year-over-year increase, while organic revenue declined by 4.3%.

The company's stock closed at $13.22 on the day of the presentation, reflecting a modest 0.72% increase. According to recent trading data, DXC has been trading between a 52-week range of $12.24 to $24.83, indicating significant volatility over the past year.

Quarterly Performance Highlights

DXC Technology's Q1 FY26 performance showed mixed results, with the company exceeding guidance on earnings per share while meeting revenue expectations. The company reported organic revenue decline of 4.3%, which fell within the guided range of -4.0% to -5.5%.

As shown in the following performance overview chart:

The company delivered an adjusted EBIT margin of 6.8%, within the guided range of 6.0% to 7.0%, and non-GAAP diluted EPS of $0.68, exceeding the upper end of guidance ($0.55 to $0.65). This earnings outperformance suggests effective cost management despite revenue challenges.

A particularly bright spot was the continued improvement in bookings, which grew 14% year-over-year in Q1 FY26, following 27% and 21% growth in the previous two quarters. The trailing twelve months (TTM) book-to-bill ratio reached 1.06, up from 0.88 in Q1 FY25, suggesting potential revenue stabilization in future quarters.

Segment Performance Analysis

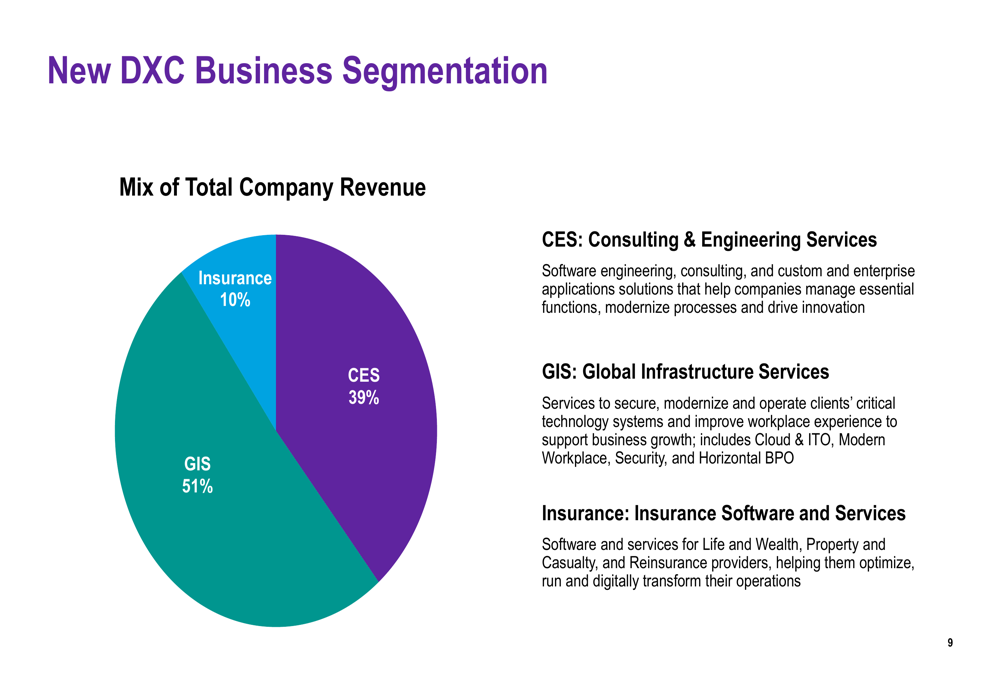

DXC Technology introduced a new business segmentation structure in the presentation, dividing its operations into three key segments: Consulting & Engineering Services (CES), Global Infrastructure Services (GIS), and Insurance Software and Services (Insurance).

The company's revenue mix is distributed across these segments as follows:

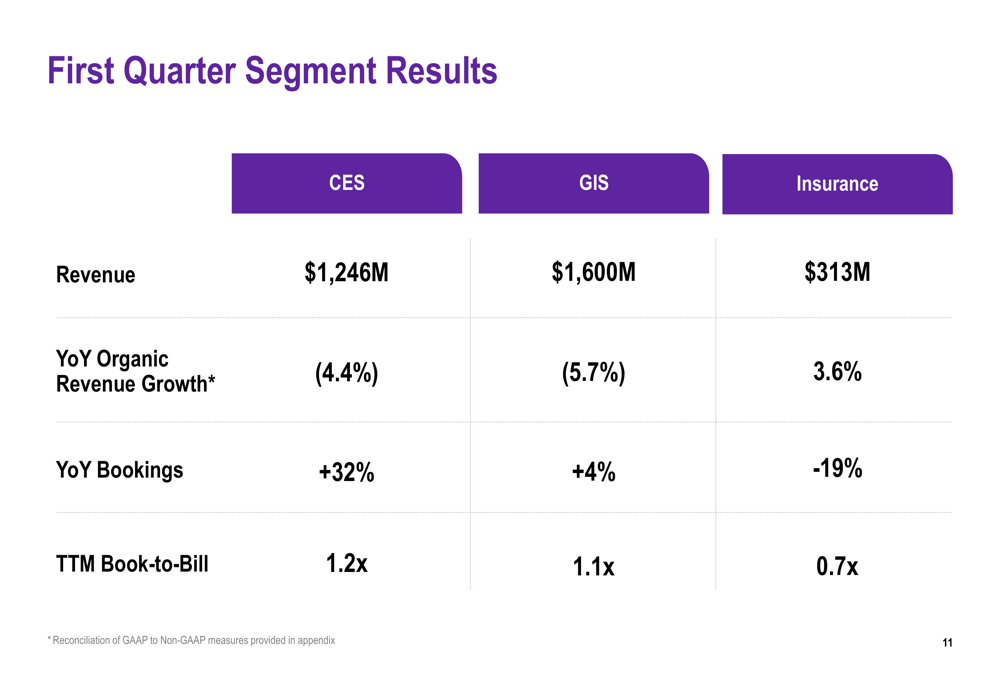

Performance varied significantly across segments, with Insurance showing growth while the larger segments experienced declines. The detailed segment results reveal:

The Insurance segment was the only one to deliver positive organic revenue growth at 3.6% year-over-year, though its bookings declined by 19%. CES, representing 39% of total revenue, saw organic revenue decline of 4.4% but demonstrated strong bookings growth of 32% with a healthy TTM book-to-bill ratio of 1.2x. GIS, the largest segment at 51% of revenue, experienced a 5.7% organic revenue decline with modest bookings growth of 4%.

Strategic Initiatives

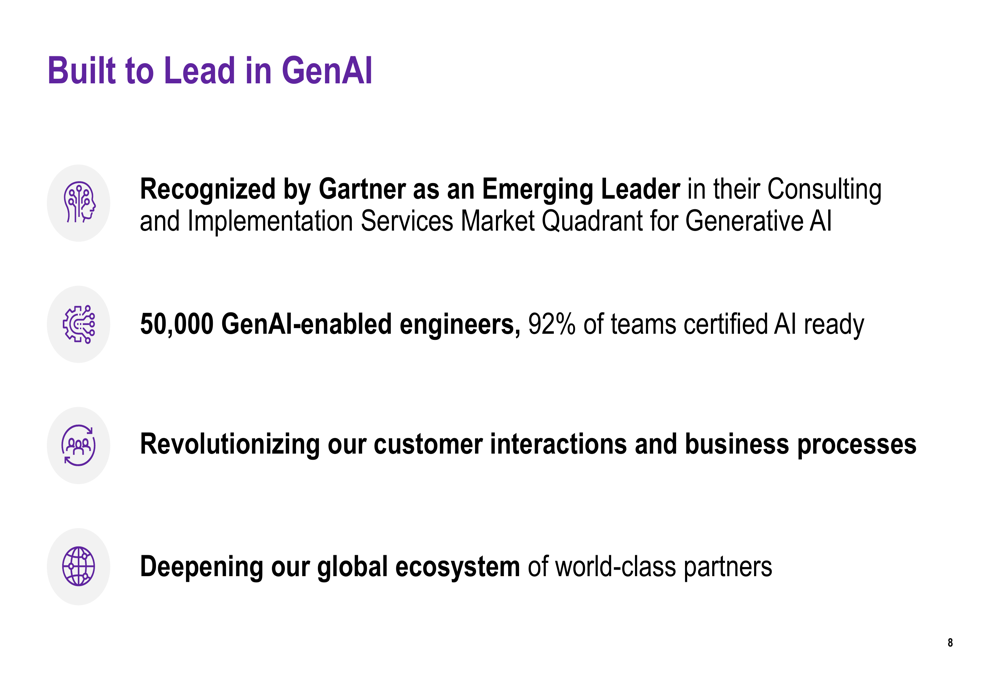

DXC Technology emphasized its strategic focus on Generative AI (GenAI) as a key growth driver. The company has been recognized by Gartner as an "Emerging Leader" in their Consulting and Implementation Services Market Quadrant for Generative AI, positioning it competitively in this rapidly growing market segment.

The company highlighted significant investments in AI capabilities, including:

With 50,000 GenAI-enabled engineers and 92% of teams certified as AI-ready, DXC is positioning itself to capitalize on growing demand for AI services. This aligns with statements from the earnings call, where President and CEO Raul Fernandez emphasized that "AI is redefining every business process and redefining every customer interaction."

The company also announced the appointment of Ramnath Venkataraman as President of CES. Venkataraman brings approximately 30 years of global experience from Accenture, with expertise in launching and growing businesses internationally and guiding clients in adopting cutting-edge technologies such as GenAI.

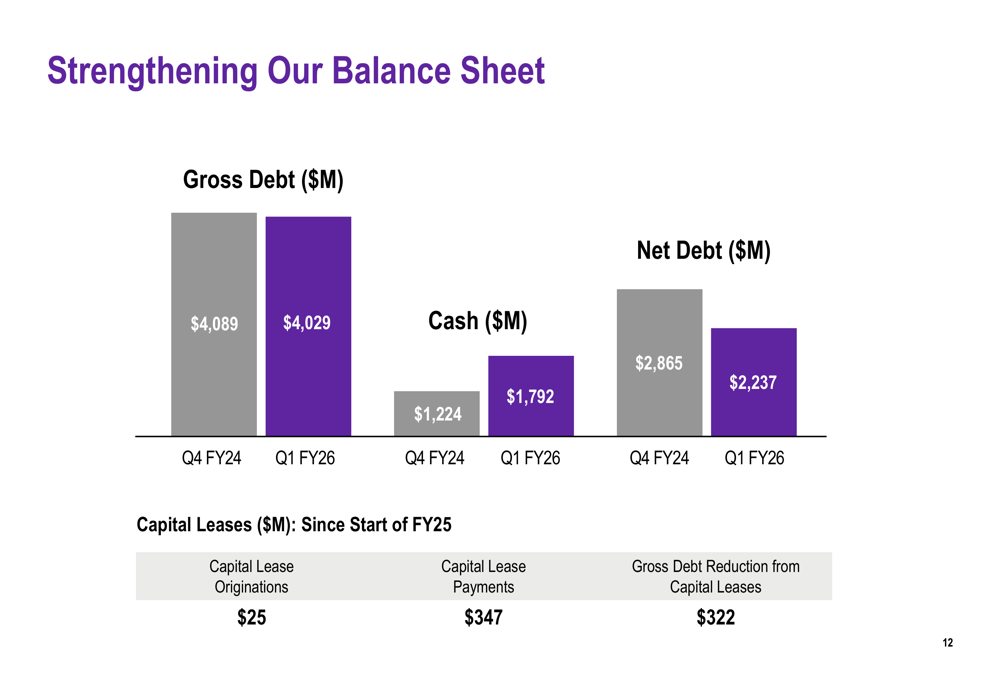

Balance Sheet Improvements

Despite revenue challenges, DXC Technology demonstrated progress in strengthening its financial position. The company reduced its gross debt from $4,089 million in Q4 FY24 to $4,029 million in Q1 FY26, while significantly increasing its cash balance from $1,224 million to $1,792 million during the same period.

As illustrated in the following chart:

Net debt decreased by $628 million to $2,237 million, reflecting the company's commitment to improving its financial health. The company also highlighted its progress in reducing capital leases, with $347 million in capital lease payments contributing to a $322 million gross debt reduction from capital leases since the start of FY25.

Forward-Looking Statements & Guidance

Looking ahead, DXC Technology provided guidance for both Q2 FY26 and the full fiscal year 2026:

For the full fiscal year 2026, the company expects organic revenue to decline between 3.0% and 5.0%, with adjusted EBIT margin between 7.0% and 8.0%. Non-GAAP diluted EPS is projected to be between $2.85 and $3.35, with free cash flow of approximately $600 million.

For Q2 FY26, DXC anticipates organic revenue decline between 3.5% and 4.5%, adjusted EBIT margin between 6.5% and 7.5%, and non-GAAP diluted EPS between $0.65 and $0.75.

The guidance suggests that while revenue challenges are expected to persist, the company anticipates potential improvement in the rate of decline compared to Q1, along with stable to improving profitability margins.

Conclusion

DXC Technology's Q1 FY26 presentation reveals a company navigating revenue headwinds while making progress on strategic initiatives and financial health. The consistent bookings growth and improving book-to-bill ratio provide some optimism for future revenue stabilization, while the focus on GenAI positions the company to capitalize on growing market demand.

The company's ability to exceed earnings guidance while strengthening its balance sheet demonstrates effective cost management and financial discipline. However, the persistent organic revenue decline across its largest segments remains a significant challenge that will require continued attention as DXC executes its strategic transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.