Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

DXP Enterprises Inc (NASDAQ:DXPE), an industrial distribution expert, reported strong first-quarter fiscal 2025 results on May 8, showcasing double-digit growth across key financial metrics. Despite the robust performance, the company’s stock dropped 6.19% to $83.28 following the announcement, continuing a pattern seen in previous quarters where positive results were met with market skepticism.

The industrial distributor has been successfully diversifying its business beyond traditional oil and gas markets, focusing on water, safety services, and rotating equipment segments. This strategic shift appears to be yielding financial benefits, as evidenced by the company’s improved profitability metrics and margin expansion.

Quarterly Performance Highlights

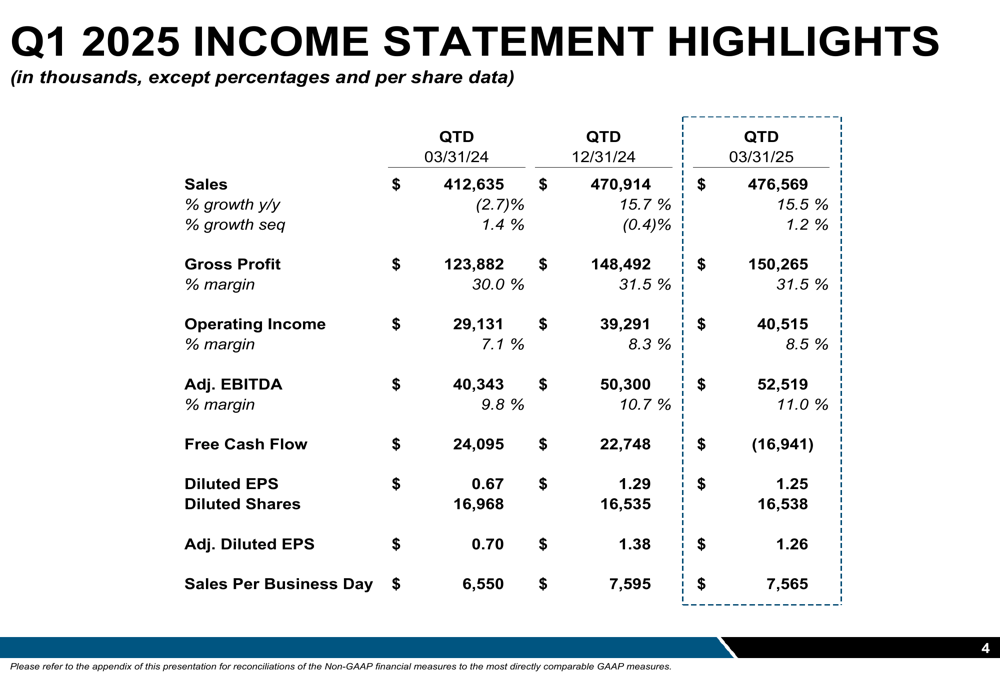

DXP reported Q1 2025 sales of $476.6 million, representing a 15.5% year-over-year increase and a 1.2% sequential improvement from Q4 2024. Organic sales grew 11.1% compared to the same period last year, with acquisition sales contributing $31.1 million to the top line.

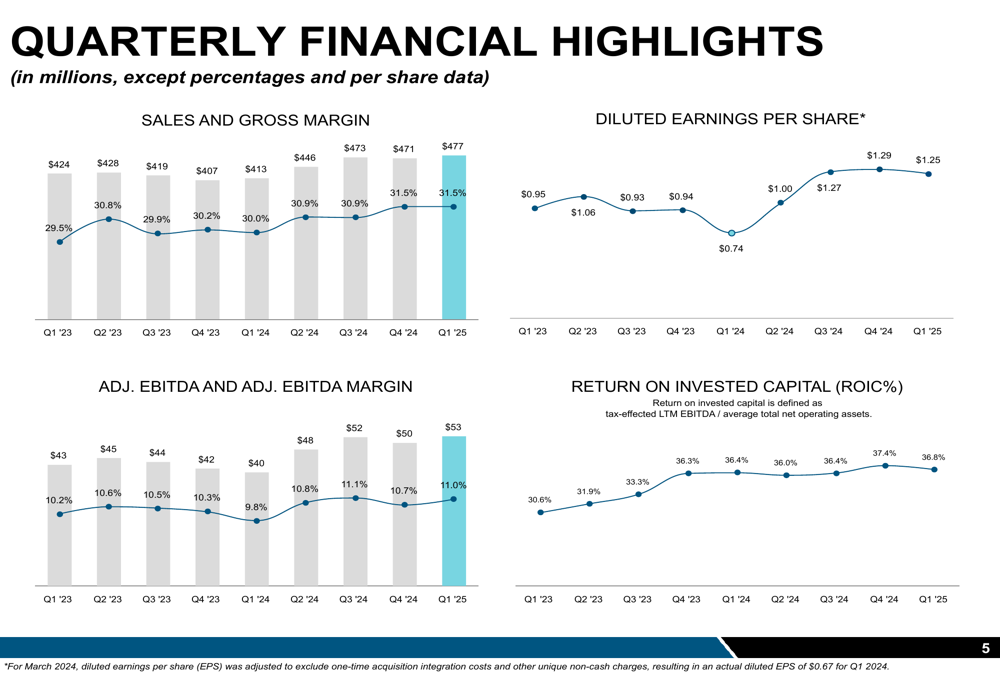

As shown in the following quarterly financial highlights chart, the company has maintained consistent growth in sales while expanding gross margins from 29.5% in Q1 2023 to 31.5% in Q1 2025:

Net income more than doubled to $20.6 million compared to $11.3 million in Q1 2024, while earnings per diluted share reached $1.25, significantly higher than the $0.67 reported in the same period last year. The company’s adjusted EBITDA increased to $52.5 million from $40.3 million in Q1 2024, with adjusted EBITDA margin improving by 124 basis points year-over-year to reach 11.0%.

The comprehensive income statement highlights below demonstrate DXP’s financial improvements across multiple metrics:

Detailed Financial Analysis

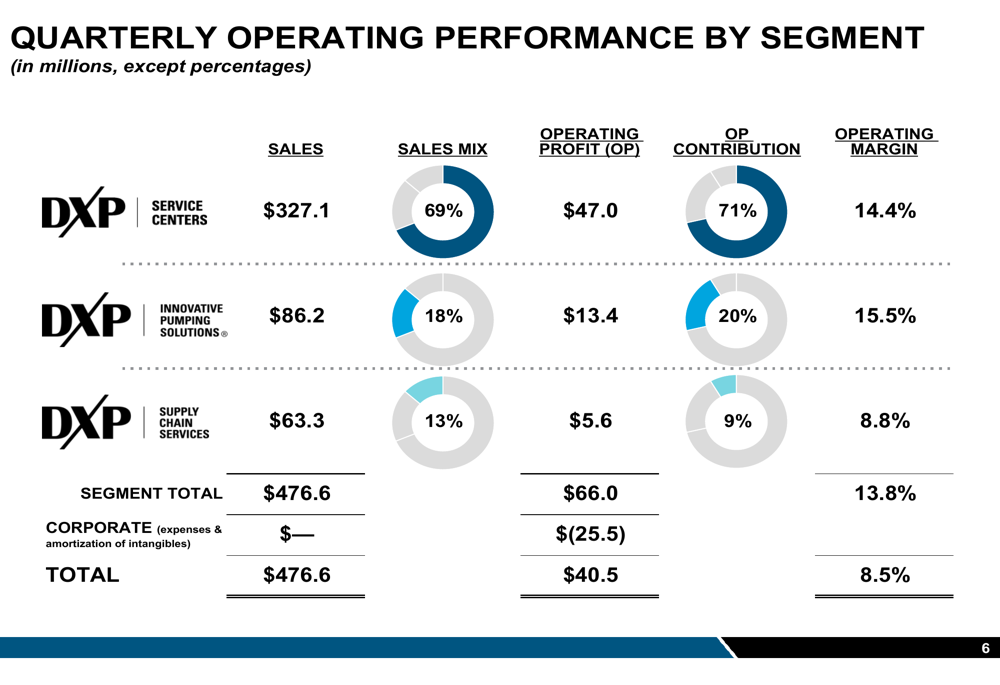

DXP’s business is divided into three segments, each contributing differently to the company’s overall performance. The Service Centers segment remains the largest contributor, accounting for 69% of total sales and 71% of operating profit, with an operating margin of 14.4%. The Innovative Pumping Solutions segment delivered the highest operating margin at 15.5%, while representing 18% of sales and 20% of operating profit. The Supply Chain Services segment contributed 13% of sales and 9% of operating profit, with an 8.8% operating margin.

The following breakdown illustrates the relative contribution of each business segment:

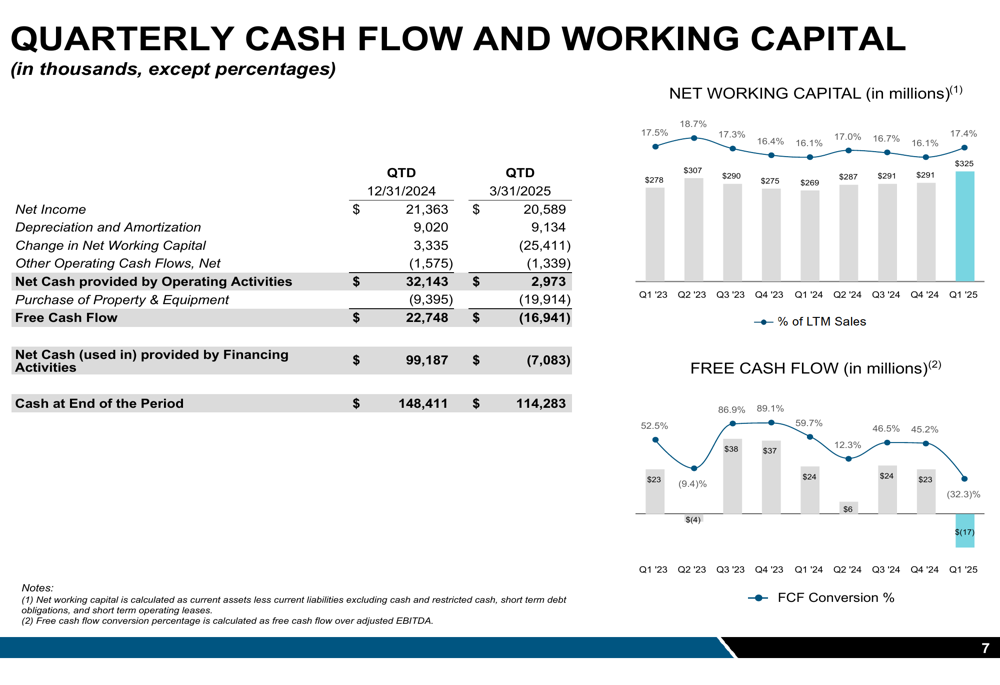

While most financial metrics showed improvement, free cash flow emerged as a potential concern, turning negative at $16.9 million for Q1 2025 compared to a positive $24.1 million in Q1 2024. This decline appears to be primarily driven by a $25.4 million increase in net working capital and $19.9 million in capital expenditures.

The company’s working capital management shows some challenges, as illustrated in this chart:

Strategic Initiatives

DXP continues to execute its growth strategy through a combination of organic expansion and strategic acquisitions. During Q1 2025, the company closed the acquisition of Arroyo Process Equipment, further strengthening its market position.

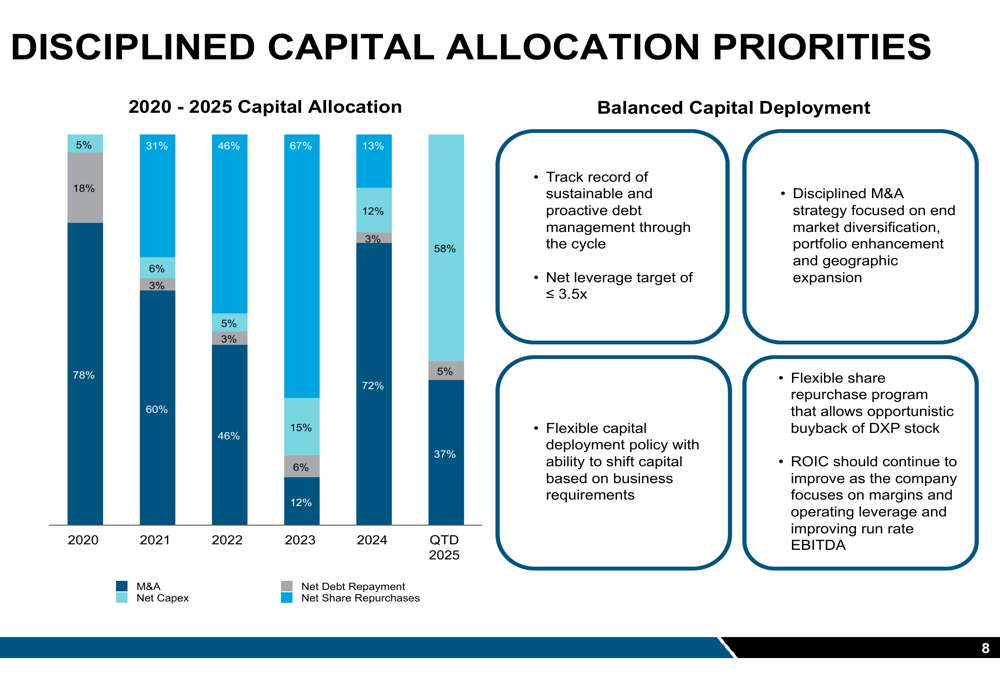

The company’s capital allocation priorities demonstrate a balanced approach between debt management, acquisitions, and capital expenditures. For 2025, DXP has allocated 58% of its capital to net debt repayment, 37% to net capital expenditures, and 5% to mergers and acquisitions, as shown in the following chart:

This disciplined approach to capital allocation aligns with the company’s stated goal of maintaining a net leverage target of ≤3.5x while focusing on margin improvement and operating leverage to enhance run-rate EBITDA.

Forward-Looking Statements

Based on the strong Q1 2025 performance, DXP appears well-positioned to continue its growth trajectory. The company’s adjusted EBITDA margin of 11.0% aligns with its previously stated target of 11%, suggesting management is executing effectively on its strategic initiatives.

The improvement in return on invested capital (ROIC) from 30.6% in Q1 2023 to 36.8% in Q1 2025 indicates that the company is generating increasingly better returns from its investments, a positive sign for long-term shareholder value creation.

However, investors should monitor the negative free cash flow trend and increased working capital requirements, which could potentially impact the company’s financial flexibility if the pattern continues in future quarters.

In the previous earnings call for Q4 2024, CEO David Little expressed optimism about the company’s future, stating, "We are excited about the future and delivering a differentiated customer experience." The Q1 2025 results largely support this positive outlook, though the market’s reaction suggests investors may be concerned about sustainability of growth or broader economic factors affecting industrial distributors.

As DXP continues to diversify its end markets and expand through strategic acquisitions, its ability to maintain margin expansion while addressing working capital challenges will likely be key factors in determining future performance and investor sentiment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.