S&P 500 slips as final month of trade for the year kicks off

Introduction & Market Context

DXC Technology (NYSE:DXC) released its second quarter fiscal year 2026 earnings presentation on October 30, 2025, revealing a mixed financial picture that prompted a modest market reaction. The IT services provider reported better-than-expected profitability metrics despite continued revenue challenges, with the stock declining 1.82% in aftermarket trading to $13.15, reflecting investor concerns about the company's growth trajectory.

The company's results highlighted the ongoing tension between improving operational efficiency and addressing persistent revenue declines in its core business segments. While DXC exceeded its profitability targets, organic revenue declined by 4.2% year-over-year, continuing a challenging trend for the company.

Quarterly Performance Highlights

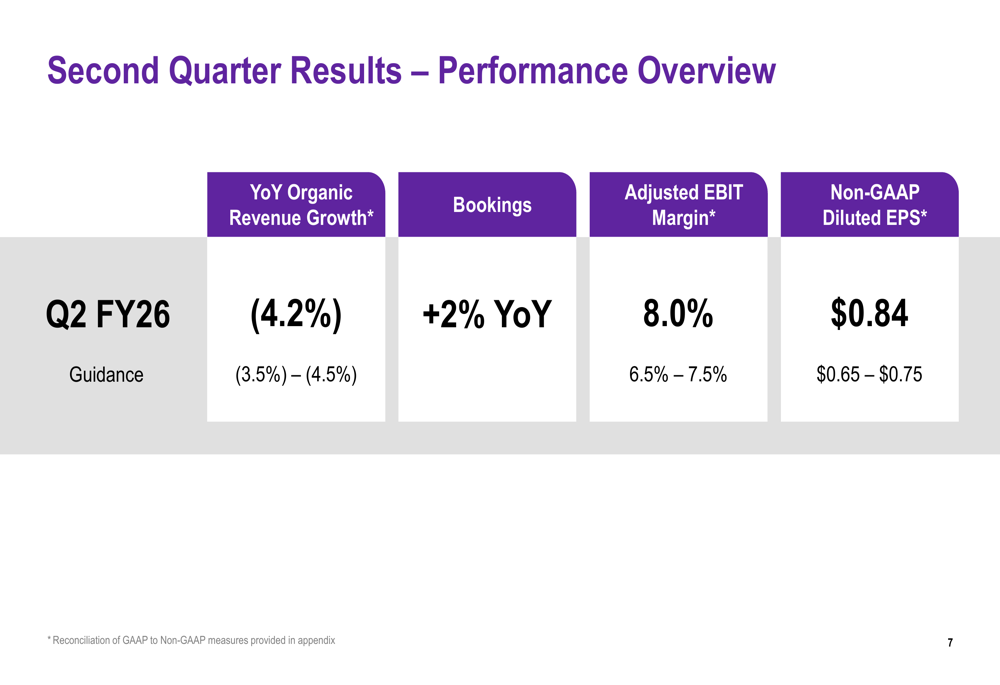

DXC Technology's second quarter results showed mixed performance across key metrics. The company reported non-GAAP diluted earnings per share of $0.84, significantly outperforming its guidance range of $0.65-$0.75. Similarly, adjusted EBIT margin reached 8.0%, exceeding the projected range of 6.5%-7.5%. However, organic revenue declined by 4.2% year-over-year, though this was within the company's expected range of -3.5% to -4.5%.

As shown in the following performance overview from the presentation:

Bookings showed modest improvement with a 2% year-over-year increase, suggesting potential stabilization in future quarters. The company's performance varied significantly across business segments, with the Insurance division emerging as a bright spot.

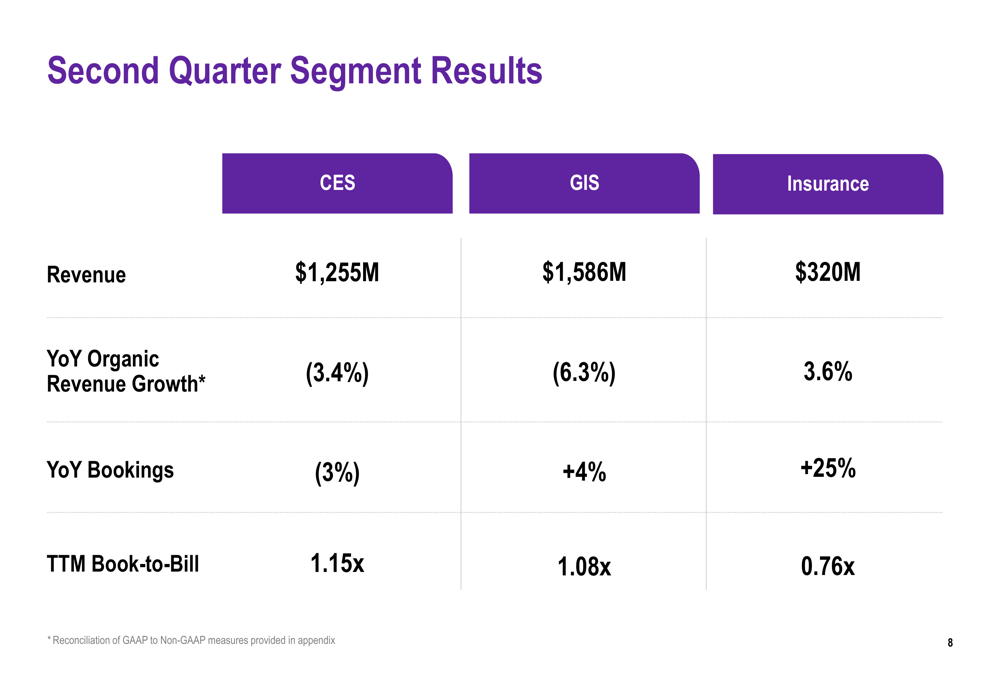

The segment breakdown reveals divergent trajectories across DXC's business units:

The Insurance segment demonstrated encouraging growth with a 3.6% year-over-year organic revenue increase and impressive 25% growth in bookings. In contrast, the Global Infrastructure Services (GIS) segment, which represents the largest portion of DXC's revenue at $1.59 billion, experienced a 6.3% organic revenue decline, though bookings improved by 4%. The Consulting and Engineering Services (CES) segment reported a 3.4% organic revenue decline with bookings down 3% year-over-year.

Strategic Initiatives

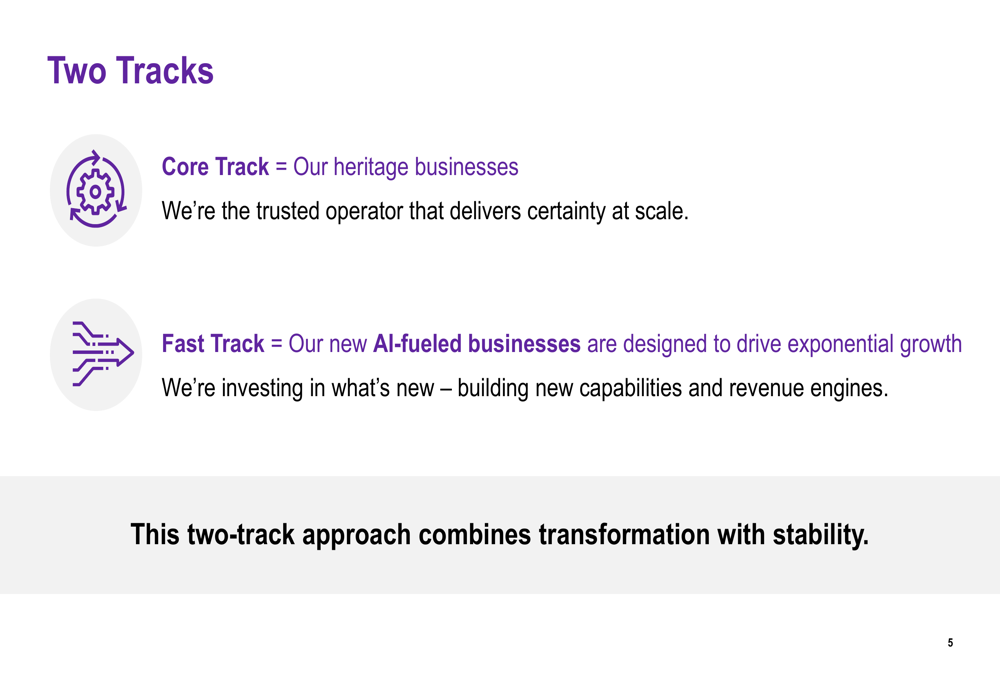

DXC Technology unveiled its "Two Tracks" strategy during the earnings presentation, outlining a dual approach to balance stability in legacy businesses while pursuing growth through new AI-powered initiatives.

The company's strategic framework is illustrated in this slide:

The Core Track focuses on heritage businesses where DXC positions itself as a "trusted operator delivering certainty at scale." Meanwhile, the Fast Track encompasses new AI-fueled businesses designed for exponential growth, where the company is investing in new capabilities and revenue engines.

Central to DXC's AI strategy is "Xponential," a newly introduced AI orchestration blueprint:

According to the earnings call transcript, CEO Raul Fernandez emphasized the strategic importance of these AI initiatives, noting: "These AI-based SaaS solutions are highly replicable and built on proprietary methodologies, models, and frameworks that create defensible competitive moats." This initiative represents DXC's attempt to pivot toward higher-growth areas while managing its traditional service lines.

Detailed Financial Analysis

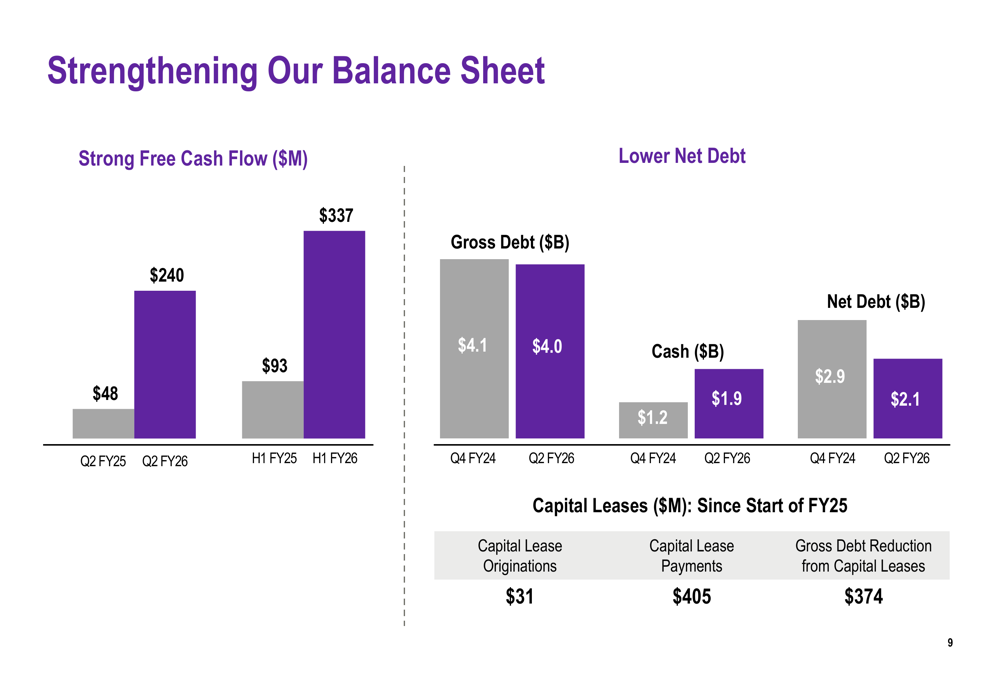

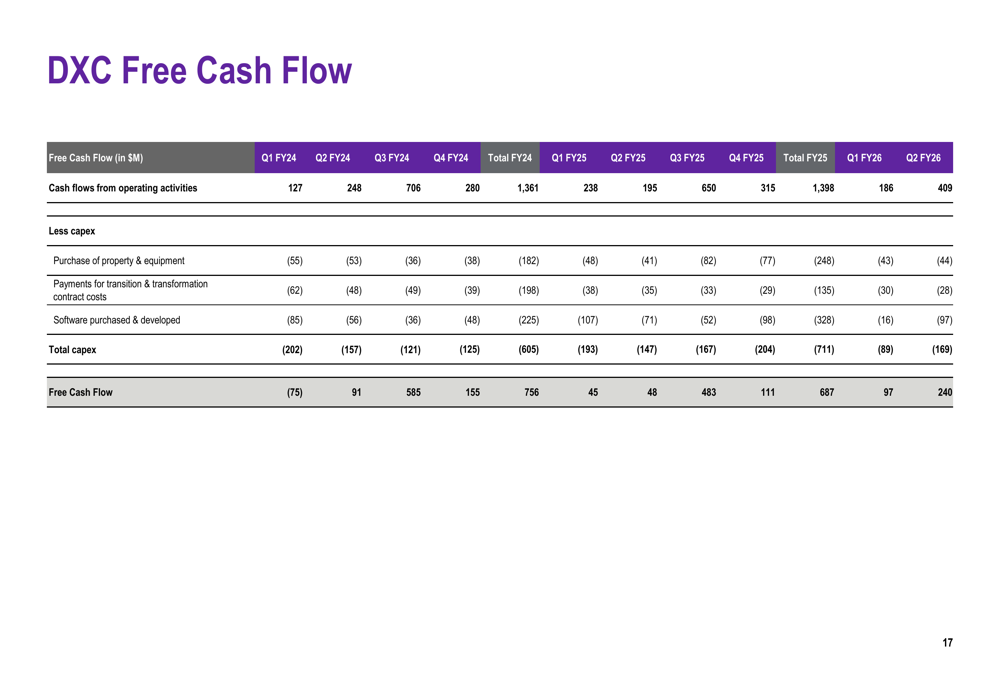

DXC Technology demonstrated significant improvement in its financial position, particularly in free cash flow generation and debt reduction. The company reported Q2 free cash flow of $240 million, a substantial increase from $48 million in the same period last year.

The balance sheet strengthening is clearly visualized in this chart:

Net debt decreased from $2.9 billion in Q4 FY24 to $2.1 billion in Q2 FY26, reflecting both improved cash generation and disciplined capital management. Cash on hand increased from $1.2 billion to $1.9 billion over the same period, providing DXC with enhanced financial flexibility.

The company's free cash flow improvement was driven by several factors, as detailed in this breakdown:

CFO Rob Del Bene highlighted the company's strengthened financial position during the earnings call, stating: "We have the capacity with the balance sheet that we've built over the last 18 months to make the necessary investments and take advantage of opportunities when we see them."

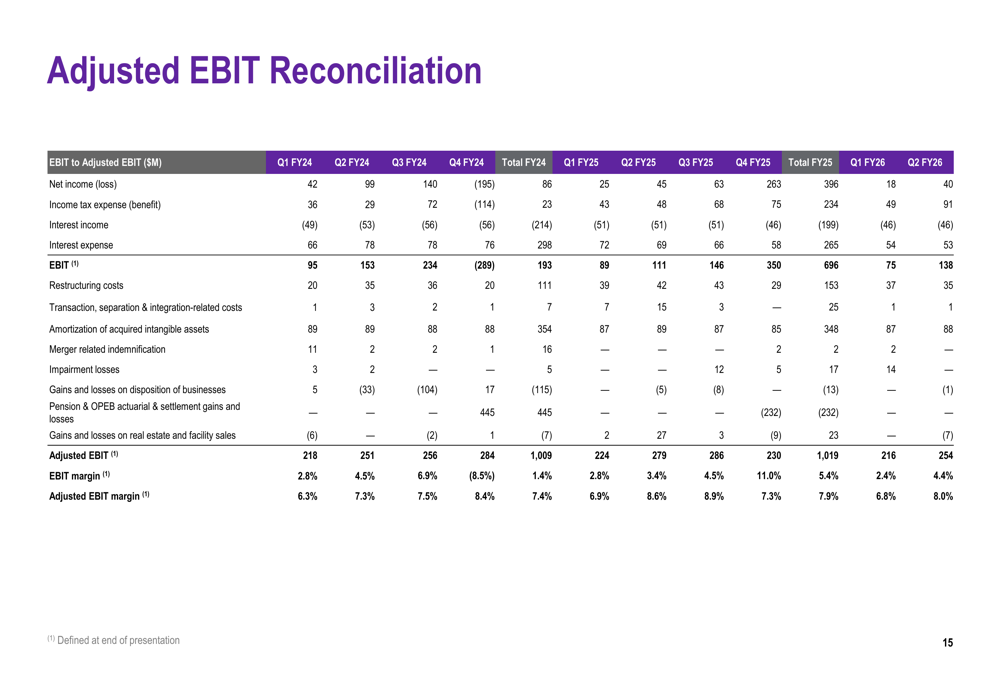

The company's adjusted EBIT reconciliation provides further insight into profitability drivers:

Forward-Looking Statements

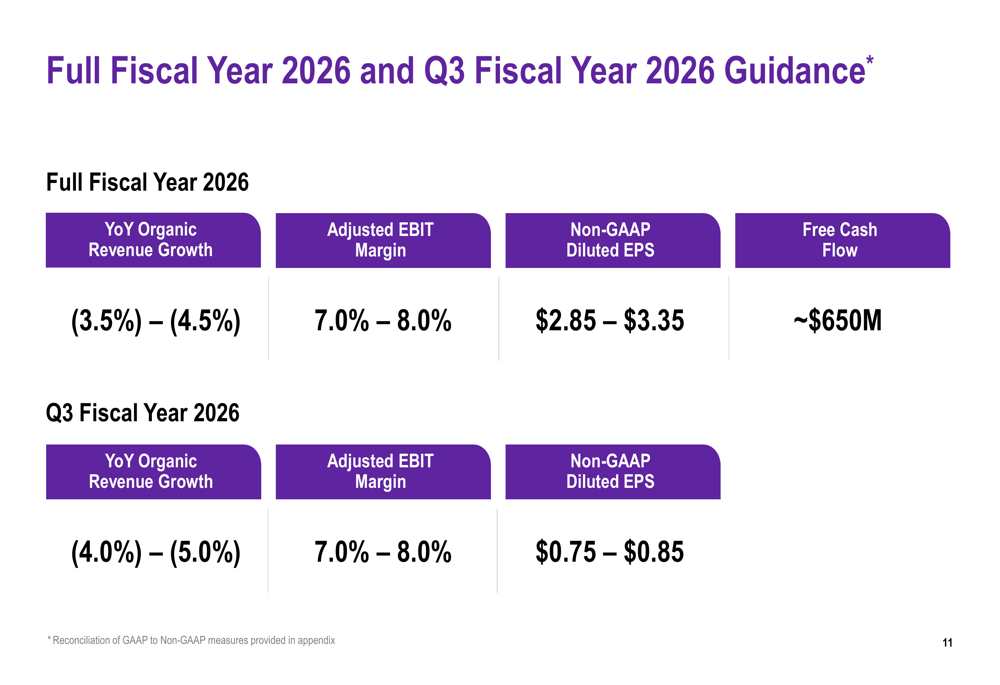

Looking ahead, DXC Technology provided guidance for both Q3 FY26 and the full fiscal year, projecting continued revenue challenges but stable profitability:

For the full fiscal year 2026, DXC expects organic revenue to decline between 3.5% and 4.5%, maintaining its previous guidance. The company projects adjusted EBIT margin between 7.0% and 8.0%, with non-GAAP diluted EPS of $2.85 to $3.35. Free cash flow is expected to reach approximately $650 million.

For the upcoming third quarter, DXC forecasts a slightly steeper organic revenue decline of 4.0% to 5.0%, with adjusted EBIT margin holding steady at 7.0% to 8.0% and non-GAAP diluted EPS between $0.75 and $0.85.

The company also outlined its capital allocation priorities, focusing on investing in the business for growth, minimizing new financial lease originations, maintaining investment-grade debt levels, and returning capital to shareholders through stock buybacks.

Despite the positive elements in DXC's presentation, the company faces several challenges ahead. The continued pressure in discretionary custom application projects, declining revenue in core service areas, and macroeconomic uncertainties affecting client spending all present headwinds. Additionally, execution risks in AI strategy implementation and industry-wide competition in digital transformation will require careful navigation as DXC pursues its strategic transformation.

As DXC Technology balances improving profitability with addressing revenue challenges, investors will be watching closely to see if the company's "Two Tracks" strategy and AI initiatives can ultimately reverse the revenue decline and drive sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.