Amcor stock falls after Raymond James reiterates Market Perform rating

Introduction & Market Context

ECN Capital Corp . (TSX:ECN) presented its first quarter 2025 financial results on May 8, 2025, highlighting solid performance across its business segments. The company, which specializes in providing credit portfolio origination and management for financial institutions, reported adjusted earnings per share of $0.03, reaching the top end of its guidance range.

ECN Capital’s performance comes amid a resilient manufactured housing market that, according to the company’s analysis, shows little correlation to interest rate fluctuations or consumer sentiment. This resilience has allowed ECN to expand its institutional funding partnerships while growing its origination volumes across key business segments.

Quarterly Performance Highlights

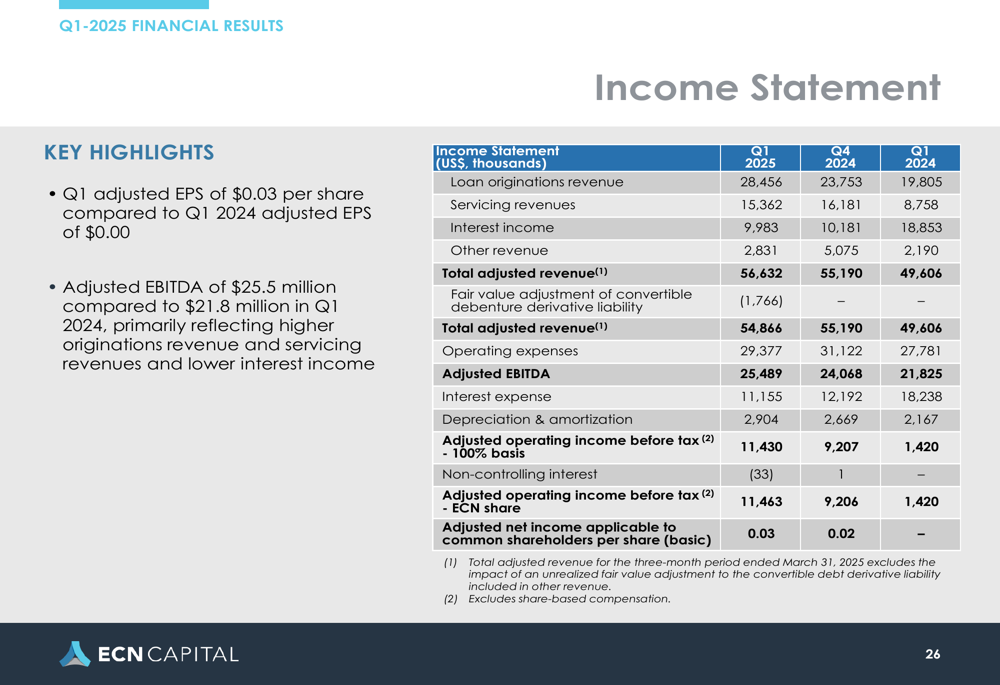

ECN Capital reported total originations of $538.2 million for Q1 2025, with adjusted EBITDA of $25.5 million, compared to $21.8 million for the same period in 2024. The company’s adjusted operating income before tax increased significantly to $11.4 million, up from $1.4 million in Q1 2024.

As shown in the following income statement, the company achieved substantial year-over-year growth in key financial metrics:

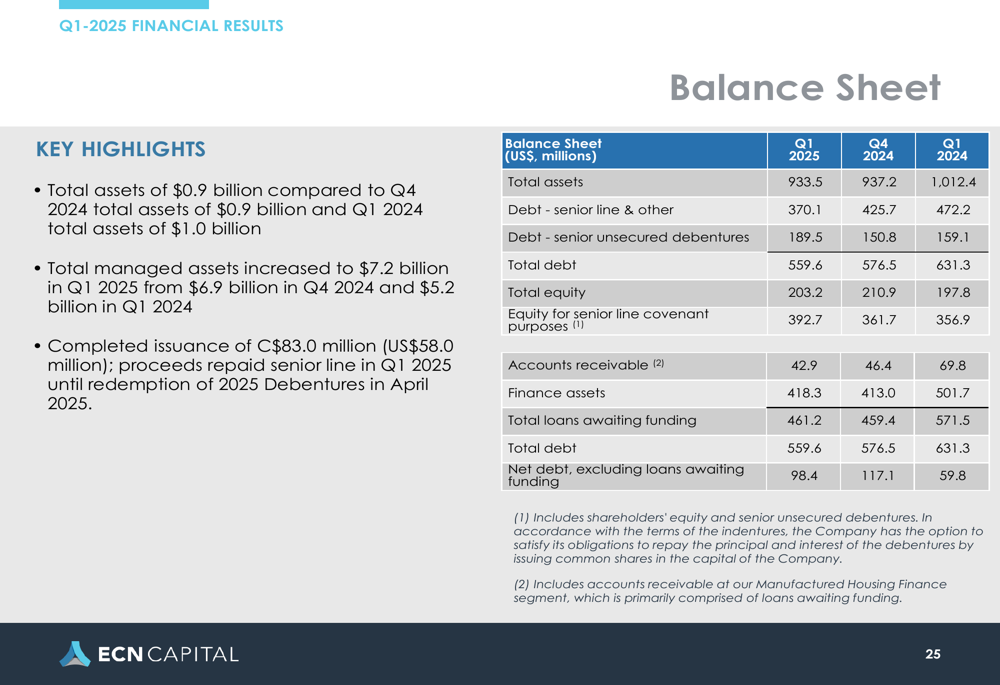

The company’s total managed assets increased to $7.2 billion in Q1 2025, reflecting ECN’s continued portfolio growth. The balance sheet remains solid with total assets of $933.5 million and total equity of $203.2 million.

Manufactured Housing Segment Analysis

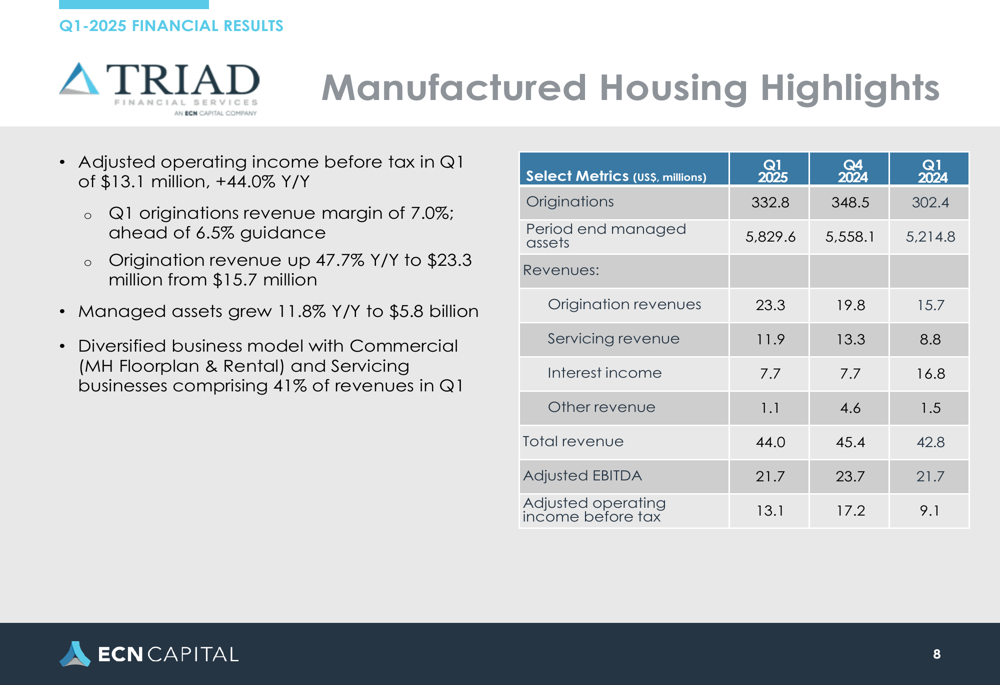

The Manufactured Housing segment, operated through Triad Financial Services, was the standout performer for ECN Capital in the first quarter. The segment reported adjusted operating income before tax of $13.1 million, representing a 44.0% year-over-year increase. Originations reached $333 million, marking the best first quarter in Triad’s history with a 10.0% increase compared to Q1 2024.

The following table highlights the strong performance metrics for the Manufactured Housing segment:

Particularly noteworthy was the growth in high-margin chattel originations, which increased by 43.8% year-over-year in Q1 and continued to accelerate with a 67.5% year-over-year increase in April. Chattel loans comprised 87% of originations in Q1 2025, compared to 66% in Q1 2024, contributing to the segment’s improved profitability.

The segment’s origination revenue margin was 7.0% in Q1, exceeding the 6.5% guidance, while origination revenue increased by 47.7% year-over-year to $23.3 million. Managed assets grew 11.8% year-over-year to $5.8 billion.

The following chart illustrates the retail originations mix for Triad Financial Services:

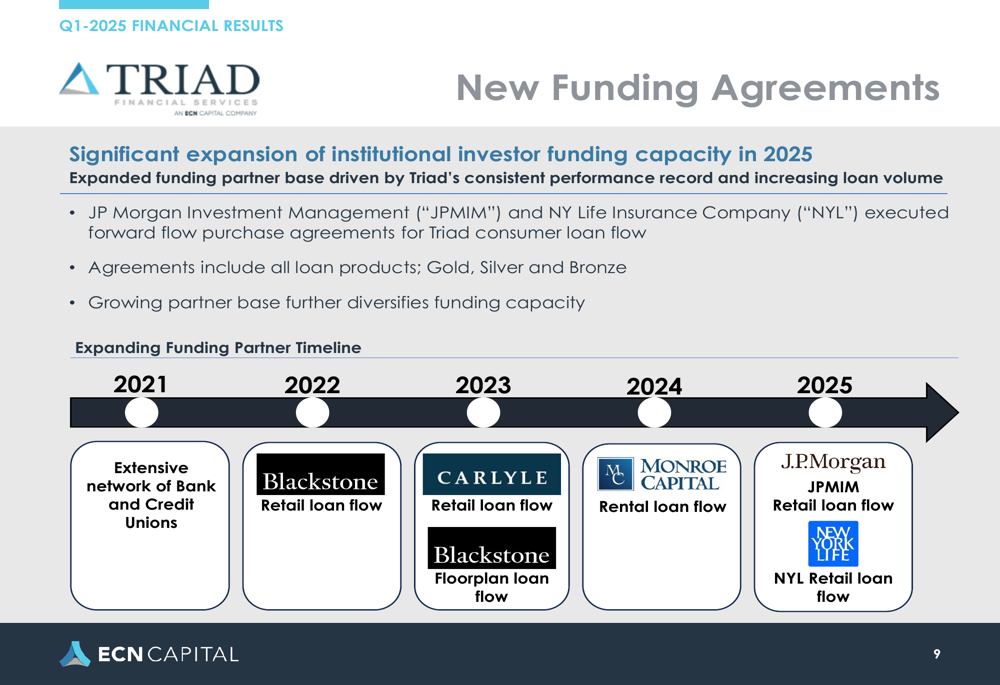

ECN Capital has significantly expanded its funding partnerships for the Manufactured Housing segment, executing new forward flow purchase agreements with JP Morgan Investment Management and NY Life Insurance (NSE:LIFI) Company. These agreements cover all loan products and help diversify the company’s funding capacity.

RV & Marine Segment Performance

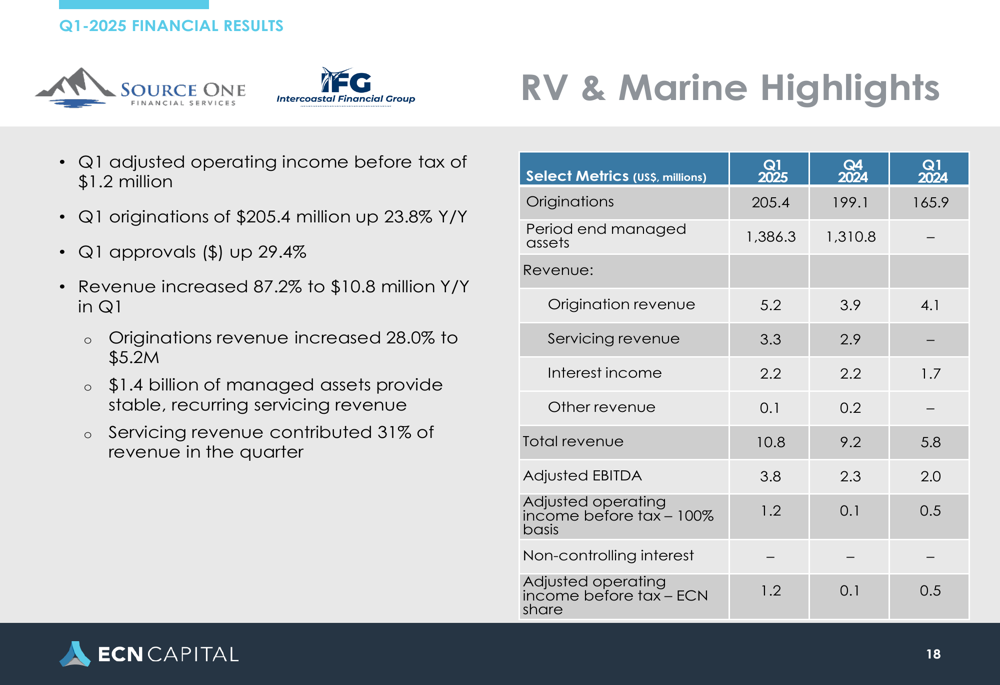

The RV & Marine segment also delivered solid results in Q1 2025, with adjusted operating income before tax of $1.2 million. Originations totaled $205.4 million, up 23.8% year-over-year, while Q1 approvals increased by 29.4% compared to the same period last year.

The segment’s revenue increased 87.2% to $10.8 million year-over-year in Q1, with origination revenues up 28.0% to $5.2 million. Servicing revenue contributed 31% of the segment’s total revenue in the quarter.

The following table provides a detailed breakdown of the RV & Marine segment’s performance:

Similar to the Manufactured Housing segment, ECN Capital has been transitioning the RV & Marine segment’s funding from banks and credit unions to institutional investors to expand volume. In March, the company completed a new funding agreement with Monroe Capital (NASDAQ:MRCC) LLC, which included an initial sale of $35.2 million and a $250 million commitment.

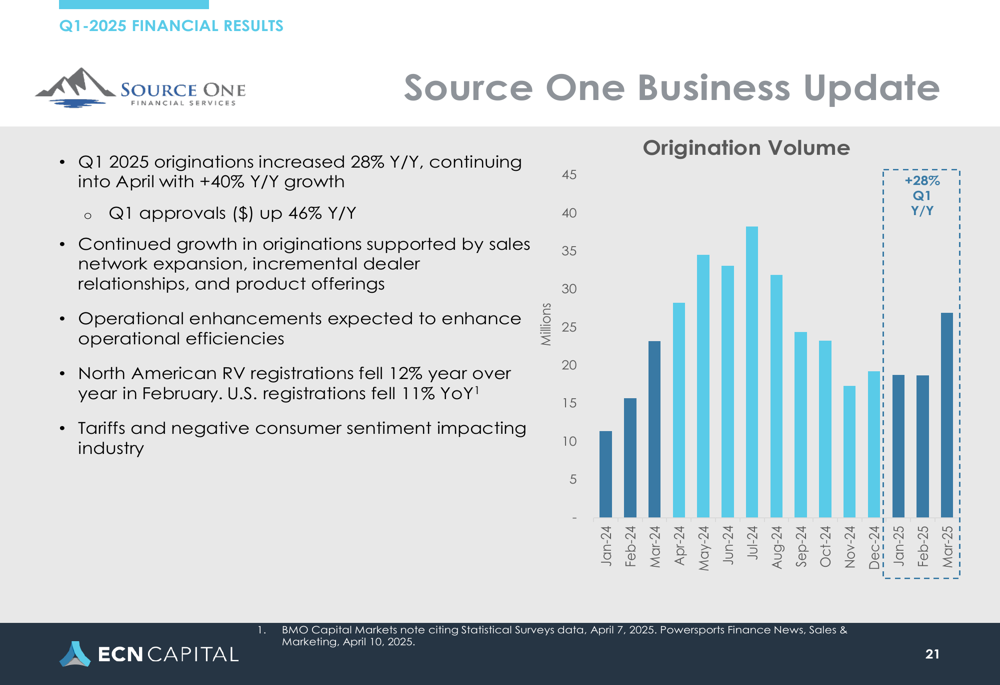

The Source One business within the RV & Marine segment saw Q1 2025 originations increase by 28% year-over-year, with growth continuing into April at a 40% year-over-year rate. This strong performance comes despite broader industry challenges, as North American RV registrations fell 12% year-over-year in February.

Strategic Initiatives and Outlook

ECN Capital has implemented several strategic initiatives to drive future growth. The company’s corporate simplification plan resulted in a one-time restructuring charge of $6.7 million but is expected to generate approximately $1 million in cost savings in Q1 alone.

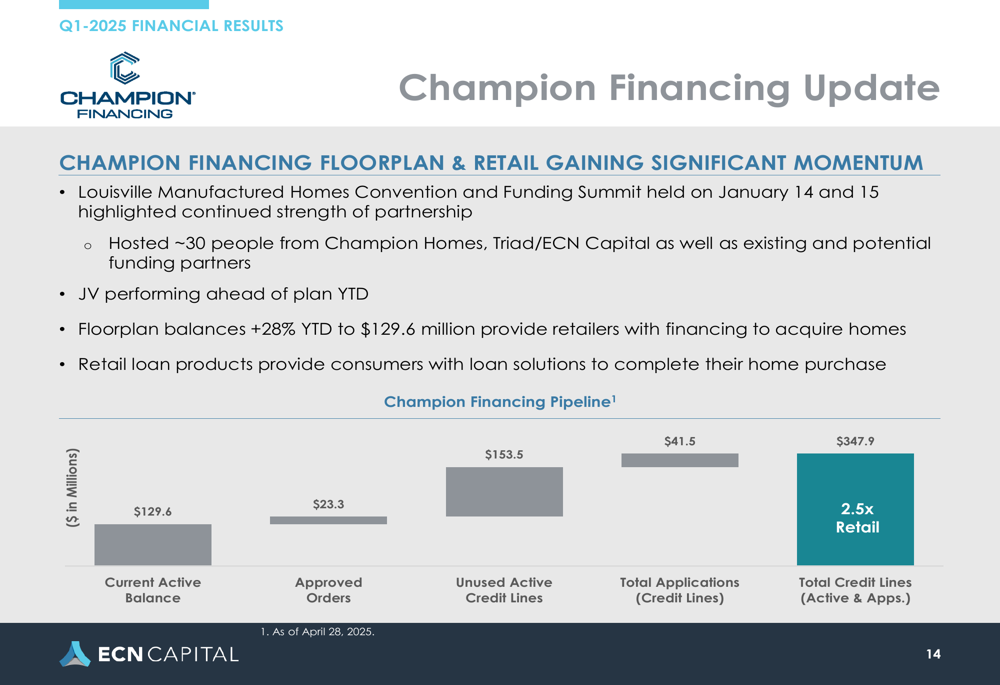

The Champion Financing joint venture is performing ahead of plan year-to-date, with floorplan balances increasing 28% to $129.6 million. This partnership, highlighted at the Louisville Manufactured Homes Convention and Funding Summit in January, brings together Champion Homes, Triad/ECN Capital, and potential funding partners to provide consumer financing solutions.

ECN Capital’s focus on expanding its institutional funding partnerships positions the company for continued growth. The transition from traditional bank funding to institutional investors provides greater capacity and flexibility, particularly important in the current interest rate environment.

In its closing summary, ECN Capital emphasized its Q1 adjusted net income per share of $0.03 at the top end of its guidance range, the addition of new funding partners in Q1 and Q2, and enhanced sales leadership and culture. The company also indicated increased guidance, suggesting confidence in its performance for the remainder of 2025.

The company’s strategy of diversifying funding sources while focusing on high-margin originations appears to be yielding positive results, as evidenced by the strong financial performance in Q1 2025. With continued expansion of institutional funding partnerships and growth in key segments, ECN Capital seems well-positioned to maintain its positive momentum throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.