S&P 500 jumps as tech rallies as investors eye end of government shutdown

Introduction & Market Context

Eidesvik Offshore ASA (EIOF) presented its first quarter 2025 results on May 13, highlighting strong operational performance amid positive market fundamentals. The Norwegian offshore vessel operator reported 100% fleet utilization and a significant increase in its contract backlog, with renewable energy projects accounting for over a third of future work.

The company’s stock closed at NOK 12.75 on May 12, up 2% ahead of the results announcement, reflecting investor optimism about the company’s performance in a market that remains strong despite some geopolitical uncertainties.

Quarterly Performance Highlights

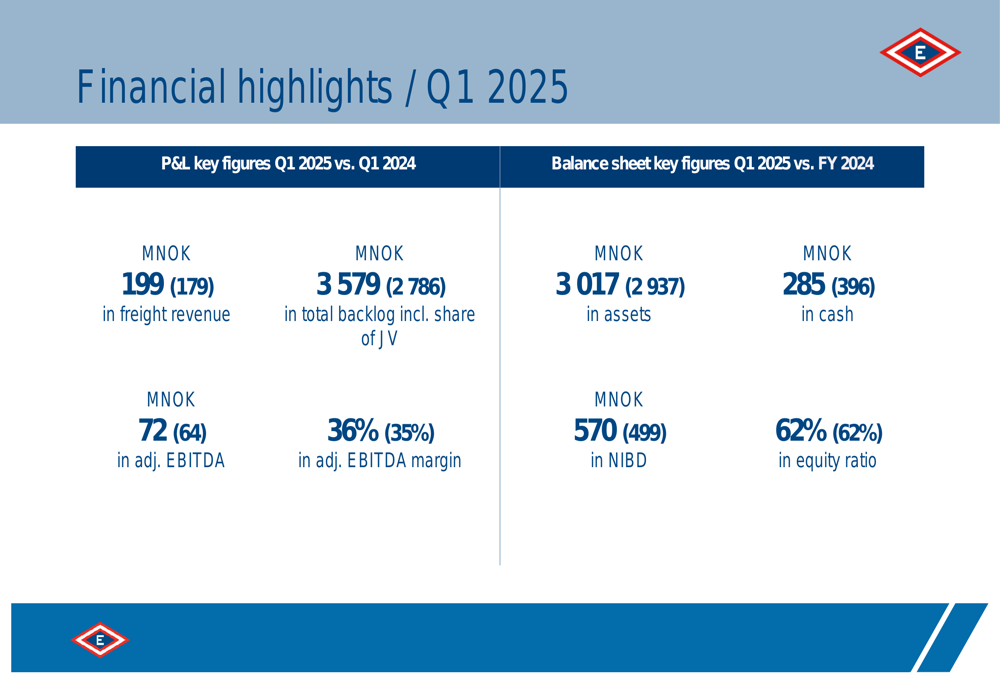

Eidesvik reported freight revenue of MNOK 199 for Q1 2025, an 11% increase from MNOK 179 in the same period last year. Adjusted EBITDA rose to MNOK 72, up from MNOK 64 in Q1 2024, with the adjusted EBITDA margin improving slightly to 36% from 35%.

As shown in the following financial highlights chart, the company maintained strong profitability while growing its backlog significantly:

The company achieved perfect fleet utilization during the quarter, with both its Supply and Subsea/Renewables segments operating at or near 100% capacity. This operational efficiency, combined with no lost time injuries (LTIs), underscores the company’s operational excellence in a demanding offshore environment.

Detailed Financial Analysis

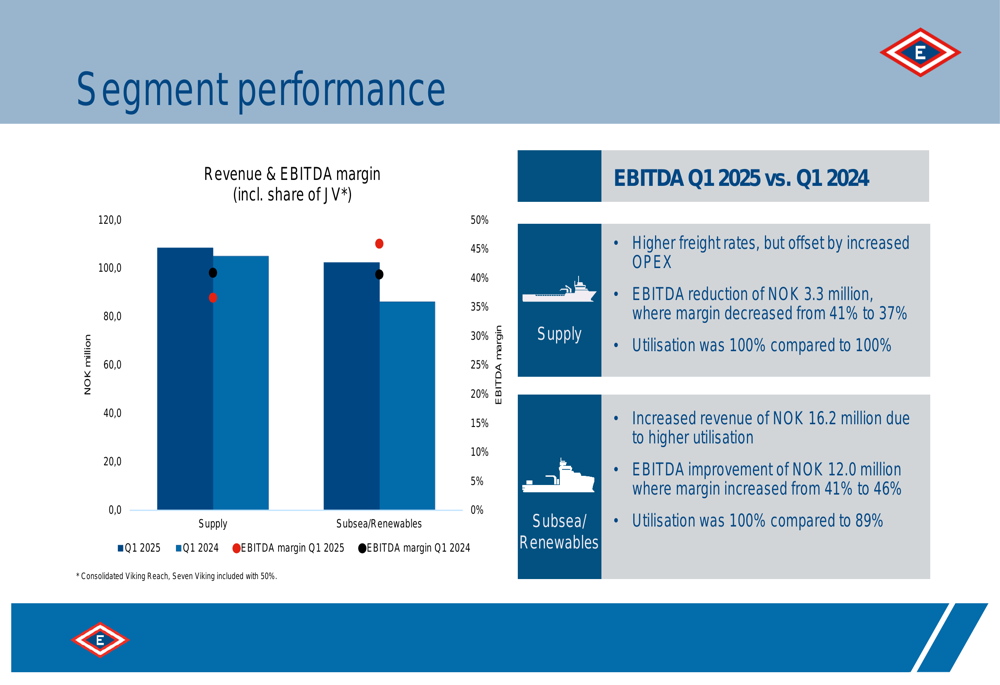

Eidesvik’s segment performance shows particularly strong growth in the Subsea/Renewables division, which saw a revenue increase of MNOK 16.2 compared to Q1 2024, along with an EBITDA improvement of MNOK 12.0. The utilization in this segment improved to 100% from 89% in the comparable period. The Supply segment maintained 100% utilization but experienced a slight EBITDA reduction of MNOK 3.3.

The following segment performance chart illustrates these trends:

The company’s balance sheet as of March 31, 2025, showed total assets of MNOK 3,017, up from MNOK 2,937 at the end of 2024. Cash and cash equivalents decreased to MNOK 285 from MNOK 396, primarily due to significant capital expenditures of MNOK 221.3 related to vessel investments. The equity ratio remained stable at 62%.

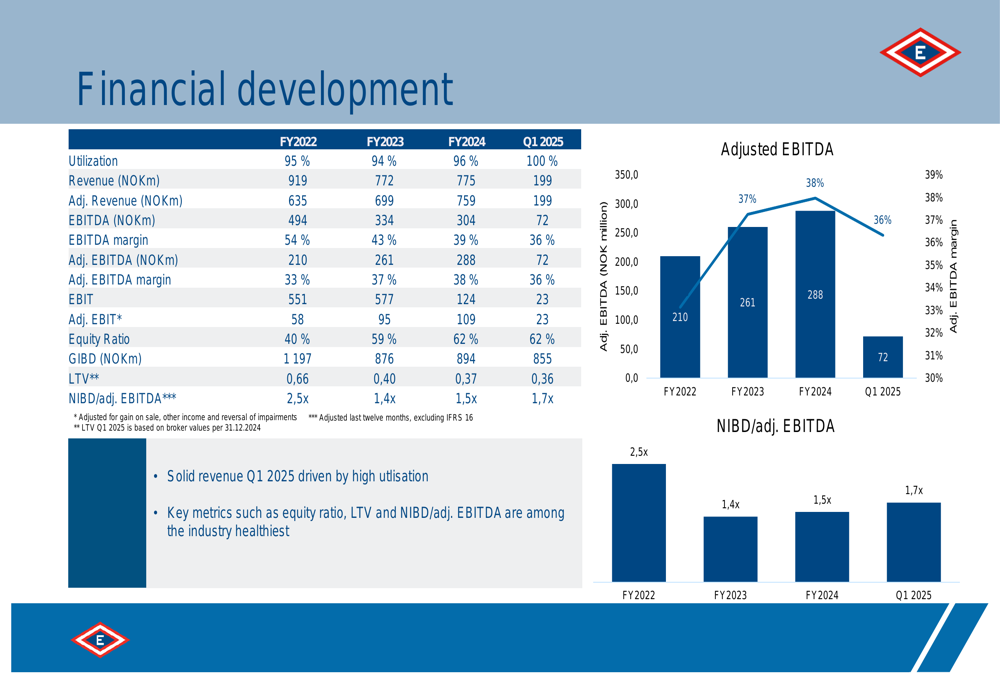

Eidesvik’s financial development over recent years shows a consistent improvement trend, with adjusted EBITDA growing and the Net Interest-Bearing Debt (NIBD) to adjusted EBITDA ratio improving from 2.5x in FY2022 to 1.7x in Q1 2025:

Strategic Initiatives

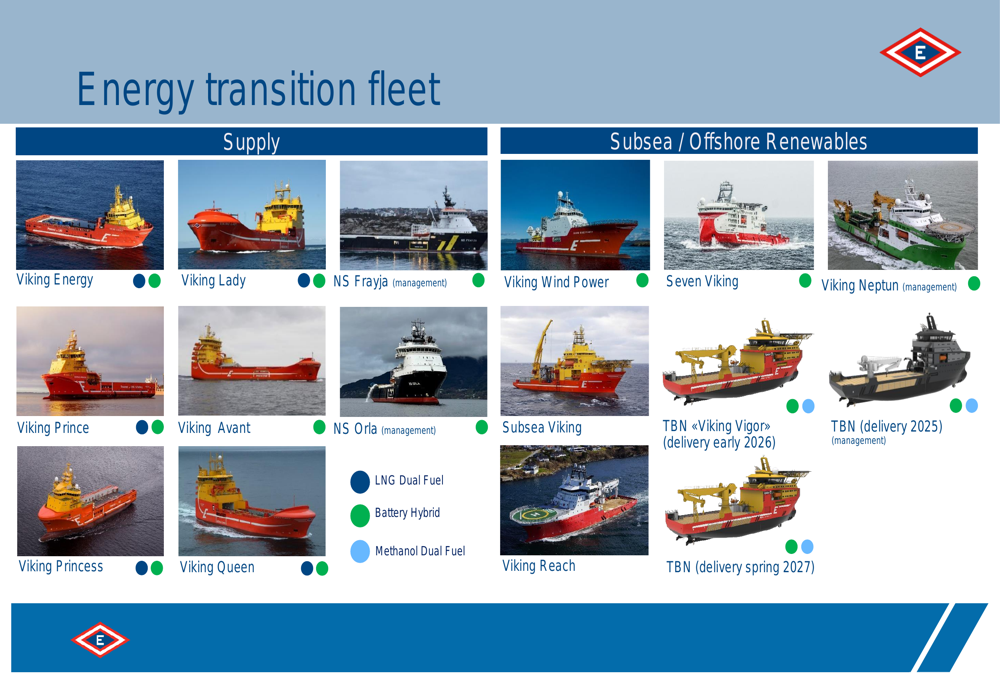

A key highlight of Eidesvik’s presentation was the announcement of a new Construction Support Vessel (CSV) being built in partnership with Agalas and Reach Subsea. The vessel, scheduled for delivery in spring 2027, will be followed by a 5-year time charter with Reach Subsea. Eidesvik and Agalas will own two-thirds of the vessel, with Eidesvik maintaining operational control, while Reach Subsea will own the remaining third.

The company also announced that Subsea7 has extended the contract for the subsea vessel Seven Viking, further strengthening its backlog.

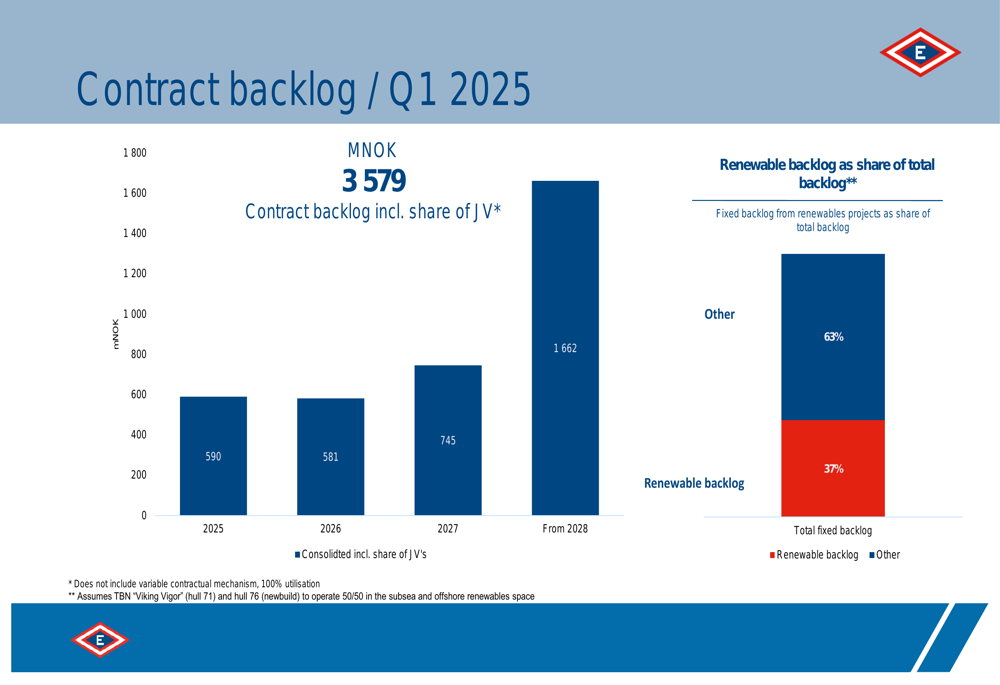

Eidesvik’s contract backlog, including its share of joint ventures, reached MNOK 3,579 at the end of Q1 2025, a substantial increase from MNOK 2,786 in Q1 2024. The backlog extends well into the future, with MNOK 1,662 scheduled from 2028 onwards. Notably, renewable energy projects now account for 37% of the total backlog, highlighting the company’s strategic shift toward greener operations.

The following chart illustrates the distribution of the company’s contract backlog:

Eidesvik continues to position itself as a leader in the energy transition, with a fleet that includes vessels powered by LNG dual fuel, battery hybrid systems, and methanol dual fuel technology. This focus on environmentally friendly vessels aligns with the industry’s move toward reduced emissions and sustainable operations.

The company’s diverse fleet of specialized vessels serves various offshore sectors:

Forward-Looking Statements

Eidesvik’s management expressed optimism about the company’s future prospects, noting that market fundamentals remain positive despite some geopolitical uncertainties. The company expects demand to continue increasing, supported by its record backlog and high vessel utilization rates in the subsea and renewables segments.

However, management did acknowledge some headwinds in the offshore wind energy sector, suggesting a nuanced approach to future growth opportunities.

The company’s debt maturity profile appears manageable, with a balanced distribution of maturities over the coming years. As of March 31, 2025, Eidesvik Agalas AS had drawn EUR 12.8 million on its construction loan for ongoing vessel projects.

Eidesvik summarized its position with five key highlights: maximum utilization, increased backlog at improved market rates, a solid balance sheet, a long-term positive outlook, and a continuing growth story. These factors position the company well to capitalize on opportunities in both traditional offshore and renewable energy markets as it continues its strategic evolution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.