Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Element Fleet Management Corp (TSX:EFN) reported solid second quarter 2025 results, demonstrating the resilience of its business model amid economic uncertainty. The company achieved 6% year-over-year net revenue growth, with adjusted EPS rising 7% and return on equity reaching 17.5%. Based on strong first-half performance, management now expects to exceed the high end of its 2025 guidance for most metrics.

Quarterly Performance Highlights

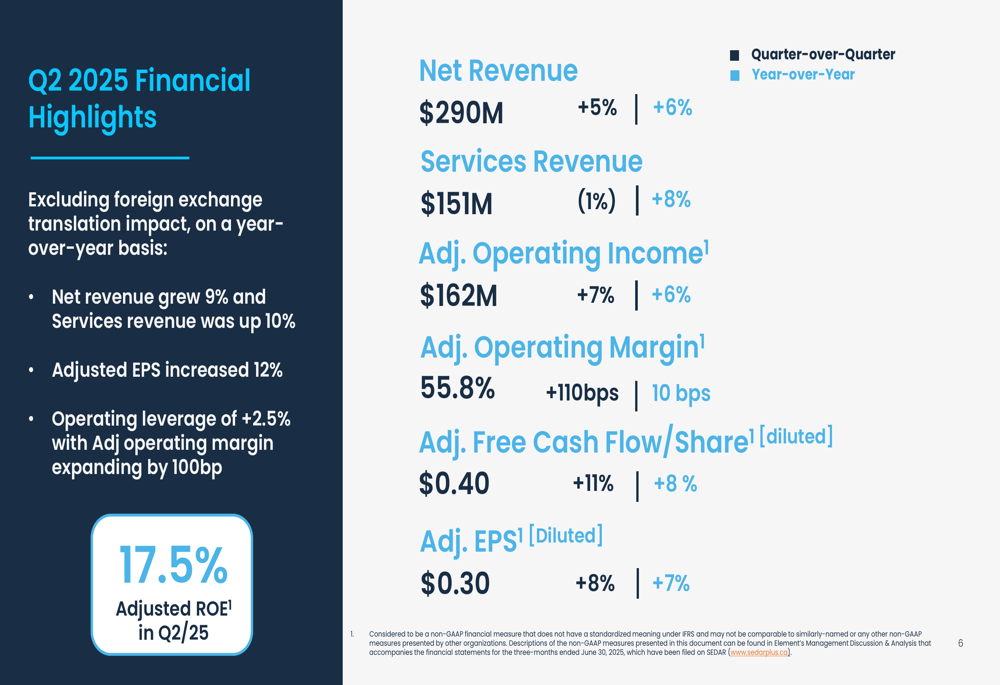

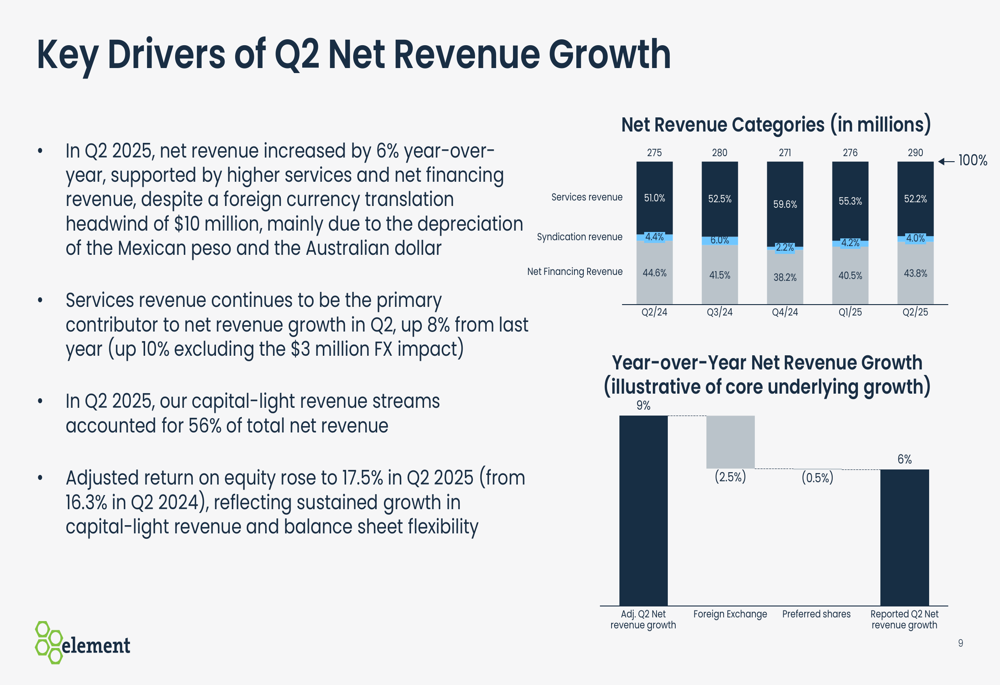

Element Fleet delivered record Q2 2025 results with net revenue growing 6% year-over-year to $290 million, despite a $10 million negative impact from foreign currency translation. Excluding this FX impact, net revenue growth was 9% compared to the same period last year.

As shown in the following financial highlights, the company achieved significant improvements across key metrics:

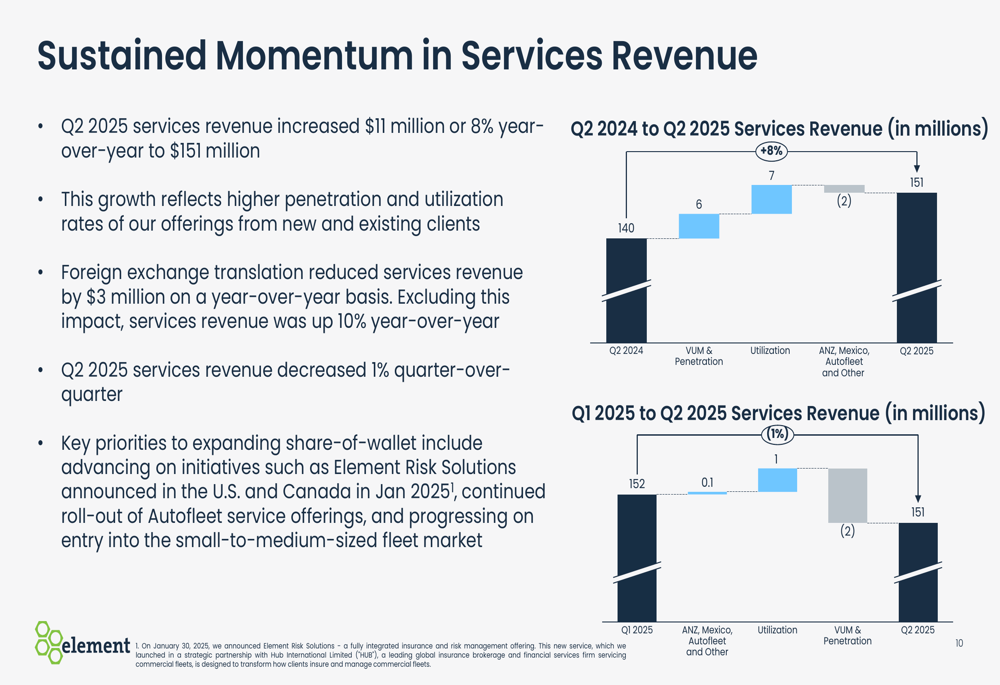

Services revenue, which continues to be the primary contributor to net revenue growth, increased 8% year-over-year to $151 million (10% excluding FX impact). This growth reflects higher penetration and utilization rates, supported by the company’s initiatives to expand share-of-wallet through Element Risk Solutions and Autofleet service offerings.

The following chart illustrates the key drivers of Q2 net revenue growth:

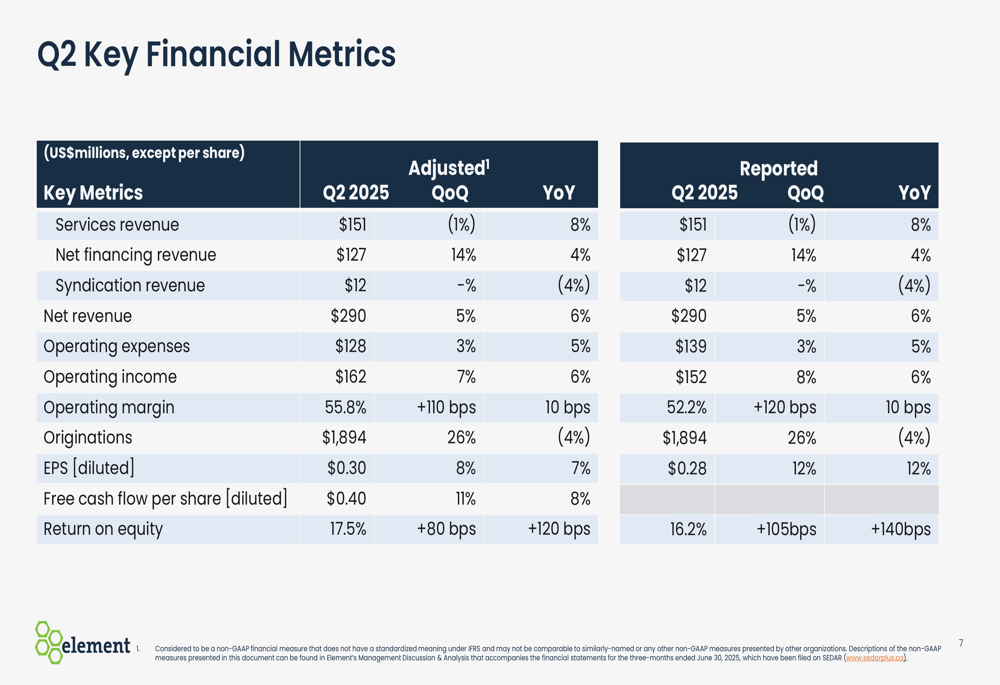

Element’s adjusted operating income rose to $162 million, up 6% year-over-year, with adjusted operating margin expanding to 55.8%. This performance generated positive operating leverage of 2.5%, as the company effectively managed operating expense growth at 5% year-over-year.

A detailed comparison of adjusted and reported financial metrics shows consistent improvement across most categories:

Revenue Growth Drivers

Services revenue momentum remained strong in Q2 2025, with growth driven primarily by higher vehicle utilization and penetration rates. The company maintained high client retention at 98% and increased service bundling to 79% of total vehicles under management (VUM).

The following chart shows the factors contributing to services revenue growth:

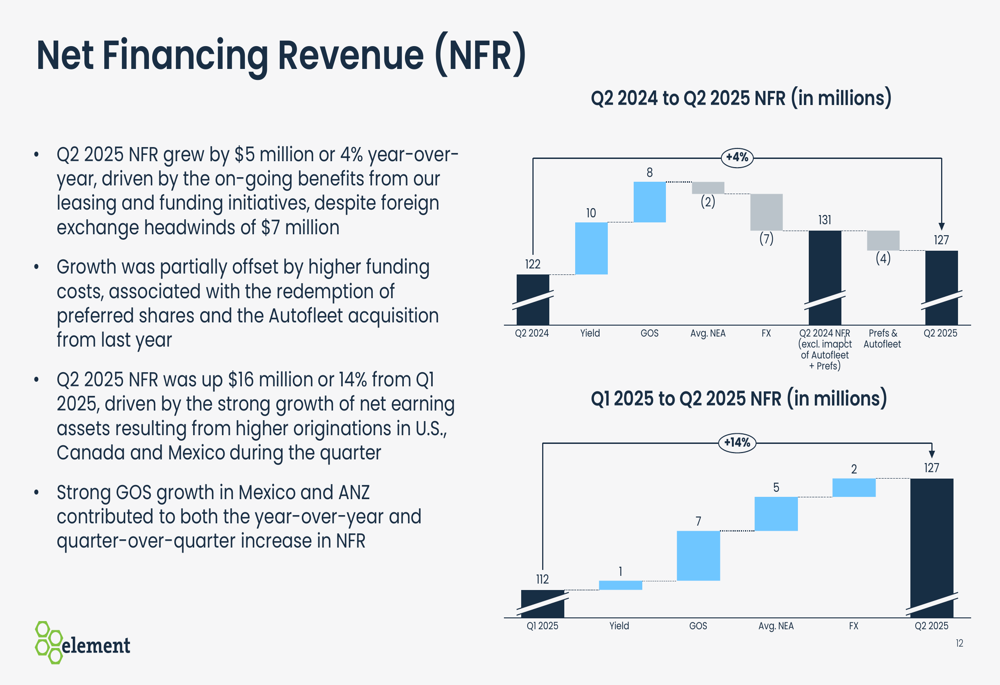

Net financing revenue (NFR) grew by $5 million or 4% year-over-year to $127 million, partially offset by higher funding costs. Quarter-over-quarter, NFR increased significantly by $16 million or 14%, with strong gains on sale growth in Mexico and Australia/New Zealand contributing to both comparisons.

As illustrated below, various factors affected the net financing revenue performance:

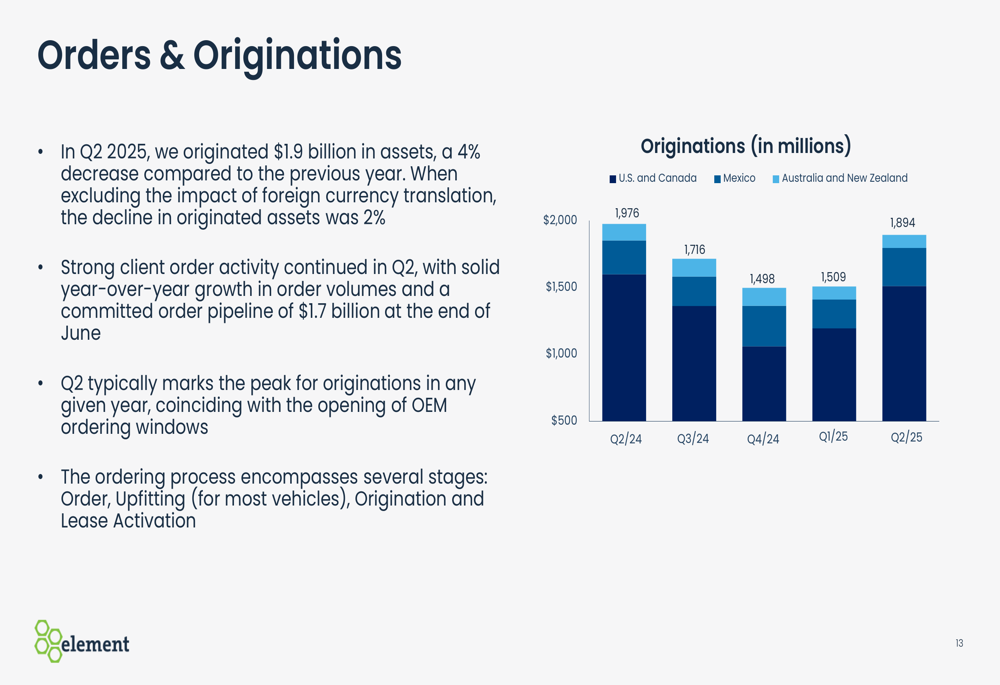

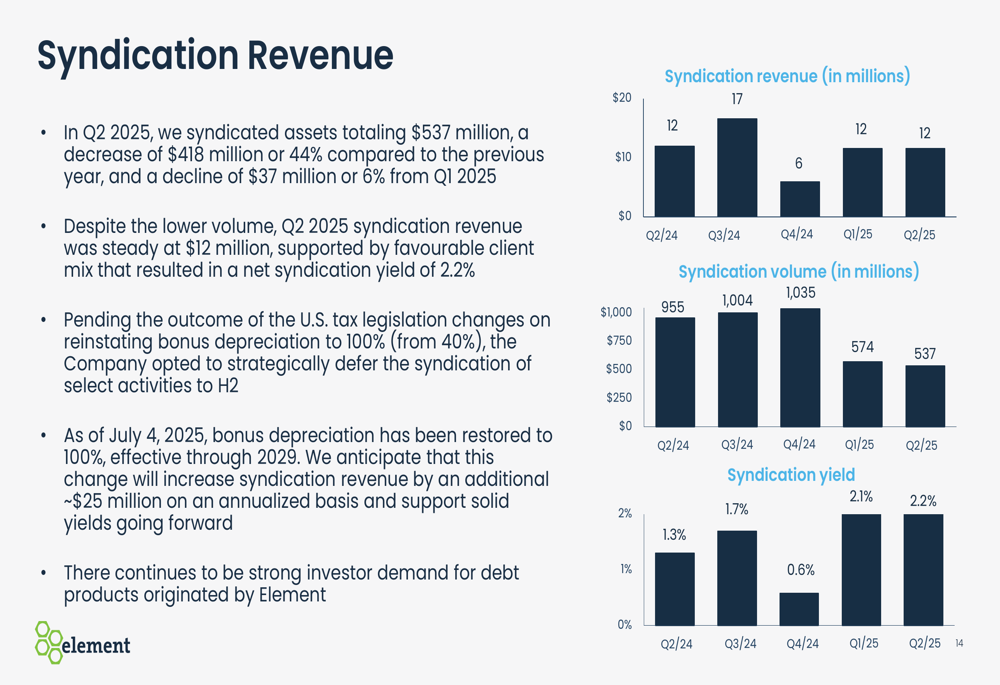

In Q2 2025, Element originated $1.9 billion in assets, a 4% decrease compared to the previous year but a 26% increase from Q1 2025. The company reported strong client order activity with a committed order pipeline of $1.7 billion at the end of June.

Financial Position and Risk Profile

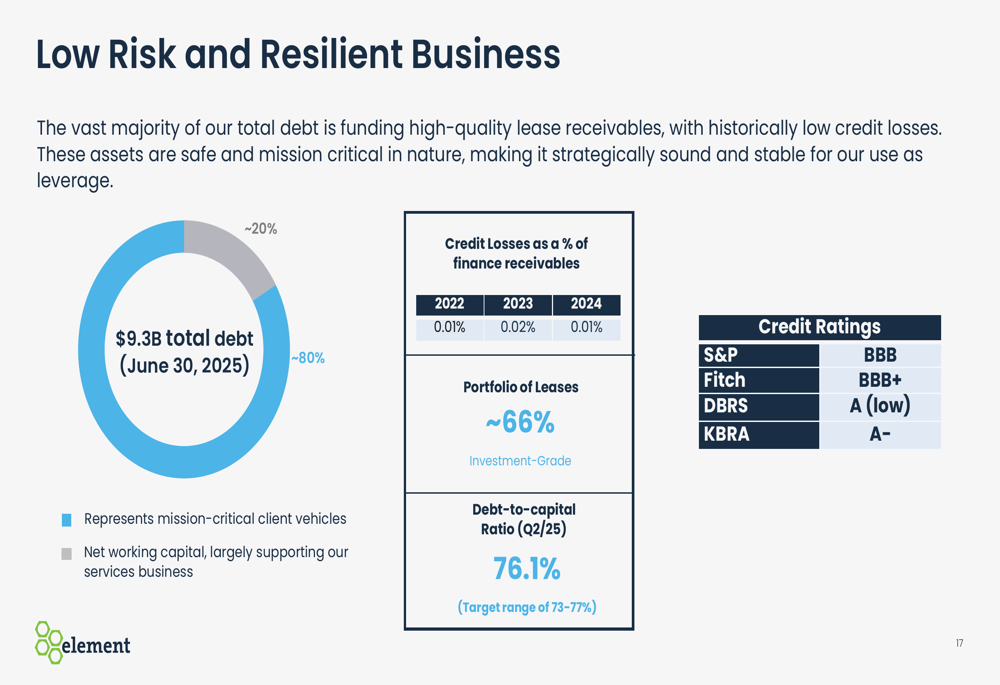

Element Fleet maintains a low-risk and resilient business model, with historically low credit losses (0.01% of finance receivables in 2024). Approximately 66% of the company’s lease portfolio is investment-grade, supporting its strong credit ratings from major agencies.

The following slide highlights the company’s solid financial position:

The company’s debt-to-capital ratio stood at 76.1% at the end of Q2, within its target range of 73-77%. Of the $9.3 billion total debt, approximately 20% represents mission-critical client vehicles, while 80% supports net working capital, largely for the services business.

Strategic Initiatives and Outlook

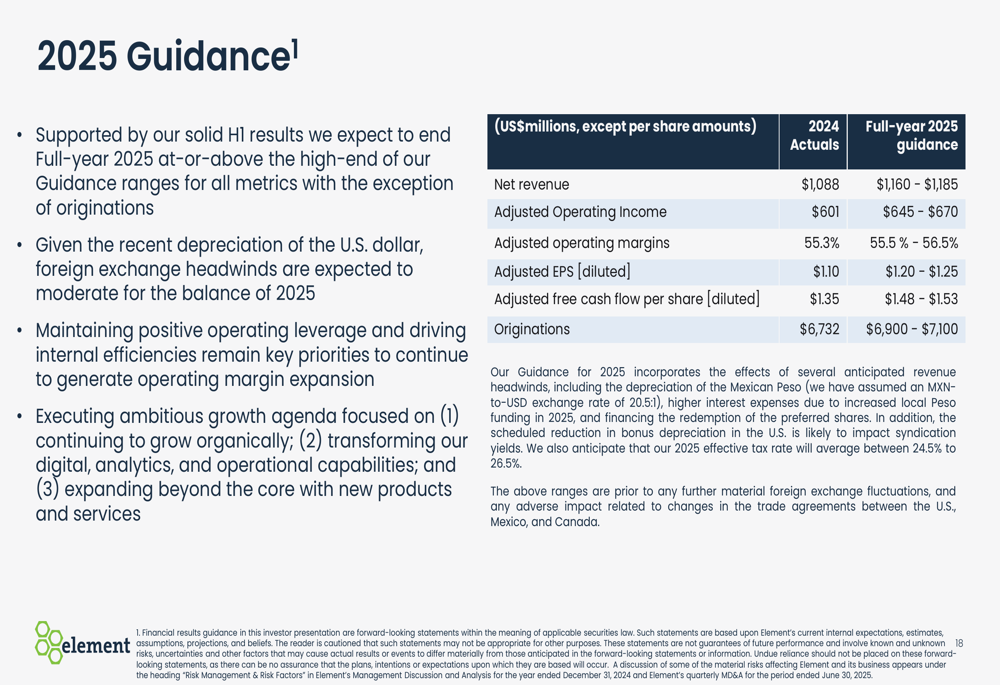

Based on strong first-half results, Element expects to end full-year 2025 at or above the high-end of its guidance ranges for all metrics except originations. The company’s 2025 guidance includes net revenue of $1,160-$1,185 million, adjusted operating income of $645-$670 million, and adjusted EPS of $1.20-$1.25.

A significant development affecting the company’s outlook is the restoration of bonus depreciation to 100%, effective through 2029, as of July 4, 2025. Element anticipates this tax change will increase syndication revenue by an additional approximately $25 million. Despite lower syndication volume in Q2, revenue remained steady at $12 million as the company strategically deferred some syndication activities to the second half of the year pending this tax legislation outcome.

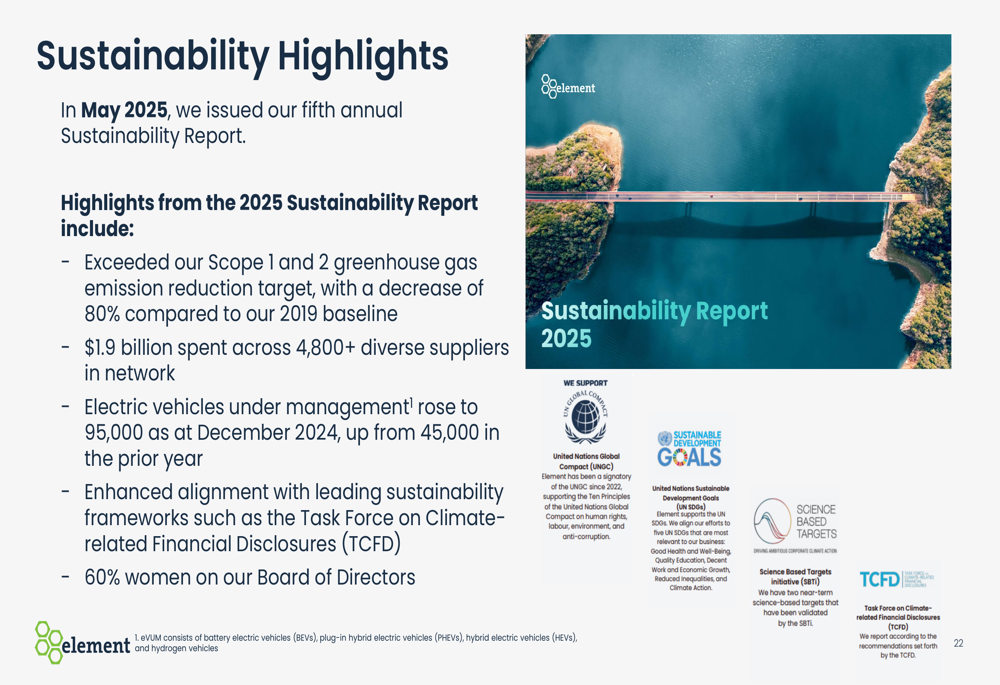

On the sustainability front, Element issued its fifth annual Sustainability Report in May 2025, highlighting significant progress in its environmental initiatives. The company exceeded its Scope 1 and 2 greenhouse gas emission reduction target with an 80% decrease compared to its 2019 baseline. Electric vehicles under management rose to 95,000 as of December 2024, more than doubling from 45,000 in the prior year.

Return of Capital to Shareholders

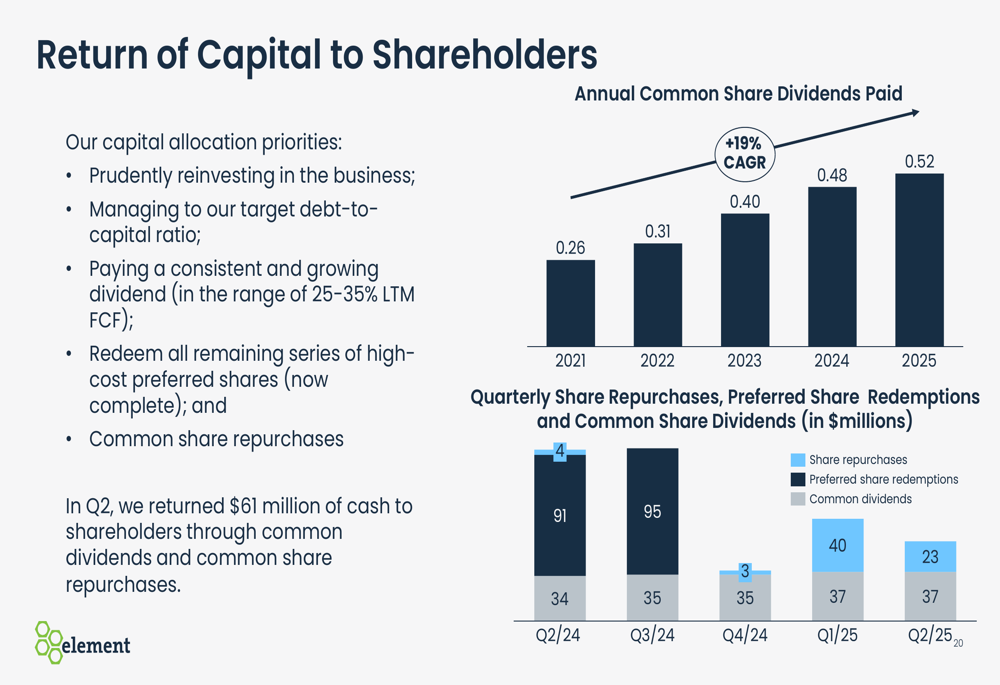

Element returned $61 million to shareholders through dividends and share repurchases in Q2 2025, representing 37% of adjusted free cash flow. The company has maintained a consistent dividend growth trajectory, with a 19% CAGR from 2021 to 2025.

Following the completion of its preferred share redemption program, Element is focusing on its capital allocation priorities, which include prudent business reinvestment, maintaining target debt ratios, paying a consistent and growing dividend (25-35% of last twelve months’ free cash flow), and common share repurchases.

The company’s adjusted free cash flow per share increased 8% year-over-year to $0.40 in Q2 2025, supporting its ability to continue returning capital to shareholders while investing in growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.